Whoever has the gold makes the rules

Published 05-NOV-2022 11:00 A.M.

|

14 minute read

Quarterly reports for our Portfolio companies have all now been released so we know how much money each company has left.

Given the market is pretty rough right now and it’s hard to raise capital, companies are ideally sitting on enough money to ride out the tough market conditions.

In down markets like these, small cap companies with low cash balances are forced to raise cash at deep discounts to already depressed share prices.

Not great if you are an existing shareholder, but lots of attractive opportunities if you have capital to invest.

We have participated in nearly every cap raise in our Portfolio over these last few rough months on the market.

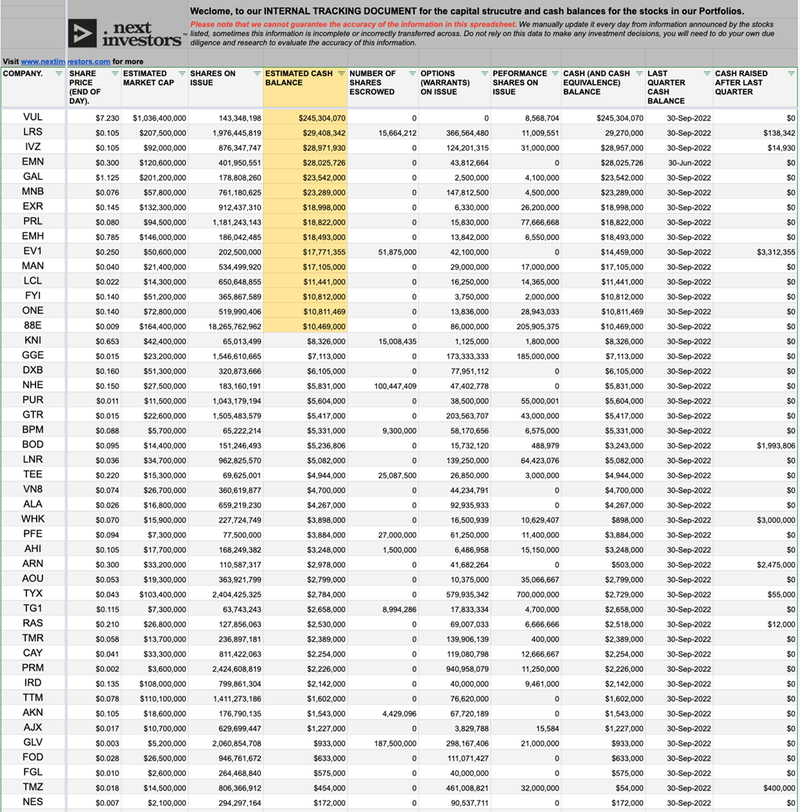

Today we are sharing our updated Cap Structures Spreadsheet that we use to track estimated cash balances for each of our Investments and potential dilution of new any capital raises.

Before we do that though, we want to cover how small cap companies can grow into bigger companies — it all comes down to executing their plan and securing funding from capital markets.

Growth and success doesn't happen overnight, and small caps often need to raise cash many times before they can join the big leagues.

A large portion of small cap companies will never make it.

Access to capital markets, i.e. getting money to be able to execute a business plan, is what makes small caps tick and lets them have a chance at growth.

Understanding capital markets is an important part of being a good small cap investor — and we’ve seen nearly every kind of capital raise under the sun.

Varying discount sizes, different broker options, free attaching options, convertible notes, cap raises above the current share price, and everything in between.

But there is a familiar pattern to capital raises...

Small caps will IPO (or re-list) and raise money to have a crack at a project.

If successful with their first round of cash, these companies can then raise more money at higher valuations to further progress or grow.

If they fail to execute their plan, experience delays, or simply fail to impress the market, the share price will go down and they will be under pressure to raise at a lower share price, diluting existing shareholders in order to keep funding their plan.

Capital markets are tough at the moment. Higher interest rates and poor investor sentiment have dried up much of the funds that would normally be flowing to small caps during a boom market.

That means companies looking to raise cash to progress their projects have to offer shares at significant discounts to the last traded share price, usually with free options as an enticement to attract cash.

Companies that raised a good chunk of money while the market was hot can generally weather the storm and keep progressing their project with minimal shareholder dilution - compared to companies that are forced to raise money in a down market to keep operations going.

(This is why it's important to track the cash balance of each Investment in our portfolio, we share our spreadsheet below)

Companies are either price makers or price takers when raising capital.

- Price makers - companies raise capital in bullish markets where their share price is trading at highs and most investors are itching to invest in small caps = good for existing shareholders.

- Price takers - companies are forced to raise capital in down markets to fund operations, often taking whatever deal is offered to them, likely being highly dilutive to existing holders to entice skittish new investors to part with their precious cash = bad for existing shareholders (unless they participate too).

We want our Investments to be price ‘makers’ and not price ‘takers’.

This brings us back to ‘quarterly reporting season’, where we are now.

A month after the end of each quarter, the ASX requires small cap companies to announce their end of quarter cash balances (so September 30 cash balances were all reported to the ASX by the end of October).

This quarterly review is a good opportunity for us, as Investors, to evaluate:

- Whether the company has been productive with its capital allocation.

- The likelihood of a capital raise in the near future.

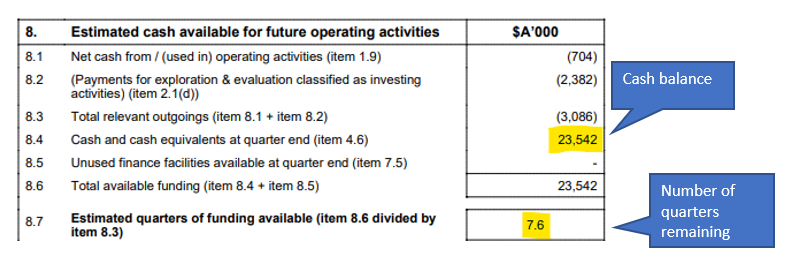

There is a quick shortcut that you can use to find out if a capital raise is imminent — by looking at the “number of quarters of cash remaining” in the quarterly report (also known as the 4C):

This is not an exact measure, as some companies may have a particularly expensive quarter if they are doing major exploration work, for example.

If the company has less than two quarters of capital remaining, it is required to explain to investors what it will do to mitigate the capital risk.

Reading through these statements can give a good insight into whether the company is looking to raise capital OR reduce spending.

We have a spreadsheet that we use internally to track the cash balances and capital structures of each of our Portfolio companies.

You can bookmark this spreadsheet and check back around quarterly reporting season to see the updated cash balances for the companies in our Portfolios.

Click here to access our Cap Structures Spreadsheet

*Please note: that we cannot guarantee the accuracy of the information in this spreadsheet. We manually update it every day from information announced by the stocks listed, sometimes this information is incomplete or incorrectly transferred across. Do not rely on this data to make any investment decisions. You will need to do your own due diligence and research to evaluate the accuracy of this information.*

Today we also highlight a number of our Investments that have plenty of cash, and outline what companies do in a down market when cash dries up (it can either go really well or really poorly).

The 15 most cashed up companies in our Portfolios

1. Vulcan Energy Resources (ASX:VUL) - Cash balance: $245M

Our 2020 Small Cap Pick of the Year is developing Zero Carbon lithium projects in Europe; an all time best-performing Investment that recently expanded into France.

2. Latin Resources (ASX:LRS) - Cash balance: $29M

Timed its cap raise perfectly after a lithium discovery in Brazil. Maiden JORC resource is due by the end of the year; it made a second discovery 500m from the initial one.

3. Invictus Energy (ASX:IVZ) - Cash balance: $29M

Drilling a huge gas prospect in Zimbabwe, funded for two wells after a series of cap raises. Major catalyst due in the coming weeks. We are still holding 4,987,102 shares into the drill result.

4. Euro Manganese (ASX:EMN) - Cash balance: $28M

Developing a high purity manganese project in the heart of Europe for EV batteries. We’re looking for EMN to seal an offtake by the end of the year.

5. Galileo Mining (ASX:GAL) - Cash balance: $23M

Drilling out a major PGE discovery at Norseman in WA, having raised ~$20M following the discovery. Recently got a scent of more nickel sulphides in new mineralised zones.

6. Minbos Resources (ASX:MNB) - Cash balance: $23M

Developing a low cost phosphate project in Angola and has green ammonia optionality. Fertiliser prices remain elevated amid gas and food crises.

7. Elixir Energy (ASX:EXR) - Cash balance: $19M

Developing a gas resource, and a green hydrogen project with SoftBank - both projects in Mongolia. Recently acquired a promising gas project in Queensland.

8. Province Resources (ASX:PRL) - Cash balance: $19M

Developing a large green hydrogen project in WA. Waiting on a signed shareholder agreement after binding key terms were established with Total Eren.

9. European Metals Holdings (ASX:EMH) - Cash balance: $18M

Developing Europe’s largest hard rock lithium resource in the Czech Republic. A Definitive Feasibility Study (DFS) is pending.

10. Mandrake Resources (ASX:MAN) - Cash balance: $17M

Timed its last raise perfectly, but the project it was drilling didn’t work out. Now with its sizeable cash balance, it is looking for a new project.

11. Evolution Energy Resources (ASX:EV1) - Cash balance: $14M

Developing a Tanzanian ESG friendly graphite resource. Released positive announcements on downstream work, and then raised $13M. We want to see the Framework Agreement signed next.

12. Los Cerros (ASX:LCL) - Cash balance: $11M

Big gold resource in Colombia, waiting on further clarity from the government on mining operations and a preliminary economic assessment.

13. FYI Resources (ASX:FYI) - Cash balance: $11M

Developing a High Purity Alumina (HPA) battery project in WA. Has a JV with aluminium giant, Alcoa. We’re waiting for Alcoa to chip in US$50M to fund a demonstration plant, with the decision due next month.

14. Oneview Healthcare (ASX:ONE) - Cash balance: $11M

Health-tech company going after the lucrative US healthcare market. Raised $20M at the top of the market in November 2021, weeks before the global tech crash. Chasing big deals in coming quarters.

15. 88 Energy (ASX:88E) - Cash balance: $10M

Preparing to drill a well in Alaska, USA next door to $1.2BN capped neighbour Pantheon Resources.

To demonstrate the power of capital markets and how market dynamics work with capital raises, let’s take a look at our 2019 Energy Pick of the Year, Elixir Energy (ASX:EXR).

Consider this marked up chart EXR, where the company raised capital at two different price points based on project development as well as market conditions at the time:

EXR completed a small but very tough raise for $2M in May 2020 at 2 cents, a 20% discount to the share price at the time - this was in the depths of the COVID market crash, not a time a small cap company wants to be raising cash.

(But a great time to be investing, which is why we are participating in most cap raises at the moment)

Fast forward to April/May 2021 and EXR raised $26.6M at 36 cents, at an 18% discount.

That much larger raise was due to a combination of the market being hot AND the company delivering on some key milestones and objectives.

This cap raise from 2021 has allowed long term EXR investors to rest easy during the current tough market with a big cash balance.

The idea is to raise only small amounts of capital in down markets and raise big in up markets.

We hope this example demonstrates how there can be difficult and successful raises, depending on market conditions and how a company’s project is tracking.

A good indication that we are in a tough market is when we see more “exotic” funding arrangements start to appear - usually with very favourable terms to the new capital providers.

As the saying goes - “he who holds the gold makes the rules”.

This is especially true for small caps in a rough market.

We have noticed a lot of companies raising capital using methods that most investors may not be accustomed to seeing - convertible notes, option funding agreements, controlled placement agreements, etc.

Those who are new to the markets may not be familiar with these as they are rarely ever done in bull markets, where issuing new equity to raise capital is the preferred option.

For some context, the last time these exotic funding arrangements were popular was back in early-2018 through to mid-2019 when markets were depressed.

One particular type of financing we are starting to see a lot of recently is “convertible notes”.

A convertible note is a loan made to a company, which includes interest payments and must be repaid in cash at maturity date OR converted into shares of the company at whatever the share price is when the loan repayment is due.

Convertible notes work well if the company uses the loan money to deliver a share price re-rating, and can elect to repay the loan or convert the loan to shares at a higher share price.

BUT... if the company fails to light up the market with their use of the loan funds, and the share price goes down, the convertible noteholders can convert the loan to shares at an even further depressed share price.

This share price weakness is compounded by the fact that the company likely needs to raise capital AGAIN if the loaned money is unsuccessfully deployed - not good for any shareholders that came in prior to the convertible notes.

Exotic funding arrangements are risky but can work in favour of the companies as it buys them time to deliver major milestones and hopefully a material re-rate in the company’s share price.

The perfect example of this is Latin Resources (ASX: LRS) which had less than $1M in cash going into its maiden lithium drilling program in Brazil early this year.

Many investors would have expected a large capital raise, but LRS chose to arrange an “option funding agreement”, securing $2.5M cash against its listed, in-the-money options — enough cash to survive and finance at least some portion of its drilling program.

A few months later LRS confirmed a new lithium discovery, raised $35M at a significantly higher share price, and repaid that loan with ease... to the delight of long term shareholders like us.

However, if LRS had failed to find lithium the convertible notes would have been very painful to deal with.

Of course, it doesn't always work out for companies.

One example from our Portfolio is Thomson Resources (ASX: TMZ), which raised $2.25M via a share placement agreement (effectively a convertible note).

TMZ did buy itself some time and delivered on some milestones but the market did not react favourably, with precious metals broadly out of favour for the last 12 months.

The convertible note caused a downward spiral in the price as the lender converted it to shares, selling those shares on the market to recoup capital pushing the price down further.

TMZ can still emerge from this rough patch, it is just a lot harder with the overhang from the converted note shares needing to be washed through.

(We should mention that we are still long term bulls on gold and silver, despite the current rough patch)

This is why ‘funding risk’ is so important to monitor as investors, particularly in a down market and why it is key to pay attention to cash balances of each of the stocks in your portfolio.

Again, the quarterly cash balances of each of the stocks in our Portfolios are tracked in our Cap Structure Spreadsheet, which you can access here.

🗣️ This week’s Quick Takes

88E: 88E neighbour $1.4BN Pantheon just weeks away from flow test

BPM: Assay results from Hawkins lead-zinc project

GAL: New nickel sulphide discovery confirmed

GTR: Got questions for GTR director Bruce Lane?

KNI: 3 Drill Programs in Q1 after strong cobalt results

LRS: Brokers comparing LRS to $5.7BN capped Sigma Lithium

LRS: A whiff of rare earths at LRS’s Cloud Nine

SGA: Companies of interest at IMARC conference

VN8: Growing, growing...

VUL: Vulcan to expand into France

This week in our Portfolios 🧬 🦉 🏹

PFE Commences Manganese Drilling

Yesterday, Panterra Minerals (ASX:PFE) confirmed that it has started a new exploration drilling campaign, this time for manganese — a crucial battery metal.

PFE has already found a number of high grade rock chips (up to 44% Mn), and is now drill testing an 800m long, 5m thick outcropping of potentially high grade manganese.

PFE has the same rocks, in the same geological setting as $162M capped Element 25. Now PFE needs to drill test that manganese outcropping and see if it can deliver a discovery.

The market seemed to like its chances with the stock closing up 54% after its announcement yesterday.

📰 Read our full Note: PFE now drilling for manganese - with a tiny enterprise value

⏲️ Upcoming potential share price catalysts

Updates this week:

- BPM: Assay results for Hawkins lead-zinc prospect

- BPM released its assay results that fell within our Bear and Base cases. Read our Quick Take here; a longer note is coming soon.

- IVZ: drilling its giant gas prospect in Zimbabwe

- IVZ went into a trading halt after a big seller entered the market. IVZ released a response to the ASX saying “it has no results analysed or available to release”.

- GAL is undertaking a second round of drilling at its Callisto PGE discovery in WA.

- Assays from RC drilling 400m north of the discovery hole confirmed a whole new nickel sulphide structure - see our Quick Take on the news here.

- PFE: Assay results for manganese (Weelarrana) project, and for polymetallic (Hellcat) project.

- Drilling commenced at Weelarrana - read our full note here. No Hellcat update.

No material news this week:

- LNR: Maiden drilling for rare earths along strike from Hastings Technology Metals

- GTR: Drilling results for uranium in Wyoming, USA.

- TYX: Drilling for lithium in Angola.

- RAS: Drilling for lithium next door to Core Lithium in the Northern Territory.

- PRL: Awaiting final execution of a joint development agreement with Total Eren

Have a great weekend,

Next Investors.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.