IVZ declares a Discovery!

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 5,715,563 IVZ shares and 2,833,212 IVZ options and the Company’s staff own 161,667 IVZ shares and 51,679 IVZ options at the time of publishing this article. The Company has been engaged by IVZ to share our commentary on the progress of our Investment in IVZ over time.

We have a Discovery!

4 hydrocarbon samples retrieved across two reservoirs.

13.9m of net pay.

Invictus Energy (ASX:IVZ):

“The discovery represents one of the most significant developments in the onshore Southern Africa oil and gas industry for decades.”

AND drilling is continuing right now.

This discovery is just in IVZ’s FIRST primary target...

IVZ is now drilling a further ~400m deeper into their SECOND primary target.

So there will be ANOTHER results announcement in the coming week/s...

Another IVZ results announcement at a time when we expect global media attention to be focused on Zimbabwe’s first ever gas discovery.

Here’s another bonus for long-time IVZ investors...

Remember Mukuyu-1?

Based on todays results, 2022’s Mukuyu-1 well can now ALSO be classified as an official Discovery:

IVZ: “The Mukuyu-2 discovery, 7km away and 450 meters updip of the Mukuyu-1 well, which can subsequently be classified as a discovery, provides confirmation of the large potential of the Mukuyu field which has a structural closure of over 200km2.

So a double discovery for IVZ today.

IVZ’s discovery has now opened up a whole new oil & gas basin in Africa.

This discovery bodes well for all of IVZ’s remaining drill targets.

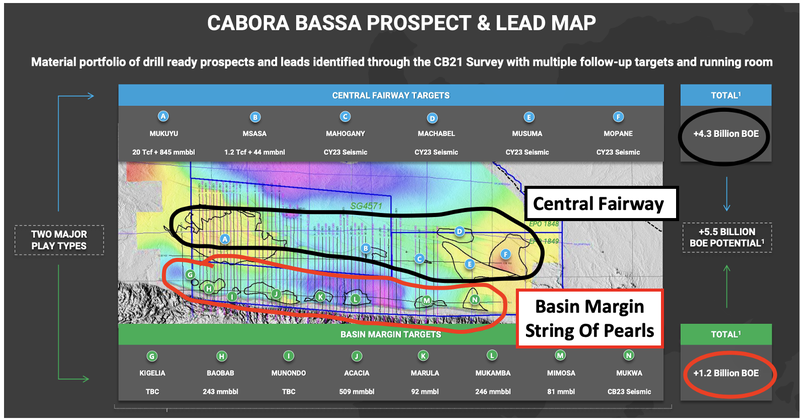

The discovery is from IVZ’s 4.3 billion barrel oil equivalent prospective resource at Mukuyu.

IVZ still has over 1.2 billion barrels equivalent of prospective resource UNDRILLED across its “string of pearls” basin margin targets.

What happens next?

- Global media attention? - Likely to see Zimbabwe’s first ever gas discovery get featured in media all over the world - will ultimately mean more eyeballs on IVZ.

- Results from the rest of drilling - could see IVZ come out with more net pay from its second primary target reservoir and extend its discovery.

- Analyse data and plan next move - IVZ can then decide where to go next - there are so many prospects and targets to go after in the basin

- Flow test - This is when we can start to get an idea of what a development pathway looks like.

You can tune in to see IVZ Managing Director Scott Macmillan do a victory lap and then explain today’s results and what is going to happen next at a shareholder briefing at 11am AEDT today:, here is the link to register:

[REGISTER FOR IVZ SHAREHOLDER BRIEFING WEBINAR]

Invictus Energy

ASX:IVZ

Today, IVZ announced a significant hydrocarbon discovery and opened a whole new hydrocarbon basin in Southern Africa.

This is globally significant news and we expect mainstream media coverage of this event to follow in the next few days (like we saw with Kenya’s first ever oil discovery back in 2012).

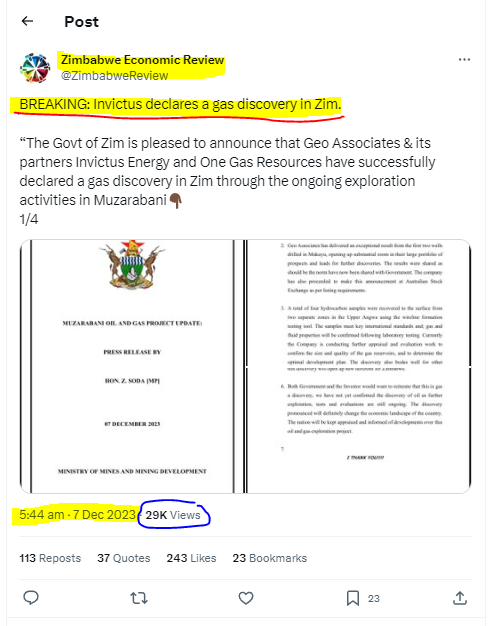

We already saw the news get leaked on X (formerly known as Twitter) by the Zimbabwe press, in the early hours of this morning AEDT:

(Source)

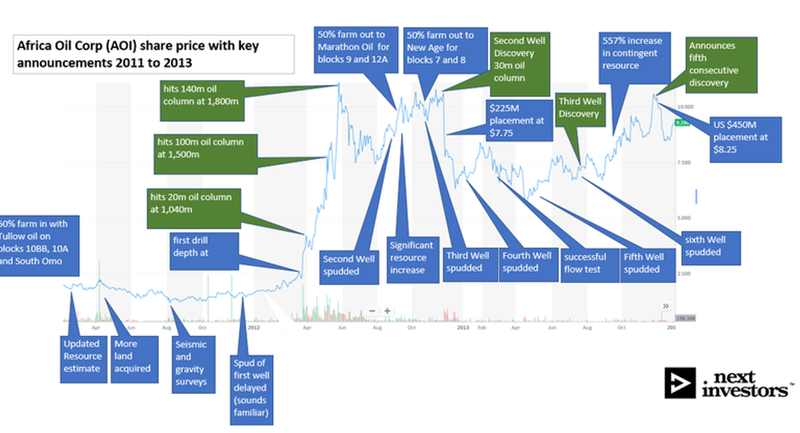

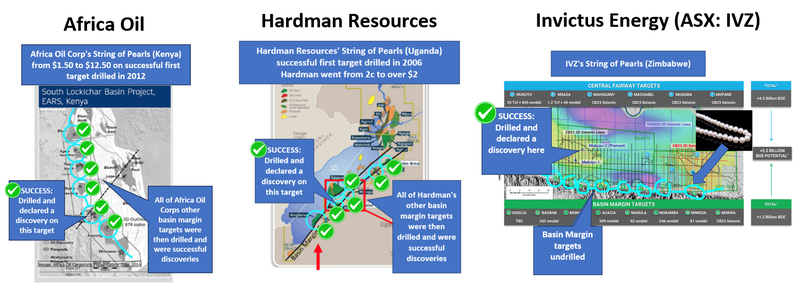

This discovery is the same style discovery that Africa Oil made back in 2012.

Africa Oil hit 20m of net pay in its first part of its well, and then it kept drilling that well and declared more net pay and more discoveries.

Africa Oil re-rated by over 10x in the months after it.

(We are not saying IVZ will perform this way, the past performance of Africa Oil Corp is not an indicator of the future performance of IVZ.)

Then, Africa Oil Corp raised hundreds of millions of dollars and went on to drill discovery after discovery for a couple of years.

Before its discovery, Africa Oil was capped at ~$175M, after its discovery its market cap moved to >$1BN.

At last close IVZ is capped at ~$200M.

The past performance of Africa Oil Corp is not an indicator of the future performance of IVZ.

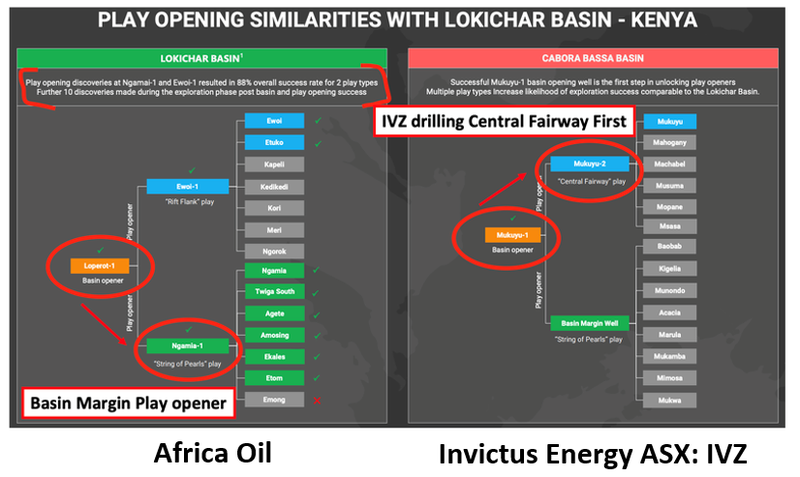

Africa Oil took a more conservative approach to IVZ and drilled its basin margin target first.

IVZ on the other hand drilled its much larger, more risky target first, with the basin margin targets to follow.

This strategy has paid off.

This higher risk strategy could have gone either way for IVZ.

It was touch and go at times (everyone remembers the 40c to 10c drop last year on Mukuyu-1 drilling results and failure to bring a sample to surface) but the reward for IVZ shareholders is a much larger initial discovery.

(side note - How good is it that Mukuyu-1 “can subsequently be classified as a discovery”.)

IVZ’s Mukuyu prospective resource was ~4.3 billion barrels of oil equivalent compared to its basin margin targets at 1.2 billion barrels.

The upside now is that IF any interested parties want a piece of IVZ’s project, IVZ will be negotiating a price from a position of strength.

This is because IVZ has unlocked the bigger, higher-risk structure, with significant exploration upside across its basin margin targets.

Up until now, all of the focus has been on IVZ’s ‘central fairway’ prospects with Mukuyu.

For us, the basin margin targets are a big part of the IVZ story.

IVZ has its own “string of pearls” across a ~90km basin margin where it has a prospective resource of ~1.2 billion barrels of oil equivalent.

IVZ’s “String Of Pearls” are yet to see a single drillhole into them...

Basin margin targets across the East African Rift System (EARS) have an extremely high discovery rate.

Across Basin Margin Fault Closures in the EARS - the success rate is 100% (14 from 14) since 2006.

The back-to-back discoveries on similar basin margin targets is what gave this style of prospects the nickname “string of pearls”.

This phrase was coined because the theory goes that as one “pearl” is drilled, the chances of a discovery from the following “pearls” is extremely high.

IVZ finds itself in a position where it has a confirmed discovery in the more technically challenging but MUCH larger part of its project.

AND it leaves all of the (technically lower risk) wells across the basin margin “String of Pearls” play as bonus upside for future exploration programs.

Now IVZ can go and drill them out one by one and look to replicate the success of Africa Oil a decade ago.

IVZ owns 80% of its project .. and new discovery

Another reason we think IVZ is in a uniquely strong position is because it owns 80% of its project.

For context - Africa Oil Corp had already farmed out a 50% share on the key blocks BEFORE its first drill...

POST-discovery Africa Oil Corp farmed out another 25% for almost $1 billion in back costs repayments and free carry on its remaining 25%.

There are obvious pros and cons to this approach, less risk and a technically savvy partner onboard to help de-risk the project but it does cap the upside once a discovery is made.

IVZ took the riskier approach of self funding its project with shareholders and has managed to make a discovery.

IVZ holds 80% of its project, already has the Sovereign Wealth Fund of Zimbabwe onboard as a project partner AND is in control of the basin's destiny.

A destiny that now includes a hydrocarbon discovery - representing one of the most significant developments in the onshore Southern Africa oil and gas industry for decades.

IVZ now finds itself in a position that the majors typically find the most interesting:

- 80% of a basin opening discovery.

- Project de-risked from an exploration perspective.

- A rig secured for the next two years

- AND heaps of exploration upside (basin margin targets).

Now its project just needs large amounts of capital to fund more drilling and development works.

A good position to be in for majors with big balance sheets looking for projects with size/scale potential.

We think IVZ is in that exact position right now - discovery delivered, plenty more to test in the main basin fairway and NONE of its basin margin targets tested yet.

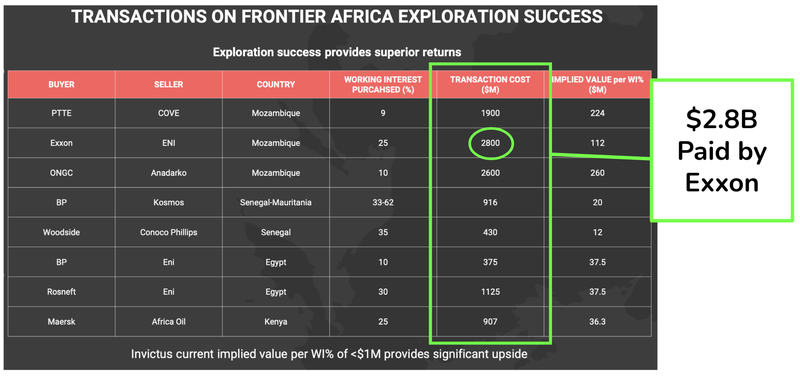

Deals for African oil & gas discoveries have traded in the billions of $

Typically post-discovery, the market tends to look to see what the small cap company’s development plan is.

Most of the time, the company will bring in an industry major as a capital/technical partner and farm-down some portion of the project.

Other times, it will wait for the market to catch onto the scale of the opportunity and then raise money at higher valuations.

Regardless of the pathway IVZ chooses to go down, the table below from an old IVZ presentation shows the valuations paid on transactions across Africa.

The biggest was the $2.8BN transaction with Exxon Mobil.

(Source)

These past transactions on frontier Africa exploration success does not indicate future performance of IVZ.

Whilst we aren't experts here, and there are no guarantees in frontier oil and gas exploration, we think that demand for THIS project in particular will be high.

This is because of the significant and well documented power issues facing South Africa.

(Source)

South Africa is structurally short in gas supply and is in the midst of an energy crisis right now.

It is estimated that South Africa will need 6GW of capacity to overcome the current deficit - and that doesn’t account for an increase of energy demand over the coming years or further cuts to supply.

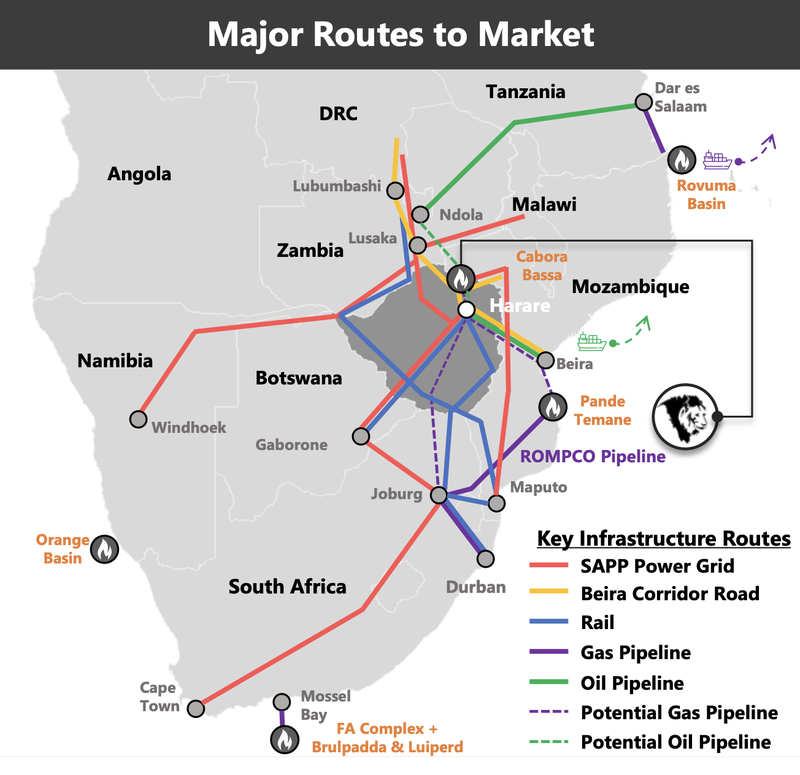

IVZ’s project is well located with access to key infrastructure routes, in particular the South Africa Power Pool grid (in red):

(Source)

Ultimately, we think that IVZ’s discovery is not only significant for shareholders and the country of Zimbabwe, but the entire Southern Africa region as a whole.

Where to from here?

From a technical point of view, IVZ will want to flow test the Mukuyu discovery and then plan the company’s next well.

IVZ has already signed an extension on its rig contract, which sees the rig stay in the basin for another two years.

This means that IVZ can drill new wells at will without having to worry about getting a rig into its project.

A clear sign of the direction in which IVZ’s management wants to take.

The company has made the discovery, opened up the basin and is ready to move its project into its next stage of development.

The harder decision will be how it plans to go about it from a corporate perspective.

The likes of Africa Oil raised capital by farming down a portion of the project.

Other’s sold into the hands of majors - like Hardman Resources which sold to Tullow for AU$1.5BN.

What’s next for IVZ?

🔄 More net pay and samples from second primary target?

The focus for the company is now to finish drilling the sidetrack well and test the second primary target (Lower Angwa reservoir).

So we could see IVZ extend its discovery and announce more net pay in the next few days or weeks.

🔲 Flow testing well

IVZ is planning a flow test for next year which will support whether this discovery can be developed in the future.

🔲 Interest from big majors

Now that IVZ has declared a discovery, we expect some major oil & gas companies to start to take notice.

After today’s announcement IVZ has hit the first part of our IVZ Big Bet (making a basin opening discovery) ...

Our IVZ Big Bet is as follows:

Our IVZ Big Bet:

“To see IVZ make a basin opening oil/gas discovery in Zimbabwe and re-rate by over 700%, similar to the move Africa Oil experienced after making its basin opening discovery in Kenya”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our IVZ Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

Why we think a discovery is so significant for IVZ:

We first Invested in IVZ back in 2020, and we named it our 2020 Energy Pick of the Year.

Over the years, we have written about the different reasons why we think a discovery for IVZ could be a company-making event.

We touched on a few of these already but below are some of the key reasons we think make IVZ’s discovery that much more interesting for the company’s future prospects:

- IVZ holds the key to the basin, if a discovery is made (Basin Master position) - IVZ holds ~80% of its project and if a discovery is made it gets to decide what happens with the project post-discovery.

- Oil and gas majors have paid multiples of IVZ’s current valuation for discoveries across East Africa - some transactions were done at 12x to 224x of IVZ’s implied working interest % on its project.

- Basin Margin ‘String Of Pearls Play’ undrilled - IVZ has ~1.2Bn barrel oil equivalent prospective resources across basin margin targets. Basin Margin targets in the East African Rift System have an exploration success rate of 100% - 14 discoveries from 14 wells.

- Directors who have had success in the East African Rift System - After drilling its first well in 2022, IVZ appointed John Bentley as its chairman and Robin Sutherland as its non-executive director. John built from the ground up and sold Energy Africa to Tullow Oil for US$500M and Robin worked for both Energy Africa and Tullow Oil.

- IVZ is looking to do what Africa Oil has done before - back in 2012, Africa Oil Corp (TSX.V:AOI) drilled a string of successful wells and delivered a 1,000% share price run and sustained re-rate. We are hoping IVZ does the same thing.

- Carbon offset projects to generate carbon credit revenues - IVZ is in the early stages of building out a carbon offset business that could generate revenues from carbon credits. IVZ is a unique small cap exposure to global carbon credit prices.

- One of the biggest conventional oil and gas prospects globally - IVZ has a gross unrisked prospective resource of ~5.5 billion barrels of oil equivalent making it one of the largest conventional oil and gas targets in the world.

- The Zimbabwe Sovereign Wealth Fund is aligned with IVZ - Back in March 2022, IVZ signed a head of agreement with the Zimbabwe Sovereign Wealth Fund which would see the fund take an interest in the project - this aligns the government and the people of Zimbabwe’s interests with IVZ.

- US$30M in work done by Mobil before IVZ acquired the project - The project had US$30M in legacy data leftover by Mobil from the 1990’s. Interestingly Mobil had never drilled the project before IVZ took control of it.

- Strategically located next to South Africa - IVZ’s project sits next to South Africa which is one of Africa’s biggest energy consumers and is expected to be structurally short of energy supplies over the next decade.

What are the risks?

Today’s news largely de-risks IVZ’s project from an “exploration” perspective.

However, the company will also need to prove the project can produce oil/gas at commercially viable rates.

IVZ is planning a flow test for next year which will determine whether or not the discovery can be developed in the future.

There is always a risk the first flow test doesn't come off for IVZ.

IVZ has also just finished drilling Mukuyu-2 and the Mukuyu-2 sidetrack well which means a lot of cash would have been spent to get the company to this discovery.

As a small cap junior that does not generate any revenue itself, “funding risk” is always apparent for companies like IVZ.

IVZ had $22.8M in cash at the end of the September quarter and is likely to have spent a large chunk of it in the subsequent months, especially on the sidetrack hole.

There is always a chance IVZ has to raise more funds through an equity raise which may put some short term pressure on the company’s share price.

Given today’s discovery news, we are hoping any funding injections can be done and much higher share prices now that the project has been de-risked.

To see a full list of the IVZ risk see our July 2023 IVZ Investment Memo.

Our IVZ Investment Memo

In our IVZ Investment Memo, you can find the following:

- Our IVZ Big Bet

- Why we are Invested in IVZ

- Key objectives we want to see IVZ achieve

- The key risks to our Investment thesis

- Our Investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.