Invictus Energy (ASX:IVZ) is an oil and gas exploration company drilling one of the largest un-tested gas prospects in Zimbabwe’s Cabora Bassa basin.

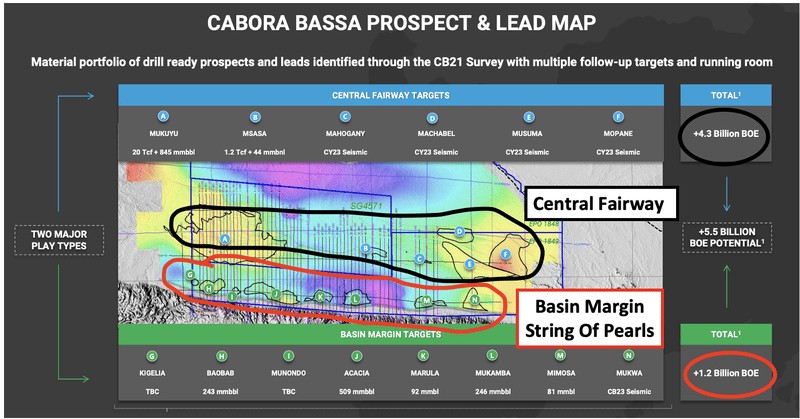

IVZ’s project has a total 5.5BN barrel oil equivalent prospective resource estimate.

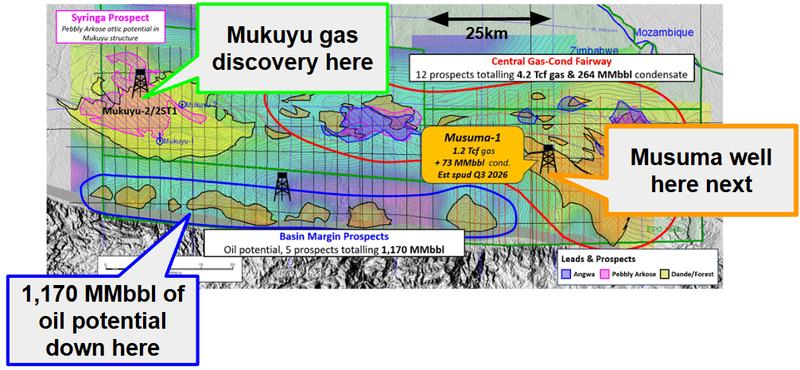

(~20tcf gas, 845MMbbl gas condensate plus 1170MMbbl)

What is the macro theme?

Oil & gas is back on the market's radar after a couple of sleepy years.

Small cap O&G explorers are catching bids again. Punters are re-engaging with drill campaigns. We're going into a period where investors are hunting for exposure to fresh frontier basin plays.

IVZ is one of the few ASX-listed names with a drill campaign, a declared discovery, a flow test ahead, AND a legitimate basin-opening story. That combination is rare right now.

Our Big Bet for IVZ

To see IVZ go on and make a basin opening oil/gas discovery in Zimbabwe and re-rate by over 1,000%, similar to the move Africa Oil experienced after making its basin opening discovery in Kenya.

Why did we invest in IVZ?

The prize is BIG: IVZ’s project has a 5.5 BN barrel equivalent prospective resource

The Cabora Bassa Basin holds a gross unrisked mean prospective resource estimate of ~5.5 billion barrels of oil equivalent.

IVZ is exploring and developing the Cabora Bassa Basin, one of Africa's largest and last untested frontier rift basins.

If IVZ can convert even just 10% of that into confirmed, commercial discoveries it should re-rate a lot higher from the current market cap.

The next well (Musuma-1) alone is targeting ~1.2tcf of gas and 73 million barrels of oil -.

Two wells have already confirmed a working hydrocarbon system.

Two wells in, IVZ has confirmed what is usually the hardest part of frontier oil and gas exploration: A working oil & gas system under the Cabora Bassa Basin.

Meaning the right technical fundamentals for defining commercial discoveries are there.

(Seal, trap, reservoir, source, maturity)

Everything from here is about proving commercial scale - just need those flow tests to deliver... 2027?

A NEW high-impact well (Musuma-1) lined up to drill in H2 2026

Today’s IVZ announcement says preparations are underway to spud and drill the well in H2 2026.

The Musuma-1 well has a prospective resource of ~1.2 Tcf gas and 73M barrels of condensate (~277M Barrels of oil equivalent). (source)

From all of the years we have followed IVZ, what we know is the drilling window typically opens in July and is open until as late as January (remember the Mukuyu side tracks?).

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Yes, delays can happen.

But IVZ’s got the rig it used last time “warm stacked” (source) - (already mobilised to site) so we are backing IVZ to spud next half as per the timeline it put out today.

The long awaited “PPSA” looks imminent, this would remove regulatory risk overhang on the stock.

The Petroleum Production Sharing Agreement has been the elephant in the room for years.

A PPSA in Zimbabwe stands for a Petroleum Production Sharing Agreement, specifically referring to the legal and fiscal framework established between the government of Zimbabwe and exploration companies to manage oil and gas production.

This agreement will be what governs the terms for any commercial discoveries IVZ makes (like royalties, taxes etc).

This agreement with the government becomes very important for IVZ as it moves from exploration into development.

Recent company commentary points to execution THIS MONTH (April 2026).

IVZ's "string of pearls" basin margin play mirrors Africa Oil's Lokichar setup. One discovery can unlock many.

Just like Africa Oil Corp’s Lokichar Basin (my first ever 10x on an oil & gas well back in 2012), the Cabora Bassa basin margin contains multiple prospects sharing similar geological characteristics.

If one "pearl" works, the probability that the next one also works goes up.

Other explorers in similar setups (Africa Oil Corp, for example) had already farmed down 50% before spudding.

No farmout means IVZ has managed to retain a big ownership stake.

So if the basin is unlocked commercially, IVZ will hold the keys to a potential 5.5BN barrel of oil equivalent basin.

IVZ sentiment has been at a multi-year low after a 2 year break from drilling and the Qatar Deal not proceeding. Exactly where we like to enter/increase position.

The failed Qatari deal. A two year break from drilling. Oil and gas sentiment ebbing.

A gas-condensate discovery where the market sold off (need that flow test!).

All of it has beaten the IVZ share price down to a level that in our opinion doesn't reflect what's actually under the ground.

We've seen this before with IVZ: Activity dries up, IVZ’s share price trades lower, then once the drill rig starts moving the market remembers the stock exists.

Generally, we observe that when IVZ has been making tangible progress towards drilling, the share price has traded much higher than it is right now.

The past performance, as always, is not an indicator of future performance.

Oil & gas is back on the small cap market's radar after years in the proverbial graveyard, giving macro tailwinds for drilling activity.

After a couple of sleepy years, oil & gas is back on the market's radar.

Small cap O&G explorers that were in the purgatory 6 months ago are now catching bids.

This is a nice macro setup for when IVZ is about to drill.

IVZ has one of the biggest dormant retail followings on the ASX.

IVZ has (had?) one of the bigger retail followings on the ASX for a small cap explorer.

Right now, it's dormant. A drill announcement could wake it up fast.

(Similar to what we've seen with names like VUL, LRS, EXR and Hycroft in their prime moments.)

When these stocks have a catalyst and a reason for punters to re-engage, the retail army can drive the share price well beyond what the fundamentals alone would suggest.

What do we expect IVZ to deliver?

Objective #1: Drill the Musuma-1 well

We want to see IVZ drill its next well targeting 1.2 Tcf gas + 77M barrels of condensate resource.

IVZ expects to be drilling next half.

Milestones

Rig mobilisation to site

Drilling starts

Drilling updates

Drilling results

Objective #2: Flow test its Mukuyu discoveries

We want to see IVZ re-enter its Mukuyu discovery - deepen the well into the Lower Angwa reservoir and flow test across both the Upper and Lower Angwa reservoirs.

Milestones

Flow tests commence

Interim results

Final results (commercial or not decision here)

Objective #3: PPSA signed and executed

We want to see IVZ sign a Petroleum Production Sharing Agreement (PPSA) with the Zimbabwe government.

Recent company commentary points to April 2026. When signed, the biggest regulatory overhang lifts.

Milestones

PPSA terms finalised

PPSA signed

PPSA executed

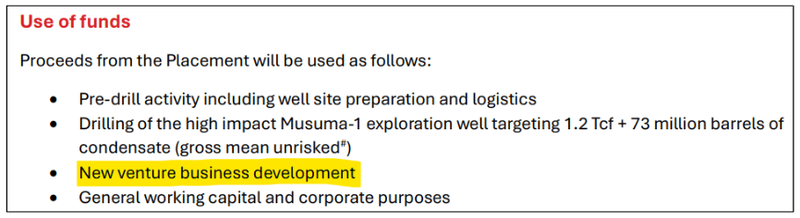

Objective #4: Bonus objective - IVZ does a deal on a new asset

A big part of the old deal with the Qatari’s was to look at acquiring new assets in Africa (more advanced assets).

IVZ also mentioned “New venture business development” again in the announcement today - which definitely caught our eye...

IF this objective came in then it would just be an added bonus for our IVZ Investment Thesis.

What could go wrong?

Exploration risk.

This is a frontier rift basin drill. The most common outcome for any frontier O&G drill is no discovery and a painful share price reaction. Even with the working hydrocarbon system already proven, Musuma-1 is a new target and could fail.

Flow test risk.

The Mukuyu discovery is declared, but commercial flow rates aren't proven. High water content, low permeability, or low flow rates could make the gas uneconomic.

Delay risks.

IVZ has been "about to drill" multiple times. If Musuma-1 slips into 2027, the market loses patience.

Funding risk.

Drilling is expensive. The Qatar deal fell over. IVZ has raised capital again recently. If a drill result doesn't land well, another raise is likely and it will be dilutive.

Jurisdiction risk.

Zimbabwe has a history of political and economic instability. Any shift in government or fiscal terms can impact the project's economics.

PPSA execution risk.

It's close, not signed. If it slips or the final terms land worse than expected, sentiment takes a hit.

Commodity price risk.

Global oil & gas prices drive the economics of any discovery. A sharp move lower changes the calculus.

Other risks:

Like any early-stage exploration company, IVZ carries significant risk, here we aim to identify a few more risks.

While previous wells confirmed a working hydrocarbon system, frontier exploration is statistically difficult and there is no guarantee the upcoming Musuma-1 well will hit commercial quantities. A failure at this specific target would likely lead to a sharp decline in the share price as the market reassesses the basin's potential.

Despite the recent $10M capital raise, deep frontier drilling is incredibly expensive and operational delays are common in the industry. Any unforeseen technical issues could exhaust the current cash balance, leading to further dilutive capital raises that would reduce the value of existing holdings.

The long-awaited PPSA is a critical regulatory hurdle, and any failure to execute this agreement on favorable terms would impact the project's long-term commerciality. Navigating the legal and fiscal framework in Zimbabwe carries inherent sovereign risk, where government policy shifts can occur without warning.

Proving the existence of gas is only half the battle, as the company still needs to demonstrate that it can flow at commercial rates. If the upcoming flow tests show poor permeability or high water content, the discovery may be deemed uneconomic regardless of the total resource size.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

What is our investment plan?

We first Invested in IVZ in September 2020 at an Initial Entry Price of 3.5c per share.

Across the last 6 years we have Free Carried our position and Taken Profit at key points. But we have held a material, core position through every drill result to date.

In April 2026, we significantly increased our position via the recent cap raise at 6c (scaled back in our offer letter).

Our plan from here:

Hold our core position into the Mukuyu flow test and the Musuma-1 drill result.

Top Slice a portion of the position if the share price runs significantly into the drill (around 10% of holding).

Reset the memo if a highly material event occurs (e.g. another strategic deal, a significant acquisition, a transformative capital raise).

This is our strategy. It suits our personal circumstances and is not financial advice for anyone else.

Disclosure: Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 13,409,767 IVZ Shares and 7,836,624 IVZ Options and the company's staff own 1,260,417 IVZ Options at the time of publishing this Investment Memo. The Company has been engaged by IVZ to share our commentary on the progress of our Investment in IVZ over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

Investment Memo:

Invictus Energy

(ASX:IVZ)

-

LIVE

Opened: 13-Jul-2023

Shares Held at Open: 5,893,666

What does IVZ do?

Invictus Energy (ASX: IVZ) is an oil and gas exploration company looking to confirm a discovery in Zimbabwe, Africa - one of the few underexplored basins remaining in the world.

IVZ is also developing a carbon offset project in Zimbabwe which could see it develop the world’s first carbon neutral gas project.

What is the macro theme?

Natural gas demand is set to increase in Africa as it replaces existing coal power generation.

As governments around the world look to phase out ageing coal generation, gas will play a critical role in providing a lower carbon footprint. Gas is a more cost-effective alternative to base-load energy generation.

A potential discovery by IVZ has the potential to supply both Zimbabwe and the gas hungry South African market.

IVZ’s carbon offset project also provides a rare ASX listed exposure to the “carbon credits” markets which is expected to grow by ~500% by 2030.

Our Big Bet for IVZ

To see IVZ go on and make a basin opening oil/gas discovery in Zimbabwe and re-rate by over 1,000%, similar to the move Africa Oil experienced after making its basin opening discovery in Kenya.

Why did we invest in IVZ?

“Basin Master” position in Zimbabwe

IVZ holds an interest in the entire Cabora Bassa basin. In the event the company officially declares a discovery, any major company looking for exposure to the basin will need to negotiate a deal with IVZ.

IVZ holds ~90km of basin margin fairway with a prospective resource of 1.17 billion barrels across five drill ready targets.

IVZ’s basin margin is analogous to the Lokichar basin where Africa Oil made its discovery and re-rated by over 10x. For context, the Lokichar basin saw >0.8 billion barrels of oil discovered with an 88% success rate after the first discovery was made.

De-risked project

IVZ has already confirmed a working conventional hydrocarbon system at its project. All the company needs to do to declare an official discovery is bring an oil/gas sample to surface.

With the data and lessons learnt from its first well, we hope IVZ will deliver this milestone.

IVZ’s project is located in Zimbabwe which borders energy hungry South Africa. The project benefits from immediate access to well developed energy markets servicing ~230 million people.

South Africa in particular needs more natural gas supply with significant shortages expected by the year 2030 as the country looks to transition away from coal powered generators.

Experienced management team to lead project development

IVZ recently brought on board John Bentley as Chairman and Robin Sutherland as a Non-Executive Director. John grew the small cap company Energy Africa before selling the company to Tullow for US$500M.

Robin led the Tullow exploration team through multiple discoveries, including the ones made in the Lokichar Basin in Kenya (the basin we always compare to IVZ).

Rare ASX exposure to a blue sky carbon offset project

Concurrent with its gas project, IVZ is developing a carbon offset project on a 50:50 partnership basis with the Forestry Commission of Zimbabwe.

Carbon credits are expected to trade for up to US$80-150/tonne by 2035 - once IVZ’s project is verified as eligible to generate carbon credits this could produce a second revenue source for the company.

What do we expect IVZ to deliver?

Objective #1: Drilling of the Mukuyu-2 appraisal well

We want to see IVZ drill the Mukuyu-2 appraisal well and officially declare a new discovery.

IVZ’s well is now funded having raised $35.4M in cash over the last 6 months. There is also a possibility IVZ looks to bring in an offtake partner for the project which may help with future funding rounds.

Milestones

Capital raise 1.1 - Placement at 12c

Capital raise 1.2 - SPP at 12c

Capital raise 1.3 - Placement at 12c

Offtake MOU/agreement

Objective #3: Identify and confirm the first basin margin well

We want to see IVZ firm up its first drilling target across its basin margin fairway. At this stage, it looks like IVZ will drill the Baobab prospect but given the company is looking to acquire more 2D seismic data this could change.

Milestones

Review targets

2D Seismic acquisition program

Prospective resource update

First basin margin well location finalised

Objective #4: Progress the development of its carbon offset project

We want to see IVZ progress its carbon offset project to the point where it becomes accredited under Vera’s Verified Carbon Standard (VCS) program so that the carbon credits can be sold in the open market.

Milestones

Results from the pilot program

Financing/partnership agreement on the project

Accreditation under Vera’s Verified Carbon Standard (VCS) program

What could go wrong?

Exploration risk

IVZ is planning two wells, the first is an appraisal well and the second is a new exploration well.

While the appraisal well is somewhat derisked (because it is targeting a known hydrocarbon system) there is still a risk that nothing commercial is found.

There is also a risk of technical failure while exploring.

Commercialisation risk

If gas is found it doesn't guarantee that it can be economically produced, there is a risk that the water content of the gas flows is too high making it uneconomic to extract.

Flow-rates will need to prove that any gas found can be economically produced.

Commodity Price Risk

Ultimately demand for gas and its price will dictate the economic viability of IVZ’s project.

Market risk

If the broader market sells off there is a chance that investors shy away from high risk investment opportunities like oil and gas explorers.

IVZ is a pre-revenue explorer and may be impacted by these market wide sell offs.

Funding risk

IVZ does not generate any revenues and so is reliant on fresh funding for its exploration programs.

This means IVZ is reliant on access to capital, if the markets are unwilling to finance IVZ’s exploration programs the company may need to go slow on its operations or offer large discounts to its share price when raising capital.

Geopolitical Risk

The project is located in Zimbabwe which has a history of political and economic instability, there is always a risk that geopolitical issues make it difficult to advance the gas project.

IVZ has a preliminary Production Sharing Agreement Finalised but the second half is not completed, there is a risk that the agreement is delayed or that IVZ gives up a portion of the project as part of the agreement.

What is our investment plan?

As with all our early stage oil and gas Investments, we Invest early, well before the main drilling event and will aim to be free carried and have taken some profit before the drill result comes in.

Disclosure: Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 5,893,666 IVZ shares and 2,675,435 IVZ options and the Company’s staff own 101,667 IVZ shares and 31,679 IVZ options at the time of publishing this memo. The Company has been engaged by IVZ to share our commentary on the progress of our Investment in IVZ over time.

Investment Memo:

Invictus Energy

(ASX:IVZ)

-

CLOSED

Opened: 16-Feb-2022

Closed:

16-Feb-2023

Shares Held at Open:

6,706,980

Shares Held at Close:

3,692,102

Reason Memo Closed:

Drill Campaign Complete

What does IVZ do?

IVZ is a gas exploration company drilling one of the largest un-tested gas prospects in Zimbabwe.

What is the macro theme?

Natural Gas demand in Africa to replace existing coal and oil energy generation. As governments around the world look to phase out ageing coal-generation, gas will play a critical role in providing a green and more cost-effective alternative to base-load energy generation.

While a large part of our macro focus was on the domestic continental need for gas, in 2022 we also saw a worldwide supply crisis break out after Russia invaded Ukraine.

African energy markets still need more gas supply (specifically the South African market) and so we think the macro theme behind IVZ has actually improved from the time we put out our Investment Memo.

To see IVZ go on and make a basin opening oil/gas discovery in Zimbabwe and re-rate by over 1,000%, similar to the move Africa Oil experienced after making its basin opening discovery in Kenya.

Why did we invest in IVZ?

First mover on an Elephant Scale Target

Our primary reason for investing in IVZ was for it to go and replicate our previous success with Africa Oil back in 2012. IVZ's Oil & Gas project in Zimbabwe has a prospective resource (100% Gross Basis) of 9.25 TcF Gas + 294m barrels of Conventional Gas-Condensate. Drilling program expected to cost US$12m which is cheap considering the size of the target being tested.

We think IVZ’s first mover status in the Cabora Bassa Basin is what led to the interest in IVZ’s maiden drill program.

While the company didn't officially declare a discovery, during the drilling program, positive newsflow was enough to take the company’s share price to ~40c per share.

Strategic Location bordering South-Africa

Zimbabwe over-looked in the past due to geopolitical issues & rampant inflation. With political climate improving & it's location bordering the Energy hungry South-Africa the project has immediate access to energy markets & direct to industrial users who are looking to transition energy consumption at there projects to a more green source.

We think this is still a key part of the IVZ story. We also think that with countries all around the world looking to secure local energy supplies, the regional importance of IVZ’s project is a whole lot higher now.

We like big oil & gas exploration drilling events

We have been investing in early stage oil & gas exploration for many years, and three of our most successful investments have been in "swing for the fence" high impact drilling, especially if it is a "basin opening" drill. These are high risk but high potential reward. Big, basin opening, exploration wells (like IVZs) take a long time to prepare, but the share price usually runs up in the lead up to commencement of the drilling.

IVZ delivered a “swing for the fence” drill program. With the share price moving up by ~400% during drilling, it demonstrated why these type drill events are interesting to us as Investors.

What do we expect IVZ to deliver?

Objective #1: Detailed interpretation of seismic survey recently conducted.

We are hoping to see the results from the seismic survey form a major part of the planning process for the upcoming maiden drilling program.

Milestones

Shoot seismic programs

Analyse/reprocess data

Refine drill targets and finalise well locations

[Memo Assessment - 16-Feb-2023]:

Grade = A

IVZ ran a ~315km 2D seismic program adding to the existing US$30M in Mobil data. The company then ran detailed modern processing of the data to finalise the drilling location for the Mukuyu-1 well. While the programs took a little longer than we would have liked, the company did manage to execute our key objective.

Objective #2: Drilling rig contracted and permitting completed

We are hoping to see all of the permitting process completed & drill-rigs contracted before the company needs to raise to finance drilling.

IVZ contracted the Exalo 202 rig, signed a well services contract with Baker Hughes (one of the world’s biggest oil and gas exploration contractors) and also managed to secure a drill permit for the Mukuyu-1 well.

We also note that the company signed an agreement with the Zimbabwe Sovereign Wealth Fund for the exploration rights covering the basin margin of the Cabora Bassa Basin. This came unexpectedly to us.

IVZ failed to sign a binding farm out agreement. Leading up to drilling, we wanted to see IVZ de-risk its position by getting a joint venture partner to finance most of the drilling. Instead IVZ decided to go it alone and funded the drilling from shareholders with a number of capital raises.

In hindsight this was a good call given the company has now identified a “working conventional hydrocarbon system” but in judging the financing objectively, we have decided a B is appropriate.

Objective #4: This is the most important: We want to see the first drill.

IVZ delivered its first drill program before the year ended, fortunately for us and all IVZ shareholders the drill program didn’t deliver a duster. While it did not deliver the fairytale “discovery on first hole in basin opening well”, it did deliver a working hydrocarbon system.

The grade here is based on IVZ successfully delivering the drilling and the result, not the actual result itself, so we have marked this down from A to B, for delays and technical issues during drilling.

What could go wrong?

Exploration Risk

IVZ will be doing a maiden drilling program at its gas project, there is a chance the drilling finds no gas which could mean the project is stranded.

This risk was somewhat mitigated as IVZ successfully identified a “working conventional hydrocarbon system” with multiple potential reservoir intervals.

While this is unrelated, IVZ did encounter a number of technical difficulties and equipment failures. In hindsight we should have listed this as a potential risk to the drill program.

Economic Production Risk

If gas is found it doesn't guarantee that it can be economically produced, there is a risk that the water content of the gas flows is too high making it uneconomic to extract. Flow-rates will need to prove that any gas found can be economically produced.

[Memo Assessment - 16-Feb-2023]:

Risk = Unchanged

If gas is found it doesn't guarantee that it can be economically produced, there is a risk that the water content of the gas flows is too high making it uneconomic to extract. Flow-rates will need to prove that any gas found can be economically produced.

Geopolitical Risk

IVZ didn't run a production test over its project so this risk remains unchanged for IVZ’s project.

[Memo Assessment - 16-Feb-2023]:

Risk = Decreased

IVZ has to date managed to sign an agreement with the Zimbabwe Sovereign Wealth Fund and also had the Minister of Mines on site during the drill program.

IVZ is yet to sign a final Production Sharing Agreement, so this risk will carry into our next IVZ Investment Memo.

Overall we feel the company has managed this risk well to date.

Commodity Price Risk

Ultimately demand for Gas and its price will dictate the economic viability of the project.

[Memo Assessment - 16-Feb-2023]:

Risk = Unchanged

This is a general sector wide risk that wasn't an issue for IVZ in 2022.

There is always a risk that a recession occurs and energy prices all over the world start to fall.

We are confident that the energy supply problems are structural and that any fall will be temporary BUT we will still carry this risk over into our next IVZ Investment Memo.

What is our investment plan?

As with all early stage oil and gas investments we invest early, well before the main drilling event and will aim to be free carried and have taken profit before the drill result comes in. We look to hold at least 40% of our initial position into the first result, this is a ~3 year strategy.

[Memo Assessment - 16-Feb-2023]:

Grade = C

We give ourselves a “C” on this on execution of our Investment plan.

While we did execute our plan to the point of free carrying before the result, we decided not to take any profit (against our plan) in the hopes that IVZ might announce a discovery.

In this instance we held more into the result that we usually would have (and still hold it now) and the result did not go our way (share price went from high of 40c down to trade at ~12c).

Our larger than usual hold into results was probably due to the emotional attachment to replicating the result we had holding a larger than usual position into Africa Oil Corp’s successful discovery result in Kenya 10 years ago.

Disclosure: The authors of this article and owners of Next Investors, S3 Consortium Pty Ltd, and associated entities, own 6,706,980 IVZ shares and 140,989 IVZ options at the time of writing this article. S3 Consortium Pty Ltd has been engaged by IVZ to share our commentary on the progress of our investment in IVZ over time.

Our Investment Summary

Date of Initial Coverage

18-Sep-20

Inital Entry Price

$0.035

Returns from Initial Entry

74%

High Point

1057%

Investment Milestones for IVZ

✅ Initial Investment: 3.5c ✅ Top Slice ✅ Free Carry ✅ Increased Investment: 11c ✅ Free Carry ✅ Increase Investment: 10c ✅ Free Carry ✅ Increase Investment: 23c ✅ Free Carry ✅ Increase Investment: 12c 🔲 Free Carry 🔲 Take Profit ✅ Price increases 300% from initial entry ✅ Price increases 500% from initial entry ✅ Price increases 1000% from initial entry ✅ 12 Month Capital Gain Discount 🔲 Hold remaining Position for next 2+ years