ALA is our best performing stock in 2023 - here’s why, and what to expect in 2024

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 15,876,579 ALA shares and the Company’s staff own 800,000 shares at the time of publishing this article. The Company has been engaged by ALA to share our commentary on the progress of our Investment in ALA over time.

It just keeps going up.

Our preclinical biotech Investment Arovella Therapeutics (ASX:ALA) started the year with a share price of 2 cents.

ALA shares are now trading at 11.5 cents.

That’s a remarkable ~475% rise, especially given the softer market conditions for small cap biotechs.

That result also makes it the best performing stock in our Portfolio over the course of 2023.

Whilst the past performance of a stock is never a guarantee of future performance, we are looking forward to a big 2024 for ALA.

ALA is seeking to develop an “off-the-shelf cell therapy” to treat cancer, and will be moving to Phase 1 clinical trials in the second half of 2024.

The company is currently capped at around ~$105M, which is still a fraction of what some of the acquisition and licensing deals we have seen for preclinical cell therapy biotechs.

We think there’s plenty more to come from ALA, as it progressively improves its manufacturing process for the treatment that will be used in its clinical trial.

ALA also has important in vivo (mice model) studies due soon from its partnership with the ~$753M capped Imugene - this is another treatment which is targeting solid tumours.

Solid tumours make up ~90% of all cancers so if data from the in vivo studies is positive, we see this as a major catalyst for ALA.

Part of what makes ALA stand out from the crowd is its iNKT cell therapy platform, which forms the basis for its “off-the-shelf cell therapy” for cancer.

Watch this explainer video on ALA’s technology here.

Current cell therapies are costly (AU$600k per patient) and unique for every patient, as a patient's own cells are being used and modified. This also means the treatment is not as reliable.

Because of the unique properties of ALA’s technology, the company’s off-the-shelf version may be more cost effective, provide a better result and can potentially target more cancers.

This potential is a big part of the reason investors seem to have taken a shine to ALA this year.

Here’s ALA’s CEO and MD Dr. Michael Baker wishing everyone seasons greetings and giving a great re-cap of 2023 for ALA, and importantly, what to look forward to in 2024:

For those new to the ALA story, it's also worth watching MD Michael Baker presenting at the Monsoon Twilight Investor briefing in Melbourne a few weeks back, which some of us headed along to:

Our take on why ALA performed so well in 2023

1. Powerful technology that is distinctly different to other cell therapies for cancer

The dominant cell therapy approach is CAR T cell therapy which has established itself at the forefront of cancer immunotherapy innovation.

However, this approach is constrained by a variety of factors.

The main limitation of CAR T is the need to pull blood from the patient suffering from cancer which comes with exorbitant costs (upwards of $600K for a treatment), complications and reliability issues.

We think ALA’s iNKT cell therapy is a different approach that could smash through the scalability problem and help drive down costs, while also providing a more effective cancer treatment.

2. Cell therapy is a “hot” thematic in the massive cancer treatment market

The size of the cancer treatment market is huge, upwards of $327BN will be spent on treating cancer in this year alone.

Cancer cell therapy is a cutting edge technology in this market, with the first CAR T cell therapy approved by the TGA in 2020.

There are hundreds of players in this space looking to improve upon what is already a remarkable technology - and big pharma is willing to pay big money for promising technology (see more on that below).

3. Clever licensing strategy

Speaking of promising technology, in 2023 ALA upgraded its platform by licensing complementary technologies to enhance the effectiveness of its cancer killing cells.

An October licensing deal with Sparx Group has allowed ALA to expand the types of cancers that it could target.

By increasing the number of types of cancer (for an upfront fee of less than $300K in shares and $500K in due diligence work) ALA now has a chance to treat pancreatic cancer, gastric cancer, gastroesophageal junction cancers and potentially even lung cancer.

4. Imugene Partnership

Last year ALA signed a partnership with ~$753M capped Imugene to evaluate whether ALA’s technology and Imugene's technology is a viable treatment of solid tumours.

This was important for the ALA story as it found a credible, bigger partner to develop its technology with.

We think cell therapy treatment for solid tumours would be the “holy grail” of cancer therapy.

Solid tumours represent 90% of all cancers, and there is no viable CAR-T cell therapy treatment for solid tumours for now, due to a range of technical challenges (Source).

An iNKT cell therapy for solid tumours, may be able to overcome some of these challenges, and that’s ALA’s goal - to prove out the viability of its iNKT technology.

Aiding ALA’s bid to develop a treatment, was good in vitro (test tube) preclinical trial data. (Read our Quick Take).

The promising results of the initial preclinical studies were published in 2023, which legitimised ALA’s technology as “one to watch” in this space.

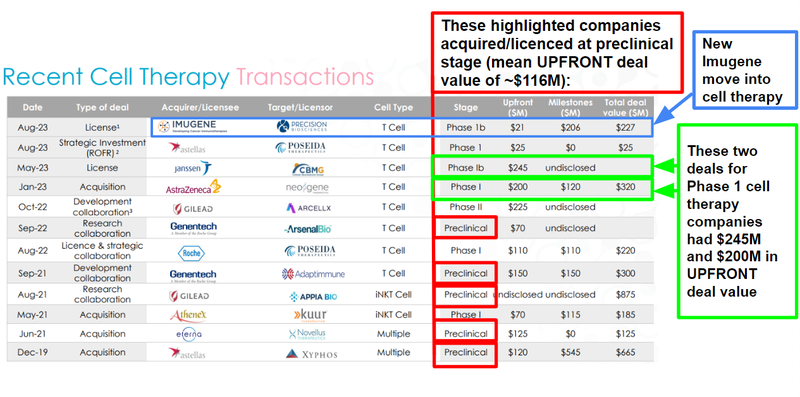

5. Valuation upside relative to cell therapy peers

Pre-clinical and Phase 1 cancer immunotherapy companies, particularly in the cell therapy space, are often acquired (or licence their tech) for upwards of $200M:

(Source)

As the ALA story started to filter through the market we think it became increasingly clear that the company was undervalued, based on the stage it was at and the valuation of its peers.

This is because cell therapy is seen as the next frontier in the fight against cancer - and big pharma is looking to get a piece of the action.

Relative to these companies, ALA’s tiny market may have been seen as attractive (and in our eyes, it still is given ALA’s ~$105M market cap).

6. Strong operational performance

ALA moved quickly to eliminate the cash burn from its legacy business and transition into a solely cancer immunotherapy company.

While doing that, ALA also managed to knock down a number of milestones as it advances towards a Phase 1 clinical trial.

Management also took fees in ALA shares, rather than cash - which is always a strong signal for us.

7. Sound management

Speaking of management, ALA has progressively added experience to its Board and management since it transitioned to just being focussed on cancer.

On top of this, CEO and MD Dr. Michael Baker is exceptionally adept at presenting each new bit of data that ALA comes out with.

He communicates clearly and often with investors about very complex topics, and we think his approach is resonating with the market.

Of all of the Managing Directors in our Portfolio, we think Dr. Baker presented the most.

He was at the most roadshows, at the most conferences, did the most webinars and showed up to the most events.

We think that this hustle built trust with family offices and high net worth investors that frequent these events, and his continued presence gave investors the confidence that the company was on the right track.

8. Sticky shareholders, loyal register

ALA conducted two capital raises in 2023.

The first, $2M at 2 cents and the second, $4.1M at 5 cents.

Normally after a capital raise there is a period of “post-raise churn” where participants look to flip the shares and take hold of the options.

ALA managed to shake off this churn on both occasions, with good on-market buying support from shareholders.

We think this is a testament to the share register of the company, in particular the lead broker Matthew Baker from Blue Ocean Capital and cornerstone investors such as the Merchant Group.

Meanwhile, the array of smaller holders appear to be accumulating over time, which combined with Dr. Baker’s frequent public appearances, we think, holds the register in good stead for the long run.

What’s next for ALA?

We think there’s plenty of newsflow to look forward to in the new year, not least of which is the all important Phase 1 trial for ALA-101, which the company is targeting for commencement in 2024.

Below is a quick summary of all the things we’re looking for from ALA:

🔲 Phase 1 clinical trial for ALA-101

This is the big one.

ALA-101 is ALA’s most advanced treatment for blood cancers and the period leading up to and the start of a Phase 1 clinical trial could be a source of a re-rate.

After ALA completes the clinical manufacturing process, it will be focussed on getting its iNKT cell therapy into Phase 1 clinical trials.

ALA has previously confirmed in its latest video, that it expects Phase 1 human trials to occur in the second half of 2024.

These are the sub-milestones we are looking for from ALA to make that possible:

- 🔲 Further manufacturing milestones (optimisation, scale up and complete lentiviral vector) - ALA needs to improve the process, make enough of the therapy to enter a trial and the lentiviral vector can be thought of as the delivery system for the therapy internal to the body.

- 🔲 Finalise clinical trial plan for Phase 1 study - These are its plans for the Phase 1 study, we expect newsflow around this.

- 🔲 Take the therapy to a Phase 1 clinical trial - After all the pre-clinical data is gathered, ALA can choose to progress the therapy into Phase 1 clinical trials.

🔲 Phase 1 clinical trial for Solid Tumour Therapy (partnership with Imugene)

At this stage, the partnership is focused on completing proof of concept studies which can then be used to commence phase 1 clinical trials, the process usually follows this route:

- ✅ Prove its most promising treatment works in a test tube - ALA and Imugene have already done this - see our Quick Take on that news here: Arovella and Imugene therapy kills cancer in a test tube

- 🔄 Prove its most promising treatment works in mice - delayed (slightly) - The next step after test tube studies, this will see how the treatment works and if it is safe in a living organism (in vivo - mice studies)

🔲 Preliminary work on new gastric cancer and pancreatic cancer tech

An October licensing deal with Sparx Group has allowed ALA to expand the types of cancers that it could target.

ALA will be conducting due diligence activities on this technology, with the goal of combining it with its iNKT cell therapy platform:

- 🔄 Manufacturing updates - early work on seeing how the Sparx tech interacts with the iNKT cell therapy platform.

- 🔄 Prove its most promising treatment works in mice - This will see how the treatment works and if it is safe in a living organism (in vivo - mice studies)

What has ALA accomplished since we Invested?

We first Invested in ALA in February 2022. Below are all our articles on ALA since then.

In addition, all of our Quick Takes on ALA can also be found on our ALA Investment Memo page which gives a quick summary of why we Invested in ALA:

New Portfolio Addition: Arovella Therapeutics (Feb-2022)

We announce our new portfolio addition Arovella Therapeutic (ASX:ALA) and outline our Investment Memo for the company.

ALA on the Pathway to Phase I Clinical Trials (Apr-2022)

ALA ticked off a key milestone on the pathway to Phase I clinical trials selecting Q-Gen Cell Therapeutics as the manufacturer for its lead cancer treatment.

$23M capped ALA partners with $1.1BN Imugene - Now Targeting 90% of Cancers (Sep-2022)

ALA announced a partnership with $1.1BN capped Immune to develop its technology against solid tumour cancers.

$1.5M annual cost savings allows ALA to focus on what really matters (Oct-2022)

ALA announced that it would phase out its legacy operations to fully focus on the iNKT Cell therapy platform.

We just increased our Investment in ALA - Here’s why (Feb-2023)

We outline why we increased our investment in ALA, and what we think the future holds for biotech stocks in 2023.

ALA shows it can scale: Pathway towards an “off the shelf” cancer treatment (Apr-2023)

ALA presented new data at a key international conference to industry experts and opinion leaders in the cancer field.

ALA edging closer to clinical trials for “off the shelf” cell therapy cancer treatment (June 2023)

Two new deals announced in the cancer cell therapy space (both north of US$200M), while ALA announced its Share Purchase Plan.

New Deal: ALA can now target lung cancer, pancreatic cancer, gastric cancer (Oct 2023)

ALA announced a deal with “Spartex Group” to licence a technology that gives ALA the ability to target new cancers (pancreatic, gastric, lung).

🗣️A selection of our favourite ALA Quick Takes:

ALA narrows focus to iNKT cell therapy

Important European patent for iNKT technology secured

ALA gets option for cytokine tech to enhance iNKT platform

Arovella and Imugene therapy kills cancer in a test tube

ALA: Appointment of medtech veteran as Chairman

ALA’s laser-like focus on INkT cell therapy; costs cut

A boost for ALA’s cancer fighting tech?

📺Other videos resources:

Risks

All investments in small cap stocks carry risk.

These are the risks we are most conscious of at the moment for ALA.

Early Stage Biotech Risk

As with many early stage biotechs, a lot can go wrong in developing technology, particularly as ALA has yet to enter a clinical setting.

- The treatment is ineffective

- The treatment is not considered safe for human use

- Patient recruitment is delayed

- Ethics approval is delayed

Manufacturing risk

With this new technology acquired ALA will need to work out how to manufacture, at scale, its iNKT cell therapy platform together with the new technology.

As new technologies are added, the manufacturing process may become more complex.

We expect that ALA did its due diligence on this front before acquiring the technology, however there is still a risk of manufacturing challenges when ALA looks to produce at scale.

Funding risk

There is always the risk with small caps that more funding is required prior to major catalysts which could cause additional dilution to current holders.

Clinical trials are not cheap and ALA is not generating any material revenue.

ALA had a cash position of $5.3M at 30 September 2023 and we’ll know more about its cash position in the coming December quarterly which will be due by the end of January. ALA also received a ~$1.9M R&D Tax Incentive refund after the quarter.

Market risk

The market could sell off, or biotechs could sell off as a sector, impacting ALA’s share price regardless of its operational performance.

The market risks for ALA are linked directly to funding risk as capital markets for biotechs remain constrained.

Our ALA Investment Memo

In our ALA Investment Memo you’ll find:

- Key objectives for ALA

- Why we continue to hold ALA

- The key risks to our Investment thesis

- Our Investment plan.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.