PFE to own 100% over 10,000 acres in the Smackover Formation: USA’s new lithium hotspot

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 3,210,000 PFE shares, 494167 PFE options, and 7 Daytona Lithium shares at the time of publishing this article. The Company has been engaged by PFE to share our commentary on the progress of our Investment in PFE over time.

It's one of the hottest real estate markets out there.

(and no it's not a crumbling inner city townhouse in an Australian capital city.)

It’s for lithium acreage in the Smackover Formation of Arkansas, USA.

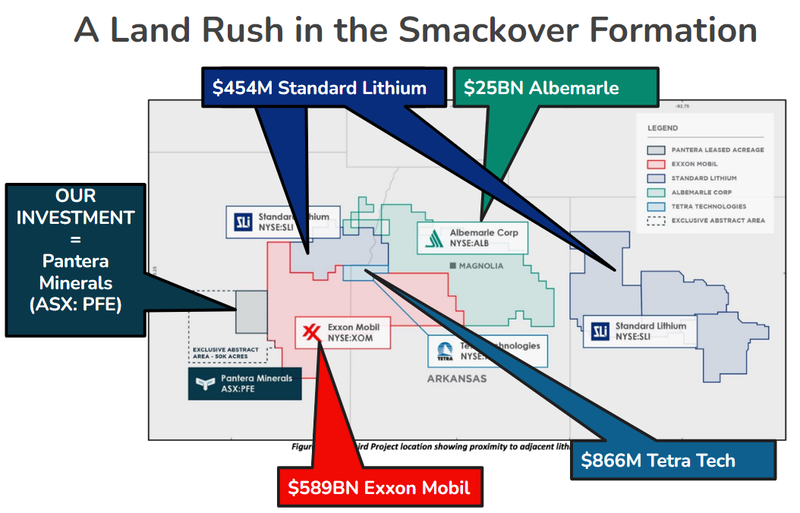

Exxon Mobil paid over US$100M for 120,000 acres in the Smackover.

(Yes, Exxon the $589BN oil supermajor is now moving into lithium extraction.)

NYSE listed Standard Lithium has 63,000 acres in the Smackover and is capped at $468M.

NYSE listed Tetra Technologies has 5,100 acres and is capped at $866M.

Lithium giant Albemarle has ~140,000 acres in the Smackover and is capped at $24.7BN.

Our Investment Pantera Minerals (ASX:PFE) just signed a deal that will give it full control over 10,000 acres (plus a further 9,000 acres under negotiation) in the Smackover.

+50,000 acres is the ultimate goal for PFE (we explain how they can get there further down).

PFE is currently capped at $5.5M - a tiny fraction of the much bigger companies around them.

PFE’s acerage is directly next door to Exxon Mobil:

Why the Smackover?

Well, it turns out that certain historical oil fields also contain lots of lithium rich brines underground.

The Smackover Formation is one of those - a former oil field, it is now prime real estate for pulling out lithium brine and selling to battery makers via a method called “Direct Lithium Extraction”.

Joe Lowry, also known as “Mr Lithium”, has said that if Direct Lithium Extraction (DLE) is going to work at scale - “it is going to be in the Smackover”.

This is because of the superior concentration of lithium in brine found in the Smackover Formation compared to other areas in North America.

And there's now a race on to secure the best acreage in the Smackover Formation - just like the shale boom in the early part of this century.

And like we have seen with the WA lithium boom, once the big dogs and their big balance sheets enter a region, it can get interesting for small players.

PFE also announced that Mr Tim Goldsmith has been appointed as Strategic Advisor - he was CEO of Rincon Mining when it was acquired by Rio Tinto for $825M early last year.

Given that Rincon Mining was the first major lithium brine success story on the ASX, Goldsmith has the necessary contacts and industry expertise to help PFE advance its USA lithium brine project - particularly around the use of Direct Lithium Extraction (DLE) technology.

Earlier this week, micro cap PFE sealed a deal to acquire 100% of over 10,000 acres in the Smackover Formation - most of which was sewn up before those other much bigger companies could get their hands on it.

Given the prices being paid by Exxon for acreage, we wonder, how much would some of the bigger players be willing to pay for PFE’s ground now?

The Smackover has become a bustling hub of lithium exploration and development activity in the last couple years.

Companies capped at many multiples of PFE are jostling to advance brine projects in the region, including none other than energy supergiant ExxonMobil.

With PFE’s acquisition of Daytona Lithium, the company now has 100% of the rights to “10,319 acres under lease, and a further 9,000 acres under negotiation”.

And as a result we think, more valuation upside in the event it is able to get high grade lithium brines to the surface.

As we highlighted above, land rights are important here - in May ExxonMobil forked out over US$100M for Galvanic Lithium which held ~120,000 acres in the Smackover:

(Source)

Just like the shale boom, where more land meant more oil - we have history repeating - only this time for battery powered electric cars.

More land, more lithium.

That’s the idea.

Again, PFE’s land leasing is taking place in an area that is immediately next door to ExxonMobil’s lithium project in the Smackover.

Shortly after making the acquisition of Galvanic, ExxonMobil announced its intention to produce lithium out of the project by 2027, providing enough of the battery metal to power over 1M EVs per year.

What did PFE pay for the project?

To make the 100% acquisition of Daytona Lithium (the private company that owned the Smackover acreage), PFE completed a $2M capital raise at 5c per share.

This will proceed in two tranches, the first of which is for 40M shares and a second tranche of 24M shares which is subject to shareholder approval.

There was a 1 for 2 options deal with the capital raise, the options strike price is 10c with a 3 year term.

We participated in this placement.

PFE is currently capped at ~$5.5M and trading at ~5c, at time of writing.

In addition to the capital raise, PFE will also be issuing 106.4M shares to Daytona shareholders initially as consideration for the acquisition, half of which will be escrowed for 12 months. Pending milestones, a further 22.4M will be issued to Daytona shareholders.

Ultimately, on shareholder approval and the issuance of the Daytona shares, we expect PFE will have ~250M shares on issue, a market cap of ~$12.5M at 5c and an EV of ~$10M (assuming $2M in cash held).

All up, if PFE is able to complete its forward works at its lithium project - we see that as a relatively small valuation relative to its potential to play a growing role in the Smackover, surrounded by much bigger peers.

Early mover advantage on acreage and IP needed to expand further

PFE holds a land position of 10,319 leased acres and has a further ~9,000 acres under negotiation at the time of writing.

With a view to pursuing an “aggressive” leasing strategy, the idea here is to rapidly expand land position to enable the largest possible resource.

PFE is aiming to secure +50,000 acres.

Leasing land for lithium exploration in the Smackover Formation is being facilitated by a proprietary database and an exclusive agreement with a commercial leasing abstract company, which is the only provider in the region.

To our understanding, leasing abstract companies are capable of tracking down complex mineral rights networks in these southern states - allowing companies to enter into leasing negotiations.

This provider is engaged to help PFE lease a further 50,000 acres.

Lithium brine and DLE expert joins PFE as Strategic Advisor

In an additional coup for PFE, the company announced that Mr Tim Goldsmith has been appointed as Strategic Advisor - Goldsmith was CEO of Rincon Mining when it was acquired by Rio Tinto for $825M early last year.

Given that Rincon Mining was the first major lithium brine success story on the ASX, Goldsmith has the necessary contacts and industry expertise to help PFE advance its USA lithium brine project - particularly around the use of Direct Lithium Extraction (DLE) technology.

This is Tim:

(Source)

Welcome to PFE Tim, we hope you can help PFE deliver something similar to Rincon’s Rio Tinto $825M acquisition.

Even a fraction of this would be a spectacular result for PFE.

What’s been happening in the Smackover?

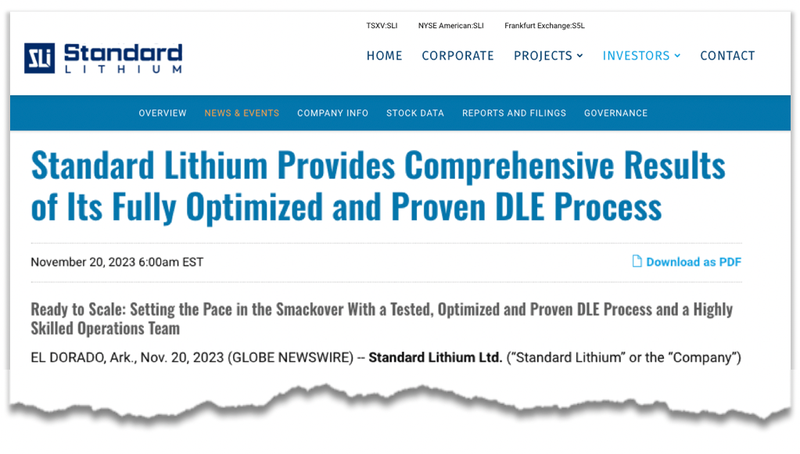

1. Standard Lithium has scaled up DLE

The big news is that Standard Lithium, one of PFE’s neighbours in the Smackover, announced that it had successfully scaled up its DLE operation and is running it continuously.

This could be a first sign that DLE is a viable technology for extracting lithium from brines:

(Source)

2. “Mr Lithium” himself has called the Smackover as the place where DLE will be ‘cracked at scale’

Last week “Mr Lithium” Joe Lowery spoke about DLE on the Money of Mine podcast focusing on the Smackover region in the US and its importance to the coming US lithium demand (from 6:51):

If you cant listen to it all, here are the key takeaways:

- Exxon is drilling new wells for lithium (not re-entering old oil wells) which has a much larger lithium content

- Brine in North America will require DLE technology (as it doesn’t have the arid conditions required for ponds)

- When asked about who is going to “crack” DLE at scale, Joe responds “I think it is going to happen in the Smackover”

- Exxon has the balance sheet to make DLE work in North America

- Arkansas “really wants this to happen” (in reference to lithium production in the region)

- If you’re going to build all these gigafactories in America they need Exxon to be successful they need Standard Lithium to be successful with their lithium production

Ultimately, the Smackover region has the companies, the government, the money and the lithium to make DLE work at scale.

3. Exxon Mobil drilling its first lithium well

And as we mentioned above, last month Exxon Mobil announced plans to produce lithium for electric vehicle batteries as soon as 2027.

The company is aiming to supply enough of the mineral to support the manufacture of 1 million electric vehicles annually by 2030.

Lithium production from brines has not been done at that scale... ever.

But if anyone is going to crack the code we think it will be Exxon, with the type of lithium concentrations that they are getting in the Smackover.

Watch President of Exxon’s low carbon solutions, Dan Ammann talk about Exxon drilling its first well for lithium:

(Source)

The Smackover is an exciting place to be if you’re looking for US lithium, and we think that PFE has perfectly nestled itself into the conversation with its land grab.

What’s next for PFE?

In Monday’s ASX announcement, PFE outlined its forward works in the Smackover Formation.

Lithium exploration target 🔄

This will give us a better understanding of what amounts of lithium PFE thinks it has on its acreage.

Re-enter a well 🔄

PFE will re-enter a well to test brine grade, permeability, and porosity from the Smackover.

DLE test 🔲

PFE intends to test a re-entry well sample by two “highly regarded” DLE technology providers.

2D Seismic 🔲

This will help with subsurface modelling of PFE’s project and inform drilling locations for the first resource definition wells.

Acquire additional project acreage 🔄

There’s a land rush on in the Smackover, so we think the more acreage PFE can lease, the better.

What could go wrong?

Leasing risk

There is a chance that PFE is not able to lease acreage quick enough or securing further mineral rights in the Smackover Formation proves to be more difficult than expected.

Alternatively, the exclusive agreement with the abstract provider expires before enough acreage is leased.

Exploration risk

PFE has said it intends to secure a lithium brine sample on the company’s acreage - there is no guarantee that lithium bearing brines are found or the brines are of economic concentrations.

Alternatively, if brines are found, they could contain contaminants that reduce or eliminate the value of PFE’s brines.

Funding / Dilution risk

PFE will likely need to raise more capital to continue expanding its foothold in the Smackover Formation. Capital raises can lead to dilution and may take place at a discount, reducing the value of PFE shares.

Technology risk

PFE is relying on Direct Lithium Extraction (DLE) technology to be proven viable and then being capable of producing lithium from PFE’s brines. There is no guarantee that the DLE tech will be advanced enough to effectively extract lithium from PFE’s brines.

Market risk

While lithium is a popular investment theme at the moment, lithium prices have pulled back before and its possible supply/demand dynamics change and in turn impact market sentiment for junior lithium explorers like SLM.

New PFE Investment Memo

Once PFE’s 100% acquisition is completed in January, we will launch our new Investment Memo for PFE.

A large part of our first PFE Investment Memo was based around its WA exploration projects, which was the reason we originally Invested in PFE.

Unfortunately these exploration projects were not successful, which is common in early stage exploration (exploration risk).

However, as the company moves into US lithium, we have reset our expectations for the company with a new Investment Memo to reflect the 100% acquisition of Daytona Lithium.

In January when PFE’s new acquisition competes, we will release our NEW PFE Investment Memo, where we will cover:

- Why we are Invested in PFE

- Our long term bet - what we think is the upside Investment case for PFE

- The key objectives we want to see PFE achieve over the next 12-18 months

- The key risks to our Investment thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.