It’s pre-drill time

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 4,249,042 IVZ shares and 130,144 options, and the Company’s staff own 60,000 IVZ shares and 10,845 options at the time of publishing this article. The Company has been engaged by IVZ to share our commentary on the progress of our Investment in IVZ over time.

Finally - it’s almost here.

Invictus Energy’s (ASX:IVZ) drill rig is now on site and about to start drilling the biggest conventional onshore oil and gas prospect in Africa.

We have been Invested and waiting for this for two years:

Our first ever significant investing success in oil & gas exploration was over 10 years ago when a company called Africa Oil Corp delivered a 1,200% surge on a successful basin opening drill result in Kenya.

Ten years later and we are back in Africa, this time in Zimbabwe with IVZ, about to drill a frontier unexplored basin.

And the macro theme for natural gas is extremely strong.

After over 700 days of waiting, our best guess is that IVZ will start drilling in September and take 30 to 45 days to drill through the six stacked targets.

We estimate the first target will be hit after ~14 days. If we get an early announcement about gas shows, it would make for a very bullish case for IVZ.

If the drill result is good (gas shows and columns announced), we expect the share price to re-rate upwards.

On a positive result we would expect larger resource funds and later stage investors to build a position in a now partially de-risked gas project, by buying shares on market from early stage IVZ investors who want to lock in a profit in return for the risk they took.

BUT, as we have observed (and experienced) over many years - most oil explorers fail to hit a commercial discovery on their first drill.

OR they may deliver a “technical success” where they learn about the geology and how to better target the next drill (which will take many months or even a year) - cue for speculators to exit.

If the result is negative then the share price will come down, possibly aggressively, as short term speculators exit and the company goes back to the drawing board to plan and fund the next campaign.

Oil and gas exploration is risky.

Our strategy is to Invest years before the drilling event. We then look to gradually Free Carry and Take Profit in the lead up to the drilling event as market excitement and speculation builds for the result, while holding a material position into the result.

We first Invested in IVZ at 3.9c back in 2020, calling it our Energy Pick of The Year. The share price has steadily risen since then. Over the journey, we Invested twice more at 11c and again at 10c, and along the way have implemented our Free Carry and Take Profit strategy on each tranche.

Share price and pre-drill speculation

As a general rule of thumb, oil & gas exploration stocks usually run in the lead up to drilling. Some more than others. Some not at all.

Our Catalyst Hunter Investments in Prominence Energy and Global Oil & Gas didn’t deliver a pre-drill run up - for a number of reasons that we covered in our post drill result analysis note.

Over the last couple of years, a few oil & gas exploration stocks HAVE had strong price runs into drilling.

The most significant price runs are often correlated to attention in online stock chat rooms.

88E saw a 1,000% plus surge off the back of pre-drilling traders and speculators, we believe driven by a cult following on Reddit in the US (88E is listed in the US as EEENF).

Unfortunately, that drill result didn’t come in.

IVZ currently seems to be very popular in Australian chat rooms, with younger investors on ASX_Bets (Australian version of Reddit’s wallstreetbets) AND with the older investors as one of the most discussed stocks on HotCopper.

We think this level of interest in stock chat rooms from young and old could make the next 8 weeks very interesting in terms of attracting attention from traders and speculators on IVZ’s drill result.

In terms of attention from the MUCH bigger pool of US investors and traders, 3 weeks ago IVZ announced a US listing via ticker code IVCTF.

We have already observed a few mentions of IVZ on US chat rooms. While there’s been nothing significant just yet, we will be keeping an eye on whether the IVZ pre-drill story gets picked up in the US over the next 8 weeks.

We also watched the significant pre-drill share price moves of Canadian listed Recon Africa, who recently drilled an exploration well in the basin next to IVZ.

Recon’s market cap went from ~$300M to a peak of ~$1.45 billion throughout its drilling program.

As a comparison, IVZ has just about mobilised its drill rig and is capped at $216M.

Short term traders probably get quite excited by the prospect of these types of price rises and liquidity, but always remember that it’s very easy to get your face ripped off if you don’t know what you are doing.

So while pre-drill run ups sound good in theory, keep in mind that there are plenty of unexpected events that can snuff out a pre-drill price run, for example:

- Global market correction - we have seen a couple of these in the last 6 months with varying levels of severity

- Delays to drilling - rig issues or drilling problems can quickly reverse a pre-drill result price rise.

- Too many profit takers - if the price runs too hard pre-drill, it can encourage too many long term holders to take profit which can dampen the run.

- Unknown - Sometimes a pre-drill run up just doesn’t happen, and nobody knows why - that’s just oil & gas exploration investing.

And even after all that - if the price runs too hard pre-drill, the result will have to be spectacular to justify it going even higher.

With oil & gas exploration, the only certain thing is uncertainty, and that each drill event, drill result and share price behaviour is different. We are not traders and we don’t attempt to move with share price momentum.

After Investing in many high impact drill events, we keep it simple and stick to our oil & gas exploration plan.

So after 2 years of waiting, we have Free Carried and Taken Profit, locked in the 12 month CGT discount and we may Top Slice another 20% before the result IF the share price really runs hard - but as always we will be holding a material position into the drill result.

Note on IVZ financing: In the last quarterly IVZ confirmed that it has received three separate farm-in offers to fund the drilling program in return for a share of the project. Now that the assignment of the additional Cabora Bassa exploration rights have been announced, we think that process can move forward - hopefully quickly.

Alternatively IVZ could “go it alone” by raising some more capital to fully fund its own drilling and retain its full current share of the project.

So while we all count down the days to the drill commencing, here is a stroll down memory lane to when we first announced IVZ as our Energy Pick of the Year in September 2020 at 5.3c:

We are very excited for the next few weeks and hope to see a great drill result and pre-drill price run.

Below is our commentary on what happened with IVZ this week.

What happened this week?

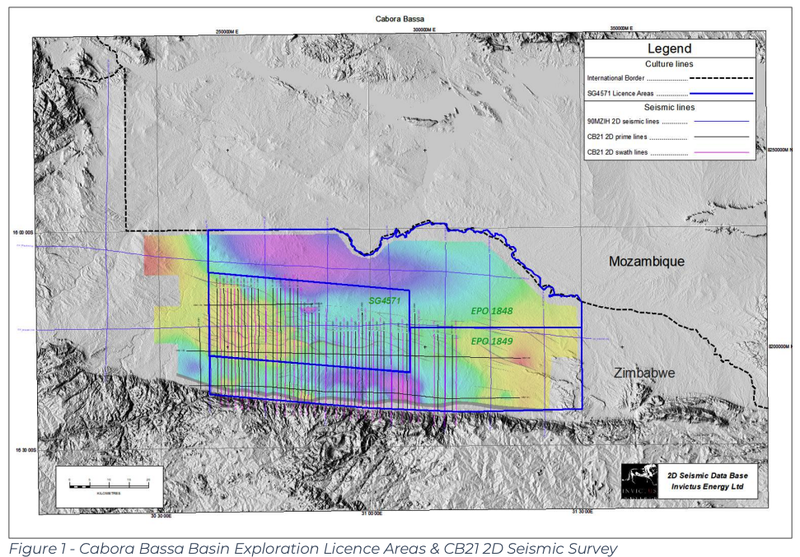

Yesterday IVZ increased the stakes for its projects by confirming that it now has full exploration rights over the entire Cabora Bassa Basin in Zimbabwe.

The announcement came after an agreement was executed with the Sovereign Wealth Fund Of Zimbabwe, assigning the exploration rights over the two remaining blocks inside IVZ’s acreage.

With the exploration rights signed over, IVZ now controls ~360,000 hectares of ground and, more importantly, has now confirmed that a second well will be drilled to target the “basin margin play”.

The whole area is huge - you can see it on the map below - basically the coloured stuff is IVZ’s:

With that agreement now signed, and the drilling site preparations well underway, this now means IVZ is only a few weeks out from starting a planned two well drilling program as follows:

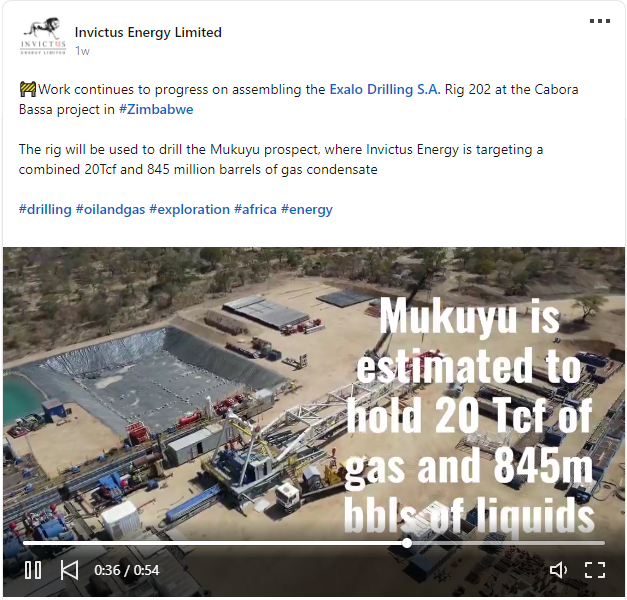

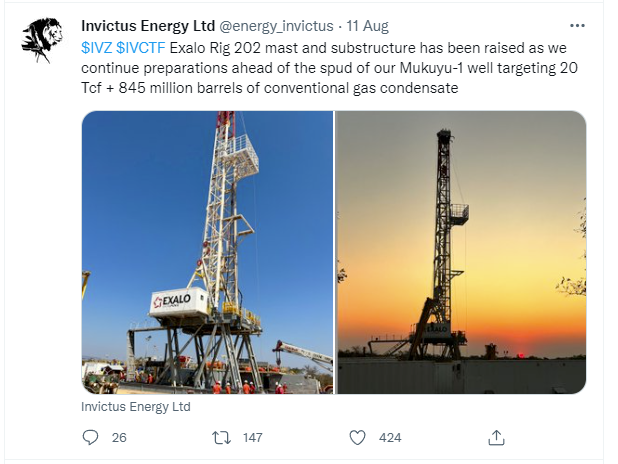

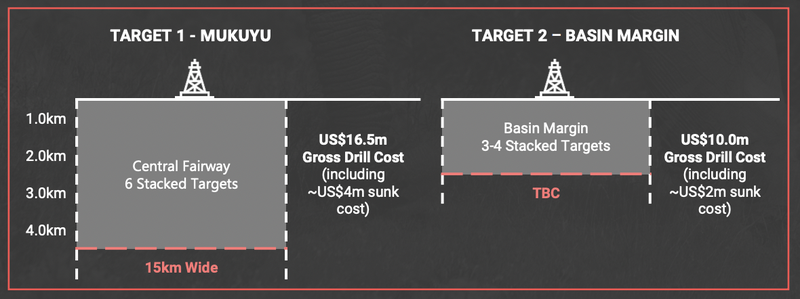

- The Mukuyu-1 well - Targeting 20 trillion cubic feet (Tcf) of gas and 845 million barrels of gas condensate (Prospective resource of ~4.3 billion barrels of oil equivalent on a gross mean unrisked basis).

- The Baobab-1 well - Targeting the basin margin play, which IVZ compares to the prolific East Africa Rift “String of Pearls” play. This play provided material discoveries in the Lokichar Basin in Kenya and Albertine Graben in Uganda.

This week's news puts IVZ in a position whereby if it makes a basin opening discovery with either Mukuyu-1 or the Baobab-1 well, it will have complete control over what happens with the remainder of the basin.

This will mean that should a large-scale discovery get made, any other company looking for exposure to the basin will need to pick up the phone and call IVZ.

In a presentation released earlier this year, IVZ said it expected its first well (Mukuyu-1) to cost ~US$16.5M and the follow up basin margin well to cost another US$10M.

Having paid some of the mobilisation costs for the Mukuyu-1 well, IVZ ended the June quarter with $13.8M in cash.

Doing the simple maths tells us that the two-well drill program is not yet fully funded.

On that front, IVZ recently confirmed that it had received “multiple farm-in offers” during the June quarter.

We are hoping to see IVZ close out a farm-in agreement which would see the partner finance the bulk of the drilling costs for as minimal a share in the project as possible.

Alternatively, we want to see IVZ go out and raise enough equity to finance the drilling program itself.

With drilling now a few weeks away, we are hoping to see this get sorted very soon, as we think this uncertainty might be holding the share price back.

Basin Margin play could be a game changer:

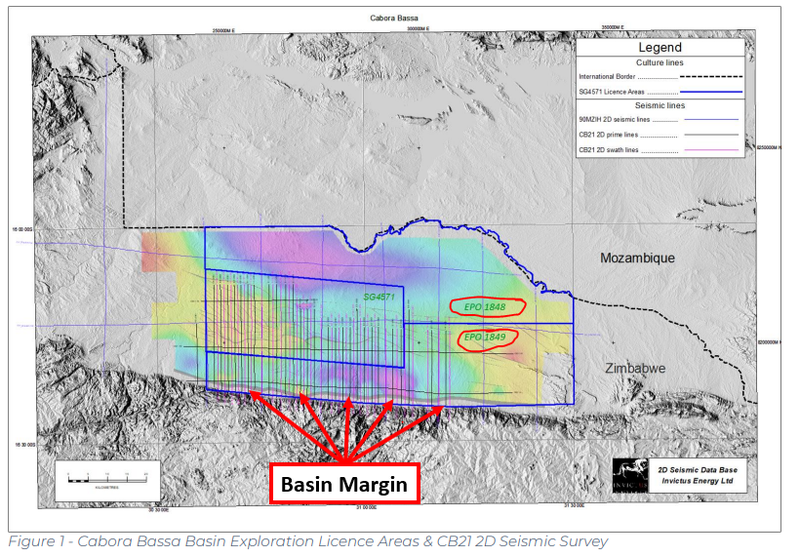

The key takeaway from yesterday’s news is that IVZ now holds all the exploration rights over the entire Cabora Bassa Basin.

Previously IVZ only held exploration rights over SG 4571. Yesterday it was granted EPO 1848 and EPO 1849, increasing IVZ’s exploration acreage area to ~360,000 hectares.

You can see these in the image below and we have pointed out the all important basin margin:

Most important for IVZ is the granting of exploration rights over the “Basin Margin”, which is all along the southern border of IVZ’s ground.

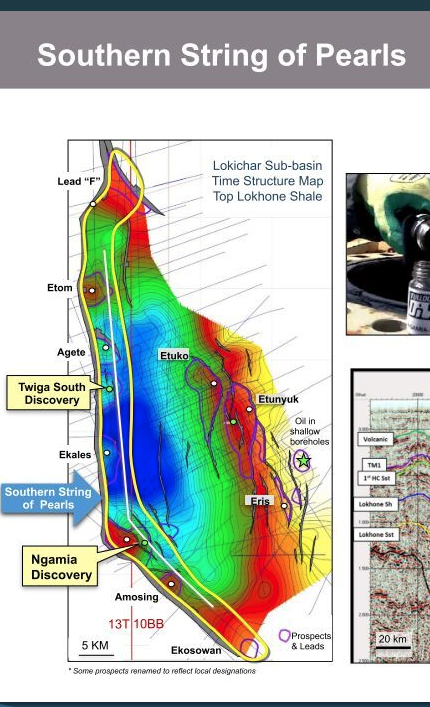

This is important because IVZ thinks its “Basin Margin” displays similar structural characteristics to the prolific East Africa Rift “String of Pearls” play and provided material discoveries in the Lokichar Basin in Kenya

Africa Oil Corp (our first oil & gas success in 2012) was the company that owned and discovered the Lokichar Basin and drilled out the string of pearls - so we are very familiar with this approach.

With the exploration rights granted, IVZ has now committed to a second well targeting the basin margin play with the commitment to drill the Baobab-1 well,

Baobab-1 is the first in a possible ‘string of pearls’ of structurally similar targets on the newly acquired basin margin.

Why is this interesting?

Like IVZ, Africa Oil Corp drilled its first basin opening well in a “string of pearls”, which basically means multiple structurally similar targets across similar geology along a basin margin.

Success on the first ‘string of pearls’ well means the other similar targets (pearls) are more likely to be successful too.

Here is Africa Oil corps ‘string of pearls’ on the Lokichar basin margin - nearly every single one delivered a significant result:

Source: Africa Oil investor presentation 2013

IVZ is now in a position whereby its Baobab-1 well could make a discovery to kick off its string of pearls exploration.

If the Baobab-1 well comes in, IVZ can expand on this by growing the size and scale of its project with its own set of “pearls” along the basin margin.

This is useful because if the Mukuyu-1 well doesn't come in, IVZ will still have another shot at a discovery all along the basin margin.

Drill rig update:

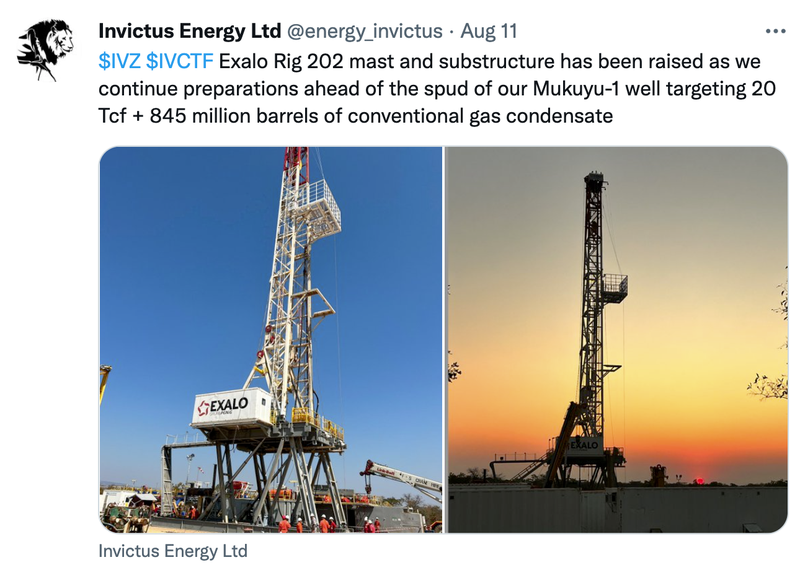

A week or so ago, IVZ also released a video update on the Exalo 202 rig being mobilised on site at the Mukuyu-1 well pad.

Click on the image below to view that video.

IVZ also put out an update on its Twitter account, which you can follow by clicking on the image below:

IVZ’s carbon offset venture: The world’s first carbon-free oil and gas project?

A few weeks back, IVZ also announced the award of three different carbon offset projects, which could potentially make its oil and gas project the first “cradle to grave” carbon neutral project in the world.

In this case, “cradle to grave” means that carbon neutrality is secured from exploration through to production and the end of the project's useful life.

IVZ’s three carbon offset projects cover ~301,565 hectares of indigenous forests and give IVZ tenure over the project for an initial ~30-year term.

The three projects are the “Ngamo, Gwayi and Sikumi projects”, which are classified as potential carbon offset projects under the Reducing Emissions from Deforestation and forest Degradation (REDD+) framework.

REDD+ is a framework created by the United Nations with the ultimate aim of reducing carbon emissions by preventing deforestation and forest degradation.

This essentially means IVZ would receive carbon credits for the work the company puts in to protect the three projects from deforestation.

Instead of planting new trees and waiting for them to mature before the carbon capture begins, the existing trees can suck up a lot more carbon dioxide NOW. So to us, the thinking behind this project makes sense.

IVZ is a 50:50 partner with the Forestry Commission of Zimbabwe and will develop deforestation programs to protect the indigenous forests as a joint venture.

Not only does the program allow for IVZ’s project to achieve carbon neutral status, but under the REDD+ framework, this could generate excess carbon credits that IVZ can sell on the open market.

IVZ is now going through the verification process to get the carbon credits recognised up to the point where they are tradable, with the company expecting this to take ~12 months to complete.

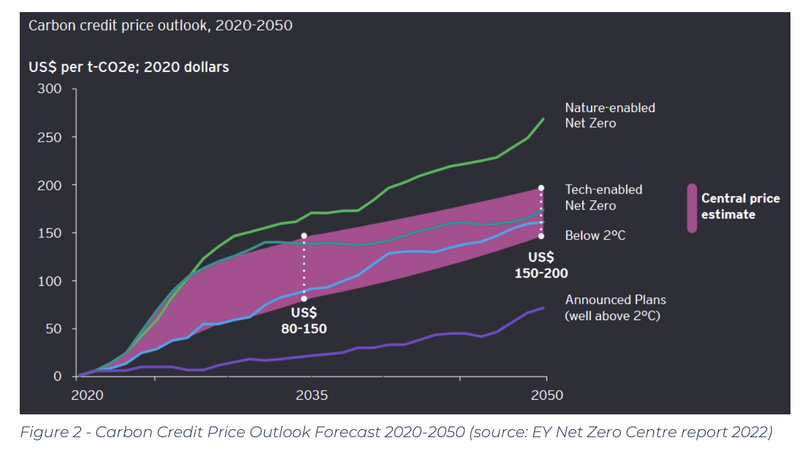

With carbon credits forecast to be worth US$80 to $150/tonne in 2035, IVZ is proactively working to reduce the company's overall carbon footprint by achieving carbon neutral status for its oil and gas project.

At the same time, the company has opened up another source of potential revenue for IVZ in the future should the REDD+ framework verify its projects qualify for tradeable carbon credits.

What’s next for IVZ?

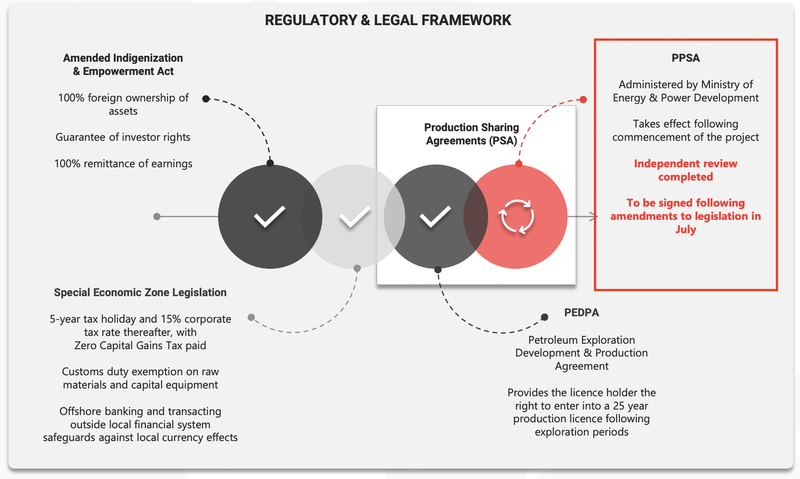

Production sharing agreement 🔄

IVZ is currently awaiting formal governmental approvals for the Production Sharing Agreement over its extended acreage position.

We are hoping IVZ can resolve this before IVZ starts drilling - given that the Production Sharing Agreement will particularly govern the ownership rights IVZ has over a commercial discovery (assuming a discovery is made).

Binding Farm-in agreement to be signed 🔄

In its most recent quarterly, IVZ put out an update on its farm-in progress.

IVZ has now confirmed that it has received three separate farm-in offers, including an updated bid from Cluff Energy Africa.

It also confirmed that “ongoing due diligence and internal approvals are being undertaken by additional parties which may result in further bids being received”.

This suggests that the company is receiving a lot more interest now.

After yesterday’s news giving IVZ full exploration rights over its entire project, we are hoping the size and scale potential of IVZ’s project creates FOMO (fear of missing out) amongst the parties interested in farming into the project.

With IVZ now committed to a two well drilling program, the forward picture should look pretty clear for anyone looking to get some exposure to the drilling program.

We are now expecting a vastly improved offer than the one that Cluff Energy Africa had put in for the project in late 2021.

Fully financing the two well drilling program 🔲

In a recent investor presentation, IVZ provided updated cost estimates for both the Mukuyu-1 well and its follow up basin margin well.

IVZ ended the June quarter (30 June 2022) with ~$13.8M in cash but also touched on how some of its funds had been used to cover some of the costs early in the Mukuyu-1 drilling program.

This should mean IVZ is going into the drilling of the first well with enough cash to fund most of the first well. Still, ideally, we would like to see the company de-risk its cash commitment further either via a farm-in agreement or through additional capital raises.

Having now committed to a two well program, IVZ will still need to shore up its balance sheet and look to finance the second well, which is expected to cost ~US$10M.

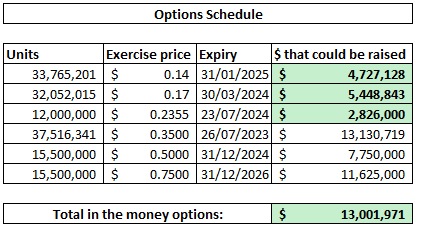

We also note that IVZ still has ~$13M in options in the money at the current share price, which could be exercised to help finance the drilling program.

The major catalyst - DRILLING now expected this month 🔲

At this point of the article, this one needs no further explanation.

With the Exalo 202 rig on site and being mobilised, IVZ has repeatedly said that drilling at Mukuyu-1 should start this month (we reckon it will be early September).

We expect to see some progress on this front in the coming weeks.

What could go wrong?

The obvious risk for IVZ is “exploration risk”.

No matter how much preparation work goes into a drilling program, the ultimate determinant of success or failure is always what comes from the drilling program.

We have been investing for two decades now and have often seen big drilling programs return nothing. As a result, it is important to understand the risks of drilling programs like IVZ’s.

IVZ is planning two separate wells, first at Mukuyu-1 and then at Baobab-1, meaning the company should have two shots at a discovery.

Both wells will ultimately produce one of the following three outcomes:

- IVZ makes a company-making oil & gas discovery - If this happens, we expect the company’s share price to perform strongly.

- IVZ drills and discovers nothing - If this happens, we expect to see IVZ’s share price fall significantly.

- IVZ drills a “technical success” but makes no discovery - This is where IVZ learns more about the geology of the project before planning another follow up drilling program. Despite this being OK news for IVZ, we would still expect the share price to fall off the back of this outcome.

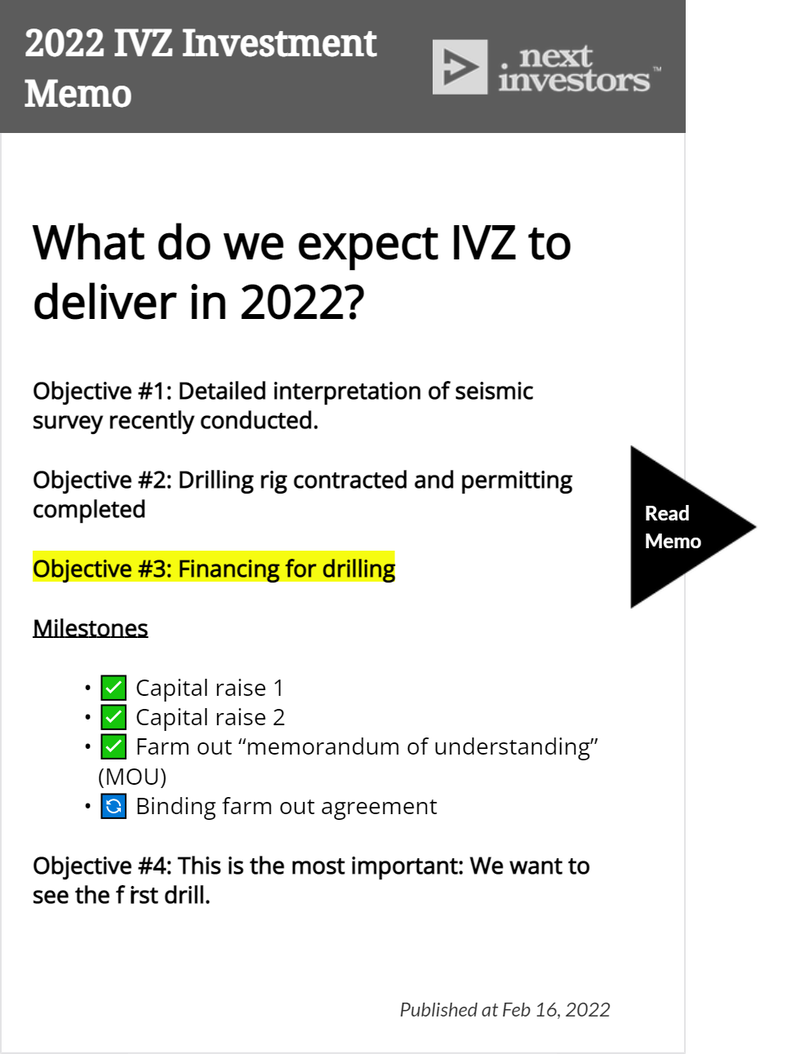

We set out some of the key risks to our Investment thesis in our 2022 IVZ Investment Memo, which you can see in detail by clicking on the image below:

Progress of Our Investment plan

Our strategy is to Invest years before the drilling event. We then look to gradually Free Carry and Take Profit in the lead up to the drilling event as market excitement and speculation builds for the result, while holding a material position into the result.

We first Invested in IVZ at 3.9c back in 2020, calling it our Energy Pick of The Year. The share price has steadily risen since then. Over the journey, we Invested twice more at 11c and again at 10c, and along the way have implemented our Free Carry and Take Profit strategy on each tranche.

Our IVZ Investment Memo for 2022:

Below is our 2022 Investment Memo for IVZ, where you can find a short, high level summary of our reasons for investing.

The ultimate purpose of the memo is to record our current thinking as a benchmark to assess the company's performance against our expectations 12 months from now.

In our IVZ Investment Memo, you’ll find:

- Key objectives for IVZ in 2022

- Why we invested in IVZ

- What the key risks to our investment thesis are

- Our investment plan

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 4,249,042 IVZ shares and 130,144 options, and the Company’s staff own 60,000 IVZ shares and 10,845 options at the time of publishing this article. The Company has been engaged by IVZ to share our commentary on the progress of our Investment in IVZ over time.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.