Arkansas Lithium Summit - lithium come back?

Published 17-FEB-2024 09:28 A.M.

|

18 minute read

After attending the Mining Indaba conference last week in Cape Town, South Africa, we sent one of our analysts to continue the journey...

All the way to the USA.

To Little Rock, Arkansas.

Watching a company CEO present at a conference is one way to get a better understanding of a company.

Directly speaking to them after their presentation is even better.

But the best insights come from actually visiting a project and seeing it for yourself.

The key parts of the USA leg of the trip include:

- To visit Pantera Minerals’ (ASX:PFE) lithium project site in the historical oil producing region - the Smackover formation in Arkansas

- Attend Lithium summit with Exxon, Albermale, Standard Lithium and the Governor of Arkansas.

- Visit a Direct Lithium Extraction research center to learn more about the process from the experts.

Today we share what we have learned so far.

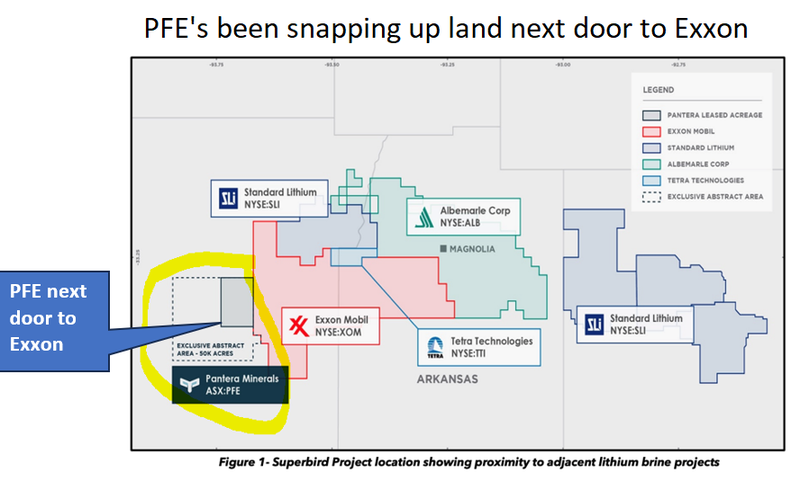

PFE has been busy over recent months, quietly acquiring old oil fields in the Smackover that have no more oil, but are rich in lithium brines.

(And contain lots of old oil drillholes that can be cheaply re-entered to extract lithium brines).

We have had a big win in the past with a certain lithium DLE project in Germany that we picked up while the lithium sector was having its previous breather in 2019 (...it was Vulcan).

(remember past performance is not a future indicator...not saying this will happen again, but we are taking the shot with PFE).

PFE’s plan is to use direct lithium extraction to extract lithium from underground brines, by entering historical oil wells drilled in the Smackover formation in Arkansas, USA.

The same plan as $411Bn capped Exxon:

(big thanks to the PFE team that made the trip possible and organised the PFE site visit and the visit to the Direct Lithium Extraction research centre).

What follows is part 1 of our analyst’s account of the trip, what he learned and what the future could hold for our lithium Investments, in particular PFE:

Part 1: Direct Lithium extraction - from Phoenix to Little Rock

Touchdown.

Forget the Super Bowl, I’d just landed in Phoenix, Arizona.

I’ve come here to learn about a technology that could be at the centre of the lithium market in just a couple short years.

Direct Lithium Extraction (DLE) is a set of technologies that use physical or chemical selective processes to remove lithium from brines while leaving other components in the brine.

I never thought I’d be learning about hydro-metallurgy as an Investor, but make no bones about it - DLE is coming.

Quicker than many think.

Here’s why.

The lithium price has cratered over the last year, taking many Aussie stock favourites with it (some of our Investments too).

Noting that lithium sale contracts are opaque and closely held secrets (the only benchmark is in China).

The arc of history is long though and recent lithium price action could just be a blip.

IF or more likely WHEN lithium prices do come back there should be immense need for localised supply - particularly in the US and Europe.

Lithium in underground water (lithium rich brines) is not new.

But the question is always how to best extract the lithium from the water.

The simple way is pumping the brines from underground into ponds that sit under the sun, then letting the water evaporate to leave behind the lithium.

Due to environmental regulations or lack of sun/heat, the US and other major economies in Europe can’t rely on huge evaporation ponds like the ones found in Chile and Argentina which stretch far into the desert plains of these countries:

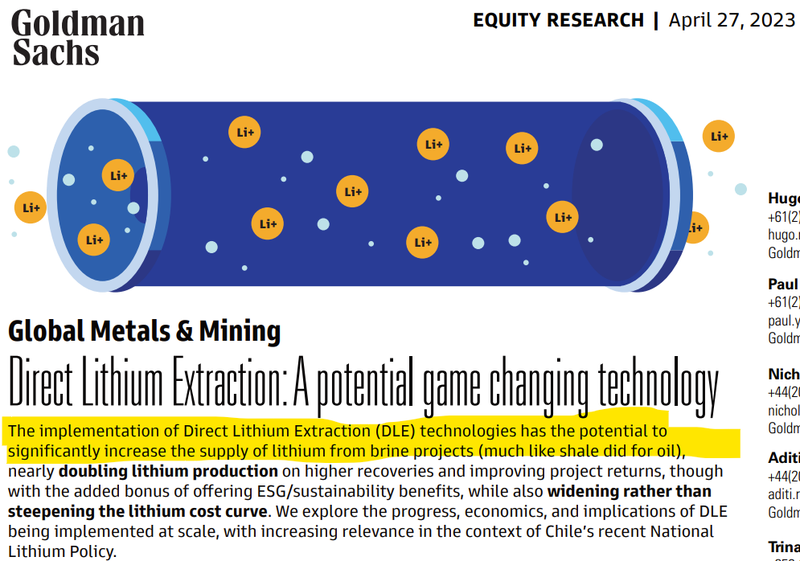

Direct Lithium Extraction (DLE) could solve that problem.

It’s a technology that has Exxon and Wall Street bankers at Goldman Sachs up and about:

(Source)

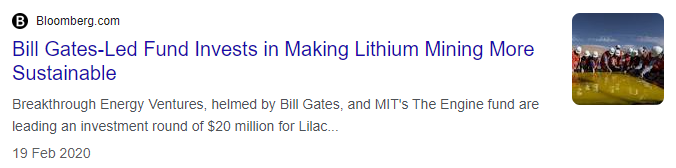

And old Billy G investing as well:

(Source)

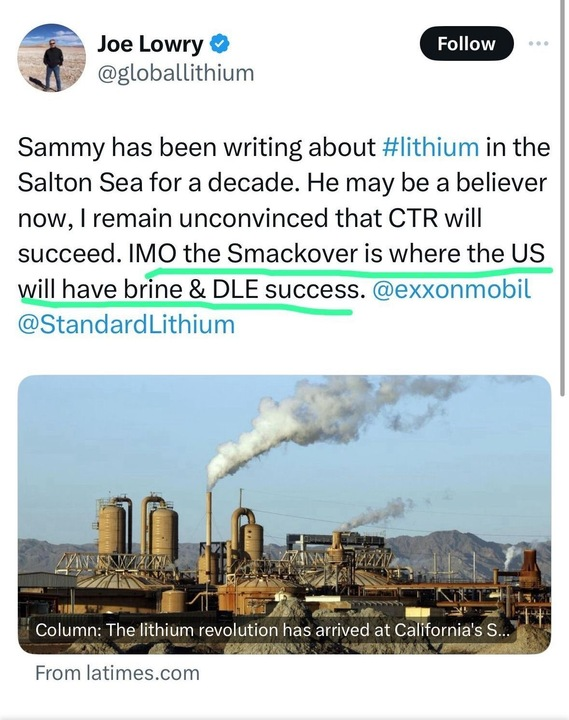

“Mr Lithium” Joe Lowry reckons DLE in the Smackover will have success...

(And he is usually sceptical about a lot of things.)

So here I am in the middle of Phoenix to get the story.

What I learned about DLE in Phoenix

To put this story together, PFE organised for me to visit a Direct Lithium Extraction research centre.

To understand the style of technology PFE and other Smackover players might use to extract lithium from brines it was important to visit a facility like this.

There I met Brett Rabe, who is the Chief Technical Officer of Arizona Lithium, which amongst its other projects has an advanced DLE project in southeast Saskatchewan, Canada.

But most importantly for this piece on DLE, Arizona Lithium also has the Lithium Research Centre in Tempe, just next door to Phoenix:

While it may look somewhat unassuming from the front - there’s a lot at this site.

Much of which I can’t show with pictures due to the sensitive nature of the research going on inside.

Lab technicians in white coats, working with beakers.

Big bits of machinery being prepared for operation.

And then there’s Brett Rabe:

Brett worked for Lithium Americas Corp as VP of Engineering, Project Manager for the Thacker Pass Project in Nevada, and is now Chief Technology Officer of Arizona Lithium.

Thacker Pass is that massive lithium bearing clay deposit in Nevada that is often in the headlines for being the largest lithium deposit of its kind in the world.

Brett is a DLE expert - he gave me a crash course in everything DLE to help understand what could be happening with DLE aspirants in the Smackover (like PFE).

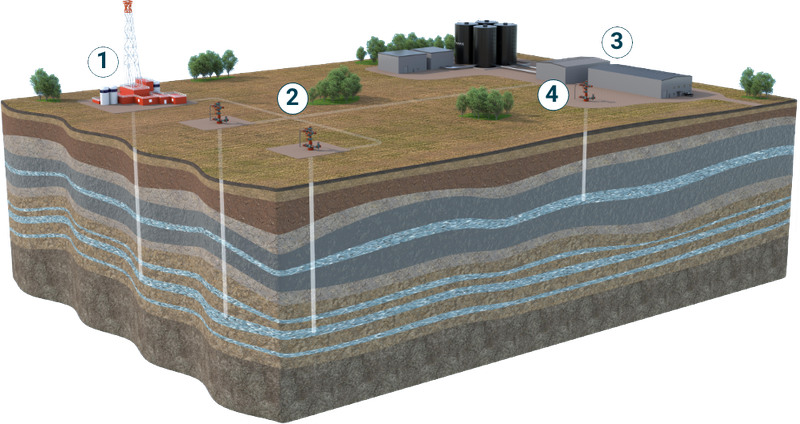

The principles of DLE as it is applied to brine are relatively simple:

- A brine well is drilled

- Brine is pumped from the subsurface and sent to a lithium extraction facility

- Lithium is extracted from the brine using DLE

- The lithium free brine is disposed of back deep underground

Each step is visible below:

(Source)

(in PFE’s case, the aim is to save costs on step 1 by re-entering existing, historical oil drill holes instead of drilling expensive new holes).

Now turns out, DLE is only a small subset of the overall process to extract lithium from brines and can be applied to a range of different types of lithium projects (including hard rock lithium projects) - I’ll get to this point later.

Here are the broad themes of my day chatting to Brett Rabe:

- The Chinese have been using DLE at commercial scale for a decade - and Western DLE has been around longer than you think +10 years - Brett said the technology is not as new as many think and there’s a significant jurisdictional divide in terms of capabilities.

- DLE could potentially be more environmentally friendly than evaporation ponds or hard rock mining -

As mentioned at the start of this piece, DLE can work where evaporation ponds won’t due to environmental regulations, water restrictions or lack of sun/heat.

And on top of that, many hard rock (spodumene and lepidolite) operations require large amounts of acid and heat to leach (chemically pull out) lithium.

DLE could have a lower carbon footprint than both evaporation ponds AND some hard rock mining because there is less heavy machinery and no mine pit required

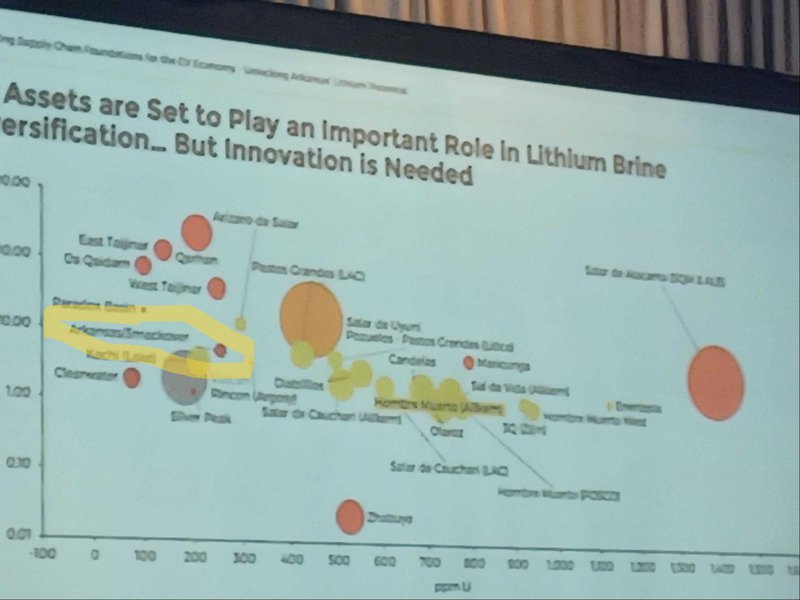

- The quality of brine is essential - Brett explained that the economic value of a project is largely linearly proportional to the concentration of lithium in the brine (assuming there are no nasty, deleterious elements in the brine, like iron, silica and zinc).

PFE’s project in the Smackover Formation Arkansas is home to other companies with +400ppm concentrations -some of the highest lithium concentrations in brine, anywhere in the world.

These are the kind of concentrations we hope to see when PFE starts sampling.

- Analysts and financiers gravitate towards spodumene projects because it is easier to understand with its centralised production - one mine pit, one processing centre - this is really important. Analysts are having a hard time wrapping their heads around DLE projects and this makes it harder for financiers to step in with cash to fund the projects. Sometimes, DLE projects even centralise their project with a single, big processing facility just so financing is easier to secure because it's a more well understood way of operating.

- Modular approach most likely to work with clusters around wells - the modular approach, where there are clusters of DLE facilities around wells may work best even though analysts and financiers may not gravitate towards these types of operations. Brett envisages these modular projects having 3 people on each site, who don’t need to be highly skilled engineers. With a remote sensing control centre potentially located in a completely different country.

- DLE at commercial scale in the West will happen sooner than you think, 1-3 years - Brett was supremely confident that DLE in the West is on the verge of success given the amount of effort and capital being put into the projects.

- Australian spodumene will always be bound for China - this has drawbacks because the benchmark price in China is highly sensitive to domestic Chinese production and EV subsidies and may not be a true indicator of the actual lithium supply/demand balance. Especially with the US EV machine revving up, localised supply (especially in the US and EU) will be extremely important and carry through to capital allocation towards DLE projects even when the lithium price is low.

- DLE may lead to creation of a midstream product (more lucrative, better for DLE companies) - this was very interesting. Brett suggested that DLE projects could be able to produce a midstream high grade lithium product that could then be easily shipped to a central processing facility to get it to battery grade lithium. This could dramatically improve the economics of DLE projects. Much like with gold producers that produce ore instead of bullion, or the various types of oil, it doesn’t really make sense for some lithium producers to go straight to battery grade material. Brett thinks that over time the creation of a benchmarked midstream product will enhance the transparency of the lithium market AND help DLE projects speak better to the market about their economics.

- Power is the biggest component of operating expenditure (OPEX), jurisdictions with cheap power will work better - Brett showed me a breakdown of OPEX across the various stages of DLE production. He clearly outlined how power costs are the main cost burden - which can be alleviated by operating in a jurisdiction with cheap power. I note that Arkansas has a plentiful supply of nuclear power and as a result has power that is ~25% below the national average (source). This is great news for PFE and other DLE aspirants in the state (including US$411BN capped ExxonMobil) - more on this later.

Needless to say, it was a lot of information to digest over a few hours talking to Brett.

But it certainly got me enthused about DLE’s prospects in the near future - something which I would see for myself as I hopped on a plane to attend the first ever “Lithium Innovation Summit” in Little Rock, Arkansas...

Big goals, serious ambition - Arkansas is all in on DLE...

I got to Little Rock in one piece late at night - flying into the Bill & Hillary Clinton Airport.

Bill was US president and Hilary had a crack, so the state has produced some big politicians.

When it comes to DLE - policy settings are incredibly important to its success.

And after attending day one of the Lithium Innovation Summit in Little Rock, I’m convinced that Arkansas is set up for lithium success as far as politics is concerned.

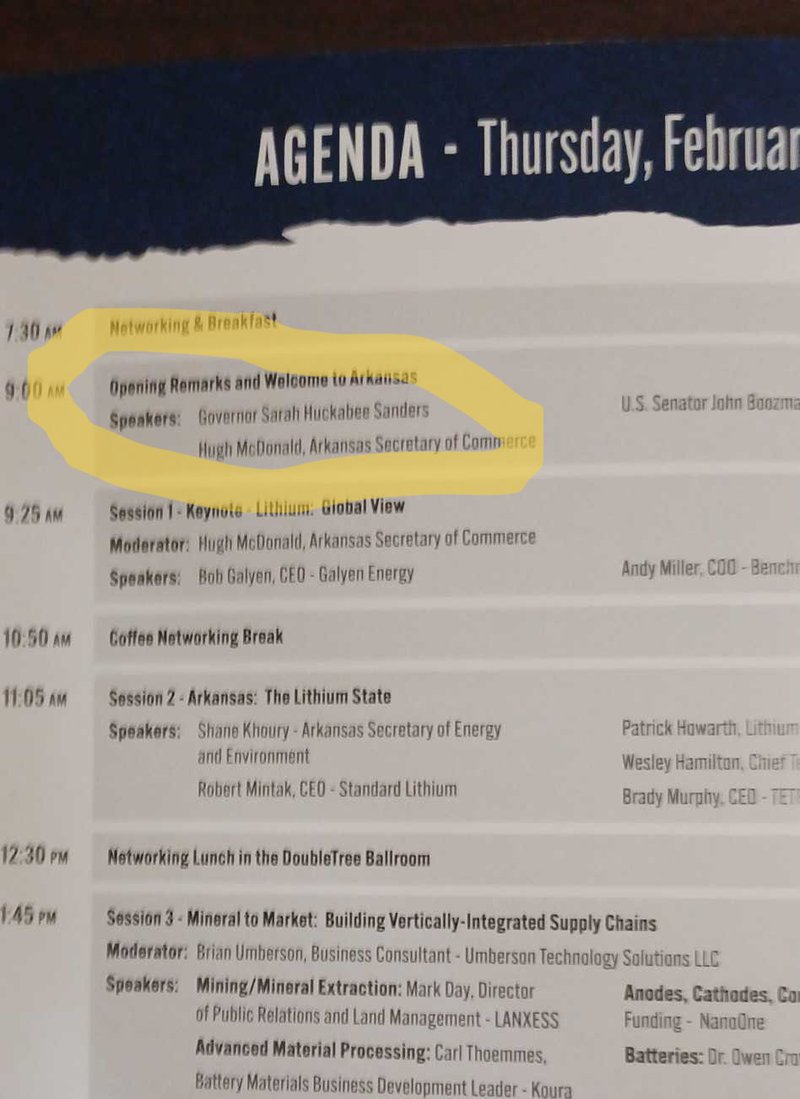

Speaking of politicians, the star of the show at the event was Arkansas governor Sarah Huckabee Sanders who was scheduled to speak at 9am to kick things off:

Huckabee Sanders received a standing ovation from the crowd and quickly moved into a speech that outlined how she sees lithium as a “once in a generation” opportunity for Arkansas.

It’s strange to say, but I felt inspired by the speech - Huckabee Sanders has been a vocal proponent of the lithium industry in Arkansas, well before the Smackover went mainstream.

Her presence in the room was immense and a clear sign of intent:

You got the sense that DLE and lithium in Arkansas is going to actually happen and Huckabee Sanders was going to make it a key pillar of her economic agenda.

At one point she got all the state senators in the room to stand up and be seen and in a charming Southern drawl of an accent she said:

“I’m going to need y’all to help me out on this one.”

Huckabee Sanders wants everyone pulling in the same direction and made clear that the right policy settings will be put in place to make Arkansas the “lithium capital of America”.

From big to small, Huckabee Sanders appeared to know all the players in the region...

..including PFE.

A couple people have told us that PFE has been mentioned by name by the governor - she's got a great grasp on who is working in the area.

The Arkansas Secretary of Commerce Hugh MacDonald also spoke - this wasn’t a fluff piece - the Secretary knew his stuff and rattled off facts and figures and spoke with a clear knowledge of DLE.

Other speakers included Bob Galyen - who helped establish China as a battery powerhouse many years ago in his work for the world’s largest cathode producer CATL.

And Andrew Miller of Benchmark Mineral Intelligence who gave some powerful insights into why Arkansas is the right place for lithium production.

I quickly realised I was in a room with a who’s who of the Arkansas business and politics scene - I felt lucky to be there.

(and to see some of the PFE top brass busy working the room).

I stepped out the conference room between sessions to take a call and came back to see that all the seats had been taken with only standing room only remaining:

Just like the 121 conference in South Africa this place was again PACKED.

So there appears to be a bit of a theme developing where soft market conditions for small caps and small cap lithium companies in particular, contrasted with the on the ground market enthusiasm seen at these conferences.

Maybe not all meets the eye when it comes to the lithium price...?

Below are my quick summaries of the speakers presentations, there were definitely some juicy nuggets in some of the slides and commentary:

Each of the speeches revealed the specific ways in which the state, federal and other companies are keen to ensure the Smackover region where PFE is working in, becomes a major lithium production hub.

US Senator John Boozman

The Senator made clear in his speech that when in Washington, he would do everything he could to make domestic production of critical minerals like lithium possible with legislation.

Legislative support at the federal level will be crucial to Arkansas’ success when it comes to lithium, as well as the entire US.

Great news for all the Smackover DLE aspirants.

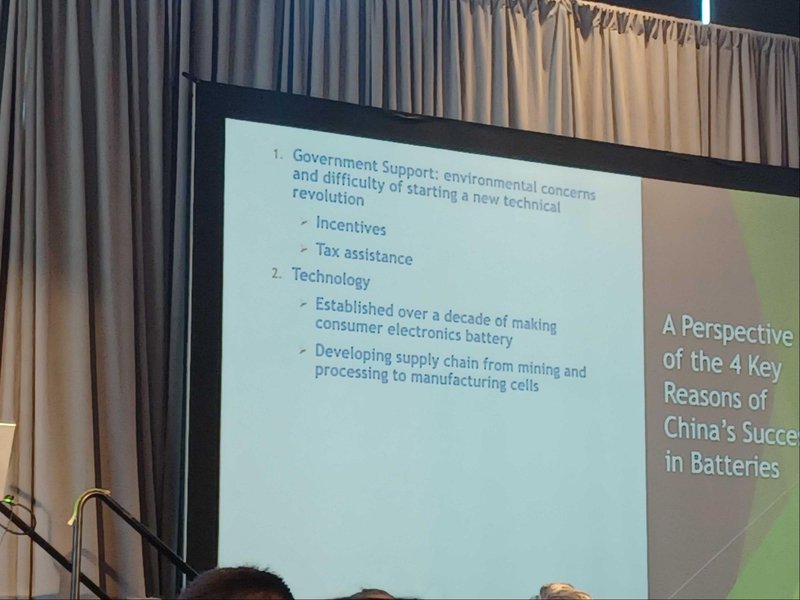

Bob Galyen, CEO Galyen Energy

Galyen has done it all when it comes to batteries - he’s one of the foremost experts in the world (read bio).

This was a slide that caught my attention:

While I wasn’t able to get a proper snap, because Bob Galyen moves so fast and speaks so fluently - the government support leads to a key reason for China’s success in batteries - it makes investment in the industry possible because funds and retail investors feel comfortable that they will get a return on investment.

This is absolutely key for the US’ burgeoning battery industry and well supported by the Inflation Reduction Act.

Galyen also made reference to the power consumption of gigafactories and Arkansas’ abundant nuclear power which provides the plenty of cheap baseload electricity that these battery factories need.

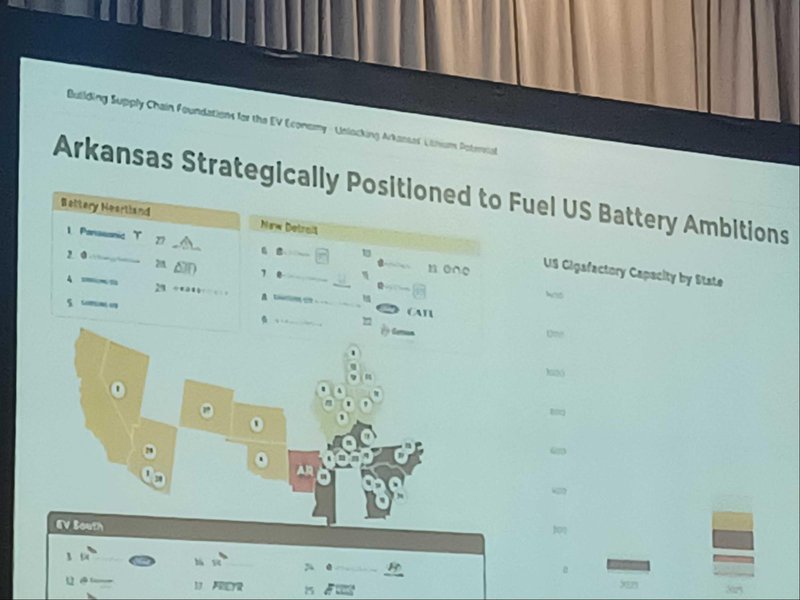

Andy Miller, COO of Benchmark Mineral Intelligence

Benchmark Mineral Intelligence does it all when it comes to battery materials research and Andy is incredibly well versed in the market dynamics driving electrification.

These were the three slides I was most interested in:

Again my photography skills were woefully deficient, but as you can see, US battery manufacturing has grown by 77% since August 2022 - outstripping Europe by a long way.

These battery manufacturing plants will be hungry for more lithium - hopefully PFE’s lithium from the Smackover in Arkansas.

This slide detailed how Arkansas is surrounded by a tonne of gigafactories that are in production or about to go into production - definitely a major bonus.

This slide shows on the left the resources of Arkansas/Smackover relative to other lithium resources in the world - we expect that bubble to grow rapidly over the next couple years - and hopefully PFE can add its own resources to that after releasing a lithium exploration target late last month.

Shane Khoury, Arkansas Secretary of Energy and Environment

Shane was very impressive, he comes from an oil and gas background and discussed in detail what Arkansas is doing to advance the regulatory environment for lithium in Arkansas.

The number one topic for him: royalties.

Like with oil - the state and local mineral rights holders would expect a cut of lithium products produced from the oil wells in the state.

But lithium is a very different beast to oil and this requires regulatory flexibility.

Lithium is in the parts per million in these Smackover brines and has no well established benchmark (the only one is based in China).

So the royalty arrangements need to be accommodating for these emerging lithium producers, so as not to hurt their economics and in turn, their ability to secure financing.

In a panel discussion - Shane asked very technical questions, in particular one about well reservoir quality.

You could tell he had a deep knowledge of the subject matter, and I think will be an excellent force for driving Arkansas’ lithium industry forward.

Having steady hands as partners in the policy space will no doubt be helpful to PFE.

Patrick Howarth, Lithium Global Business Manager, ExxonMobil

Patrick was a big star of the show alongside governor Huckabee Sanders.

Patrick is charged with pushing the US$411BN capped Exxon into Arkansas lithium at a fast pace - and has plenty of charisma to boot.

We first heard Patrick speak on Joe Lowry’s Global Lithium podcast a couple months ago.

For anyone wanting to really understand Exxon’s role in the Smackover and US lithium brine industries, the podcast is a must-listen.

(Source)

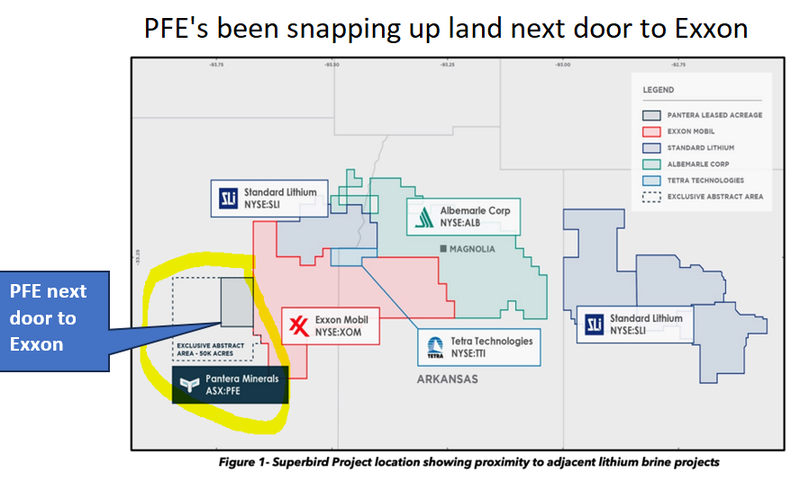

As we’ve detailed previously, ExxonMobil is going HARD at lithium production in the Smackover.

(PFE’s land position happens to be immediately adjacent to Exxon’s project to the West):

Patrick shared a great video which will be a part of ExxonMobil’s public relations push.

He also announced a new ExxonMobil charitable foundation for southern Arkansas which was warmly received by the audience.

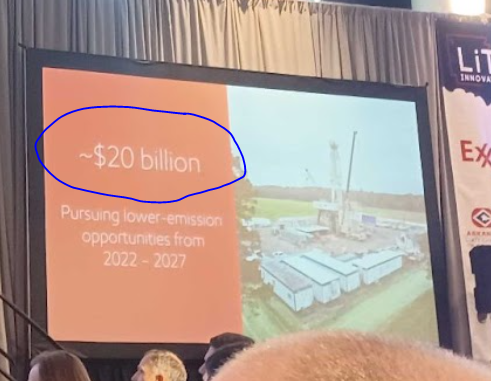

Most importantly though, here was the key slide:

Again, I’m no Stanley Kubrick or Ansel Adams with my photo but you can just see a REALLY BIG number - US$20BN is what ExxonMobil has earmarked for “lower emission opportunities” over the next 5 years.

Like lithium from DLE in Arkansas.

It’s a huge chunk of change and is a massive sign of commitment - when that slide came up there were some murmurs in the audience.

Even a fraction of this would be a game changing investment for the state of Arkansas, and we hope that kind of decisive capital allocation by ExxonMobil will have second order benefits for PFE (next door) as it advances its own Smackover lithium operations.

After the speakers had finished, we moved to have lunch.

Again, just to give a sense of how well attended this event was here’s how many people were packed into the lunch room:

Sitting next to me was the recently appointed director Tim Goldsmith of PFE (formerly of Rincon), along with PFE chairman Barnaby Egerton-Warburton, the very friendly Cleve and John who head up PFE’s land and mineral rights work in the Smackover.

For lunch, turkey breast with a mustard cream sauce, green beans, mash and a glass of iced tea.

For dessert, a slice of Southern hospitality - pecan pie.

Looking around the table and chatting to the people of Arkansas, I knew that these are some of the friendliest people I’ve ever met.

They also just want to get things done.

And that includes making the state the centre of US lithium production.

Up next...

Armed with a new appreciation of DLE technology and seeing first hand the commitment of Arkansas to become a key lithium producer, it’s time to head over to PFE’s project and hear from the people on the ground making it happen.

Next, I’ll be sharing a write up of my PFE site visit, onto the ground on the Smackover Formation:

What we wrote about this week 🧬 🦉 🏹

Global Oil and Gas (ASX:GLV)

GLV started 3D seismic reprocessing at the first of its three major prospect areas at its 80% interest in a giant exploration block offshore Peru.

Read: 🛢️ GLV Commence Pre-Drill Work on Potentially Giant Oil Resource

Minbos Resources (ASX:MNB)

This week MNB provided an update on its Green Ammonia project, highlighting that its project is now attracting significant interest from potential investors.

Read: 🎯 Does MNB have the “most commercially attractive zero-carbon green ammonia project globally”?

Global Uranium and Enrichment (ASX:GUE)

GUE provided an update on its Uranium Enrichment technology this week. Uranium has been in all of the headlines to start 2024 as a global supply crunch looms.

But whatever supply chain instability is for the uranium markets, the “enriched uranium” markets are much worse.

Read: ☢️ GUE: Uranium Enrichment Technology

Quick Takes 🗣️

GUE uranium drilling permits lodged in the USA

IVZ discovery samples in the lab for testing.

Bite sized summaries of the latest mainstream news in battery metals, biotechs, uranium etc: The Future Money: https://future-money.co/

Read: Biotech Companies Riding the M&A Wave

Have a great weekend,

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.