We just increased our Investment in ALA - Here’s why

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 21,131,579 ALA shares at the time of publishing this article. The Company has been engaged by ALA to share our commentary on the progress of our Investment in ALA over time.

A few weeks ago, a child in the UK received a “base edited” cell therapy for leukaemia.

The child went into remission (was cured) within four weeks:

This was a major breakthrough in the fight against cancer — this success had never been achieved before with this type of cell therapy.

Cell therapy is an arm of cancer treatments that uses the body's own immune system to fight the disease.

This cutting edge technology could be the key to cracking the cancer “code”. It is the focus of billions of dollars of R&D right now - and we have taken a position.

We first Invested in early stage cell therapy biotech Arovella Therapeutics (ASX:ALA) in February 2022, where our Initial Entry Price was 3.8 cents. We recently increased our Investment in ALA’s January capital raise at 2 cents.

Our average ALA Entry Price is now ~2.7 cents, which is around where ALA is trading right now.

ALA is progressing a number of cancer cell therapy treatments to clinical trials.

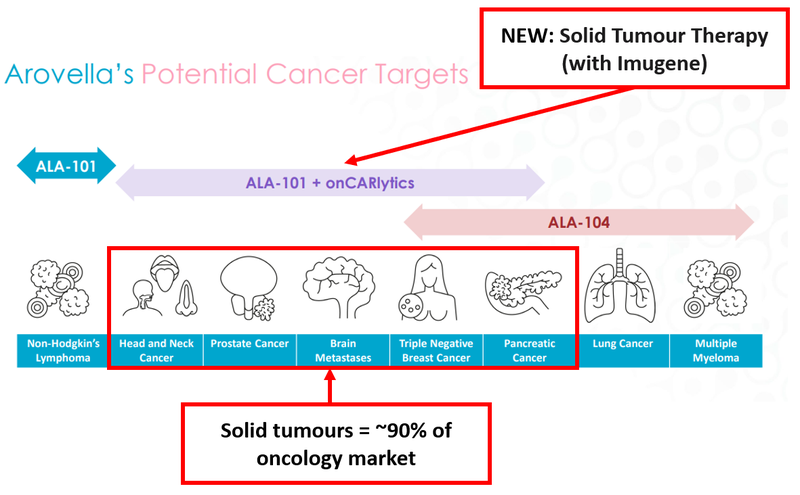

Now in partnership with the ~$899M capped Imugene, ALA’s technology aims to treat solid tumours, which accounts for 90% of all cancers.

ALA’s treatment could prove to be cheaper, more readily available, and more effective than existing cell therapy treatments.

ALA has just raised money and we think it now has a clear runway to get its treatment for solid tumours into clinical trials over the next 12-18 months - which we think could significantly re-rate the stock.

Achieving these things won’t be straightforward (it’s cutting edge scientific research) and ALA isn’t alone in cell therapy - there are a lot of companies out there looking to advance cell therapy using T cells.

In contrast to those companies though, ALA uses iNKT cells which we think gives it certain advantages.

Today we will lay out why we chose ALA in particular for our Portfolio and how success could re-rate the ALA share price.

Why we are Investing in biotech stocks in 2023

After watching the cell therapy space closely for over a year now, we like what we see — both from a Investment perspective and a moral perspective.

Cancer is a nasty disease and many of us have been directly or indirectly impacted by it.

We want it gone.

So there’s a moral element involved when we Invest in companies that have goals of improving health outcomes and saving lives.

From an investment perspective, cancer is arguably the biggest target to hunt down in the life sciences — an estimated US$200BN was spent globally on oncology in 2022.

Cell therapy is just one sector in the wider biotech space.

Things are tough right now for pre revenue small cap biotech stocks - there just isn't as much “risk capital” available compared to 2021, and completing clinical trials is a capital intensive endeavour.

ALA has not been immune to the broader downturn in early stage biotech stocks.

This is part of why we participated in the 2 cent ALA placement a couple of weeks ago.

In our view, there are attractive valuations around in tech and biotech after a rough 2022, so we will look to put money into any placements that come up in our tech/biotech portfolio companies.

We think this weakness is a cyclical moment, one that isn’t in keeping with broader trends in advances in life sciences — and even with the current out of favour nature of biotech stocks, it’s still the case that successful clinical trials can deliver large rewards for investors.

Why we like ALA’s technology

The short version of why we like ALA’s cancer fighting tech is this...

ALA’s treatment could prove to be cheaper, more readily available, and more effective than existing cell therapy treatments.

It’s early days, but here are the specifics of how ALA’s treatments could have important advantages over existing CAR T cell therapies:

- It’s “off the shelf” - meaning the treatment doesn’t need to draw cells directly from the patient themselves i.e be “tailored”; and

- The treatment naturally suppresses GvH disease (where the body rejects the donor’s cells).

It’s the “tailored” approach of current CAR T cell therapies that leads to high treatment costs - often these therapies cost over $500,000 per patient.

Even better is the fact that ALA’s treatments are targeting both blood cancers AND solid tumours, which together make up more than 90% of cancers.

This means the technology could have many broad and varied applications - meaning a very large potential market.

As a result, we don’t have any qualms about saying that ALA’s share price could re-rate to multiples of our Initial Entry Price of 3.8 cents, such is the magnitude of the preclinical cancer-fighting tech that ALA is developing.

But at the end of the day, ALA remains a pre-clinical stage company - so we think that re-rate hinges on ALA successfully reaching clinical trials. We are hoping that its first clinical trial starts in the next 18 months.

We know what happens with biotechs when a breakthrough is made too — bigger players start circling, looking to integrate the new tech into their R&D pipelines via an acquisition - keep reading for the valuations ascribed to successful cell therapy companies.

After successful treatments in mice for its standalone treatment (which it is now combining with Imugene’s treatment), at this stage, there is still a big IF around whether ALA’s tech works in humans.

This is what clinical trials are all about and ALA has much work ahead of it in order to de-risk its treatments (see our risks section further down this note).

At the same time, it’s the kind of biotech Investment we explicitly look for, and a strategy that has worked for us previously in other sectors.

We like to Invest early in high risk/high reward stocks, and patiently wait for a major catalyst. At that point when speculation is at its highest, we like to de-risk a portion of our position and hold the remainder in hope of a successful outcome and sustained share price re-rate, but are also prepared for failure.

ALA now has cash to achieve its 2023 objectives

In mid January, ALA completed a $1.65M placement at 2c - this is the placement which we recently participated in.

So with a market cap of ~$20M and a cash balance of ~$5.1M (cash balance of ~$3.5M as of 31 December 2022 + ~$1.6M placement), we estimate this leaves ALA with an Enterprise Value (EV) of ~$15M at the current price of 2.6 cents.

Every little bit of cash counts, and ALA has ditched its legacy “OroMist” business in order to reduce its cash burn.

There’s only up to $300k left to pay off in restructuring costs, which we’re glad to see go (as this re-structure should save ALA $1.5M a year).

It also helps that directors have recently been taking fees in shares rather than cash.

Despite ALA being below our Initial Entry Price, we think the cash from the placement leaves ALA with enough runway to deliver on key catalysts in the next 6-18 months, and room for its share price to re-rate as well.

How is ALA going to deliver for its shareholders?

ALA has (for now) three shots at creating significant value for shareholders such as ourselves.

The chart below shows the range of cancers ALA is targeting with its three treatments.

The most recent, and perhaps most promising, is the latest cell therapy treatment that ALA is working on with the $899M-capped Imugene:

The cancers highlighted in the image above are solid tumours. In a previous note on ALA we outlined how these cancers make up roughly 90% of the total cancer market.

Finding treatments for these cancers is seen as the “Holy Grail” of oncology because they affect so many.

Given how big a deal this is - we’re adding a new Objective to our ALA Investment Memo (Investment Memos are how we track companies’ progress over time) to reflect the importance of the Imugene partnership, which we call the Solid Tumour Therapy (with Imugene).

Back to the crux of the matter though - what does ALA need to do to achieve a major re-rate?

We think the short answer is: ALA could re-rate if the company moves any of the three cell therapy treatments above into a Phase 1 clinical trial.

Biotechs like ALA can generate significant shareholder value by simply advancing their projects to trials.

Curing cancer as a standalone business would be nice, but the sheer amount of time it takes to go from discovery to full-scale commercialisation (~10 years) and the multiple hurdles (Phase 1, 2, 3 trials + regulatory approval) makes this outcome unlikely.

In addition, small cap biotech stocks typically get taken over before they bring a drug to market. Big pharma wants de-risked technology, and is prepared to pay for it.

But let's not get too far ahead - we’re very much focussed on the here and now for ALA - and that’s the steps needed to reach clinical trials.

These trials would represent a big achievement in their own right, as ALA occupies a very small niche of the wider oncology market.

We’re aware of only three other cancer immunotherapy companies that currently have similar technology to what ALA is working on.

No doubt, this is cutting edge cell therapy research that few companies are either willing or able to take on.

So with cash harder to come by in the biotech sector right now, we think promising new tech could be snapped up by larger players at significant premiums as they look to outsource their R&D pipelines.

A good setting for our ALA Big Bet:

Our Big Bet

“ALA achieves a major breakthrough in cancer immunotherapy, and is acquired by a major pharmaceutical company for multiples of our Initial Entry Price.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved, and it will require a significant amount of luck. There is no guarantee that it will ever come true. Some of these risks we list in our ALA Investment Memo.

Our ALA Progress Tracker

To visualise what ALA has done since we Invested, check out our Progress Tracker for ALA:

It takes just a few minutes to scroll the ALA Progress Tracker to get a quick helicopter summary of progress, which we find helpful to do before reading each new ALA announcement.

A quick scan of the Progress Tracker helps give context to how the new announcements contribute to our Big Bet and near term Investment Memo objectives for ALA.

Our ALA Investment Memo

We track our Investments using Investment Memos which lay out what we expect from a company, but in this case, a new and promising avenue of research opened up for ALA.

One which we think will be important to the company’s future success.

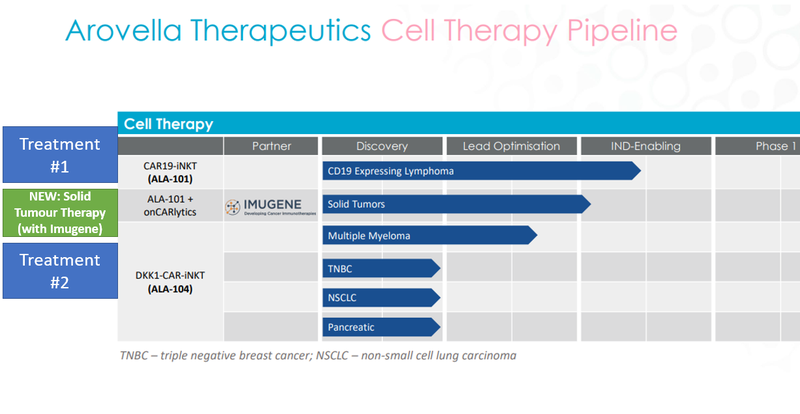

When we first Invested in ALA, our initial ALA Investment Memo focussed on two different treatments it had in its preclinical pipeline.

As before, ALA is progressing 3 cell therapies treatments, all at varying stages of development:

The treatments (treatments #1 and #2) at the top and bottom of the chart are the ones ALA started out with.

ALA subsequently partnered with Imugene in September of last year to work on a therapy that combines one of these treatments with Imugene’s onCARlytics technology that greatly expanded the number of cancers ALA’s treatment could target.

As a result, we think this warrants an update of our ALA Investment Memo to reflect the importance of the Imugene partnership.

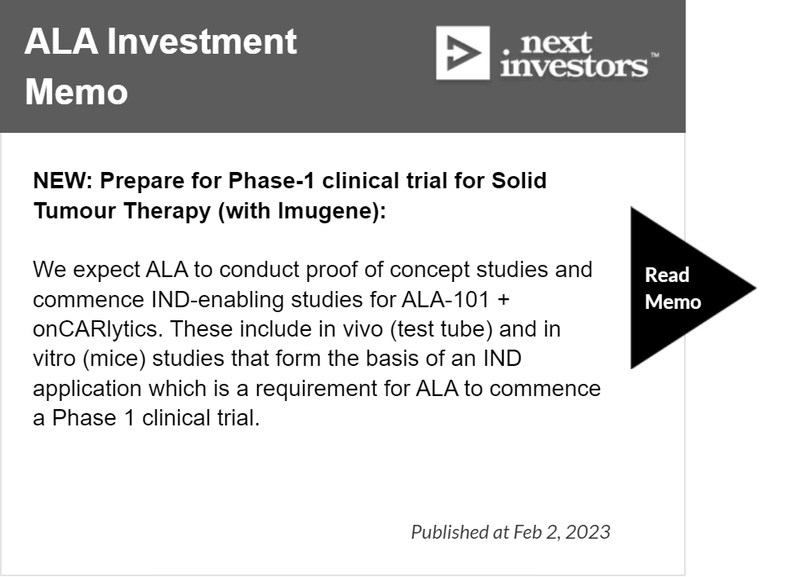

New Objective: Prepare for Phase-1 clinical trial for Solid Tumour Therapy (with Imugene)

Due to the very early stage nature of the ALA partnership with Imugene, specifics of the funding of the partnership are not available.

That being said, we suspect ALA will be funding the majority of this early work for relatively little outlay and commercial terms will be thrashed out later if the research program is successful.

We’re calling the treatment that ALA is working on with Imugene “Solid Tumour Therapy (with Imugene)” for ease of reference.

Solid Tumour Therapy (with Imugene) now makes up Objective #4 of our updated ALA Investment Memo:

Let's now zoom into the details of what needs to happen here.

An Investigational New Drug (IND) application is required by the US regulator to get ALA’s treatment to Phase 1 clinical trials.

This means ALA needs to do test tube studies and mice studies to prove its pharmacological and (hopefully) lack of toxicological properties.

Simple explanation: an IND application will answer two questions for regulators - how does ALA’s Solid Tumour Therapy (with Imugene) work and is it safe in test tube and mice studies?

ALA has had success before with its lead treatment in test tube and mice studies (ALA 101, treatment #1) - it very quickly kills cancer in mice.

So the company now needs to show that the combination of this treatment with Imugene’s tech works and is safe before trying it out on humans.

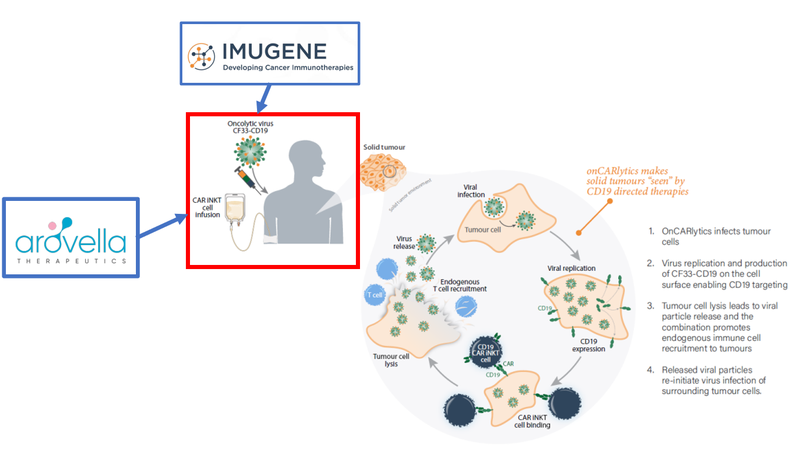

Here’s how this would work in practice in a potential Phase 1 study:

Patients would receive an infusion of ALA’s treatment #1 and a jab of Imugene’s treatment.

Roughly speaking, the Imugene jab would contain a virus that helps ALA’s treatment #1 get in and kill the cancer cell by showing it where to find the cancer.

The Imugene treatment is, by itself, in two Phase 1 trials already - which means it has previously passed the safety test when it comes to test tube and mice studies — we think this bodes well for ALA’s Solid Tumour Therapy (with Imugene).

A quick rundown on what’s happened at ALA since our last note

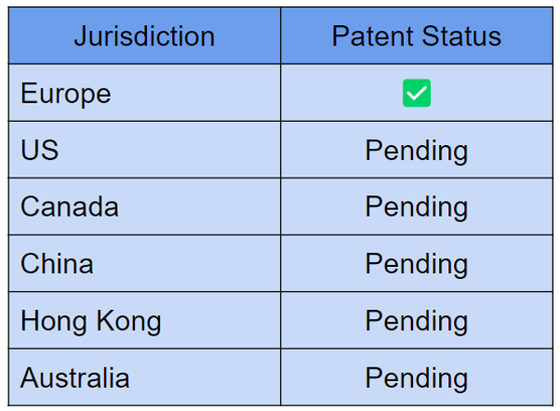

European patent secured ✅

ALA has been busy securing its intellectual property and in November, the company announced that a European patent for its iNKT cell therapy platform is slated to proceed to grant early this year.

This means that the granting is simply a formality.

The patent covers the manufacture of CAR-iNKT cells and can be found on the European Patent Office website.

ALA has patents pending in other major jurisdictions as below:

ALA has also been expanding its portfolio of licensed technologies.

Booster tech option agreement ✅

In December, ALA announced it had signed an exclusive option to licence a cytokine technology.

Cytokines are small proteins important in cell signalling for the immune system and we see the use of this technology as a potential “booster” for ALA’s existing iNKT platform.

In other words, the cytokine tech can cause iNKT cells to persist for longer, so they don’t get cycled out of the body as quickly, boosting their effectiveness.

The Professor behind the cytokine technology, is Gianpietro Dotti of the University of North Carolina’s Lineberger Comprehensive Cancer Center who is an eminent scholar in the field iNKT cells:

A quick search of Professor Dotti’s publications yields more than 193 works which he has either authored or contributed to — a rough measure of his significant influence in the field of cancer immunotherapy.

Importantly, Dotti also worked on a program studying the CD19-specific chimeric antigen receptor (CAR) — the very same receptor that ALA is working on in its upcoming slate of preclinical trials that will involve Imugene’s onCARlytics platform.

The exclusive option agreement, which was for an “immaterial” (small) cost, lasts for 15 months and has two primary benefits:

- If initial data is good, it allows ALA to secure an enhancement to its technology

- Because it is exclusive, it gives ALA a potential leg up over other iNKT cell therapy companies

New chief operating officer ✅

Furthering ALA’s aim of preparing for a Phase 1 trial, ALA has added a chief operating officer, Dr Nicole van der Weerden.

We see the appointment of Dr van der Weerden as a sign that ALA is now gearing up for a more labour intensive period that we hope brings positive newsflow.

Here’s more on what we expect from ALA in the coming 6-18 months.

What’s next for ALA?

ALA has an expanding research program and we know that biotech research doesn’t proceed in a linear fashion and timelines sometimes get stretched.

Here’s the three things we most want to see next from ALA that could catalyse the share price:

- Prove its most promising treatment works in a test tube

- Prove its most promising treatment works in mice

- After this, take any of its three treatments to a Phase 1 clinical trial

Before that happens we want to see this first of all...

Complete manufacturing of Treatment #1 (Non-Hodgkin's Lymphoma) 🔄

ALA needs to show it can scale up the process and produce sufficient quantities of the treatment. ALA has selected Q-Gen Cell Therapeutics (Q-Gen) for this, which is the cell therapy manufacturing arm of the QIMR Berghofer Medical Research Institute (QIMR Berghofer).

Based in Brisbane, Q-Gen has successfully produced cell therapy products for clinical trials and can produce cellular immunotherapies for patients in Australia, Asia, Europe and the US.

Next we want this to happen...

In vivo (test tube) studies for Solid Tumour Therapy (with Imugene) 🔄

This will check to see the treatment can kill cancer cells and does not attack healthy cells.

In vitro (mice) studies for Solid Tumour Therapy (with Imugene) 🔄

The next step after test tube studies, this will see how the treatment works and if it is safe in a living organism.

Commence a Phase 1 clinical trial Solid Tumour Therapy (with Imugene) 🔄

We think this is the ultimate end goal for ALA right now, and relies on successful test tube and mice studies.

Bonus: Commence a Phase 1 clinical trial with treatment #1 for Non-Hodgkin’s Lymphoma 🔄

This by itself would be a major step for ALA. Non-Hodgkin Lymphoma is another nasty cancer that attacks the lymph nodes — while not on the scale of the solid tumour market, the market for this cancer is still ~US$8BN.

Bonus: Advance treatment #2 (ALA 104, DKK1-CAR-iNKT) 🔄

While Solid Tumour Therapy (with Imugene) is the big shiny target, we’re also looking for ALA to advance this treatment for a range of less prominent, but still important, cancers.

What else is happening in the cell therapy space?

Science, and oncology in particular, is advancing quicker than it ever has in human history.

The major global pharmaceutical companies worth tens of billions (J&J, Pfizer, Novartis, Roche etc) are attuned to this and are busy acquiring promising cell therapy companies, leading to some big valuations being attached to companies in the space.

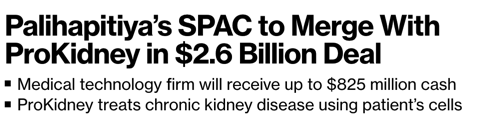

In January, despite the out of favour nature of the biotech sector, famous investor Chamath Palihapitiya’s special purpose acquisition company (SPAC) put together a total funding package of US$825M via a merger for ProKidney (now valued at US$2.5BN) to advance Phase 3 development of a cell therapy for kidneys.

So there’s clearly still large pools of capital funding this sector - even in recent weeks.

Other companies are also able to link up with the advancements in cell therapy with their own technology.

Notably and closer to home, is the ~$900M capped ASX listed Imugene, a company which ALA is partnered with (more on this partnership later).

Other peers in the specific cell therapy space that ALA is working in include MiNK Therapeutics, which at one stage reached a market cap as high as ~US$650M.

There’s also Appia Bio which got US$875M in a strategic partnership with Kite Pharma which is owned by the US$105BN-capped Gilead Sciences.

This demonstrates that there's a lot of money around to back successful cell therapy companies, and we hope ALA can one day join these much larger peers.

ALA is a very early stage cell therapy company - with the valuation to match - ALA is capped at ~$20M right now, with ~ $5.1M in the bank following its recent capital raise.

As you can see with the big numbers above, there’s significant upside here if ALA can succeed in proving its technology is effective.

However, testing in the clinic is going to take time. For this reason, ALA is a long term investment for us.

We like ALA’s technology, the leadership team in place, and ultimately ALA’s potential to make a major breakthrough in cancer immunotherapy and in the process, re-rate significantly.

More on the CAR T cell breakthrough

Closing out Christmas weekend with some fantastic news:

— ALL-IN TOK (@all_in_tok) December 26, 2022

Alyssa in the UK was cured of blood cancer thanks to a new T-cell treatment!

This is a huge breakthrough in human longevity and quality of life, @chamath celebrates 👇 pic.twitter.com/6lvWNl754h

Key takeaways:

- 13 year old patient was diagnosed T-cell acute lymphoblastic leukaemia

- All other treatments failed

- Treatment involved “base editing” - chemically converting single nucleotide bases (letters of the DNA code) which carry instructions for a specific protein

- This was CAR T cell therapy - multiple DNA changes were needed to create banks of ‘universal’ anti-T-cell CAR T-cells for this study

- Overall, we think this demonstrates the potential of cell therapy to treat a growing range of cancers

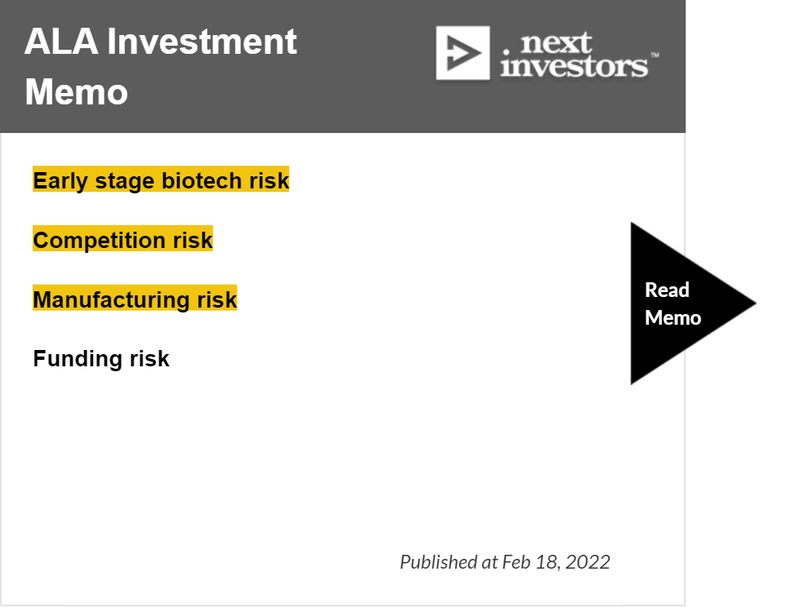

Risks

We’re now focussed on the three risks below for ALA:

ALA is a pre-clinical biotech, meaning it faces a unique set of hurdles.

Although ALA’s standalone treatment (ALA-101) appears effective in mice, this might not translate to humans when combined with Imugene’s technology, which we are calling the Solid Tumour Therapy (with Imugene).

Competition risk is an ever-present aspect of ALA’s work and although only three other companies to our knowledge are working on iNKT cell therapies, breakthroughs can happen elsewhere and diminish the need for ALA’s treatment.

Finally, manufacturing risk involves the scale up of the process that ALA needs to accomplish for the treatment to be viable in a clinical setting.

As for funding risk, the recent capital raise sees any concerns there as being resolved for the near term. ALA seems to have enough cash to allow itself to kick some goals and hopefully grow in value over 2023 before needing to raise again.

Our updated ALA Investment Memo

In our updated ALA Investment Memo you’ll find:

- Key objectives for ALA

- Why we continue to hold ALA

- The key risks to our Investment thesis

- Our Investment plan.

For more in depth coverage, you can find our ALA initiation article here: New Portfolio Addition: Arovella Therapeutics.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.