IVZ Secures Gas Sample From Major Discovery

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 5,740,409 IVZ shares and 2,967,713 IVZ options and the Company’s staff own 132,501 IVZ shares and 40,568 IVZ options at the time of publishing this article. The Company has been engaged by IVZ to share our commentary on the progress of our Investment in IVZ over time.

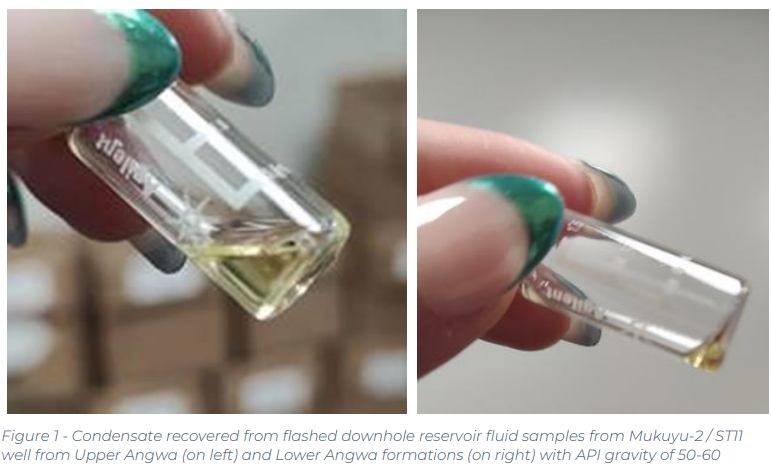

The photo we have been waiting years to see.

Invictus Energy (ASX:IVZ) has now CONFIRMED a rich gas-condensate discovery in their giant Mukuyu oil & gas field.

IVZ’s latest announcement shows a photo of somebody (is it Scott?) holding the precious rich gas-condensate sample from the Mukuyu-2 well:

IVZ now has uncontaminated samples from the reservoir that production could be drawn from.

We also have a preliminary lab assessment of “High quality natural gas with minimal impurities”.

Meaning the gas is easier to process for sale to end users.

There is also helium and hydrogen in the sample - both valuable gases in their own right.

And the key takeaway is that this preliminary analysis supports IVZ’s thesis about the entire basin structure:

- Liquid hydrocarbons south towards the “string of pearls” at the basin margin

- increasing dry gas to the north.

In December last year IVZ declared a discovery in Mukuyu-2 (and by extension also Mukuyu-1).

For some reason unbeknownst to us, the IVZ share price went up... then down on the discovery announcement day.

The small cap market often doesn’t behave rationally OR as you expect.

The IVZ share price traded down after the discovery announcement.

Then sideways for the last few months while IVZ analyses the results and the share register rebalances.

The share price response has been baffling and disappointing.

Based on the discovery announcement, we are confident that IVZ is sitting on a monster.

So we continue to hold our full pre-discovery position in IVZ.

Because we expect the market to eventually price in what we believe IVZ is sitting on.

We are also taking up our full rights in the IVZ entitlement offer that is currently open to existing IVZ shareholders.

The 1 for 12 entitlement offer closes tomorrow at 5pm AWST.

Existing holders can acquire 1 share for every 12 held, at an issue price of 13 cents.

Participants will also receive 1 listed IVZ option (IVZOA) for every 2 shares subscribed to.

We are transferring our $ this afternoon so expect to see an extra ~600,000 or so shares on our disclosure at the top of this email in the future.

The IVZ entitlement offer is to raise ~$15M, and the prospectus document says the company has 3 months after the entitlement offer closes to place any stock that has not been taken up by existing IVZ shareholders (this is called a shortfall).

Existing IVZ shareholders are entitled to apply for more than their entitlement, which we are doing.

(this is our strategy and works for our risk profile, it's not right for everyone, early stage O&G investing is high risk, consult your advisor before making any decisions)

Entitlement offers, rights issues and SPPs usually put pressure on the share price at around or below the offer share price (13c in this case) because most investors can sell their stock and replace it with stock from the entitlement offer.

In our view, once the entitlement offer is closed, the shortfall is placed AND the company announces the 2024 plan, we should see the IVZ share price finally start to run as the market prices in the discovery and expectations from the 2024 work program.

(this is just our opinion, sometimes we get it wrong... remember that we expected the IVZ share price to rerate upwards on the discovery announcement back in December, which it didnt for some reason)

What will wake the market up to IVZ’s discovery?

First, a couple of months of sideways trading always helps - this is now out of the way.

The 13c entitlement offer closing tomorrow will also help.

Completion of the shortfall placement, and maybe a week or two for any short term shortfall holders to churn through.

And then...

We think the company will eventually get its post-discovery re-rate off the back of one (or multiple) of the following:

- Re-rate from flow test results - IVZ flow tests its discovery, shows the market a commercialisation strategy and gets re-rated to reflect that potential.

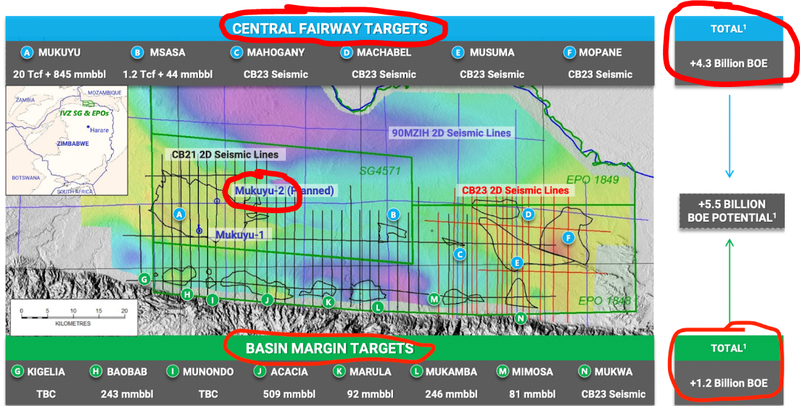

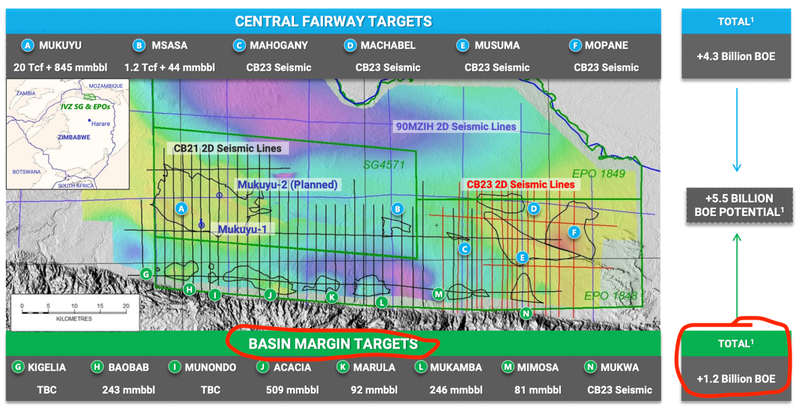

- Re-rate off the back of NEW discoveries across its Basin Margin targets - IVZ drills the ~1.2bn barrel prospective resources across its basin margin and delivers additional discoveries, OR another exploration well in the central fairway.

- Re-rate due to big corporate interest - A big oil and gas producer or a sovereign comes in and takes an interest in IVZ’s project. This could be a strategic move (a country looking to sure up oil/gas supply) or a corporate looking for exposure to Zimbabwe (likely a Chinese major, the Chinese have been making large resource investments in Zimbabwe recently)

- Re-rate due to investor interest - market sentiment turns for small-cap companies and investors start to bid up IVZ shares to a valuation that reflects the potential of its discovery.

- Expectation of positive results from 2024 work program - once IVZ announces the plan for 2024, the market should start building expectations for the results - hopefully a flow test of Mukuyu-2 AND a new exploration well.

IVZ hasn't set a firm timeline of what's next just yet - as the focus right now is probably on analysing the results from Mukuyu-2.

But, here is what we want to see over the next ~9 months:

- More lab results from Mukuyu - more results like the ones put out yesterday.

- Flow test the Mukuyu discovery - this will show the market if IVZ’s discovery can be commercialised or not.

- New exploration well - potentially a well across one of IVZ’s Basin Margin targets?

- Funding from a cashed up partner - this would be a major unexpected catalyst...

IVZ has a drilling window during the Zimbabwe dry season (April to October) and in the last two years has pushed drilling into as late as December, so we expect any flow test and/or exploratory well to happen in this time frame.

Ideally we see both a flow test AND exploration well squeezed in during the 2024 window

We hope to see IVZ’s 2024 plan released to the market in the near term.

Our key takeaways from the announcement

- Gas condensate confirmed - IVZ confirmed gas condensates in a sampling bottle confirming its discovery.

- High quality natural gas - IVZ returned natural gas with minimal impurities, which typically means the gas requires less processing before it's made available for sale. IVZ reported <2% carbon dioxide and no hydrogen sulphide in its samples.

- Geological model showing more liquids to the south - IVZ commented on the results coming back from its project, showing that to the south (closer to the basin margin), the reservoirs are more liquid-rich (oily) and to the south, dryer (gassy). The significance of this is that IVZ’s project isn't a pure play oil or gas asset - it could be both.

- Helium and hydrogen confirmed - IVZ also noted helium and hydrogen in its samples. We found this news interesting especially because London listed Helium One saw its share price go up ~10x off the back of Helium/hydrogen shows at its Tanzanian project.

(we also note that our helium explorer NHE’s share price has popped this morning on announcing a “probable free gas cap” - more on this soon... why do these gas explorers (IVZ, NHE, EXR) always announce big news so close to each other?)

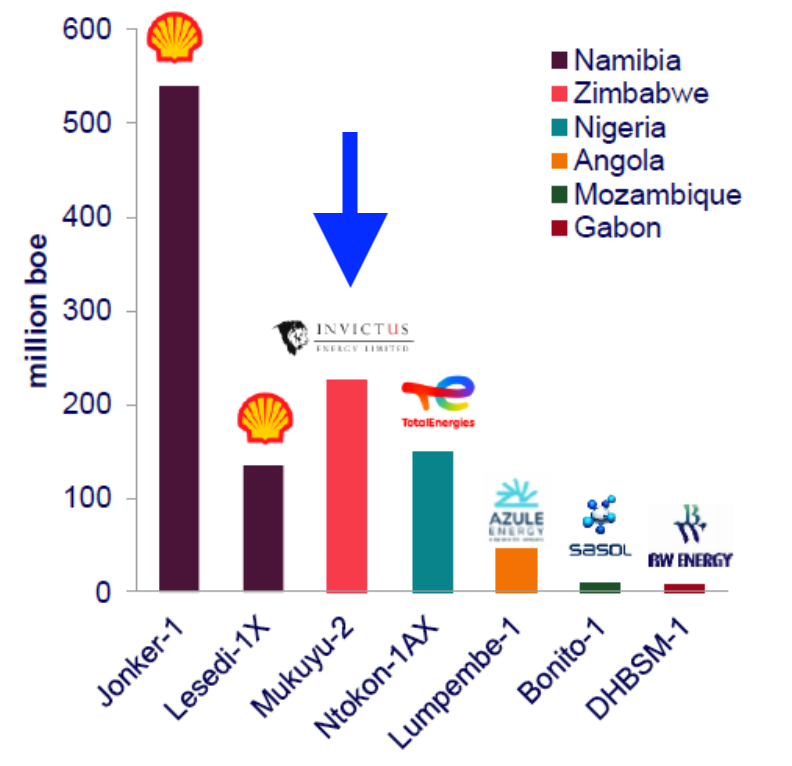

2nd biggest discovery in Sub Saharan Africa in 2023?

Consultants Wood Mackenzie are calling IVZ’s discovery “the 2nd biggest discovery in Sub Saharan Africa for 2023”.

Second only to oil and gas supermajor Shell’s discovery in Namibia:

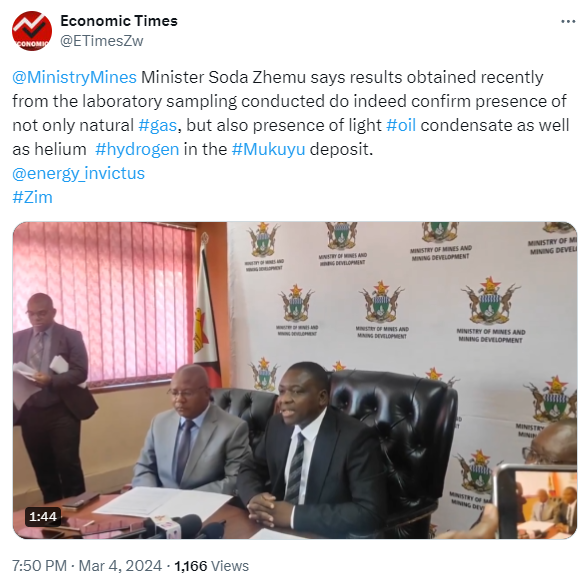

Given the size of the discovery it's no wonder Zimbabwe’s Minister for Mines Soda Zhemu held a press conference to talk about yesterday’s results.

(Source)

Watching the video and seeing the bottle full of gas condensates was almost like a flashback to what we saw ~12 years ago from one of our first big oil and gas wins.

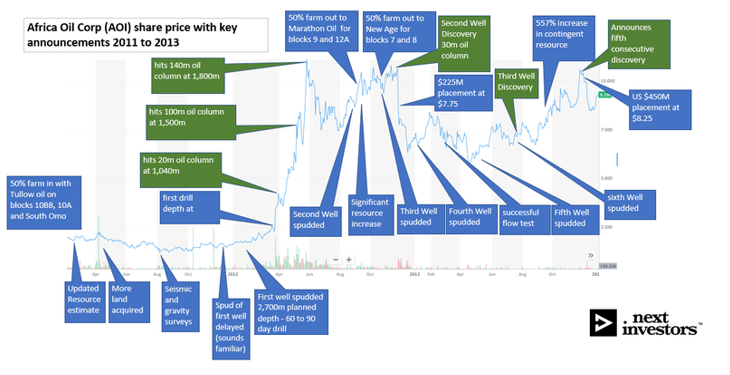

Anyone following our Investment in IVZ will remember the comparisons we have made to Africa Oil.

Africa Oil was our first big win in the oil and gas space back in 2012.

We were Invested in Africa Oil when it made the big Ngamia-1 discovery.

Post discovery the Kenyan Energy minister came out holding a sampling bottle full of crude oil and the images were all over the news.

Here is a side by side of IVZ and Africa Oil’s bottles:

A fluid sample in a small bottle in the media contributed to Africa Oil’s share price run over the next ~6 months from $1 to over $10.

After its discovery, Africa Oil drilled and declared a second discovery, then raised $193M at $7.75 per share. Africa Oil then had enough cash to keep rigs in country and continue making additional discoveries all along its basin margin.

Eventually, Africa Oil farmed down half of its 50% ownership in the Lokichar Basin to Maersk for a deal worth nearly $1 billion in back cost repayments AND future carry.

This is what we were HOPING to see off the back of the IVZ discovery, but the market had other ideas in the near term, now we are hoping for a gradual pricing in of the news over time.

We are Invested in IVZ to see a similar sort of outcome over the coming years.

Why we are backing IVZ

A key differentiating factor between the Africa Oil and IVZ discoveries were the % ownership of their respective projects going into their first discoveries.

Africa Oil went into its first discovery, owning ~50% of its project.

IVZ went into its discovery, owning 80% of its project.

While it may not seem like a huge difference, the higher % ownership coupled with no existing relationship with any major means IVZ is open to negotiating any potential deals from a much stronger position.

It also leaves room for competitive tension to creep in amongst any interested parties. In contrast, if the project already had a 50% JV partner it could deter any corporate interest from a competing major.

Read more about why we think it's a big point of strength for IVZ here: IVZ holds the key to the basin, if a discovery is made (Basin Master position).

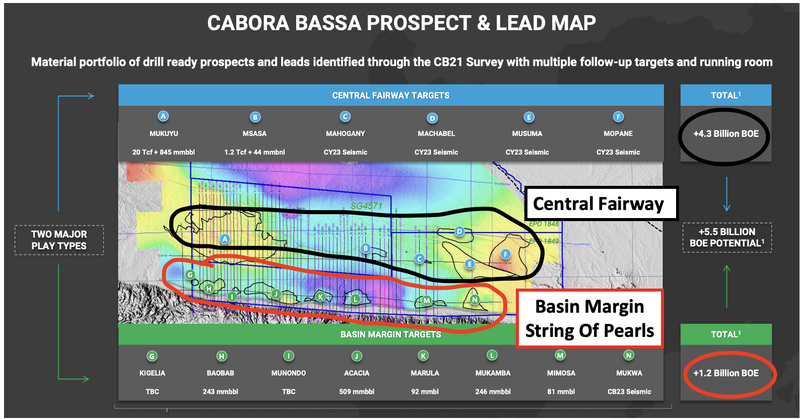

We have also mentioned several times that IVZ’s Mukuyu discovery is from just one of IVZ’s multiple targets...

AND that IVZ has yet to drill any of its Basin Margin targets.

For context - Africa Oil (as mentioned earlier) made its initial discoveries along a basin margin.

Basin Margin targets in the East African Rift System have an exploration success rate of 100% - 14 discoveries from 14 wells.

IVZ still has ~1.2 billion barrels of oil equivalent in prospective resources across its Basin Margin targets and is yet to drill any of them.

We covered IVZ’s basin margin targets here: Basin Margin ‘String Of Pearls Play’ undrilled.

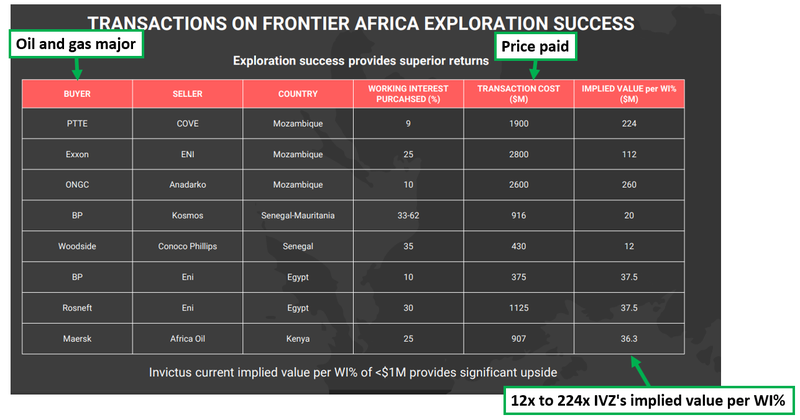

Having exploration upside and an existing discovery is massive for any company, especially when looking to attract funding to take a project from discovery into the feasibility and commercialisation stages.

Majors and funding partners typically look to assess the value of a project not just based on what's in the ground now but also on how much exploration upside there is.

We think IVZ has a good combination of the two IF the company looks to go down the partnership route.

(Source)

We have previously covered the types of valuations projects get post discovery across East Africa here: Oil and gas majors have paid multiples of IVZ’s current valuation for discoveries across East Africa

The final piece of the puzzle when it comes to taking discoveries to the next level is always the team running a company.

IVZ’s directors have had success in the East African Rift System (EARS) before and have built companies from the ground up and sold them to majors.

As an example - IVZ non exec chairman John Bentley built up and sold Energy Africa to Tullow Oil for US$500M.

See our take on IVZ’s team here: Directors who have had success in the East African Rift System.

Ultimately, we are hoping that the above factors help IVZ achieve our Big Bet which is as follows:

Our IVZ Big Bet:

“To see IVZ make a basin opening oil/gas discovery in Zimbabwe and re-rate by over 700%, similar to the move Africa Oil experienced after making its basin opening discovery in Kenya”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our IVZ Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true

Invictus Energy

ASX:IVZ

What’s next for IVZ?

Forward work program for 2024 🔄

The IVZ team is analysing the data from Mukuyu-2 and we are hoping to see a work plan for 2024 with timelines announced soon.

More sampling results 🔄

We expect to see more news similar to yesterday's announcement given IVZ is still analysing samples taken from the Mukuyu discovery.

Resource update 🔄

We expect to see IVZ convert its prospective resource into a contingent resource/reserve.

Usually after a company makes a discovery it is able to take a resource out of the prospective classification and into higher confidence levels.

We expect this to come after all the data is gathered from the discovery wells.

🎓 To learn more, read: How to Read Oil & Gas Resources

Flow testing 🔲

IVZ is planning a flow test for next year which will support whether this discovery can be developed in the future.

Interest from majors 🔲

Now that IVZ has declared a discovery, we expect some major oil & gas companies to start to take notice.

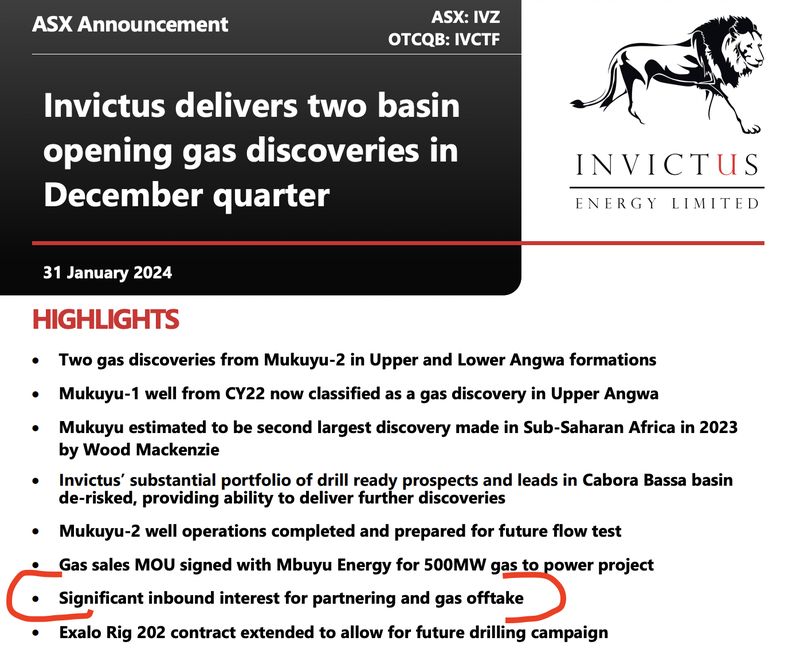

IVZ made mention of corporate interest in its December quarterly report where it noted “significant inbound interest for partnering”.

Our IVZ Investment Memo

In our IVZ Investment Memo, you can find the following:

- Our IVZ Big Bet

- Why we are Invested in IVZ

- Key objectives we want to see IVZ achieve

- The key risks to our Investment thesis

- Our Investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.