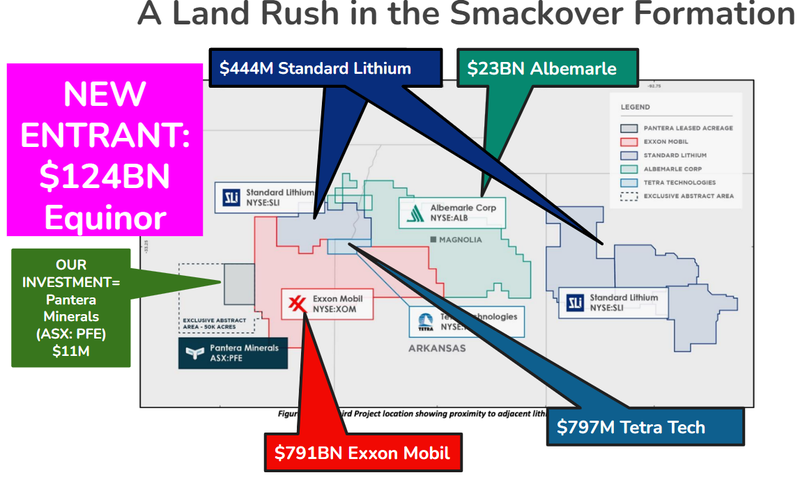

PFE: Another oil major enters US lithium in the Smackover - joins Exxon (...and PFE)

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 9,816,662 PFE shares and 2,994,167 options at the time of publishing this article. The Company has been engaged by PFE to share our commentary on the progress of our Investment in PFE over time.

Another global oil major just entered the Smackover Basin looking for lithium...

Equinor (formerly Statoil) is a A$122BN Norwegian state owned oil giant .

And they are paying up to US$160M to follow oil super major Exxon into the Smackover basin to hunt for... lithium.

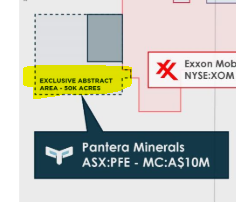

Last week's news means that both Equinor and Exxon now hold interest in projects next to our Investment, ~$11M Pantera Minerals Ltd (ASX:PFE).

PFE entered the Smackover before both Exxon and Equnior.

and PFE is the only ASX listed small cap with ground in that part of the USA.

Oil majors moving into lithium is a trend that seems to be getting stronger every day.

And so far they seem keen on the Smackover Basin, in the USA.

Equnior and Exxon have written huge cheques to get involved, but others, like Saudi Aramco, $84BN Occidental Petroleum, and ADNOC, are also looking at dipping their toes into the DLE space.

Yes... the biggest oil producer in the world Saudi Aramco is looking into DLE...

(Source)

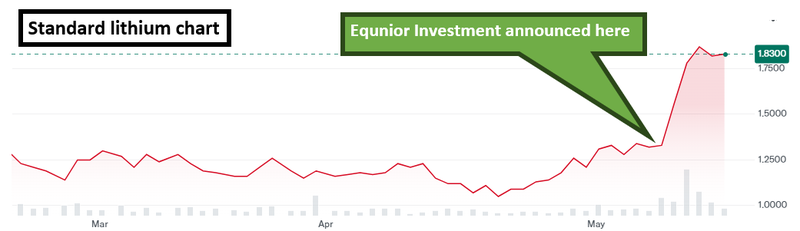

Just last week Equinor agreed to contribute up to US$160M to get its hands on a 45% stake in two Smackover lithium brine projects in Arkansas and East Texas owned by Canadian-listed Standard Lithium.

ExxonMobil paid at least US$100M for its projects in Arkansas in early 2023.

Depending on milestones, now Equinor will pay up to US$160M for only a 45% stake in two projects in Arkansas and east Texas.

Simple maths points to the value of Arkansas lithium brine land getting increasingly pricey.

We think the valuations for ground in the region will just get higher especially considering the work the majors are putting in at the moment...

Standard (now partnered with Equinor) recently commissioned a pilot DLE plant and Exxon recently drilled its first lithium well in the region.

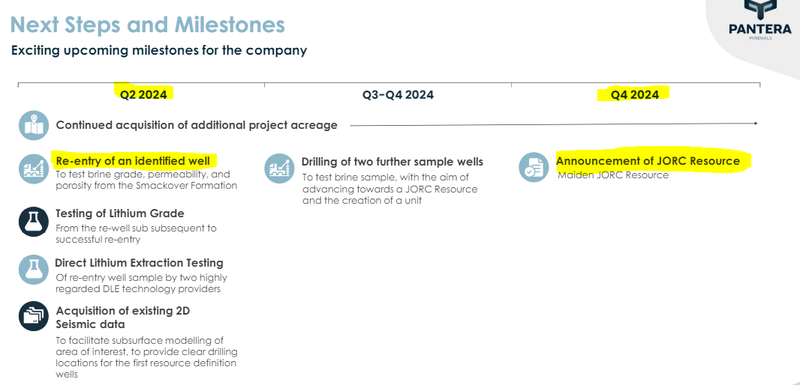

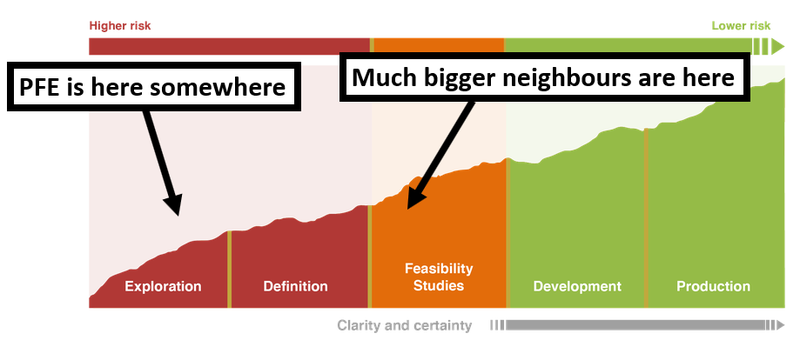

Until now PFE has been focused on increasing the size of its project by leasing more and more ground.

Over the next 12 months PFE’s plan is to re-enter an old oil and gas well, sample for lithium and upgrade its exploration target into a maiden JORC resource.

We think the JORC resource estimate will be a big catalyst for PFE as it will give the market a metric that can be compared to PFE’s neighbours.

(Source)

More on the Equinor/Standard lithium deal:

The deal between Standard and Equinor was announced on the 9th of May and the market definitely liked the news...

Standard’s market cap almost doubled in the last week or so adding over A$200M to its valuation.

For context - the move in Standard’s valuation is almost ~20x our Investment PFE’s market cap..

Here is an article that gives a pretty good overview of the deal:

(Source)

New York listed, and majority owned by the Norwegian government, Equinor has traditionally made its money from North Sea oil and gas.

Equinor was previously known as Statoil - and with the rebrand it's increasingly clear that the Norwegians want to move further into clean energy.

The Smackover is now part of Equinor’s plans, just like ExxonMobil.

The Smackover is a large underground formation that once made this region, which includes southwest Arkansas, once the most prolific oil producing region in the US.

But now, the Smackover appears to be quickly becoming the place to be for US lithium.

(especially for Major oil companies wanting to get into clean energy)

Relative to PFE, Equinor is “late to the party” in the Smackover region of Arkansas - PFE has been building its land position well before Equinor made its move last week.

This is now the second energy giant to enter the Smackover too, with $800BN capped Exxon Mobil also present.

PFE is rapidly advancing a lithium brine project of its own, in acreage immediately adjacent to ExxonMobil:

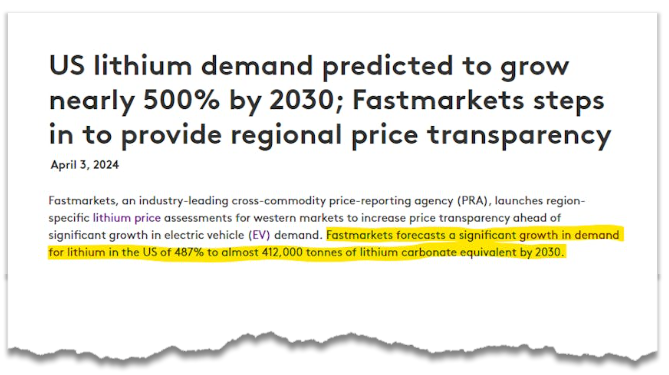

The timing is good too - PFE is positioning itself as a potential source of domestic lithium for the US, at a time when lithium demand in the US is forecast to rapidly ramp up:

(Source)

Importantly, a good portion of PFE’s Smackover acreage was picked up BEFORE ExxonMobil made its move.

Here’s the key takeaway for us as long term PFE Investors:

Equinor’s equity stake in two lithium brine projects in the Smackover provides an excellent baseline valuation of lithium brine acreage in the region.

In other words, we think:

With a market cap of just ~$11M, PFE’s land position in the Smackover continues to become more and more valuable as the oil giants pour capital into the Smackover.

Here’s some context on what leased acreage is going for in the Smackover:

- ExxonMobil paid at least US$100M for its projects in Arkansas in early 2023.

- Now Equinor has paid up to US$160M for only a 45% stake in two projects in Arkansas and east Texas.

Again, simple maths points to the value of Arkansas lithium brine land getting increasingly pricey - which is why we’re very pleased that PFE moved quickly on the once prolific oil and gas region, a good portion of PFE’s Smackover acreage was picked up BEFORE ExxonMobil made its move.

Now with close to 20,000 acres in the Smackover we think PFE will make a strategic shift from aggressively leasing land to establishing a resource by re-entering a well to extract a brine sample.

Our PFE Big Bet:

PFE to return 10x by making a discovery and defining a deposit significant enough to move into development studies.

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our PFE Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

Smackover in full swing, PFE’s neighbour commissioned a DLE plant, Exxon drilled a well

Three weeks ago, $444M Standard Lithium announced that it had “successfully commissioned and validated” the largest continuously operating direct lithium Extraction (DLE) facility in North America.

The move is a big step for the US lithium industry and the specific region Standard operates in.

(Source)

Why does the Standard Lithium news matter for PFE?

At a very high level we think it increases the look through valuation for PFE’s assets.

PFE holds ground in the Smackover inside a 50,000 acres AOI “Area of Interest” - the AOI is basically the area PFE has rights to negotiate leases in.

Across that 50,000 acre ground position PFE has already estimated a JORC lithium exploration target between 436,000 to 2,966,000 tonnes of Lithium Carbonate Equivalent (LCE).

Over the past few months, PFE has been increasing its ground position (adding ~8,131 acres in the first 4 months of 2024).

Right now, of that 50,000 acre AOI, PFE holds ~18,570 acres.

PFE is currently working toward a maiden JORC resource by the end of the year.

We think the JORC resource estimate will be a big catalyst for PFE as it will give the market a metric that can be compared to PFE’s neighbours.

Our view is that IF PFE can put together a resource estimate somewhere in the middle of its exploration target (436kt to 2.96mt LCE) then its market cap could re-rate higher as the market will have something to compare PFE against its regional peers with.

For context - Standard Lithium has a Measured and Indicated resource of 2.8 Mt LCE and a market cap of $444M & Galvanic Lithium which Exxon paid over US$100M for had an inferred JORC resource of ~4mt LCE.

PFE’s current market cap (~$11M) is relatively low considering the potential resource it has on its ground.

PFE now working with oil services giant (SLB) to make a lithium discovery...

Earlier this week, PFE also announced that it will engage with $105BN oilfield services company SLB (formerly Schlumberger) to help find lithium in the Smackover.

SLB is one of the go to operators when it comes to drilling and testing oilfields.

We see SLB as the perfect partner for PFE here considering a big part of PFE’s strategy is to resample old oil wells to test for lithium.

Next, the two companies will combine a range of geophysics datasets that PFE already has to build a subsurface 3D model of PFE’s acreage.

The desired outcome from this work is to increase PFE’s confidence in finding high concentration lithium on its nearly 20,000 acre lithium project.

That work will form the basis for PFE’s maiden JORC resource estimate which the company expects to deliver in Q4 of this year.

We eagerly await that well re-entry program which we hope produces a lithium sample that has a comparable or (ideally) better grade than PFE’s neighbours in the Smackover.

Our Past Coverage:

We visited PFE’s project in Arkansas - and saw the project for ourselves.

The two articles below are our write ups of that trip and what we learned from it.

Lithium report filed by our international correspondent and roving reporter

Arkansas Lithium Summit - lithium come back?

What’s next for PFE?

Below is a list of the key catalysts PFE is working toward, from a recent investor presentation the company put out.

(Source)

The two key catalysts we are looking forward to in the short term are the following:

Re-enter a well 🔲

The first step toward converting its exploration target into a maiden JORC resource will be to re-enter historic oil & gas wells that sit on its acreage.

The goal for the re-entry programs will be to see how much lithium sits in the ground and at what concentrations.

DLE test 🔲

The re-entry will bring up samples which PFE can then send off to DLE (Direct Lithium Extraction) tech partners.

If PFE continues making progress along these milestones, we think it should move closer to achieving our ultimate upside case for our PFE Investment.

What are the risks?

At the moment, we are most focussed on “Exploration risk” and “Funding risk”

Exploration risk

PFE has said it intends to secure a lithium brine sample on the company’s acreage - there is no guarantee that lithium bearing brines are found or the brines are of economic concentrations.

Alternatively, if brines are found, they could contain contaminants that reduce or eliminate the value of PFE’s brines.

Funding risk

Well re-entry programs are generally much cheaper than new wells, but it is worth noting that PFE had $1M in cash at 31 March, 2024 (+$3.45M April 2024 placement). Meaning that PFE will need to be careful with its cash and much hinges on their exploration efforts. Small caps like PFE often need to raise capital and these capital raises can take place at a discount and incur dilution.

Our PFE Investment Memo

Below is our Investment Memo for PFE where you can find a short, high level summary of our reasons for Investing.

The ultimate purpose of the memo is to record our Investment thesis in order to benchmark the company's performance against our expectations.

In our PFE Investment Memo you’ll find:

- Key objectives we want to see PFE achieve

- Our PFE Big Bet

- Why we Invested in PFE

- What the key risks to our Investment thesis are

- Our Investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.