ASX rests pre-Christmas as the market trades on very low volumes

Published 11-DEC-2021 11:18 A.M.

|

14 minute read

It’s been an eerie start to December on the ASX.

At times we were feeling like we were the only ones still sitting in front of our desks watching the markets. The ASX has been trading on low volumes over the past few weeks, and no matter what announcement a company released, the response seemed muted.

Everyone has their own theories to try and explain why the markets are behaving the way they are.

Our team has been bouncing around ideas from “everyone is on holidays” and “people cashing up for Christmas”, all the way to high level theories based on portfolio rebalancing year-end, P&Ls being reset for institutional investors and funds locking in gains from an almost 19 month bull market.

Or maybe this is actually what a normal market looks like... and it's just strange because we have become accustomed to the wild bull market that came after the COVID fuelled lows of March 2020.

All valid theories we think, but as with almost everything there is probably some data set that provides context on all of this.

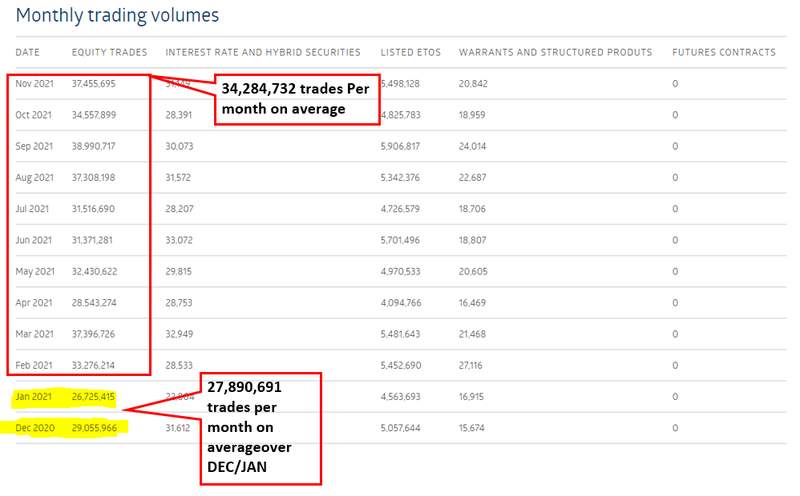

Naturally, this led us to the ASX’s trading volume reports which are published monthly.

Looking around the same period 12 months ago, the Dec-Jan period showed an average trading volume of ~27.9M trades/month, whereas the average trading volume between Feb-Nov 2021 was ~34.3M trades/month.

This is a 20% drop off during the holiday period.

Clearly there is seasonality with trading volumes, and it is no surprise that people are tired by the end of the year and would rather spend it with family and friends instead of being stuck behind a screen trading the markets.

Why does all of this matter?

The data shows that trading volumes are down across the ASX by ~20% between Dec-Jan and we suspect that the volume changes in the more volatile micro cap market are much larger than this.

Lower volumes for blue chip stocks like Commonwealth Bank or BHP don't mean much.

Blue chip companies have endless equity research coverage with buy/sell recommendations and price targets, whilst index and algorithmic fund traders support volumes in these stocks.

At the large-cap end of the market, moves of 2-3% are seen as big.

The micro cap space, on the other hand, has almost no mainstream coverage. This can make it more susceptible to market sentiment and external market forces.

These markets are inherently high risk/high reward and are naturally more volatile.

Small cap markets are dominated by private investors who tend to do their own research and react to news the way they interpret and understand it.

So when an individual with a large position needs to sell-down to fund a family Christmas holiday after two years of COVID lockdown, it can significantly move the share price on low volumes.

This is why being aware of low volume moves is important. A brutal move to either direction is fairly common in the micro-cap space, with 15% moves either way all part of investing in the space.

A low volume sell-off of 15% in a company’s share price can give the illusion that a company is being punished for bad news. However, often the reality is that a $50M market cap company suffered a 15% share price fall from just $25k in trading volumes.

If a small amount of shares are traded because someone needs to pay for a wedding or a new car it can lead to a large change in the value of a company - all because there just isn't enough eyeballs on the buy side at that particular time.

Generally you will see the share price quickly recover the next day as the markets work the same conditions in the opposite direction. In the grand scheme of things, these moves are insignificant and more a result of buyers shutting up shop for the holidays.

For the astute investor looking to build a position, these times can present good entry points - especially for undervalued stocks suddenly made cheaper due to a sell-down on low volumes.

Just like the markets, we are taking this relatively quiet period as a chance to catch our breath and evaluate our investment strategies going into 2022.

With that in mind, we have been preparing investment memos for each of our portfolio companies, reminding ourselves of why we invested, and laying out a clear set of key objectives we want to see them achieve next year.

More investment memos out this week:

Lately we have been writing investment memos for each stock we have invested in.

Each memo summarises why we invested in a stock and it gives us a framework to track a company’s performance against our initial investment thesis.

It is a very quick investment snapshot that is easily explainable to a friend or family member over a few drinks.

This comes just in time for the holidays, so we can all avoid putting our family members to sleep over Christmas dinner with a 3 hour pitch on why our favourite investment is drilling a certain rock structure in the middle of WA.

Last weekend we released the first batch of our investment memos.

We always encourage investors to be responsible for their own investment decisions. A big part of this is doing your own due diligence - especially by writing down and recording the reasons for making an investment at the time. Save it and revisit the memo down the track, to see if things turned out the way you hoped it would.

Here are a few more investment memos from our portfolio companies that we produced this week:

Alexium International Group (ASX: AJX)

Grand Gulf Energy (ASX:GGE) - Catalyst Hunter

Please reply to this email if you have any comments, suggestions or feedback on anything else you would like to see included.

📰 This week on Next Investors

To start off the week, Kuniko Ltd (ASX:KNI) announced some early stage exploration results from its Norwegian Cobalt projects.

The two key take-aways from the announcement were:

- Updated geophysical interpretations of the primary EM target at its cobalt project showed that previous drilling done by the former owner (Berkut Minerals) may have missed the target conductor.

- The geochemical soil sampling confirmed the presence of cobalt mineralisation over that particular anomaly of interest.

With geochem and geophysics both pointing to a particular area of interest, KNI’s cobalt project is now set up as a key exploration target going into 2022.

📰 Read more: KNI Geophysics Unveils EM Conductor Under Historic Cobalt Mine

On Wednesday, Alexium International Group (ASX:AJX) announced the first commercialisation of its cooling technology product in the “body armour” segment, partnering with US-based manufacturer, Premier Body Armor.

The news is a big milestone for AJX because it validates the expansion strategy into new markets.

This deal is another step towards AJX’s overall strategy of becoming cash-flow positive in 2022.

📰 Read more: AJX Announces First Body Armour Contract - Breaks into New Market

On Thursday, our 2020 Energy Pick of the Year Invictus Energy (ASX:IVZ) signed a non-binding, farm-in option agreement with Cluff Energy Africa.

This agreement goes some way to de-risking the funding of IVZ’s maiden drilling program at the largest conventional oil and gas prospect in Africa.

Cluff Energy Africa are backed by UK based resources entrepreneur and oil tycoon Algy Cluff OBE and British billionaire Lord Michael Spencer. The two are deep pocketed oil and gas financiers and have significant in-country experience in Zimbabwe.

Importantly, this is a non-binding agreement which gives IVZ optionality should a better offer to farm-in or acquire a piece of the project comes along.

After we published our note, on Friday IVZ announced it has secured a drill rig for its well. The rig is contracted for one firm well and one contingent well, with drilling anticipated to commence in May 2022.

📰 Read more: IVZ Commits to Farm in Deal with British Tycoons - But Maintains an Open Relationship

🗣️ Quick takes on key portfolio company events this week:

Vulcan Energy Resources (ASX:VUL)

On Wednesday after market, VUL signed a binding lithium offtake agreement with the Volkswagen Group, the world's largest automaker by revenue and the largest company in Germany.

The agreement is for an initial five-year term anticipated to start in 2026. The agreement dictates that the Volkswagen Group is to purchase a minimum of 34,000 tonnes and a maximum of 42,000 tonnes of battery grade lithium hydroxide over the duration of the agreement. Pricing will be based on market prices on a take-or-pay basis.

VUL also announced that the Volkswagen Group has agreed to a first right of refusal to invest in additional capacity at VUL’s Zero Carbon Lithium Project.

VUL followed that up with Friday’s acquisition of an operational geothermal power plant in Germany. The plant currently has the technical ability to produce a maximum of 4.8MW renewable power, equivalent to approximately 8,000 households.

VUL anticipates that the plant will be a source of revenue for the company, having reported sales of €5.8M and an EBITDA of €2.9M for the FY ending 31st Dec 2020.

The plant is being paid for in cash for €31.5M, with VUL using the proceeds from its recent A$200M capital raise to cover the cost.

This is a big first step in VUL becoming a revenue generating renewable energy producer.

In addition to this acquisition, VUL has executed a 20 year brine offtake agreement with the operational Landau geothermal renewable energy plant in the Upper Rhine Valley.

The Landau plant will provide access to accommodate VUL’s demonstration lithium extraction plant, with a target start up date of Q2 2022.

The impact of these deals will inform VUL’s Definitive Feasibility Study.

Next: We want to see VUL’s demonstration plant operating, the DFS complete, and a Vulcan listing on the main German bourse.

Minbos Resources (ASX:MNB)

Yesterday MNB went into a trading halt pending a capital raise.

MNB had $4.2M in cash at the end of the September quarter; any extra funding will go a long way to help MNB hit its company objectives in 2022.

Next: We want to see some more news with respect to the zero carbon ammonia project as well as progress and development on the phosphate production plant.

Elixir Energy (ASX:EXR)

On Thursday, EXR provided its final operations update for the year with respect to its coal bed methane exploration and appraisal program at its 100% owned Nomgon Project in Mongolia.

This was a big year for EXR, exceeding its own expectations, drilling 17 wells from 13 planned at the start of the year. 76% of the wells intersected coal, a successful outcome and valuable data as EXR moves into the second phase of its project - production testing.

EXR confirmed that its plans for a long-term pilot production testing program in 2022 have been lodged with the Mongolian petroleum regulator.

The ultimate aim of the pilot program is to form a basis for its planned modular gas fired energy generation project. The results from the pilot production program will also feed into the ongoing feasibility study works running concurrently to the testing.

EXR also announced the completion of its 2D seismic acquisition program and has started interpretation to generate drill-targets for the 2022 drilling campaigns, all while it completes the final two wells from its 2021 program.

Next: For EXR it is all about production testing as drilling takes a back seat. We will monitor the project over the next 12 months and provide updates and commentary as it progresses.

GTi Resources (ASX:GTR)

Early in the week, GTR released the first batch of drilling results from its Wyoming ISR uranium project. The results came from the first 10 holes from a total drilling program that spans ~100 holes.

In our last note on GTR leading up to drilling, we had set some expectations for GTR based around the already operational Lost-Creek ISR project which neighbours GTR’s grounds.

The results so far are exceeding our expectations significantly:

- Grade greater than 0.02% Uranium: Result so far - Peak grade of 0.044%.

- Grade X Thickness greater than 0.2: Result so far - Average GT of 0.99 GT.

Importantly, a typical ISR deposit is considered economically viable if grades are above 0.02% uranium + “GT” is above 0.2.

So far, GTR is producing economic grade results that could lead to a maiden resource for the project.

Next: We expect drilling results to be progressively released to the market all the way up to the New Year given that this type of ISR focussed drilling doesn't need to be assayed. We want to see drilling continuously return “grade x thickness results above the 0.2 cut-off”.

Titan Minerals (ASX:TTM)

TTM closed off the week by announcing it had moved one of its diamond drill rigs across to its Copper Duke porphyry target in Ecuador.

The drill-rig will be testing two diamond holes drilled in 1978 by the United Nations (U.N.) that were aimed at discovering molybdenum but intersected gold instead.

The drilling program is part of the existing geophysical and geochemical works ongoing at the project and will form part of the current target generation works being completed.

Because these holes are being drilled ‘blind’, without any modern exploration techniques applied, we are not expecting a large copper strike to eventuate.

This program is in place to help generate high-priority drill targets that can be followed up in the future.

Next: With in-fill drilling ongoing at the Dynasty gold project we expect TTM to start releasing more assay results leading up to what we hope will be the all important JORC resource update.

88 Energy (ASX:88E)

On Monday 88E announced an operations update with respect to the much-anticipated Merlin-2 well. Of particular interest to us was the following points from the announcement:

- One of 88E’s key contractors was willing to accept payment in shares totalling ~US$7.5m. Oil & Gas exploration contractors don't generally opt-in to being paid in shares. In our opinion, this is a positive sign going into drilling in 2022.

- Permitting for the Merlin-2 well is well advanced and expected to be received around year-end leading up to an expected spud date of February 2022.

88E’s big drilling event that we look forward to every year is now only ~2.5 months away.

Next: We want the drill permit granted for the Merlin-2 well and all of the drilling preparation works completed. We are looking forward to drilling commencing in February 2022.

In our other portfolios

🏹 Catalyst Hunter

This week our 2021 Catalyst Hunter Pick of the Year Grand Gulf Energy (ASX:GGE) announced its maiden helium resource - a gross 7.4BCF (Billion Cubic Feet) (P50) prospective resource.

Assuming the 75% earn-in agreement is completed, GGE will have a 5.6BCF net prospective Helium resource under the current leases.

GGE also confirmed that drilling permitting is well advanced and is expected in Q1-2022 with drilling only around three months away.

With GGE currently trading at almost half the market cap of its nearest ASX listed peer, we expect the upcoming drilling program to be the catalyst that leads to a rerating of the share price.

📰 Read the full breakdown: First Look at GGE Helium Resource. How does it stack up?

🌎 Mainstream Media:

Battery Metals (VUL)

Lithium extraction company Vulcan adds VW to customer line-up (Reuters)

Volkswagen closes three new partnerships to amp up EV production (TechCrunch)

African Energy (IVZ)

Powerless: Zimbabweans hit with another electricity price rise (Aljazeera.com)

Global energy targets don't deal with people's real problems in Zimbabwe (The Conversation)

Helium (GGE)

First Helium (Investing News Network)

Hydrogen (PRL)

Elizabeth Gaines steps down as Fortescue Metals Group CEO (AFR)

Commodities

Mining exploration spending soars by a record $2.5 billion (AFR)

Have a great weekend,

Next Investors

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.