First Look at GGE Helium Resource. How does it stack up?

Disclosure: The authors of this article and owners of Catalyst Hunter, S3 Consortium Pty Ltd, and associated entities, own 49,940,826 GGE shares. S3 Consortium Pty Ltd has been engaged by GGE to share our commentary and opinion on the progress of our investment in GGE over time.

In October we announced our Pick of the Year Grand Gulf Energy (ASX:GGE) - Catalyst Hunter’s biggest ever investment.

The reason for our investment was GGE’s recent acquisition of a US helium project in the heart of the world’s most prolific helium producing region.

Today GGE confirmed a large prospective helium resource at that project and stated that maiden drilling is on track for late next quarter.

We like that GGE is drilling in just a few months time - drilling events generally draw the attention of the wider market and see rapid share price appreciation in the lead up.

In November, we discussed how GGE had expanded their acreage by 16% to a total lease holding of 27,303 acres — an important step ahead of the estimation of the maiden prospective helium resource. Naturally, a larger acreage would lead to a larger resource.

Today GGE confirmed a 7.4 billion cubic feet BCF (P50) prospective resource over the gross lease holdings of the project.

GGE is earning a 75% interest in the project via an earn-in agreement with Valence, a joint venture holding company.

So from the 7.4BCF prospective resource, 5.6BCF will be net to GGE - assuming full earn in.

We did some quick back of the envelope calculations for the prospective resource and what it could mean for the “in ground” value for GGE.

At 5.6BCF and applying a helium price of ~$600/Mcf, we calculate $3.36BN net in the ground helium for GGE.

Of course this is only a prospective resource we are talking about - there is less confidence in this number as the project is in its early stage and hasn't been drill tested yet.

We would expect the resource size to reduce as exploration drilling continues and some of the ‘estimates’ convert into contingent resources and reserves. Plus exploration and development costs have not been considered.

In any case, a “multi-billion dollar in ground value” is a nice place to start heading into the drilling of the first well.

The prospective resource gives GGE a target to chase and is the first step towards being able to commercialise its helium project.

With a prospective resource secured, the next step is for GGE to get a drill rig on-site and really test the project's potential.

Today’s announcement also confirmed that GGE was well advanced with drilling permitting and is expecting to drill the first well in late Q1 2022 - roughly three months from now.

With existing infrastructure in place, and assuming the drilling programs are a success, GGE could skip the proving up stage of the resource definition phase and quickly put it’s project into production.

With GGE currently trading at almost half the market cap of its nearest ASX listed peer, we expect the upcoming drilling program to be the catalyst that leads to a re-rating of the share price.

More on GGE’s prospective resource announced today:

When announcing GGE as our 2020 Pick of The Year we said we wanted to see a maiden prospective resource announced before Christmas.

🔲 Resource on Current Leases [before Christmas]

With the maiden resource now delivered, GGE will have a few extra weeks by the year’s end to focus its efforts on moving closer to a drilling program.

Just like any other gas exploration project, a “prospective resource” is the first step toward making a discovery. Think of it as an estimate of what the company thinks could be in the ground.

Generally with gas exploration projects a company would need to drill the prospects and upgrade the resource from prospective to contingent and then from contingent to a final reserve figure.

The “contingent” stage of the delineation process refers to the amount of resource that is known to be recoverable but which aren’t considered commercially recoverable. The commercially recoverable part is generally with reference to a lack of infrastructure or difficulties related to access.

So it would be easy to think GGE has a lot of work to do before it can commercialise this “prospective resource” but it’s important to remember where GGE’s projects are.

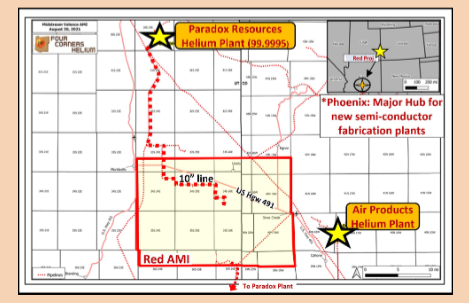

GGE’s helium project is located in a specific part of the US dubbed “the Saudi Arabia of Helium” due to the number of large producing helium companies and helium production plants here.

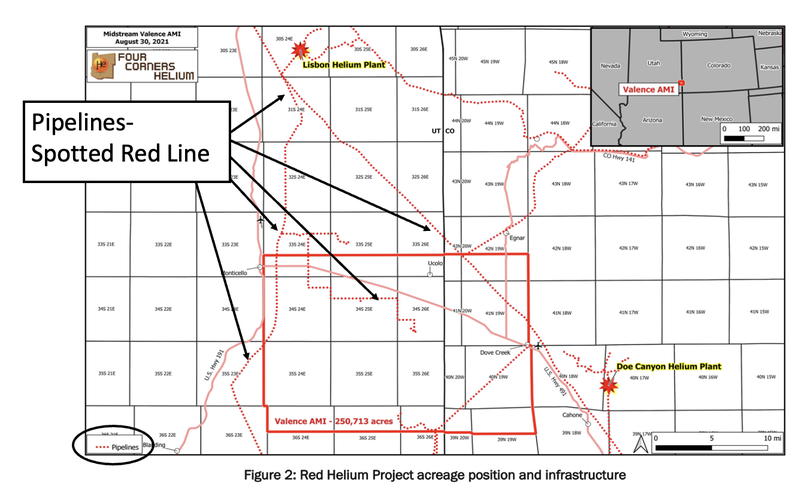

Here, there are over seven large-scale already producing helium fields and two helium processing plants, as well as existing pipeline infrastructure.

In fact a pipeline runs through GGE’s “Area of Mutual Interest”, directly to the Paradox Resources owned helium plant.

With this in mind, we are confident that GGE is in the right place to be able to quickly put into production any successful discovery.

Should GGE’s drilling program confirm a helium reservoir with commercial flow rates, it could quickly tie the well in via a pipeline agreement and start selling into local markets.

This is completely different to a mining project. There is no open-pit mine that needs to be stripped back, there is no shipping port that needs to be built, GGE just has to get drilling done, confirm commercially flow-rates of helium & then negotiate a pipeline agreement.

All of this could lead to GGE skipping the “proving up” stage of the resource and just go from drilling straight into production.

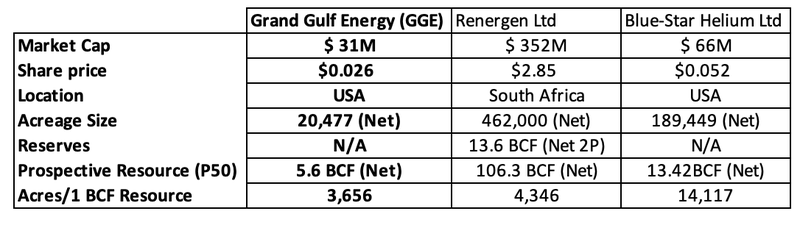

GGE has the lowest market cap of its ASX helium peers:

At present there are only 3 pure play helium stocks on the ASX.

The first of these is Blue Star Helium - currently capped at $79.5M and is looking for helium in Colorado, USA. In this state, a lot of the leases sit on Federal land.

GGE has leases on freehold land - this is preferred over Federal land

In our last note we touched on the importance of GGE’s leases in Utah sitting on freehold land as opposed to Federal land because of the complex business agreement overlays that are associated with Federal land.

With leases on freehold land, GGE has much less bureaucratic red tape to overcome compared to a company like Blue Star, whose leases are on Federal Land.

GGE can secure permitting for exploration, pipelines and future developments quicker and on much simpler terms.

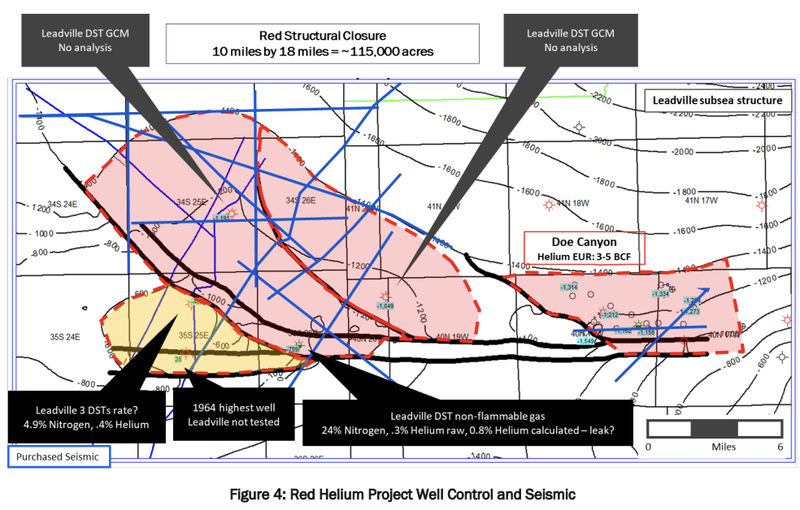

GGE already has seismic data

GGE also has 190km of 2D Seismic already acquired and re-processed. So far the data points to a lot of similarities between the Doe Canyon Helium Field (8 miles to the west of GGE’s assets) which is producing 18mmcf/day of raw gas with average helium grades of ~0.5%.

Blue Star, meanwhile, has no 2D seismic data.

Previous drilling: GGE’s historic wells demonstrated the presence of helium

Historic oil and gas wells drilled in the 1950-60s on GGE’s project showed up to 0.4% helium, but no further testing was done since the drillers were primarily looking for oil.

Again, we think this is another advantage GGE has over Blue Star.

Helium resource concentration per acre leased

GGE also has the highest concentration of resource with 1BCF prospective resource for every 3,656 Acres leased.

This compares favourably with Blue Star who have 1BCF prospective resource for every 14,116 Acres leased.

GGE exploring in well established helium region

The second and much further advanced helium stock is Renergen Ltd, which holds one of the only onshore petroleum production rights in South Africa.

Renergen Ltd is essentially building an industry from the ground up - the latest company presentation indicates a US$800m CAPEX figure to get their helium project off the ground.

The key advantage GGE has over Renergen comes from the fact that GGE’s assets sit in the “Saudi Arabia of helium” in the US - a major advantage over Renergen’s African location. .

Given all of the existing infrastructure in the region, GGE won't have to commit hundreds of millions of dollars to develop infrastructure, providing its project with a fast pathway to production.

Let's summarise some of the key differences:

- GGE’s project sits on mostly freehold land. Less red tape leads to a quicker pathway to production. Blue Star’s project is on Federal Land.

- GGE has 190km in 2D Seismic & Historic drill results - Seismic data is showing similarities between the Doe Canyon helium field (8-miles to the west of GGE), producing 18mmcf/day of raw gas with average helium grades of ~0.5%. Historic wells drilled in the 1950-60’s also showed 0.4% helium. Blue Star has no Seismic data.

- GGE has a higher helium concentrations per acre

- GGE has access to existing pipelines in a region already actively producing Helium - GGE’s project sits near 2 already producing helium projects and heaps of existing pipeline infrastructure. Renergen is developing the only onshore petroleum production rights in South Africa and needs to spend US$800m on CAPEX to get its helium to market.

Essentially, as GGE increases the size of their lease holdings we expect the prospective resource to increase relatively quickly.

All of these differences considered GGE has the lowest market cap of all three of these pure play ASX helium stocks.

We think that eventually the market will catch onto the differences and re-rate GGE accordingly.

Share price performance of ASX helium stocks:

Blue Star announced its acquisition of its helium assets in the USA in November 2019. It has since gone on a share price run from 0.5c all the way up to where it is now at 5.1c - an impressive 10x return in under 24 months:

GGE made it’s helium acquisition in September this year - only four months ago.

To finance the acquisition, GGE raised $950k @ 1c. Within three months the share price ran to a high of ~5c - an almost 5x return for investors who participated in the capital raise.

Naturally when a big move like this happens in a short-period of time, investors look to lock-in some profits - and that creates some “churn” in the share price.

Considering the current broader sentiment in the market, we think GGE is holding up well above the placement price. We do expect to see some consolidation happen before a sustained move higher.

With a prospective resource now announced and its maiden drilling program only a few months away, we hope GGE’s share price will perform similarly to its peers over the next 18-24 months.

We made some early stage investments in GGE at 1c at the placement, when the market cap was significantly lower than all of its peers. We have since added to our investment at 3c.

Given GGE’s large discount to its peers, we think the market will eventually catch up with the potential at its helium projects.

Typically these large re-rates happen over a longer period of time, similarly to its peers we expect this to happen in the 18-24 months prior to the helium assets being acquired (Sept-2021).

What are the risks?

GGE’s project is still at the prospective stage.

There is a risk that drilling returns no helium and the project is considered stranded. And assuming GGE does make a helium discovery, if the flow rates are too low or the helium recovery rates are not high-enough then the project could be considered uneconomic.

GGE, being an early stage explorer, is also reliant on markets to be willing to finance drilling programs. A change in market conditions could lead to potential financing issues.

What’s next for GGE & what do we want to see?

We recently launched a project we have been working on for a while called “Investment Memos”.

Our idea behind the project was for the milestones and developments of a company to be easily comparable to our initial investment thesis.

You can check out our GGE investment memo here.

Below is a breakdown of the things we want GGE to achieve in the short-medium term:

Objective 1: Execute Big Drilling Event

🔲 Pre-Drilling Work Complete

- 🔲 Identify the highest priority Drill Targets

- 🔲 Drill Rigs to be Secured

- 🔄 Drilling permits to be granted

🔲 First well drilled by the end of Q1-2022

- Our base-case target is for GGE to prove there is a helium system present at the project.

- An exceptional result for us would be if they return >0.4% helium concentration in the raw gas stream at a flow rate of 10mmcfpd of raw gas (we will find out grade and flow rate 2 weeks after the well is complete).

Objective 2: Expand the resource through leasing

✅ Resource on Current Leases [before Christmas]: Today GGE announced the initial gas resource on the current leases. This forms a baseline for resource expansion.

🔄 Additional Leasing: GGE’s leases cover 23,600 acres with an additional 3,703 acres secured on the 18th of November. GGE’s goal is to secure 35,000 acres of leased land.

Objective 3: Commercialise the gas resource

🔲 Offtake Agreement [6 months] - GGE has said an offtake negotiations are underway. In our experience, offtake negotiates can take longer than expected - a good result would be to see this within 12 months.

🔲 Pipeline deal secured [End of 2022] - Again these kinds of deals can take longer than expected, we would be happy for this to occur by the end of 2022, and very impressed if it comes earlier

Disclosure: The authors of this article and owners of Catalyst Hunter, S3 Consortium Pty Ltd, and associated entities, own 49,940,826 GGE shares. S3 Consortium Pty Ltd has been engaged by GGE to share our commentary and opinion on the progress of our investment in GGE over time.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.