IVZ’s resource is now 2.7x bigger - Drilling in August

Disclosure: The authors of this article and owners of Next Investors, S3 Consortium Pty Ltd, and Associated Entities, own 5,175,145 IVZ shares and 65,072 IVZ Options and the Company’s staff own 60,000 IVZ shares and 10,845 options at the time of publication. S3 Consortium Pty Ltd has been engaged by IVZ to share our commentary and opinion on the progress of our Investment in IVZ over time.

2.7 times bigger.

That's how much our 2020 Energy Pick of the Year, Invictus Energy (ASX:IVZ), has upgraded its prospective oil and gas resource by.

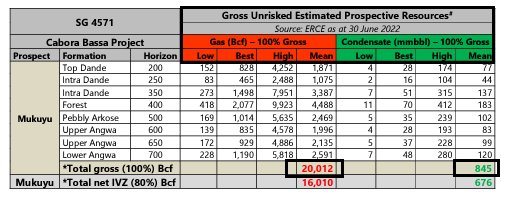

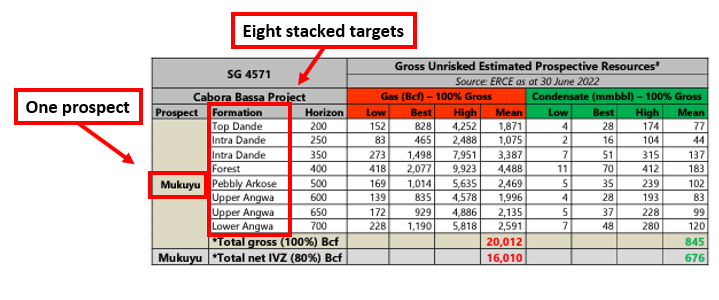

Today, IVZ upgraded the prospective resource at its Mukuyu prospect to a giant 20 trillion cubic feet (Tcf) and 845 million barrels of gas condensate.

A prospective resource that now stands at a total of 4.3 billion barrels of oil equivalent on a gross mean unrisked basis.

Importantly, this entire prospective resource sits inside a single prospect (Mukuyu-1) across eight stacked targets, meaning there could still be multiple follow up exploration prospects that contribute to an even larger project size.

IVZ’s project was already the largest undrilled conventional oil and gas exploration prospect in onshore Africa.

With the prospective resource now 2.7 times larger, the upside case for IVZ’s project has set it up as one of the largest conventional oil and gas exploration prospects globally.

A prospective resource is an initial, high level estimate that sets an exploration target for the company to discover via a drilling program. There’s no guarantee that the oil and gas is down there - the only way to find out is by drilling.

To put IVZ’s prospective resource upgrade into perspective - and comparing it to actual discoveries and resources - as of 2019, BP’s “Greater Tortue Ahmeyim” discovery in Mauritania was considered one of the largest discoveries in Africa.

That project is currently being developed and is expected to produce ~15 trillion cubic feet of gas over its 30+ year production life.

Another is the Bass Strait, offshore Victoria, which has been Australia’s biggest source of domestic gas supply. At its peak, it had reserves of ~10 trillion cubic feet.

IVZ’s updated prospective resource is almost 3.5x the size of BP’s discovery and nearly 2x the size of one of Australia's most prolific oil and gas fields, the Bass Strait.

However, we reiterate that the key difference is that IVZ’s project is a “prospective” resource.

IVZ has not drilled a single well yet and is very much a high risk explorer.

This is a high risk / high reward investment. If IVZ’s drilling is successful, there is significant upside, but like the majority of exploration wells, there is a high chance of failure.

IVZ’s prospect was already the largest seismically defined, undrilled oil and gas structure in onshore Africa. And now it is 2.7x bigger.

IVZ owns an 80% interest in the project, so its net share of the prospective resource equates to 16 Tcf and 676 million barrels of gas condensate (~3.44 billion barrels of oil equivalent).

As part of today’s announcement, IVZ also confirmed that wellpad construction works for the drill rig have finished and that the drill rig is en route to Zimbabwe.

Drilling of the Mukuyu-1 well is expected to commence in August.

We have been Invested in IVZ since September 2020, patiently waiting for this big drilling event.

Long time readers know that we have a clear Investment Strategy when Investing in these high risk high reward oil and gas exploration projects.

We generally have the following plan:

- We invest early in first movers who can secure the best acreage on the best terms. ✅

- We patiently hold onto our investment as the company matures or nears a drilling event that could be a big catalyst for a re-rate. ✅

- As the share price increases on the speculation of positive drilling results, we Free Carry, selling enough shares to cover our Initial Investment and Subsequent Investments. ✅

- The final stage is when we ‘Take Profit’ and hold the remainder of our investment into the drilling results. 🔄

We are currently in stage 4, having Free Carried our Investment and Taken (some) Profit.

With the big drilling event now less than two months away, we will continue to hold the majority of our position going into the drilling program. We will only consider further de-risking if the share price moves materially higher.

Our plan, as always, is to hold a large enough position going into drilling so that in the event IVZ makes a basin opening discovery, it will be transformational for IVZ, and we would expect to make multiples on our investment.

If the drilling is unsuccessful, we would have limited our downside risk having already Free Carried our initial Investment.

We want to reiterate that this Investment Strategy and our Investment in a company like IVZ fits in with our risk profile, but it is not suitable for everyone.

Click below to view our 2022 IVZ Investment Memo, where you can find our detailed Investment Strategy:

IVZ’s project is now one of the biggest conventional prospects globally

With today's news, IVZ's project has gone from one that is regionally significant to now having global significance.

IVZ’s managing director Scott Macmillan spoke to this in today’s announcement, saying IVZ’s “prospect has grown significantly in its scale and now represents one of the largest conventional exploration targets globally”.

IVZ did this by increasing its resource by 270% from ~8.2 trillion cubic feet (Tcf) and 247 million barrels (~1.6 billion barrels of oil equivalent).

The project now has a gross, mean unrisked prospective resource of 20 Tcf + 845 million barrels of conventional gas condensate (~4.3 billion barrels of oil equivalent).

While IVZ’s 80% net share of the resource is 16 Tcf and 676 million barrels of conventional gas condensate (3.44 billion barrels of oil equivalent).

Before today’s news, IVZ’s project was already the largest undrilled conventional oil and gas exploration prospect in onshore Africa.

Now it ranks among one of the largest conventional prospects in the world.

The key takeaways for us from today’s announcement were related to:

- The sheer size and scale of the prospective resource.

- The way the prospective resource sits inside ONE prospective across EIGHT different stacked targets.

First, let’s consider the sheer size and scale of the upgraded prospective resource number.

For some context on just how large IVZ’s upgraded prospective resource number is, it's important to compare the project to those previously discovered, especially those being put into development.

After all, the projects that make it into development require size and scale so that the capital expenditures spent developing them can generate a sufficient enough return to justify all of that upfront investment.

One example from Africa is BP’s “Greater Tortue Ahmeyim” discovery in Mauritania, considered one of Africa’s largest discoveries in the last decade.

BP first made the discovery in 2015 and made a final investment decision to develop the project in 2018.

BP’s project is expected to be put into production in 2023 and produce ~15 trillion cubic feet of gas over a production life of 30+ years.

IVZ’s upgraded prospective resource figure sits at a total of 20 trillion cubic feet, putting its project's upside potential on par with BP’s project.

The obvious caveat is that IVZ’s project’s resource is ‘unrisked’ and entirely prospective - IVZ is yet to drill a well and make a discovery of any kind.

As with all exploration wells, we expect any commercial discovery to have a far lower resource figure than this upside prospective number.

[ 🎓 = To understand more about oil and gas resources, especially the differences between prospective resources and reserves, check out our educational article here ]

The difference is that IVZ is a tiny small cap company with a market cap of $131M and is holding a project with size and scale usually seen in the hands of an oil and gas supermajor like BP (capped at $136 billion).

Second, putting aside the sheer size and scale of IVZ’s prospective resource, we also like that this is the FIRST prospect across the entire Cabora Basin region.

With IVZ holding that entire 20 trillion cubic feet, 845 million barrel gas condensate prospective resource in the single Mukuyu-1 prospect, it means there could still be multiple follow up exploration prospects that contribute to an even larger project size.

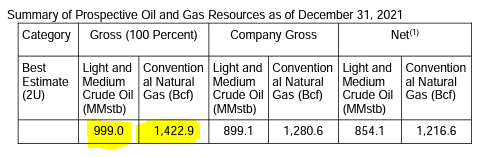

By way of comparison, TSX listed Recon Africa (capped at $1.16 billion) has a gross unrisked mean prospective resource of ~1.4 trillion cubic and ~999 million barrels of gas condensate at its project in northeast Namibia.

Importantly, Recon’s prospective resource report comes from a total of ~35 different leads.

This compares to IVZ’s project, where that entire upgraded prospective resource comes from the SINGLE Mukuyu-1 prospect.

IVZ, therefore, has a prospective gas resource ~14x the size of Recon’s prospective resource on a single prospect, compared to Recon’s 35 different prospects.

We note that Recon has drilled two well across their ground already. Both were “stratigraphic wells” testing the geology over their project area and made no discovery.

Despite this, Recon Africa still trades with a market cap of ~$1.16 billion, compared to IVZ at a market cap of only $131M.

So IVZ holds an interest in a project with a prospective gas resource almost 14x the size of Recon Africa’s whilst also having the optionality of opening up an entire basin to increase its overall project size.

If IVZ does make a discovery with the Mukuyu-1 well, it could be the first of many that opens up an entirely new energy hub in East Africa, all at a fraction of the market cap of a peer like Recon Africa.

The cherry on top for IVZ is that it will have multiple shots at making this discovery with a single exploration well (Mukuyu-1) targeting eight different "stacked targets" over a width of ~15km.

Individually, all eight targets contain a prospective gas resource bigger than Recon Africa.

The stacked nature of IVZ’s well design means that with one drilling program, IVZ will be targeting eight different zones, each large enough to make a transformational discovery.

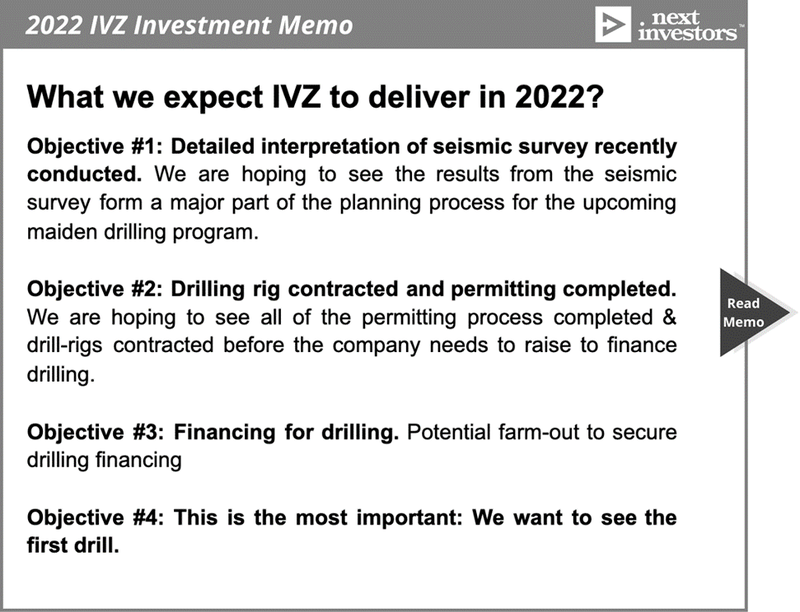

With drilling now scheduled for August, below are the things we are watching for between now and then.

What’s next for IVZ

Below are the key objectives we want to see IVZ achieve in 2022 as per our 2022 IVZ Investment Memo.

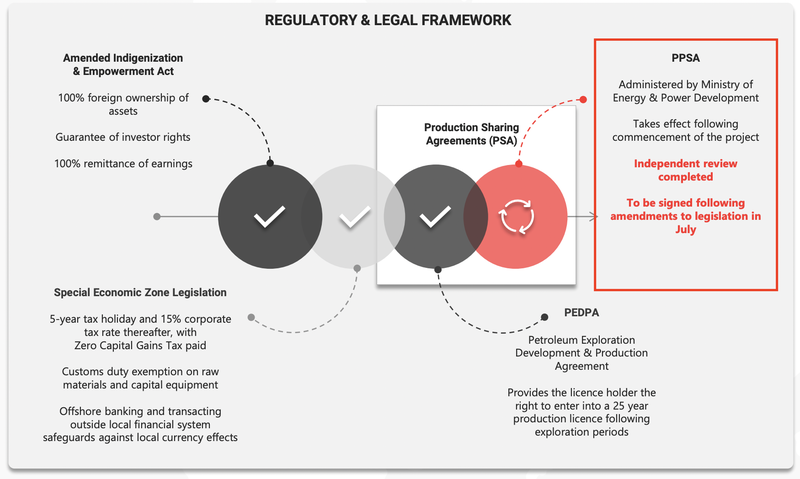

Production sharing agreement + Permitting on extended acreage 🔄

IVZ is currently waiting on formal governmental approvals for both the Production Sharing Agreement and the approval over the extended acreage position.

In today’s announcement, IVZ also confirmed that the pre-gazettal (approval) administration process to increase the SG 4571 permit area by 7x had been completed and was now pending final government approvals.

We hope to see both of these resolved before IVZ starts drilling - given that the production sharing agreement will particularly govern the ownership rights IVZ has over a commercial discovery (assuming a discovery is made).

Second well location to be finalised 🔄

We are still waiting on IVZ to confirm the drilling location for the second well.

With the expanded acreage covering the majority of the “basin margin” play, we think that this will be finalised once all of the permitting is completed, and the company can put in place a plan to drill one of the basin margin targets that is being picked up in the seismic data.

Binding Farm-in agreement to be signed 🔄

In late April, IVZ put out an update on the progress being made on the farm in front.

In that announcement, IVZ confirmed that it had received three separate farm-in offers, including an updated bid from Cluff Energy Africa.

It also confirmed that “ongoing due diligence and internal approvals are being undertaken by additional parties which may result in further bids being received”.

This suggests that the company is receiving much more interest now.

With the acreage position expanded by over 7x in terms of overall size and the Sovereign Wealth Fund of Zimbabwe now involved at the project level, we suspect those interested parties now see some more certainty around tenure hence the heightened level of interest.

We are now expecting a vastly improved offer than the one that Cluff Energy Africa had put in for the project in late 2021.

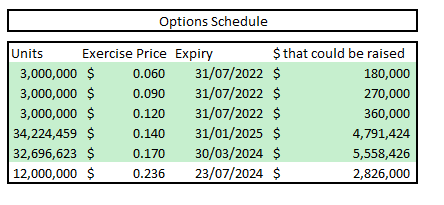

Fully financing the two well drilling program 🔲

In a recent investor presentation, IVZ put out updated cost estimates for both the Mukuyu-1 well and its follow up basin margin well.

The first well is expected to cost ~US$16.5M (of which US$4M has already been paid) and the second US$10M (of which US$2M has already been paid).

IVZ, at the end of the March quarter had $7.3M in cash. Since then, it raised ~$12M via a placement @ 20c per share and had ~$3.3M in options exercised.

This should mean IVZ is going into the drilling of the first well with enough cash to fund most of the first well, but ideally, we would like to see the company de-risk its cash commitment further either via a farm-in agreement or through additional capital raises.

We also note that IVZ still has ~$11.1M in options in the money if the share price stays above 17c per share which could be exercised to help finance the drilling program.

The major catalyst - DRILLING now expected in August 🔲

This one needs no explanation. All of the above milestones will lead to the all important drilling event that IVZ now expects to happen in August.

With the wellpad construction now completed, IVZ expects the rig to be mobilised on site before drilling commencing in August.

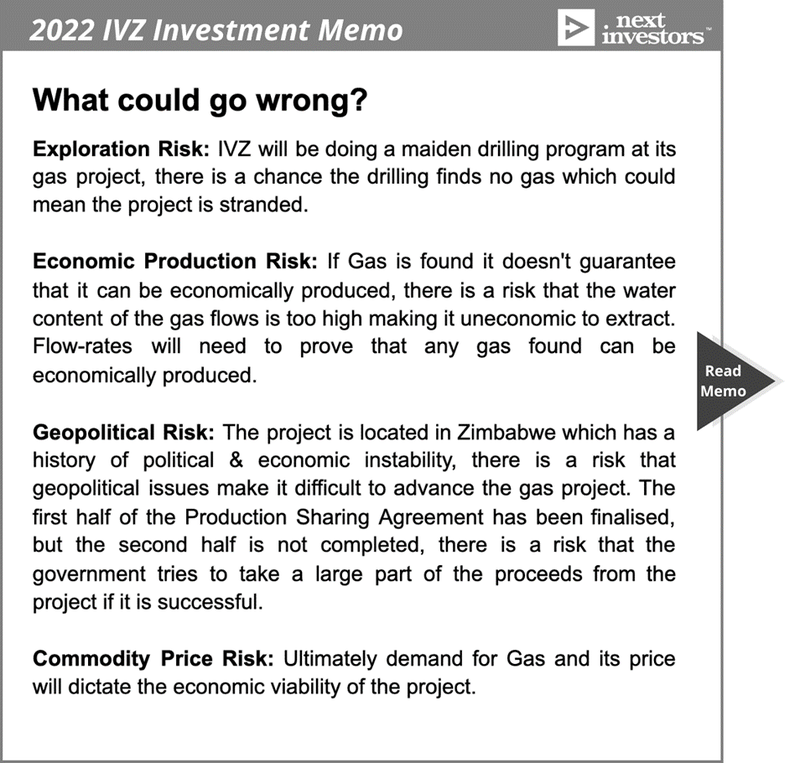

What are the risks?

As with all high risk, high reward exploration Investments, IVZ is preparing to drill a MAIDEN exploration well at its oil and gas project in Zimbabwe.

IVZ is planning two separate wells across its project area meaning we will get to see it take two shots at making a discovery. We still think it is worth noting that both of these will have binary outcomes which could see either:

- IVZ make a company making oil & gas discovery - If this happens, we expect the company’s share price to perform strongly.

- IVZ drill and discover nothing - Noting that IVZ has a second well location being planned, we want to see at least one more drilling program completed. We would still expect to see the share price perform poorly in the event nothing was found.

It is important to consider all of the risks associated with oil and gas explorers going into drilling events with two contrasting outcomes.

Below are the risks we set out in our 2022 IVZ Investment Memo, with the first being the “Exploration Risk” we mentioned above.

Our IVZ Investment Memo for 2022

Below is our 2022 Investment Memo for IVZ, where you can find a short, high level summary of our reasons for investing.

The ultimate purpose of the memo is to record our current thinking as a benchmark to assess the company's performance against our expectations 12 months from now.

In our IVZ Investment Memo, you’ll find:

- Key objectives for IVZ in 2022

- Why we invested in IVZ

- What the key risks to our investment thesis are

- Our investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.