Arovella Therapeutics (ASX:ALA) is an early stage biotech research company seeking to develop an off-the-shelf cancer cell therapy treatment - part of the broader field of cancer immunotherapy.

What is the macro theme?

Cancer cell therapy is a burgeoning industry and the next frontier of cancer treatments.

The worldwide spend on cancer therapies is immense and cancer immunotherapy, and cell therapy in particular, hope to unlock new avenues for treatment that are more efficient, more readily available, and ultimately, more successful at treating cancer.

ALA achieves a major breakthrough in cancer immunotherapy, and is acquired by a major pharmaceutical company for multiples of our Initial Entry Price.

Why did we invest in ALA?

New technology to treat cancer with large commercial upside

Cancer cell therapies exist today, but it is in a form that is inefficient, expensive and unreliable - it needs to be individualised to each patient and can cost up to $500K.

ALA's technology aims to produce an ‘off-the-shelf’ treatment that can be produced using healthy, non-patient specific engineered cells, which if successful, will have significant commercial value.

We are impressed with the board and CEO. Chairman Paul Hopper has backed a number of successful ASX-listed biotechs including Imugene (1,160% returns in under 2 years).

Cornerstone ALA investor Merchant Funds Management has an impressive track record in biotech investing.

Licensed technology from top research institutions

The two primary technologies that ALA has licensed both come from top cancer research institutions, the Imperial College in London and MD Anderson Cancer Center.

What do we expect ALA to deliver?

Objective #1: Prepare for Phase-1 clinical trial for treatment #1

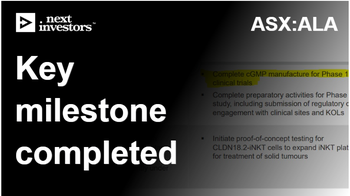

Preclinical studies have been completed for ALA’s first treatment (CAR19-iNKT) and we expect ALA to spend the next 12-18 months preparing for a Phase I clinical trial.

This involves completing the manufacturing milestones for the treatment, completing the trial design and securing ethics approval.

Objective #2: Undertake preclinical trials to confirm safety and specificity of treatment #2

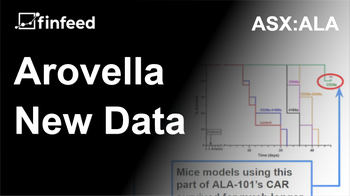

ALA will need to confirm that it’s second treatment (DKK1-CAR/mAb), can successfully combine with the iNKT technology and that it does not target healthy cells.

We expect ALA to do this through a preclinical study in mice.

ALA’s board has deep knowledge of the cancer immunotherapy market. If a compelling opportunity to licence further tech for their portfolio emerges, we want to see ALA expand on their existing base of technology.

Objective #4: Prepare for Phase-1 clinical trial for Solid Tumour Therapy (with Imugene)

We expect ALA to conduct proof of concept studies and commence IND-enabling studies for ALA-101 + onCARlytics. These include in vivo (test tube) and in vitro (mice) studies that form the basis for an IND application, which is a requirement for ALA to commence a Phase 1 clinical trial. [Added 2-Feb-2023]

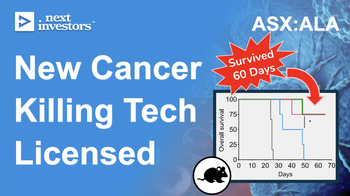

There are some standard risks that are associated with early stage biotechs, although the treatment appears effective in mice, this might not translate to humans. Key risks:

The treatment is ineffective

The treatment is not considered safe for human use

Patient recruitment is delayed

Ethics approval is delayed

Competition risk

There are a large number of companies targeting cancer cell therapies. If a company makes a breakthrough targeting the same disease or using a similar technology to ALA, it may damage the commercial value of ALA’s technology.

Manufacturing risk

As ALA has licensed cutting edge technologies, it may encounter difficulties in the manufacturing process. These could include hurdles found in the manufacturing partner selection process or difficulties scaling the process.

Funding risk

ALA says it is fully funded to prove out the safety profile and get initial manufacturing going through to Phase I trials, but should additional research be needed or manufacturing hurdles encountered, ALA may need to raise more funds before Phase I trials can commence.

We have added this risk to the ALA investment memo going forward.

Biotechs have been out of favour for a long period and this likely impacted ALA’s share price performance, and may impact it in the future.

The market risks for ALA are linked directly to funding risk as capital markets for biotechs remain constrained.

What is our investment plan?

We plan to patiently wait with our investment as the company delivers on the above objectives towards its next major catalyst, which for ALA is the commencement of Phase I clinical trials in the first half of 2023.

We will hold the majority of our position into the Phase I trial and re-assess our investment based on the results. As with all our early stage investments we will look to take some profit in the lead up to the key catalyst event, looking to sell ~20% of our position.

Disclosure: The authors of this article and owners of Next Investors and Finfeed, S3 Consortium Pty Ltd, and associated entities, own 13,631,579 ALA shares. S3 Consortium Pty Ltd has been engaged by ALA to share our commentary on the progress of our investment in ALA over time.

Our Investment Summary

Date of Initial Coverage

18-Feb-22

Inital Entry Price

$0.038

Returns from Initial Entry

68%

High Point

453%

Investment Milestones for ALA

✅ Initial Investment: @3.8c ✅ Top Slice 🔲 Free Carry ✅ Increase Investment 1: @2c 🔲 Top Slice 🔲 Free Carry ✅ Increase Investment 2: @4.5c 🔲 Top Slice 🔲 Free Carry 🔲 Price increases 300% from initial entry 🔲 Price increases 500% from initial entry 🔲 Price increases 1000% from initial entry ✅ 12 Month Capital Gain Discount 🔲 Hold remaining Position for next 2+ years