Pantera Drilling Next Month. $7.8M Market Cap. $5.8M Cash. $2M Enterprise Value

Disclosure: The authors of this article and owners of Next Investors, S3 Consortium Pty Ltd, and Associated Entities, own 2,410,000 PFE shares and 227,500 PFE options and the Company’s staff own 25,000 PFE shares at the time of publication. S3 Consortium Pty Ltd has been engaged by PFE to share our commentary and opinion on the progress of our Investment in PFE over time.

It’s rough out there.

Equity markets have been hit hard in recent weeks, and small cap companies short on cash are being hit the hardest.

As such, many of these pre-revenue companies will look to slow down spending, which normally translates into very limited exploration or other costly (but potentially value adding) business activities.

Several of our Investments are in the position of having a relatively solid amount of cash on hand (at least compared to their market caps). This means they don’t have to go into capital preservation mode but can continue with planned exploration programs.

Our multi-commodity micro cap Investment Pantera Minerals (ASX:PFE), which listed in August last year, is one such example.

As of 29 April, PFE held $5.8M cash in the bank - quite healthy for a micro cap stock.

At its current 10c share price, PFE has a market cap of $7.8M, so the company PFE is trading with an enterprise value (EV) of $2M.

Rather than just sit on its hands and preserve capital, PFE is full steam ahead, advancing several projects in its exploration stable in the effort to deliver value for shareholders.

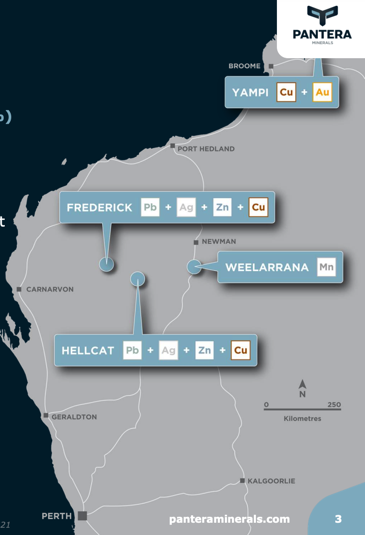

PFE has four WA exploration projects with potential for a discovery, prospective for a host of commodities including lead, zinc, iron and manganese.

There are two in particular that are about to get interesting with maiden drilling programs set to kick off next month.

Despite being down from our Initial Entry Price point of 20c, we like the leverage to a discovery that PFE has right now, given its tiny enterprise value and upcoming drilling programs.

Drilling is typically the period of most excitement for juniors - especially when it is the first drilling program on freshly identified targets.

Once the rigs arrive on site, the allure of a company-making discovery becomes a near term possibility.

There is a reason that drill rigs are sometimes referred to as ‘lie-detectors’: they deliver the assays that provide the truest insight into what riches, or lack thereof, are found under the surface.

However it can sometimes take a couple of drilling campaigns to latch onto something of value, and patience is important when it comes to early stage exploration.

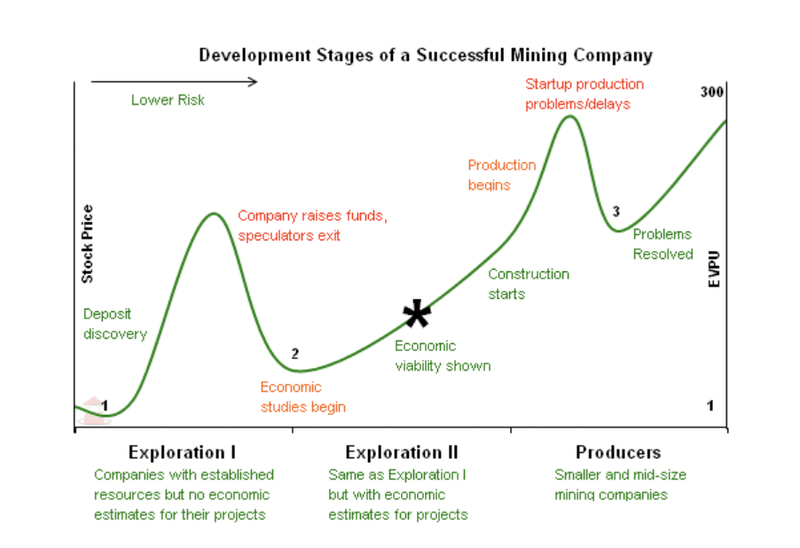

Below is the typical life cycle of a mineral discovery - more details can be read here.

Of the thousands of junior exploration companies advancing their multitudes of projects, only a very, very small number ultimately become producing operations. As you can see, those that do enter into production tend to deliver substantial returns to early investors.

However, you can note from the chart below that large returns are often also made during the drilling to discovery phase as investor interest and hype heightens.

That said, no matter where in the life-cycle an explorer is, only a very few successfully make it to production and thereby cashflows and possible dividends.

These are the ones that create long-term shareholder value and this is the hope of just about every maiden drilling campaign launched.

The two PFE projects where initial drilling is about to commence are:

- Hellcat - a polymetallic project near $73M capped Galena Mining’s globally significant base metals discovery

- Weelarrana - manganese project with promising rock chip results near $67M capped Element 25’s Butcherbird project, Australia’s largest onshore manganese deposit

We’ll go into more detail on these projects later below, and will also touch on another project with drilling anticipated before year-end.

As we highlighted above, with $5.8M cash and a market cap of just under $7.8M, PFE has an enterprise value of just $2 Million.

Having an enterprise value this low, means PFE could significantly re-rate higher if a new discovery is made across either of its projects in the coming months.

PFE is exploring for a diverse suite of commodities within its tenements, including iron-ore, lead, zinc, silver, copper and manganese, providing exposure to an early stage discovery in what we expect to be the coming commodity super-cycle.

On the corporate front, PFE recently completed a pro-rata non-renounceable rights issue to raise $193,750. This provided existing shareholders the opportunity to buy options for $0.01 each, which have a strike price of $0.25 and are exercisable on or before 1 May 2026.

We liked this offer, given the downward trending share price, this loyalty offer gave investors the opportunity to gain additional exposure to the upside of a metals discovery.

PFE is currently well funded to complete all its drilling campaigns in 2022, and more importantly, taking multiple shots at making an entirely new and potentially company-making discovery.

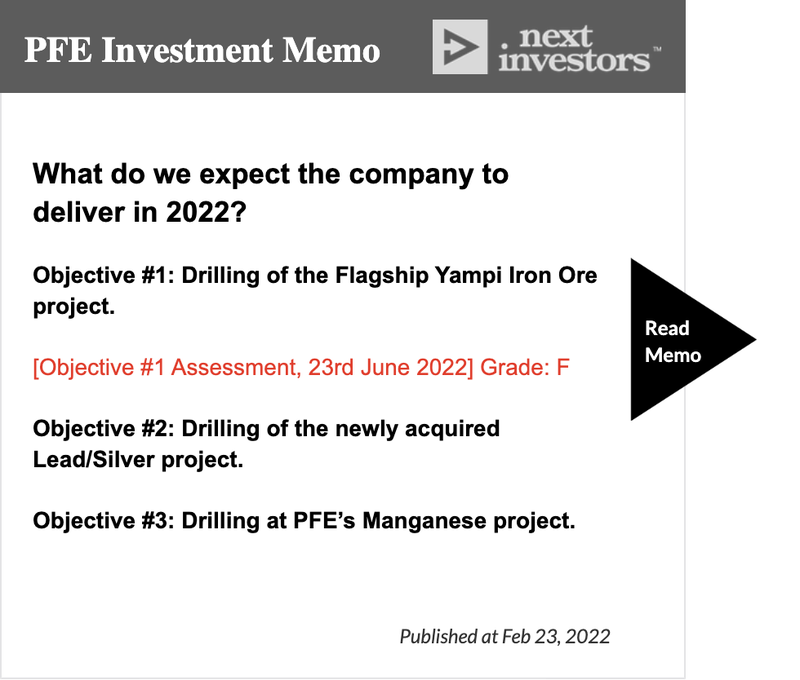

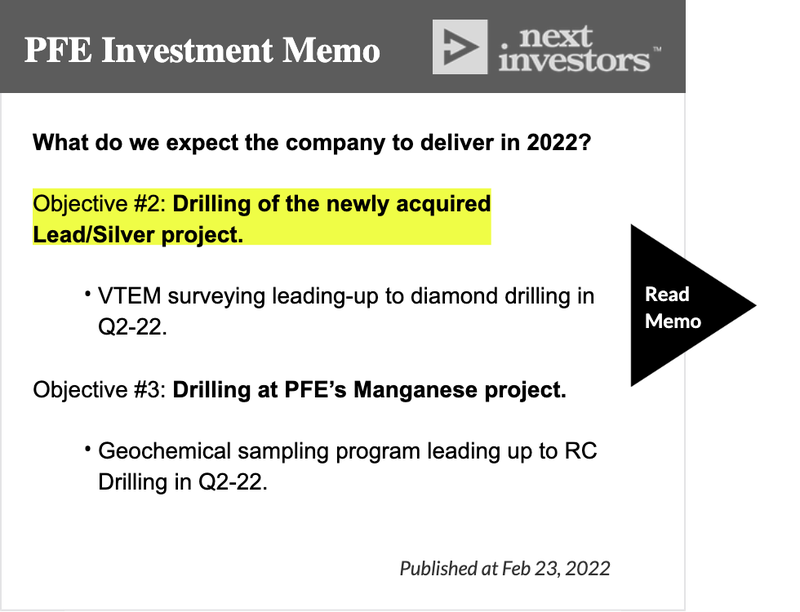

This is one of the key reasons we hold PFE in our portfolio, highlighted by Objectives 2 and 3 within our PFE Investment Memo. Of note, our #1 Objective has not delivered the results we were hoping for, which we will go into more detail later.

To see all of the key reasons check out our 2022 Investment Memo by clicking the image below:

The map below shows the location of PFE’s projects in WA, and the prospective metals that could be discovered in each:

Drilling hell for leather - let’s look at Hellcat

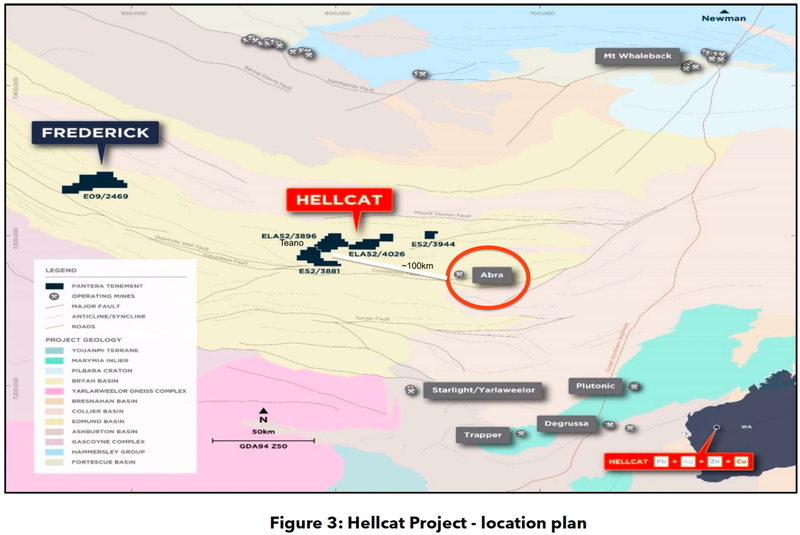

Last week PFE announced the completion of a heritage survey at its Hellcat polymetallic project in WA’s Edmund Basin

This paves the way for its maiden drilling program — an 1,800 metre diamond drilling program that is set to commence early next month.

PFE owns an 80% interest in the Hellcat Project, which it acquired in December 2021.

Hellcat is just down the road from one of the region’s most significant discoveries — the ‘Abra’ polymetallic deposit that’s being developed by ASX-listed Galena Mining (a company capped at $76M - about 10 times that of PFE).

Modified source: ‘Pantera Acquires Exciting Abra-Style Lead-Silver Project’ ASX announcement 23.12.21

Abra is one of the most significant mineral discoveries in the region, with a JORC inferred resource of 34.5mt at 7.2% lead and 16g/t silver.

With around two-thirds of the project construction completed, once operational, Abra is expected to operate for an initial 16 years, producing 95 ktpa of lead alongside byproducts.

Abrat has also managed to attract Japanese smelter Toho Zinc to invest alongside owner Galena Mining, forming a 60:40 joint venture (Galena is the majority holder).

First lead and silver production is now slated for 2023.

We like that PFE’s Hellcat sits over similar geological fundamentals as the Abra project, and shares an almost identical geophysical signature.

We are looking forward to the maiden drill program on PFE’s ground, and are hoping for some intersections that provide motivation to keep exploring here.

With drilling on the horizon, first assay results could arrive as soon as the next quarter.

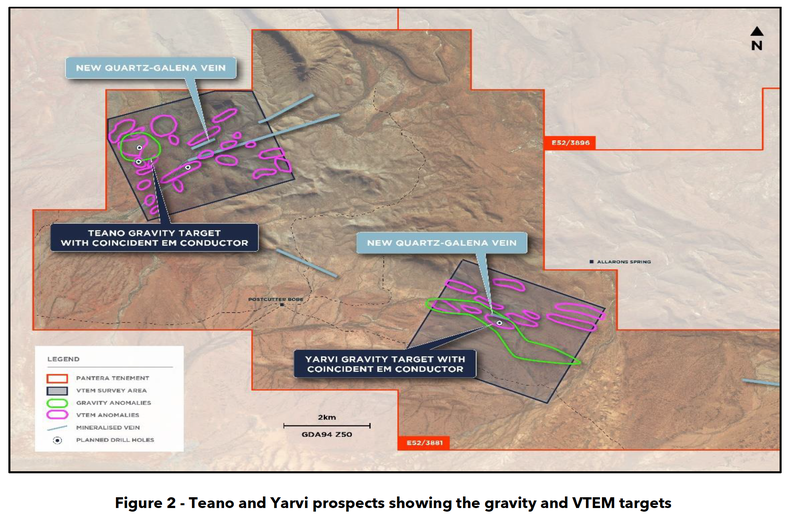

The Teano prospect will be an area of interest for the first holes. We covered why this prospect is of particular interest in our last PFE note, which you can read here: Pantera acquires “Hellcat” polymetallic project.

Also of note is that PFE’s Frederick base metals project is located nearby. This project has the potential for Pb, Ag and Zn (i.e. similar to Hellcat and Abra).

We will be watching to see PFE put out its forward plan for Frederick either while drilling at the Hellcat project or immediately after it.

This all contributes to Objective #2 of our 2022 PFE Investment Memo being achieved.

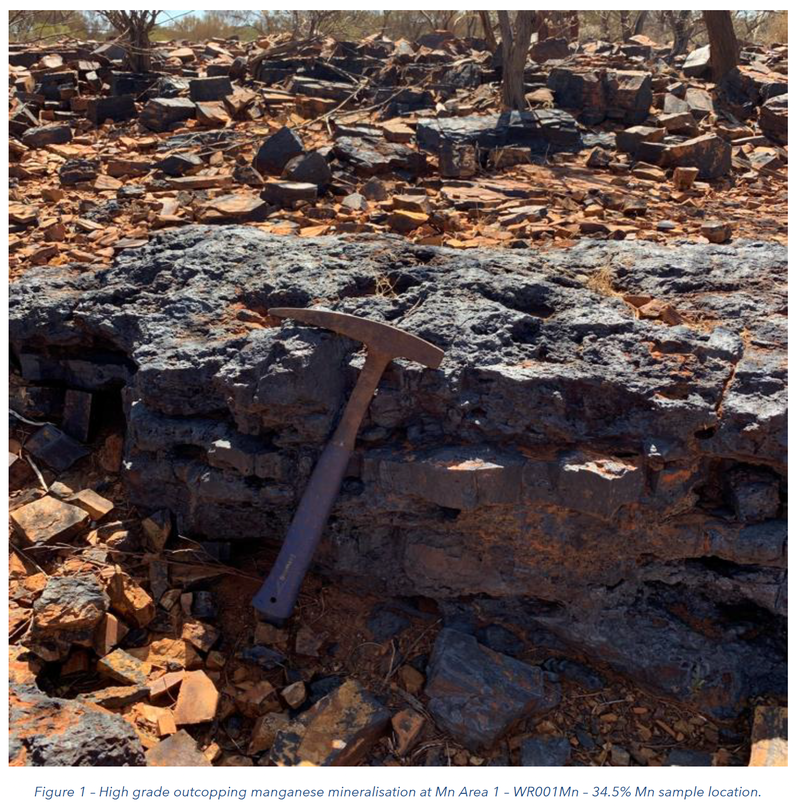

PFE’s Weelarrana holds manganese promise

PFE recently completed a heritage survey at its Weelarrana project — meaning the rigs can now be mobilised here too.

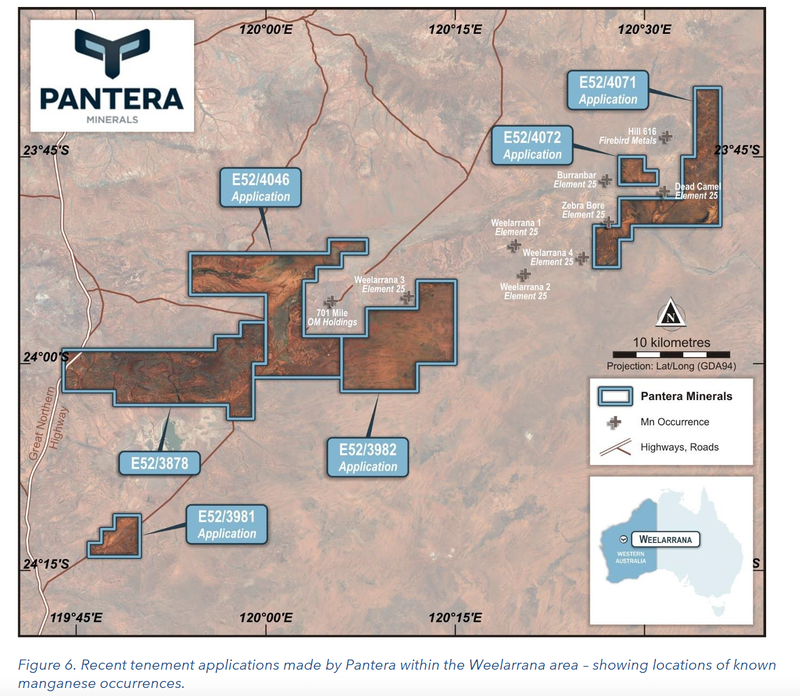

Weelarrana is PFE’s manganese project in the Pilbara, about 70km south of Newman. It is in the same geological neighbourhood as the 701 Mile Manganese Project (owned by ~$600M capped ASX-listed OM Holdings) and ASX-listed Firebird Metals’ (capped at ~$16M) Hill 616 Project.

There has already been some historical exploration work done at Weelarrana with previous results returning high grade manganese (between 11% to 43% grades) from 16 out of 22 rock chip samples.

Three areas of outcropping high grade manganese mineralisation have now been identified along a strike length of ~280 to 800m, with large parts of the tenement area yet to be assessed.

Now the heritage surveys are complete, the stage is set for PFE’s maiden 1500m RC drilling program next month.

In early May, PFE increased its landholding in the area from 401 km2 to 758 km2 with three new tenement applications - a positive sign should PFE make a discovery here.

The drilling campaign will comprise two phases.

The first phase in July is for 25 RC drill holes at MA1 (MA stands for Manganese Area) for 1,000 metres.

Then, in September, a further 500m will be drilled at MA2 and MA3.

We expect to start seeing the results from this drilling program towards the end of this year, which should mean PFE tick off key objective #3 of our 2022 Investment Memo.

On the macro front, the manganese market has been strong in 2022, particularly for high purity manganese.

Whilst the primary use for manganese remains in steelmaking, demand growth has been on the rise of late as part of the battery metals boom. Manganese can be used as a substitute for higher cost inputs such as cobalt and nickel within lithium ion batteries, whilst maintaining energy density.

We believe that manganese is a promising space to be involved in.

What happened to PFE’s iron ore?

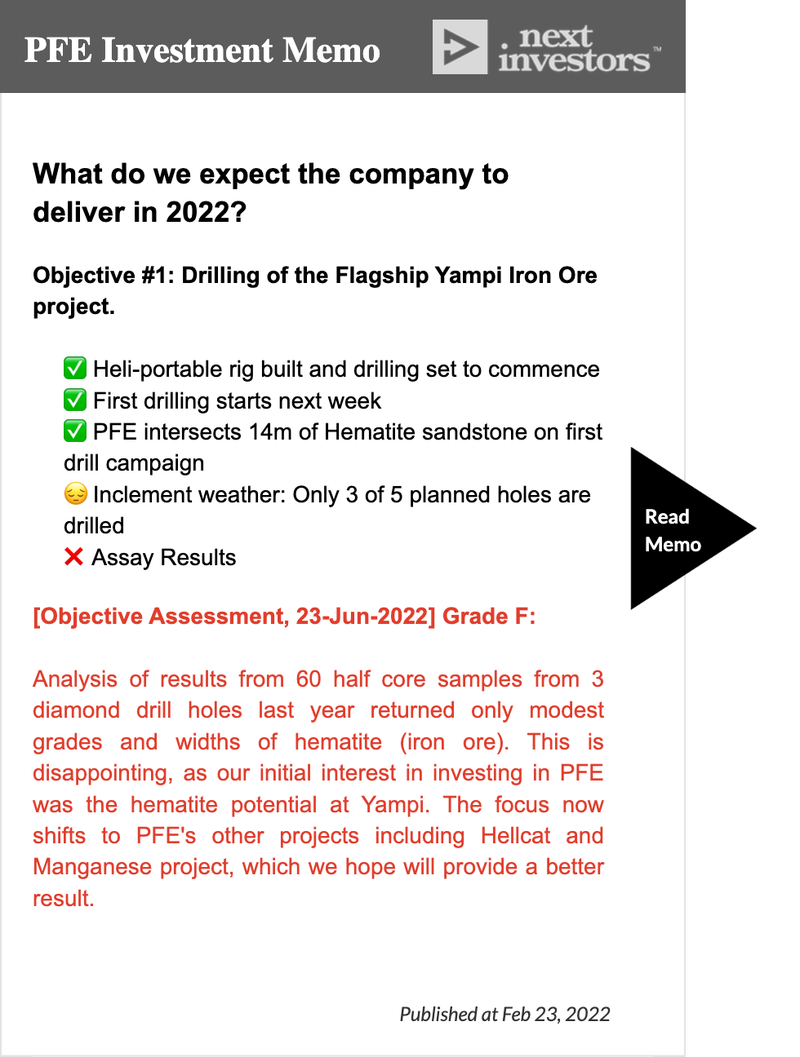

Regular readers will know that we initially Invested in PFE for its exposure to its Yampi project, a high grade iron ore project near to Mt Gibson’s Koogan Island operation (the highest grade iron ore mine in Australia).

PFE would be following up from initial promising early exploration at Yampi, post listing. This was the #1 Objective we wanted to see PFE deliver.

However, in late April, PFE announced an update on Yampi, essentially relegating this project to the bench.

This followed analysis of results from the three diamond drill holes completed last year, all of which returned only modest grades and widths of hematite ore.

This was obviously a disappointing result, especially given the optionality PFE would have had at its disposal if it had managed to intercept anything indicative of a new discovery, given how near it is to the Koolan Island operation.

We have updated our PFE Investment Memo accordingly:

Whilst the iron ore grades have not impressed, somewhat interesting is that several pathfinder elements for porphyry copper-gold mineralisation were encountered. This is of note as Yampi is near the promising Orion Copper Project (owned by Dreadnought Resources), with structures that extend well within PFE’s tenements.

The presence of these pathfinder elements warranted PFE to greenlight an aeromagnetic and radiometric survey over the majority of Yampi, which was recently completed - results still to come. The ultimate aim for this program will be to help narrow down where to focus the next exploration campaign to hunt for a possible copper/ gold porphyry.

It is not uncommon for junior explorers to pivot to new projects following disappointing results at their previous flagship project. The rationale is that resources can be better applied to determine the prospectivity of other projects within the pipeline.

In addition, market and commodity interest often changes, and so it may be a better allocation of resources to fund exploration of in-demand commodities.

A case in point is Chalice Mining which was initially targeting gold/vanadium across its Julimar project.

After shifting focus to PGE’s and nickel, the company went from junior explorer to market darling with a market cap of $1.4 billion.

And so PFE has committed its resources to progressing campaigns at a number of its other non-Yampi projects.

That is not to say that PFE will completely abandon Yampi - we suspect they will return to the project down the road.

It is just that the company has several promising projects, so it makes sense for management to determine if it has a company-maker in its entire suite.

Our PFE Investment Memo for 2022

Below is our 2022 Investment Memo for PFE where you can find a short, high level summary of our reasons for investing.

The ultimate purpose of the memo is to record our current thinking in order to benchmark the company's performance against 12 months from now.

In our PFE Investment Memo you’ll find:

- Key objectives we want to see PFE achieve in 2022

- Why we invested in PFE

- What the key risks to our investment thesis are

- Our investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.