Inflation, US Fed Reserve, Bond Yield, Cash Buffer Portoflio

Published 31-JAN-2022 15:01 P.M.

|

28 minute read

The pain in the markets continued this week, with many of our small and micro-cap stocks bearing the brunt of it.

We can sense the fear in the market, but as long-term investors we remain firmly committed to our portfolio companies.

As a result, what follows today is a look at how we see things playing out in the market now and into the future.

We’ll also share with you what we (internally) call the ‘Cash Buffer Portfolio’ - companies we hold that are best placed to ride out any future storm of negative sentiment with a decent chunk of cash in their bank, raised while the market was strong.

We’ve seen the market bounce back before after a range of mini-panics — these notably include the one in May, during the Evergrande mess, the soft December conditions, and the current panic playing out right now.

Decent cash balances should help these companies execute on their plan through this current rough patch in the market.

Bottom line: we think our carefully selected small and micro-cap stocks will reward our long-term conviction.

And despite the recent pain, the last 24 months saw many of the small and micro-cap stocks in our portfolio tack on multiples of where we entered.

For anyone who only started investing after the March 2020 rally got underway, it would be easy to assume this is how markets are at all times.

More seasoned investors know though that the last two years have been an exception to the norm, and that the ‘all-green everyday’ ride had to end eventually.

So markets started this week in exactly the same manner they left off on Friday, leaving a sea of red across most of our portfolio.

Words like ‘panic’ and ‘contagion’ get thrown around in the mainstream media at times like these as everyone starts to question the narrative.

One key question keeps coming up however.

Why?

Here are some short answers: inflation leading to tightening global monetary policy, the crisis in Ukraine, bond yields, profit-taking by big funds and general mainstream media bear narratives.

We think trying to lay your finger on a single cause is a largely fruitless exercise in short-termism. It’s usually a combination of all these readily available answers plus ones you may not even know about yet.

So around our virtual (Metaverse?) office yesterday, we surveyed opinions and came to two interesting conclusions.

Conclusion #1: Given how much focus gets put on the top end of the market (ASX200, S&P 500 etc), a bear market for these indices is a genuine possibility.

Remembering that a bear market is usually defined as a 20% fall from recent highs, we want to stress the following...

Conclusion #2: While a bear market may drag down smaller stocks initially, these indices may stabilise as investors cycle into commodity stocks and more of these stocks enter the top-end of the index.

We’ve often written to you about our belief in a “commodity supercycle” and why we intentionally weighted our portfolio towards these types of stocks (especially in energy and battery materials).

And it comes back to a single thing - cheap cash.

Yes, declining ore grades, a history of low exploration expenditure, fiscal stimulus and increased demand from emerging industries are all crucial factors.

But for us, it's the loose monetary policy that really lit a fire under the commodities supercycle we see playing out right now.

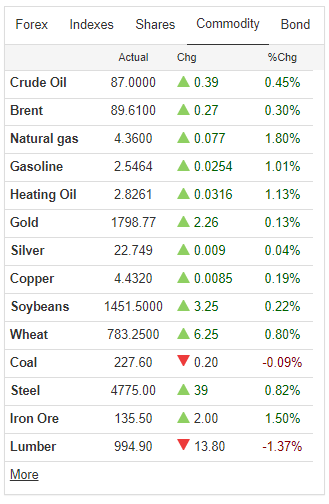

Have a quick peek at this list of commodity prices on Friday:

Most of them were in the green - it's why huge resource companies like Rio Tinto and BHP are near all-time highs, despite the broader market wobbles across most other sectors.

That’s telling us something important - primarily, that the tunnel-vision focus on the big indices is not telling the whole story.

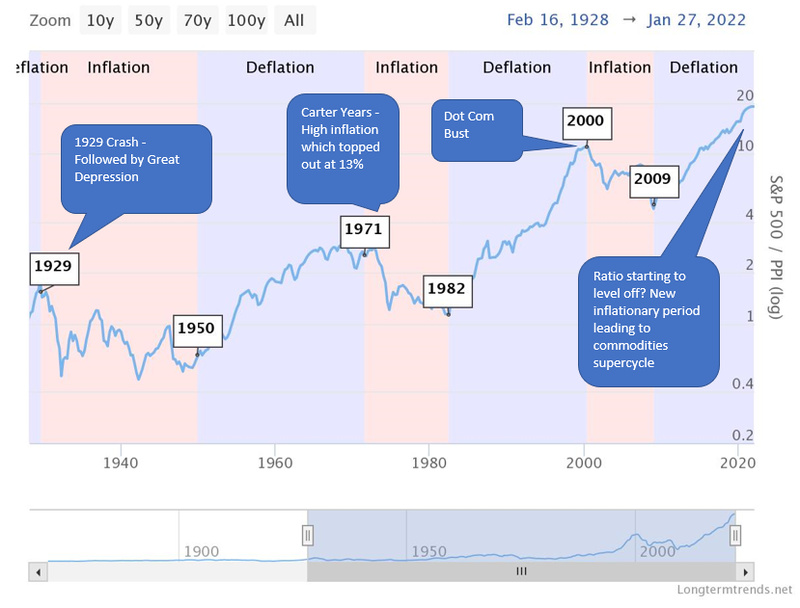

Which is why we like to refer back to one powerful chart when the market notches another bad week:

In deflationary periods or periods of low inflation, the S&P 500 (which is now heavily weighted towards tech) outperforms commodities. In periods of high inflation, commodities outperform the S&P 500. As you can see, over the last year the S&P outperformance is starting to level off which we believe is further evidence that we are in the middle of a new commodity supercycle.

Which is again, why we think the big indices may stabilise as investors cycle into commodity stocks and more of these stocks enter the top-end of the index.

And the more cash and confidence the commodity super majors have, the more they will be in the market to acquire smaller companies who can delineate a quality asset, companies like those in our portfolio

We think this commodity supercycle is fuelled by all the cheap cash sloshing around the market.

Here is a quick rundown on how loose monetary policy works in practice for investors.

We think this is fundamental to understanding why we hold the positions that we write to you about every week.

We watched the US Federal Reserve press conference and this is what we concluded...

The US Federal Reserve held a press conference on Thursday that was hotly anticipated - we watched it because the statements they release impact global markets, which in turn impacts the small cap stocks in our portfolio.

With inflationary pressures creeping up Western economies and the US experiencing >7% inflation over the last year, all eyes were on Jerome Powell who was expected to convey a message signalling “tighter” monetary conditions.

Federal Reserve Chair Jerome Powell as expected stated that they were willing to do whatever it took to maintain price stability but he also caveated that by saying they were going to start thinking about unwinding the Fed’s balance sheet.

He also mentioned that he expected tighter monetary policy wouldn’t affect employment or growth - pretty much saying that cash rates are expected to rise without affecting employment, growth or asset prices.

The reality is this is the same person who only a few months ago was calling inflation “transitory” in their press conferences.

It seems to us like the Fed are playing catch-up with inflation and now find themselves on the back-foot. For the Fed to signal upcoming tighter monetary policy is a sharp 180 degree shift in stance.

So why does this matter to us?

It is actually pretty simple to explain the connection between all of the stuff about the Fed and our micro-cap stocks.

Signalling tighter monetary policy means that cash-rates (the thing that is used to price mortgages, personal loans or car loans) are expected to increase. This means that people should be expected to be paid to hold savings in a term-deposit at a higher interest rate then they would be getting paid today.

For example, the current term-deposit rates across the big 4 Aussie banks sit at around the 0.1% rate and as a result of these low-funding costs, banks are able to offer loans to people starting at ~1.8-2%.

This essentially means that money is “cheap”, you get paid very little to hold it in a savings account and you pay very little to borrow it.

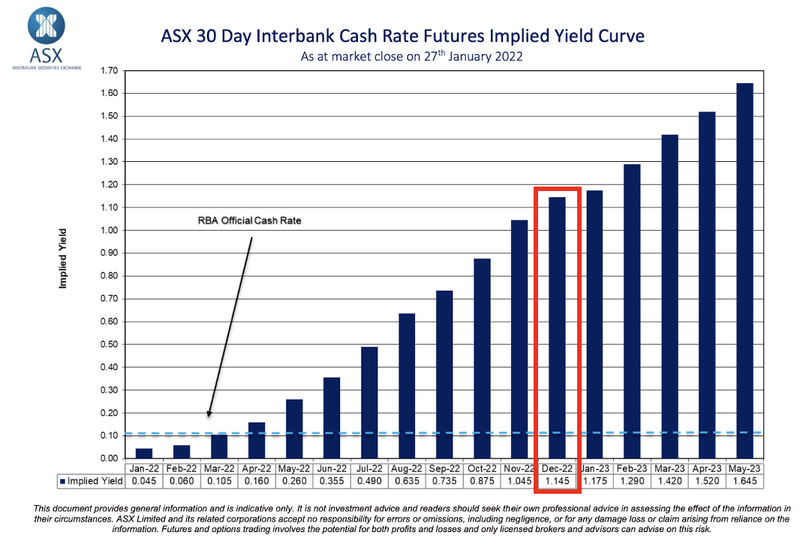

With the signalling from the US fed towards a shift to “tighter monetary policy”, rate expectations are now starting to creep higher globally.

Just in Australia, we have seen rate expectations move significantly higher with the implied cash rate in Dec-2022 being ~1.1% a whole 1% higher versus today.

This isn't somewhere we haven't been before, we remember the times when a term deposit would pay 4-5% on savings in a bank account - happy days for those with savings.

So the 1% could be mistaken for an anomaly.

The reality is that with a lot more debt in the global financial system any incremental change in the interest rate translates into significantly more capital being used to finance these debts.

A move from a cash rate of 4% to 5% is an increase of 25% whereas the movement from 0.1% to 1.145% is an almost 10x increase. This is why any incremental movement from the low base has significant implications.

The key take-away from this is tight monetary policy leads to higher interest rates which leads to investors being more cautious with their funds because now there is a more material “opportunity cost” - be it the increased interest rate for the mortgage on the house (paying higher interest) or the interest the bank is willing to pay an investor for holding their cash (receiving interest).

How we think this affects our portfolio of micro-cap stocks

When the small cap markets are running hot and “cheap” money is plentiful, raising capital is significantly easier to do - but this doesn’t last forever.

The recent market wobbles and potential interest rate rises led to our team getting together to ask “which of our portfolio companies have recently raised cash and will be able to see out periods in which access to capital won't be as easy?”

Markets often view capital raises in a negative light given most of the time the capital raises are done at discounts to market prices and generally because they lead to a short term movement lower in the company’s share price as some investors sell any time the stock trades above the cap raise price.

We look at capital raises a little bit differently.

Large capital raises help companies see out times like this, having a cash buffer helps companies operate without having to think about how they will try to raise cash during a period of market turbulence where investors sentiment is negative and share prices are low.

Raising money in good times typically means companies are also raising that cash at much more favourable terms (higher share prices) which reduces the impact of dilution to existing holders.

This compares to raises done in more volatile conditions like now, amid rate hike fears and geopolitical uncertainty. Investors are less willing to part ways with their cash and so the whole process distracts companies from focussing on their operations.

With company quarterly cash flow reports now coming out, it’s a good time to look at our portfolio companies to see who some of our portfolio companies that we think did a great job of timing a capital raise during good times, ahead of the recent market volatility.

Below are those companies.

We’d like to call it the ‘Cash Buffer Portfolio’ split into our portfolios:

Next Investors “Cash Buffer Portfolio” - which of our companies have a decent amount of cash in the bank:

Kuniko (ASX: KNI)

- Cash in the bank at 30/09/21 = $7.1M

- Raised $7.9M @20c in August 2021.

Oneview Healthcare (ASX: ONE)

- Cash in the bank at 31/12/21 = €15.1M

- Raised A$20m @ 27c in November 2021

Vulcan Energy Resources (ASX: VUL)

- Cash in the bank at 30/09/21 = €187M

- Raised A$203m @ $13.50 in September 2021

Elixir Energy (ASX: EXR)

- Cash in the bank at 30/09/21 = $30.9M

- Raised A$10m @ 36c in April 2021

- Raised A$16.6m @ $36c in May 2021

Province Resources (ASX: PRL)

- Cash in the bank at 31/12/21 = $22.3M

- Raised A$18m @ 15c in May 2021

Euro Manganese (ASX: EMN)

- Cash in the bank at 30/09/21 = $31.2M

- Raised A$25m @ 60c in March 2021

- Raised A$5m @ 60c in May 2021

Tempus Resources (ASX: TMR)

- Cash in the bank at 30/09/21 = $4.3M

- Raised A$6.3m @ 28.35c in September 2021

Dimerix (ASX: DXB)

- Cash in the bank at 31/12/21 = $16.2M

- Raised $20m @ 20c in August 2021

- Raised $4m @ 20c in October 2021

Advanced Human Imaging (ASX: AHI)

- Cash in the bank at 30/09/21 = $330K PLUS US$10.5m (A$15M) @US$0.75 (A$1.07) in November 2021

88 Energy (ASX: 88E)

- Cash in the bank at 31/12/21 = $32.3M

- Raised $24m @ 2.8c in September 2021

Invictus Energy (ASX: IVZ)

- Cash in the bank at 30/09/21 = $7.3M PLUS $3.5m @ 10c in December 2021 PLUS $4m @ 10c In January 2022

Vonex Limited (ASX: VN8)

- Cash in the bank at 30/09/21 = $10.2M

- Raised $12m @ 11c in July 2021

- Raised $2m @ 11c In August 2022

Pantera Minerals (ASX: PFE)

- Cash in the bank at 30/09/21 = $6.3M PLUS $1.5m @ 20c in December 2021

Galileo Mining (ASX: GAL)

- Cash in the bank at 31/12/21 = $9.01M

Los Cerros (ASX: LCL)

- Cash in the bank at 30/09/21 = $23.4M

Pursuit Minerals (ASX: PUR)

- Cash in the bank at 31/12/21 = $7.4M

BPM Minerals (ASX: BPM)

- Cash in the bank at 31/12/21 = $4.4M

🦉 Wise-Owl “Cash Buffer Portfolio”:

European Metals Holdings (ASX: EMH)

- Cash in the bank at 30/09/21 = $7.4M PLUS A$14.4m @ $1.40 in January 2022

Auroch Minerals (ASX: AOU)

- Cash in the bank at 31/12/21 = $9.1M

- Raised A$8m @ 16c in October 2021

BOD Australia (ASX: BOD)

- Cash in the bank at 30/09/21 = $6.2M

FYI Resources (ASX: FYI)

- Cash in the bank at 30/09/21 = $10.2M

Evolution Energy Minerals (ASX: EV1)

- Cash in the bank at 31/12/21 = $10.7M

- Raised $22m @20c in November 2021.

🏹 Catalyst Hunter “Cash Buffer Portfolio”:

Mandrake Resources (ASX: MAN)

- Cash in the bank at 31/12/21 = $16.4M

TechGen Metals (ASX: TG1)

- Cash in the bank at 31/12/21 = $3.1M

Ragusa Minerals (ASX: RAS)

- Cash in the bank at 31/12/21 = $3.4M

Aldoro Resources (ASX: ARN)

- Cash in the bank at 30/09/21 = $4.3M

- Raised $2.4m @40c in August 2021.

📰 This week on Next Investors

We closed off the week by covering our junior gold exploration investment Tempus Resources (ASX:TMR) who reported bonanza grade gold assays from its newly discovered “Blue Vein” discovery.

TMR’s gold project has historically produced over 230,000 ounces of gold. It is now trying to expand on this historic resource by making new discoveries and hopes to put the project back into production.

The assays marked the second “bonanza grade” gold-hit from the newly discovered vein with intercepts from a depth of 111m, including 2.7m grading 13.4g/t gold and includes a 0.5m intercept of 71.3g/t gold.

One of the two assays returned mineralisation of almost three times what we were hoping, so it looks to be game-on at the Blue Vein discovery.

📰 Read the full breakdown: TMR’s “Blue Vein” discovery mineralised along strike - Exceeding what we wanted to see

In our other portfolios 🧬 🦉 🏹

🏹 Catalyst Hunter

This week in the Catalyst Hunter portfolio we put out an update on our 2021 Pick of the Year Grand Gulf Energy (ASX: GGE).

We touched on the US government’s plan to invest US$50B to develop its semiconductor manufacturing industry in a bid to maintain its edge over China. With helium being critical to the manufacturing process of semiconductors, we see GGE’s asset as strategically well located.

GGE has commenced the permitting process for its upcoming maiden drilling program, and has appointed the highly experienced Doug Frederick as the drilling superintendent.

Frederick brings significant experience to the GGE team, having worked on the analogous Doe Canyon Field — the second largest North American helium discovery in over 70 years — which sits next-door to GGE’s project.

📰 Read the full breakdown: GGE starts well permitting, appoints experienced driller as helium supply tightens

🗣️ Quick takes on key portfolio company events this week:

Kuniko (ASX: KNI)

On Monday, KNI announced its detailed exploration program for the entire 2022 calendar year.

With our portfolio companies, we like to see a detailed mapping out of the year ahead and the company focused on executing its plan, rather than jumping from one project to another in a more reactionary manner.

KNI management has put together a very detailed program that involves at least some level of exploration work across most of its project portfolio.

This is in line with our 2022 investment memo. Our objective #1 and objective #2 were for KNI to identify its highest priority projects and to then determine the highest priority drilling targets at these projects, ahead of drilling in 2022.

With exposure to some of the most critical battery metals (copper, nickel, cobalt and lithium), 2022 is shaping up nicely for KNI.

Next: We want to see KNI drill the high-priority EM targets at its cobalt project.

Evolution Energy Minerals (ASX: EV1) - Wise-owl portfolio

On Monday, EV1 announced that Phil Hoskins has been appointed Managing Director. This comes as part of a management restructure that saw Trevor Benson move from executive chair to non-executive chair.

We believe Phil’s appointment strengthens EV1’s management significantly, especially considering his involvement in the first drill-holes ever completed at the project back in 2014. Phil also brings significant in-country experience having worked in Tanzania for over 10 years.

While there was no specific mention of anything management-related in our 2022 investment memo for EV1, Phil’s addition to the team adds to each of the three objectives we set and was a welcome surprise.

He brings to EV1 an intimate understanding of the project, in-country experience, extensive knowledge of the graphite market, and well-established relationships with end-users of graphite material. We believe Phil will bring a lot to EV1 as the company works towards a final construction decision and project funding.

Invictus Energy (ASX: IVZ)

On Monday, IVZ announced it has received the 2D seismic data sets from the 2021 seismic acquisition program. It has also received the re-processed US$30m legacy data-set leftover by Mobil.

Data from the 2021 seismic acquisition program and Mobil dataset have highlighted several seismic anomalies of interest. These are encouraging early results, with the final fully processed data-sets not expected until early February.

As mentioned in our 2022 investment memo, we want to see the final interpretation of the 2D seismic program shot in 2021 so that IVZ can identify the highest priority drill targets and increase the probability of making a gas discovery.

With fully interpreted results due in early-February we want to see IVZ finalise the location of the maiden drill hole.

On Tuesday, IVZ also announced the hugely oversubscribed SPP raising $4m @12C with 1:2 free 14c options. IVZ has now raised a total of $8m (split $4m via a placement + $4m via the SPP).

With heaps of cash in the bank, IVZ is in a strong position going into the expected drilling program in May.

Next: We want to see detailed results and final interpretations from the 2D seismic data acquired before we turn our full attention to the drilling program scheduled for May.

Whitehawk (ASX: WHK)

WHK released their 4C on Thursday, reporting US$657K (A$933K) of receipts from customers during the quarter.

For the 2021 year ending December 31, WHK invoiced US$3.4M (A$4.8M), up from $1.9M in 2020.

While the company’s burnt through US$517k in cash during the quarter, which was not well received by the market — it still has US$1.35M in cash and no debt. A large chunk of that operating cash burn was spent on product manufacturing and operating costs, but to put that in context,WHK has US$928K in receivables due next quarter.

Progress has been slower than we’d like to see, yet WHK does continue to progress its large sticky deals with US federal government departments and major institutions. That said, as long-term WHK shareholders we continue to hold and recently bought more on market.

Increasing revenues is a staple implicit objective for WHK that is built into all of the objectives we have set in our 2022 investment memo (which we will publish shortly) and the quarterly shows us that the company is making some genuine progress relative to what we want to see them achieve in 2022.

Euro Manganese (ASX: EMN)

On Tuesday, EMN announced that it will settle the outstanding US$3.6m owed to extinguish the 1.2% net smelter royalty (NSR) that exists over its manganese project. The final amount to be split US$1.8m cash / US$1.8m in EMN shares.

The settlement of the final balance follows a May 2021 agreement with the project vendor for EMN to buy-out the NSR for US$4.5m. The first installment of US$900k was paid then, with the remaining balance payable by 31 January 2022.

With the recent CAD$8.5m investment from the European Bank for Reconstruction and Development (EBRD), EMN has plenty of cash on hand to make the US$1.8m payment. The issuance of the US$1.8m in shares is still subject to approvals and will be listed on the TSX once completed with a four month and one day escrow period after being issued.

The buy-out of the NSR will mean the project economics at the DFS level should be improved.

The completion of the DFS is a core component of our 2022 investment memo for EMN.

Next: We want to see EMN complete the construction of the demonstration plant and announce the updated DFS.

Vulcan Energy Resources (ASX: VUL)

On Monday, VUL announced the granting of a research permit in northern Italy prospective for geothermal lithium brine.

The permit, which extends over ~11.5km^2, includes an area where a historical geothermal well yielded two hot brine samples containing average grades of 350-380mg/L lithium.

We consider this move by VUL to be an attempt to get in early and peg sites that it thinks could have similar potential to that of its German project. This Italian project may come into play in 5-10 years’ time, but for now we consider it non-core to VUL’s portfolio. At the same time, we like that VUL is thinking ahead, and if they can replicate their German success in different jurisdictions - we think that would make VUL a titan of the battery metals space.

The granting of the permit sits outside of our 2022 investment memo for VUL. We are more focussed on the flagship project in Germany progressing to a DFS and the construction of a demonstration plant.

Next: We want to see VUL’s demonstration plant operating, the DFS complete, and VUL’s listing on the main Frankfurt stock exchange.

Thomson Resources (ASX: TMZ)

On Monday, TMZ updated the market on the progress of its resource estimation program at the Mt Gunyan Silver-Gold deposit.

The bulk of the works being completed involves new 3D geological modeling and the re-logging of over 20,000m of historical drilling results. This comes in addition to the ongoing metallurgical test work being done.

The primary objective outlined in our 2022 investment memo (which we will publish shortly) is for TMZ to deliver the milestone 100Moz silver equivalent resource estimate across all of the deposits that contribute to its “Hub and Spoke” business strategy.

The update gives us an idea of how far along this process TMZ is, with JORC compliant resource estimates expected by the end of Q1-2022 for all three of the Texas Projects deposits.

Next: We want to see the JORC resources delivered and an updated “global” resource announced that validates the hub and spoke strategy that TMZ is working towards.

Los Cerros (ASX: LCL)

While there were no exploration updates from LCL this week, it did report that leading institutional investor Franklin Resources has increased its holdings in LCL.

On Thursday, LCL advised that Franklin Resources had become a substantial holder, after two purchases last week totalling ~$120k at an average price of ~12.5c, giving them 5.05% ownership in LCL.

We view this as a significant endorsement of the company and its management. As LCL proves out its projects and gradually increases its resource base it wouldn’t be surprising if more of this type of institutional investors invest in LCL.

Gold is still waiting to make a big move higher - something which would improve the economics of LCL’s project.

Galileo Mining (ASX: GAL)

On Monday, GAL announced that it has commenced EM surveying at its Norseman project, following up on the unexpected massive sulphide intercept GAL made whilst completing its air-core drilling program last year.

After clipping the massive sulphide ~60 metres downhole, the air-core rig wasn't able to drill any further so GAL prioritised the assay from this intercept. The assay returned 1m grading 0.24% nickel, 0.35% copper, 0.04% cobalt, and 0.25 g/t palladium.

The assay, as yet, isn’t indicative of any major discovery but the EM surveys will provide enough information for GAL to go back in with a heavier rig and properly test the massive-sulphide structure.

In our 2022 investment memo (coming soon), we want to see more drilling at the Nickel-PGE focussed Norseman project. This EM survey should be the precursor for a heavier rig being brought on-site and discovery potential targets being drilled.

Next: We want to see the assay results from the diamond drilling program at the Delta-Blues prospect in the Fraser Range, plus assays from the 10,000m air-core drilling program across the Norseman project.

Mandrake Resources (ASX: MAN) - Catalyst Hunter portfolio

On Monday, MAN announced that Roger Fitzhardinge had been appointed as a new independent non-executive director of the company.

Mr Fitzhardinge, who is a geologist with over 23 years of experience, is the general manager for exploration and growth at Centaurus Metals. He was instrumental in identifying, acquiring, and developing Centaurus’ flagship Jaguar Nickel Sulphide Project which took the company's market cap from $24M at the time of acquisition in August 2019 to its current >$500M valuation .

In our 2022 investment memo (coming soon), we highlighted that we want to see MAN make the most of its huge amount of cash and (selectively) look at new project acquisition opportunities.

The appointment of Roger to the board, with his experience in identifying, acquiring, and developing projects, is a massive addition and increases the likelihood of our objectives being met.

Next: We want to see MAN drill the third EM conductor at its nickel project next door to Chalice’s Julimar project and for MAN to acquire a new project.

FYI Resources (ASX: FYI) Wise-owl portfolio

On Tuesday, our high purity alumina investment FYI announced it had completed week three of pilot plant operations.

The pilot plant operations are being run together with FYI’s US listed partner Alcoa (capped at over $10bn) with the ultimate aim of commercialising FYI’s innovative process for refining high quality HPA.

While the grades from the trial run are not yet available, FYI said, “The week-long pilot plant trial performed exceedingly well and within the expected operational parameters including the HPA production being in-line with target outcomes”.

We expect the results to mirror the results from the first and second runs of pilot production, which averaged 99.9974% alumina and 99.9978% alumina, respectively.

Creso Pharma (ASX:CPH)

On Tuesday, CPH announced that its wholly owned subsidiary “Halucenex Life Sciences” had lodged clinical trial authorisation (CTA) for phase II clinical trials with the Canadian health authorities.

The phase II clinical trial is being designed to test the efficacy of psilocybin on treatment resistant Post Traumatic Stress Disorder (PTSD). The trial will be a single-arm, open-lab trial administered to 18-20 adults that suffer from treatment-resistant PTSD.

The clinical trial authorisation (CTA) will be subject to a 30-day review and approval by Health Canada. CPH are concurrently working on ethics approvals and are aiming to start patient recruitment as soon as the health authorities in Canada have approved the trial.

The next major milestone will be the Health authorities approving the trial, with CPH expecting the trial to commence in Q2 CY2022.

GTI Resources (ASX: GTR)

On Thursday, GTR announced that they would re-commence drilling operations at their Wyoming ISR Uranium project.

The drilling program is scheduled to re-mobilise in the week beginning 31 January, drilling the remaining ~60-holes from the total ~100-hole drilling program. Results to date confirm a uranium mineralised system at the project, while the remainder of the drilling will work to confirm and extend this system.

With results so far exceeding expectations, we hope to see a continuation of a high average GT (Grade X Thickness) from the remaining drill-holes.

The first of our objectives for our 2022 investment memo for GTR was to see them drill the Wyoming ISR uranium project with the aim of putting together a maiden resource estimate. We are hoping the next 60-holes will enable this.

Titan Minerals (ASX: TTM)

On Thursday, TTM announced it has appointed experienced geologist Mr Pablo Morelli as its exploration manager.

Pablo has over 15 years experience working across copper and gold projects. Most of this experience was gained working for majors like Barrick, Newmont, Kinross and Rio Tinto in northern and central Chile and in Mexico.

His most recent experience was as the superintendent at the Norte Abierto Project, a joint venture between Newmont and Barrick Gold that has a resource of 26.6M oz of gold and 6.7B lbs of copper.

All three of our 2022 investment memo objectives (our memo will be published soon) are linked to exploration activities so bringing someone onto the team with the experience of Pablo we think is a positive boost in the company's ability to make progress with our objectives.

After the announcement experienced institutional resources investors Tribeca Investment Partners put out a substantial shareholder notice for TTM.

Tribeca looks to have purchased ~$250k in shares on-market at an average price of 10c between the 24-25 January, and now own 5.14% of the company.

Aldoro Resources (ASX: ARN) Catalyst Hunter portfolio

ARN this week completed phase 1 of the drilling program at its rubidium project, with the first 17-holes done and 47 to go.

The drilling program has so far confirmed and extended historic drilling results as ARN keeps intersecting thick pegmatite bodies. These pegmatite intersections have been as thick and even thicker than was initially expected.

The drilling program is targeting lithium and rubidium mineralisation, and with the pegmatite intercepts seen to date we think there the assays could reveal mineralisation from which ARN can use to establish a resource.

One of two objectives in our 2022 investment memo was to see ARN get some drilling done targeting lithium/rubidium so we will be eagerly watching to see the results from this program. Pending the results from the drilling program we will likely make updates to our investment memo.

Latin Resources (ASX: LRS) Catalyst Hunter portfolio

On Monday, LRS announced that it had received drilling permits for its lithium project in Brazil, where it anticipates drilling will begin in early February.

The company's lithium project is located in the Bananal Valley district of eastern Brazil where the CAD$1.3 billion capped TSX-listed Sigma Lithium Corporation’s key projects sit.

LRS is planning a 14-hole diamond drilling program to test outcropping lithium-bearing pegmatites that were previously identified during mapping/geochemical sampling programs. Emphasis will be on two priority areas where rock-chip samples returned grades of 2.71% and 1.45% lithium over a 1.2km strike length.

With lithium prices making new all-time highs almost on a daily basis it makes sense to go exploring for lithium.

Our 2022 investment memo (coming soon) is mostly focused on LRS progressing its halloysite project but the last of the objectives we set for LRS to achieve in 2022 does include testing the lithium potential of these Brazilian tenements.

Drilling success at the lithium project is not a make or break for us, but the market could become really interested if LRS does find something substantial.

As for the halloysite project - LRS released assays from a 13-drill holes from cross-sectional drilling at its WA Halloysite project on Thursday.

The drilling work is mostly being done in and around the area of the known ~207mt JORC resource. The results from this round of drilling reinforces our understanding of the scale of the deposit and could lead to a resource upgrade for LRS.

The peak results from the drilling program were:

- 6m @ 24% halloysite from 7m

- 13m @ 18% halloysite from 21m

- 16m @ 27% halloysite from 14m

- 6m @ 26% halloysite from 14m

- 18m @ 26% halloysite from 7m

LRS also announced that it has appointed a specialist drilling contractor to complete geotechnical and metallurgical drilling. This is expected to commence in February.

The upcoming drilling program along with results from the last round of drilling will form the basis for a resource upgrade from LRS, which we are looking forward to seeing.

The Food Revolution Group (ASX: FOD) Wise-owl portfolio

As announced on Monday, FOD has finished developing its 100% plant-based protein smoothie range which it expects to be stocked in Coles in late February ahead of wider distribution from June 2022.

We haven't had a drink of the new product as yet but it looks like the right product to get out to market right now. With consumers becoming increasingly health-conscious and plant-based alternatives for protein being hard to find, we believe the product is targeting an area of the market that has structural demand tailwinds.

In our investment memo, the 3rd objective we set for FOD to achieve in 2022 is for it to announce “new products and innovations", these types of products are exactly what we are looking for. We expect products like these to open up FOD’s exposure to new markets and could increase revenues together with its established Juice business.

Auroch Minerals (ASX: AOU) Wise-owl portfolio

On Tuesday, AOU announced that it has commenced a 3,000m infill drilling program at its Nickel project in WA. The ultimate aim of the drilling program is to update/upgrade the current JORC resource of 1.02Mt grading 2.0% nickel for 21,400kt of contained nickel.

Alongside the 3,000m of infill drilling, AOU will drill an additional 2,000m to test for extensions to the existing mineralisation at greater depths.

The drilling program is expected to take around six weeks to complete and the results will be used in an updated scoping study that is due by the end of March.

Advanced Human Imaging (ASX: AHI)

On Thursday, AHI announced that they had signed a binding term Sheet with Activate Health in Estonia.

While Estonia is one of the more digitally advanced countries in Europe and the move makes sense, we’re more interested in seeing more revenues start to come through in their upcoming 4C.

We also note that a North American investor or group of investors sold down 1.46% of their shares yesterday, after having increased their substantial holding in the weeks before.

As the global tech sell-off gathers pace, revenues and a lower operating cash burn may help put a floor under the AHI share price, which bounced back strongly on Friday afternoon after a sharp drop in the morning.

🌎 Mainstream Media:

Jeremy Grantham Has an Even Scarier Prediction Than His Crash Call

China’s Vast Blueprint for Tech Supremacy Over U.S.

Serbia revokes Rio Tinto lithium project licences amid protests

Rio Tinto strikes Mongolia settlement

India Plans $19 Billion Fertilizer Subsidy to Placate Angry Farmers

Have a great weekend,

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.