Market Mood Swings, Price Discovery & Enterprise Value

Published 27-JUN-2022 13:14 P.M.

|

26 minute read

How quickly market sentiment can change.

The start of the week was the depths of doom and gloom, with peak fear and uncertainty crushing small cap paper portfolios.

It felt like we were deep in a market rout from which there was no end in sight.

Many investors staring at crippling paper losses were sad and despondent - probably vowing never to touch the small cap stock market again...

Then all of a sudden a few small cap risk takers came in with some buying, perhaps hoping to grab an early bargain before June tax loss selling pressure stops in July.

...and many small cap stocks whose share prices had been pushed way down on low selling volumes, sprung up on equally low volumes of buying.

And the mood suddenly changed.

Paper portfolios showed signs of recovery and everyone remembered that stocks can in fact “go up” and how great the small cap market can be when it’s all green.

Positive news from the global markets also contributed to the good mood with a solid Friday session on the broader ASX.

Not to mention a stunning announcement from our 2020 Pick of the Year Vulcan Energy Resources (ASX:VUL) that was noticed by many market observers, and certainly contributed to the positive mood in the small cap space.

VUL announced a A$76M (€50M) equity investment from leading automaker Stellantis, making Stellantis VUL’s second largest shareholder - plus a 5-year extension to their lithium offtake agreement with VUL.

This news reminded the smaller end of the market that the critical metals theme IS REAL and there are big companies with serious money out there looking to secure critical metals supply.

Stellantis’ investment into VUL marks the world’s first upstream investment by a top tier automaker into a listed lithium company.

Stellantis is one of the world’s leading automakers and owns 14 vehicle brands and two mobility companies — Abarth, Alfa Romeo, Chrysler, Citroën, Dodge, DS Automobiles, Fiat, Jeep, Lancia, Maserati, Opel, Peugeot, Ram, Vauxhall, Free2move and Leasys.

After VUL released this news in the morning we watched as most other ASX lithium companies rose too.

...along with many other oversold small cap stocks.

The combination of all the factors above led to a couple of green days in the small cap space.

That’s not to say we’re blindly bullish on markets right now - the last couple weeks have seen some nasty days of selling.

And a couple of good days doesn’t mean there won’t be more pain ahead.

Holding onto all our positions through the Covid 2020 market crash ended up working out very well for us, so we decided to NOT do any selling and ride out the current crash too.

We thought it would be easy to keep a cool head as we wait for the market to recover, but we admit there have been a few nervy moments.

It’s never easy watching your paper portfolio value get destroyed (even if only temporarily), no matter how experienced you are in the small cap market or how many crashes and rebounds you have lived through.

But we said we wouldn’t be selling in June and we haven’t.

The low point for us was seeing one of our largest recent winners Galileo Mining (ASX:GAL) spike to a low of $1.055 on Wednesday this week, down from its recent highs of almost $2.

Prior to the drop on Wednesday, GAL was doing nearly all the heavy lifting in softening our paper portfolio losses from the last few months.

Even though GAL was up ~1,000% we haven’t implemented our de-risk plan yet because we believe there is much more to come in the next few months.

Seeing GAL spike down brought home the reality of just how much our overall Portfolio value is down (at this moment) in the current market down cycle.

It tested the resolve to hang on to all positions through this weak patch in the market.

Thankfully, GAL finished the week strongly, edging up on Friday to close at $1.30.

We think the share price action on GAL is symptomatic of a shift in psychology playing out in the market right now.

Namely, we think “sell in May and go away”, followed by tax loss selling in June, may be starting to give way to some bargain hunting on oversold companies.

Combine that with a very recent shift in the global mood too.

It’s far too early to say for sure, but the sellers look to have dried up a bit lately and we have seen across the board how even just a little bit of buying interest can generate big moves.

Low volume works both ways.

But sometimes a few brave souls can spark a movement. Just like some bold bargain hunting can be the start of a change in market sentiment.

We have seen some of this behaviour in the micro cap end of the market this week, with stocks rebounding off lows on very small trading volumes, but ending the trading day up 20%, 30% and even 40%.

We think this shows that anyone who wanted to sell and exit a position has likely already done so, and in the event that there is any buying pressure in a stock, there just aren't enough sellers to accommodate the new demand for shares.

It works pretty intuitively in markets.

Once all the selling is done, share prices for companies that have been hit hard become “oversold” and act almost like a “coiled spring”, where any sniff of buying translates to bigger than usual % rises.

The share price then quickly comes back to a level closer to its true value (but probably still a way off its high point).

This process is called “price discovery” and is defined by Investopedia as:

“The overall process, whether explicit or inferred, of setting including supply price or the proper price of an asset, security, commodity, or currency.

“The process of price discovery looks at a number of tangible and intangible factors, including supply and demand, investor risk attitudes, and the overall economic and geopolitical environment. Simply put, it is where a buyer and a seller agree on a price and a transaction occurs.”

In a bull market we often see price discovery happen when a company releases a great announcement.

The share price will spike up and overshoot as exuberance takes hold.

Over the next few days the share price will usually settle back lower than the spike levels and start trading around the “real price” at which investors are willing to buy and sell the stock.

Or it might settle then spike up again. It depends on the demand of buyers willing to pay higher versus the supply of sellers who can be enticed to sell at the current pricing.

The same price discovery process works during a market crash.

In a crash, prices will overshoot DOWNWARDS.

When the mood changes and buying comes back into a stock, it will quickly find its new trading range, usually higher than the initial spike down. Or, it might just keep going down.

All of this is dependent on the quality of the company and management team - plus how aggressively the stock was sold down during peak fear and uncertainty.

In an economic environment where cash is king, companies trading on low Enterprise Values are more prone to large movements when the bargain hunting mentality kicks in.

Enterprise Value is a simple yet powerful tool to understand what value the market is ascribing to a company’s projects or products at any given time, and is calculated as follows:

Enterprise Value = Market Cap + Debt - Cash

Basically it is the value of the leftover asset if you remove any debt and cash the company has in the bank - leaving the company's actual project or business value.

For example, imagine you purchase a second hand car for $10,000.

...but you find $9,000 cash in the back seat.

You have effectively “acquired” the car itself for $1,000.

(For now, let’s just ignore any questionable reasons why there might be so much cash in the back seat of a used car - it’s just an example.)

Similar reasoning applies to owning shares in a company (brace yourself for some maths).

Let’s say that company ABC owns a lithium exploration project.

ABC has 100M shares on issue and is trading at 15c, and has $5M in the bank with no debt.

15c x 100M shares give ABC a market cap of $15M.

So with $5M in the bank, the market is ascribing an Enterprise Value of $10M to ABC’s lithium project.

(Enterprise Value = $15M market cap minus $5M cash on hand.)

NOW, let’s say in the market crash ABC is trading at 6.5c.

ABC’s market cap is now $6.5M - with $5M in the bank ABC’s Enterprise Value is just $1.5M.

(Enterprise Value = $6.5M market cap minus $5M cash on hand.)

As long term investors, we think of ourselves as part owners of the COMPANY, rather than it being a financial product tradeable on an exchange.

This is why we tend to look at the Enterprise Value of a company first.

Over our 20 years of Investing, we’ve seen companies find some level of support around their cash balances. While in some more extreme scenarios when sentiment is really low (like the GFC in 2008-9), companies may even trade BELOW their cash balances.

Sometimes investors can buy a company’s shares paying close to ZERO for the potential in its projects, by definition they are getting the most upside leverage to the company’s success.

Of course, the caveat here is that just because the company is trading with a low enterprise value it doesn't make it a great investment opportunity.

We look at these as preliminary filters - all it does is make us interested enough to take a closer look at a company.

We will always look at the management team and the quality of a company’s project/prospects before making an Investment decision, and place the most emphasis on this.

After all, it is company management who will be the stewards of the cash a company holds in a bank account, ultimately choosing where cash gets deployed and in what manner.

The trick is in finding high quality projects and high calibre management teams for as low an Enterprise Value as possible.

The “high quality project” part can make this difficult. Investors will hold onto their shares, even in a downturn, if they think the company’s prospects are unaffected by the macro issues causing a temporary share price sell off.

It's a fine balancing act and not an exact science, but it's a great place to start the wider due diligence process.

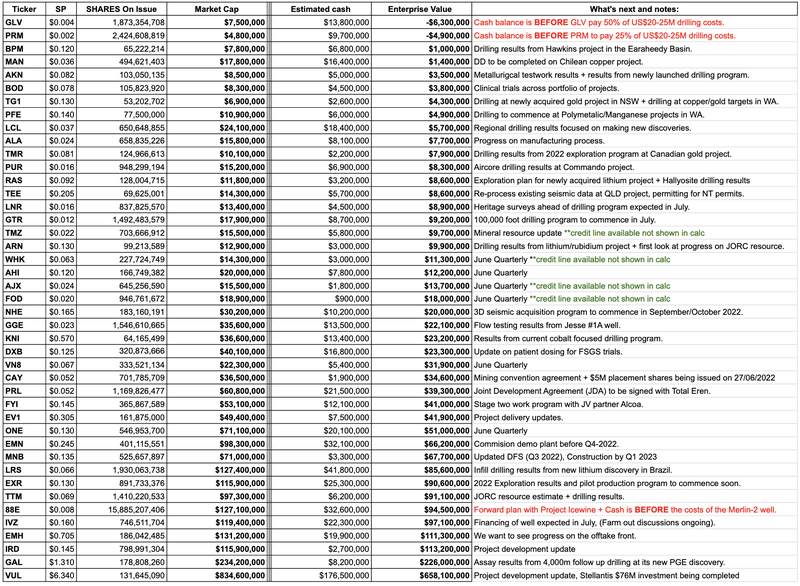

As part of our Portfolio-wide review, we have reviewed Enterprise Values and cash positions at June 24 2022 for all our Investments - you can view our internal spreadsheet here.

* Please note that these are just our rough estimates of cash and enterprise value. Given how late we are in the June quarter, a lot of our Portfolio companies are likely to have used up a portion of this cash so this will not be 100% accurate. Please also note that these market caps are not fully diluted. The numbers in the screenshots below and our spreadsheet are just a rough guide and should NOT be relied upon to make any decisions.

Some notable mentions based on this list:

BPM Minerals (ASX:BPM)

BPM is currently trading at an Enterprise Value of just ~$1M with $6.8M cash in the bank.

This comes after the company recently completed a recent $3M capital raise at 21c per share, with the company now trading well below that level.

BPM is in the middle of its maiden drilling program at the Hawkins Project - the primary reason for our Investment in the company.

With that major drilling program underway and results likely to start coming through over the next few months, we think the $1M Enterprise Value provides for good leverage if BPM does in fact hit anything of interest.

TechGen Metals (ASX:TG1)

TG1 is trading with an enterprise value of just $4.3M.

This is ahead of drilling at both its newly acquired gold project in NSW and its copper/gold targets in WA.

We covered all of the target generations works across TG1’s projects in a recent note we put out which you can read here: Microcap TG1 pinpoints gold drill targets

With several drilling programs coming in the back end of the year, TG1 again offers heaps of leverage to a successful discovery given the current enterprise value.

Pantera Minerals (ASX:PFE)

PFE is another junior explorer that is trading at a low enterprise value of just $4.9m.

Again, PFE is heading into a busy exploration period with drilling at its Hellcat polymetallic project and its manganese project in WA.

Earlier this week we did a deep dive into why we like the way these drilling programs are shaping up. You can read that note here: Pantera Drilling Next Month. $7.8M Market Cap. $5.8M Cash. $2M Enterprise Value

GTI Energy (ASX: GTR)

GTR is currently trading with an enterprise value of just $9.2M.

Its share price is down almost 50% following its recent $5M capital raise which was priced at 2.1c per share.

GTR is due to kick off a 100,000-foot drilling program across its uranium project in Wyoming, USA in July. This comes amid news that the US government is looking at shoring up domestic supplies of uranium to safeguard its nuclear power industry.

GTR is another company in our Portfolio that may be in a position to announce company-making news over the next few months, with an EV that is highly leveraged to good news.

Tempus Resources (ASX: TMR)

TMR is currently trading with an enterprise value of just $7.9M.

The company has kicked off its 2022 exploration program at its gold project in Canada, with visible gold already intercepted in the first few drill holes.

TMR is looking to extend the “Blue Vein” discovery it made last year, as well as targeting new discoveries with the ultimate aim of getting its project back into production.

With assays pending from the visible gold intercepts and heaps of drilling newsflow to come over the coming months, TMR is again valued at a level where any good news could lift the company’s share price.

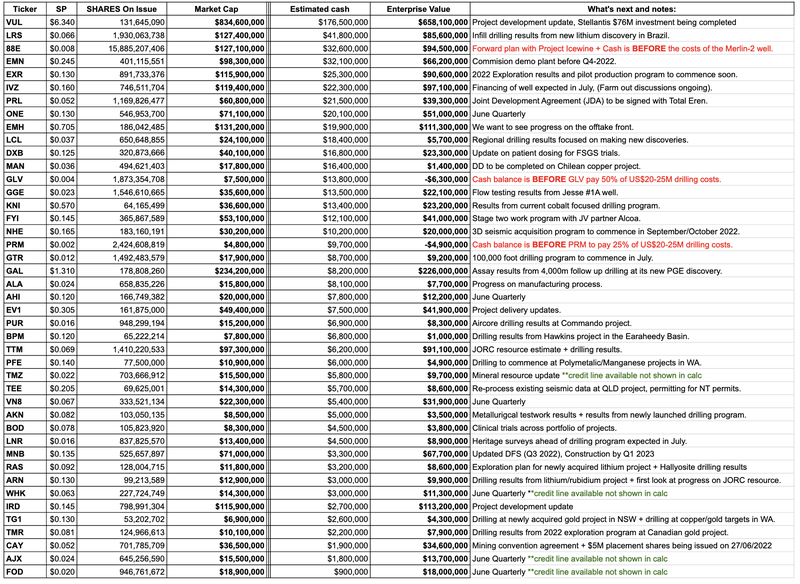

Companies with strong balance sheets - lots of cash

A second filter we ran through was to check which of our Portfolio companies are sitting on large cash balances.

For a long time, cash was easy to come by and so there was little value ascribed to a company’s cash balance. Things are a lot different now.

In a down market where it’s hard to raise new capital - cash is king.

If the rough market continues over the medium term, currently cashed up companies will be the best placed to thrive.

Strong balance sheets and heaps of cash in the bank gives companies optionality.

By ‘optionality’ we mean it gives the company the ability to finance its business objectives and allows it to look at opportunities that may not have been available when valuations were much higher.

A strong balance sheet also means that a company can invest in its business at a time when other businesses’ are cutting back expenditures, effectively giving the company a leg up over it’s competitors.

Below are our Portfolio companies sorted from largest cash balance to smallest:

* Please note that these are just our rough estimates of cash and enterprise value. Given how late we are in the June quarter, a lot of our Portfolio companies are likely to have used up a portion of this cash so this will not be 100% accurate. Please also note that these market caps are not fully diluted. The numbers in the screenshots below and our spreadsheet are just a rough guide and should NOT be relied upon to make any decisions.

Some notable mentions based on this list:

Vulcan Energy Resources (ASX:VUL)

VUL had ~€116M (A$176M) in cash at the end of the March quarter.

This comes before its announcement on Friday confirming that upstream automaker Stellantis agreed to invest a further $76M at A$6.662 per share.

This would bring VUL’s cash balance to more than $250M while providing direct backing from the €38 Billion capped Stellantis.

Not only does VUL have heaps of optionality, but the financial firepower to progress the development of its Zero Carbon Lithium Project.

At the same time VUL can also pour capital into its unique R&D exposures, all at a time when other companies would be cutting back on these types of expenditures in favour of preserving cash.

Latin Resources (ASX: LRS)

By our estimates, LRS has around $41M cash in the bank.

This comes after it completed a $35M raise at ~16c per share earlier in the year and from the exercise of in-the-money options.

We think the LRS team got the capital raise spot on, raising at an almost 150% premium to the current share price.

This means LRS can continue progressing the drilling programs at its new discovery and focus on building up its project, instead of having to go into cash preservation mode in a rough market.

With infill drilling ongoing at its new lithium discovery in Brazil, we hope to see a JORC resource before the end of the year and think that LRS can flex its financial muscle to get this done.

Los Cerros (ASX:LCL)

LCL is a rather unique proposition, with its ~$18M cash balance.

LCL is one of those stocks that comes up on both the low enterprise value filter as well as the strong balance sheet filtering process of our overall Portfolio review.

With its $18M cash balance and a market cap of only $24.1M the company trades with an enterprise value of just $5.7M.

This means that we are effectively getting exposure to its existing JORC resource base and exposure to new discoveries for $5.7M.

Not only does LCL already have well defined JORC gold resources of 2.6 million ounces, but the company is also actively drilling across its regional targets, which could grow the overall size of its project with entirely new discoveries.

With $18M in cash in the bank and well defined JORC resources, LCL is currently being valued at levels that we are used to seeing in early stage explorers with far less advanced projects.

We think the levels the company is trading at have more to do with the overall market sentiment and that the gold sector as a whole is seriously unloved.

Mandrake Resources (ASX:MAN)

MAN ended the March quarter with $16.4M cash in the bank.

Coupled with its low enterprise value of only $1.4M, it is one of the companies in our Portfolio that has a serious amount of optionality with respect to where it deploys its massive cash balance.

MAN actually picked up an interesting copper project recently, which is still going through the due diligence process. We covered that acquisition in our last MAN note - you can read it here: Cashed up MAN picks up high grade Chilean copper asset

When/if the acquisition is complete, we expect to see MAN put its cash balance to use and get drilling.

And if a new discovery is made, MAN can throw even more cash at the project to quickly test just how big it could be.

Again, MAN is another one of our Portfolio companies that comes up on both the low enterprise value filter as well as the strong balance sheet filter.

Oneview Healthcare (ASX:ONE)

ONE held ~€11.8M (A$18M) in cash at the end of the March quarter and received a further $2M from a legal settlement bringing our estimate for its cash balance to ~$20M.

This comes after ONE managed to pull off a A$20M capital raise in November at 27c per share.

We especially like that ONE did its capital raise at a time where market sentiment was still strong (right before the US tech crash) and at an almost 100% premium to where the company’s share price is trading now.

ONE is now uniquely positioned to be able to execute its growth strategy and can invest in the business on an “as needed” basis instead of having to cut back on growth expenditure at a time when capital is harder to come by.

Again this investment into ONE’s growth strategy will be able to happen at a time when other companies may be holding back on investment in growing their business’.

Another major positive here is that ONE is also revenue generating meaning its cash balance will last the company for a lot longer than say a junior explorer.

Elixir Energy (ASX:EXR)

EXR ended the March quarter with $25.3M cash in the bank.

Perhaps one of the most currently underappreciated companies in our Portfolio, EXR’s last capital raise was done in April 2021 close to the peak of the market at 36c per share.

EXR is now trading at 13c per share and still has enough cash on its balance sheet to operate the business for multiple years, in its most recent quarterly it put that number at 9 quarters of cash burn, meaning it could technically go without having to raise for over 2 years.

EXR isn't just sitting on this cash pile either, the company is currently in the middle of its 2022 drilling program across its coal bed methane (CBM) gas project in Mongolia.

Whilst exploration drilling continues, EXR has also started preparations for its much anticipated long term production testing program at the project now scheduled for August 2022. That program should ultimately determine whether or not EXR can produce commercially viable rates of gas from its project.

But that isn't the only thing EXR is progressing, its large cash balance has also seen it opportunistically start putting together the initial pieces to a potential company making green hydrogen project in Mongolia.

So far it has the Mongolian government in its corner and earlier this week announced that it had managed to sign a Memorandum Of Understanding (MOU) with a subsidiary of Softbank (Yes that Softbank) to progress the project.

With heaps of cash in the bank and two projects being progressed at the same time, we are looking forward to the next few months as EXR shareholders.

Province Resources (ASX:PRL)

PRL ended the March quarter with $21.5M cash in the bank.

PRL is another one of our Portfolio companies that managed to raise $18M at 15c per share near the peak of the positive market sentiment in May 2021.

With PRL now trading at 5.2c per share, that raise was done at almost 3X its current share price.

The strength of PRL’s balance sheet is especially important because of the type of project it is trying to develop.

PRL is progressing its green hydrogen project and has a Memorandum Of Understanding (MOU) signed with major renewable energy player Total Eren.

With other energy majors inking deals in the green hydrogen space we are looking forward to PRL signing its Joint Development Agreement (JDA) with Total Eren - the due date for this is now set at 31 July 2022.

The green hydrogen sector reminds us a little bit of the early days of the lithium run, where downstream capacity is being developed but not yet up and running.

We think that it is less about if and more about when this happens.

With its strong balance sheet PRL has plenty of cash to keep moving its project closer towards being development ready.

In Summary

This is just a rough scan we have run across our Portfolio companies in a down market.

While the market has had a couple of good days, there could be more pain ahead so Enterprise Values may still come down even more.

There are now only four trading days left in “tax loss selling” June. We hope the global mood stays positive into the first week of July, but are also mentally prepared for more rough waters.

With all of this in mind, below is a list of our Portfolio companies with upcoming potential major catalysts.

⏲️ Upcoming potential share price catalysts list

Results expected in the near term:

- GGE is drilling its maiden helium well in Utah where it’s aiming to make a commercial helium discovery (memo).

- IN PROGRESS: GGE’s maiden drilling program is complete with a ~203 foot (~62 metres) gas bearing column intercepted.

- Update: This week we saw GGE stimulate its Jesse #1A well ahead of the flow testing program. We covered this in a Quick Take which can be read here: Stimulation work completed, flow testing next. We hope to see flow testing results at some point over the next two weeks.

- PRL signing a Joint Development Agreement with its partner, Total Eren, to materially de-risk its WA Green Hydrogen Project (memo)

- IN PROGRESS: The signing of the “Joint development agreement” (JDA) with TotalEnergies. PRL’s deadline to sign the JDA is now set at 31 July 2022.

- Update: No updates on this front this week.

- IVZ to drill its giant gas prospect in Zimbabwe - we have been waiting two years for this event (memo).

- IN PROGRESS: Drilling is scheduled for July. IVZ says it is considering three separate farm-in offers.

- Update: No updates on this front this week.

- KNI to drill its cobalt targets in Norway (memo).

- IN PROGRESS: KNI confirmed has completed ~1,007 metres of its total ~2,800m drilling planned. We covered the update in a Quick Take in late-May - read here.

- Update: No update on this front this week.

- BPM to drill its lead zinc prospect in the Earaheedy Basin close to Rumble Resources’ recent discovery (memo)

- IN PROGRESS: BPM is completing a ~7,500m AC/RC drilling program at its Hawkins project (along strike from Rumble’s discovery).

- Update: After brief delays due to unseasonal rainfall in the Pilbara, BPM restarted its drilling program this week. We put out a Quick Take on that announcement - read here: Earaheedy basin drilling along strike from Rumble restarted

- LNR (formerly FNT) commencing drilling for rare earths (memo)

- IN PROGRESS: LNR is still in the process of getting approvals so we are not sure exactly when drilling will occur. It may be later than most on the above list, but we are keeping an eye on progress.

- Update: No progress has been made this week.

🗣️ Quick Takes

Here are this week's Quick Takes:

VUL: Stellantis to become a substantial shareholder, invests $76M

BOD: BOD to launch low dose CBD schedule 3 product

GGE: Stimulation work completed, flow testing next

ARN: Purple specs of lithium intersected at lithium/rubidium project

AKN: Updated investor presentation

TMZ: Mt Carrington restated MRE gets TMZ close to 100Moz target

AKN: Flagship base metals project progress update

BMP: Earaheedy basin drilling along strike from Rumble restarted

EXR: Extended pilot production program planned for August 2022

EXR: New coal bearing sub-basin discovered, more drilling to come

GTR: US based director with uranium experience appointed

FOD: FOD signs deal with Costco and expands distribution with Woolies

FOD: FOD launches new products: Veggie Goodness and Calm shots

Gas Macro: Gas to bridge the gap between fossil fuels and renewables

Hydrogen Macro: Tsunami of capital coming into the green hydrogen sector

📰 This week on Next Investors

Four wells to be drilled in the Beetaloo in coming months - TEE paying attention

On Thursday we took a look at Top End Energy’s (ASX:TEE) prospects in light of what its gas neighbours are up to in the Beetaloo Basin.

TEE holds a 50% interest in no less than 30 different permits covering over ~162,000km2 in the Northern Territory with exposure to five key basins prospective for gas — the McArthur Basin, Wiso Basin, Georgina Basin, Murraba Basin, and the Amadeus Basin.

📰 Read our full Note: Four wells to be drilled in the Beetaloo in coming months - TEE paying attention

EXR Inks Green Hydrogen MoU with a SoftBank Subsidiary

This was a big one for EXR this week - EXR surprised us and the market by signing an MoU to develop its green hydrogen project with SoftBank subsidiary SB Energy.

SoftBank is a massive Japanese multinational investment conglomerate and EXR will work with SB Energy to advance its project in Mongolia, with significant implications for renewable energy in Asia.

📰 Read our full Note: EXR Inks Green Hydrogen MoU with a SoftBank Subsidiary

NHE Awards 3D Seismic Contract - Helium Shortage Persists

On Wednesday, we talked about how our helium Investment, Noble Helium (ASX:NHE) fits into “Helium Shortage 4.0”.

We also delved into NHE’s latest step towards hopefully proving a massive prospective helium resource in Tanzania - awarding a 3D seismic contract ahead of its Q3 2023.

📰 Read our full Note: NHE Awards 3D Seismic Contract - Helium Shortage Persists

Pantera Drilling Next Month. $7.8M Market Cap. $5.8M Cash. $2M Enterprise Value

On Thursday, we had a look at next month’s drilling for our multi-commodity explorer, Pantera Minerals (ASX:PFE).

As of Thursday, PFE had a market cap of $7.8M, so the company was trading with a very small enterprise value (EV) of $2M, which may have been reflective of PFE’s shift away from its iron ore project.

We examined the merits of PFE’s Hellcat project which is just down the road from one of the Edmund Basin’s most significant discoveries — the ‘Abra’ polymetallic deposit that’s being developed by ASX-listed Galena Mining (a company capped at $76M - about 10 times that of PFE).

In our update we forgot to mention that we had participated in the recent PFE rights issue. This means that our Shares Held in PFE now include 227,500 PFE Options - this has been updated on the disclosure on our website.

📰 Read our full Note: Pantera Drilling Next Month. $7.8M Market Cap. $5.8M Cash. $2M Enterprise Value

Visible gold to kick off the new drilling season

On Wednesday we checked in on our gold Investment Tempus Resources (ASX:TMR).

Drilling started three weeks ago and after three diamond drill holes at the high grade Blue Vein discovery, TMR has already delivered visible gold intercepts in its drill cores.

Our big bet with TMR is that it can become a medium term gold producer - we have been holding TMR for over two years now, hoping that it can discover enough new high grade gold veins at its Canadian project to restart the existing and permitted gold mill.

📰 Read our full Note: Visible gold to kick off the new drilling season

GAL Hits Sulphides on Every New Hole

Earlier in the week our long term exploration Investment Galileo Mining (ASX: GAL) gave us a first look at its next round of drilling at its newly discovered PGE deposit at its Norseman Project.

On Tuesday, GAL confirmed that all four of the newly drilled holes had intersected more sulphides, with each hole stepping 50m further east of the discovery hole and the discovery now interpreted to extend over at least 250m of strike.

This drilling will run for a further four weeks with 16 more drillholes planned. Assays from the first four holes are due at some point in July.

GAL has already commissioned a second drill rig to speed up the drilling program, so we expect to see plenty of newsflow by way of drilling results and assays over the coming weeks/months.

📰 Read our full Note: GAL Hits Sulphides on Every New Hole

📰 This week in our Portfolios 🧬 🦉 🏹

🏹 Wise-Owl

Key Engineering Appointment – Following the Syrah Playbook

On Tuesday our 2021 Wise Owl Pick Of The Year, Evolution Energy Minerals (ASX: EV1), took another step toward developing its shovel ready, graphite project in Tanzania.

EV1 progressed the development of its project by appointing a “front end engineering and design” (FEED) contractor.

📰 Read our latest full Note: Key Engineering Appointment – Following the Syrah Playbook

Have a great weekend,

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.