Quick Takes

A short form commentary on a particular announcement for a stock in our Portfolio or macro news that we publish on our website

PR1 - former Chief of Australian Navy added to advisory board

ASX:PR1

|2 min

ION - Trump signs critical minerals recycling Executive Order

ASX:ION

|4 min

SGQ hits record 207m rare earths intercept from project in Brazil

ASX:SGQ

|3 min

PAT acquires new copper project in Zambia - drilling in Q3

ASX:PAT

|3 min

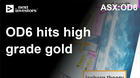

OD6 samples high grade gold at Nevada fluorspar project

ASX:OD6

|2 min

MNB - phosphate fertiliser project construction update

ASX:MNB

|3 min

Quick Takes

A short form commentary on a particular announcement for a stock in our Portfolio or macro news that we publish on our website

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573) (62C), and an employee of S3 Consortium Pty Ltd (trading as StocksDigital).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.