The "Lesser Kown" Energy Transition Metals: Copper, Aluminium, Graphite, Helium, Rare Earths

Published 05-FEB-2022 09:11 A.M.

|

27 minute read

Our best investments to date have been in battery metals.

We think this investment theme is just getting started and we’re determined to repeat that success across a range of new commodities that are critical to the “energy transition”.

Long time readers will be familiar with our current 45x return on Vulcan Energy Resources (ASX:VUL) and our 6x return on Euro Manganese (ASX:EMN).

Over the last six months we’ve been hard at work looking for new investments in the battery metals and “energy transition” metals space.

We hope to announce these new investments in the coming weeks, and you can find our latest investment and a sneak peek of future investments below.

Yesterday we added a new “energy transition” metal investment to our Catalyst Hunter portfolio: Auking Mining (ASX:AKN), who have a 6.8MT @1.3% copper JORC resource and a key catalyst coming in the next few months that could help them extract it.

Here is a quick, high-level summary of why we invested in our AKN Investment Memo.

In our portfolio initiation for AKN, we stressed our view that copper could join a growing cadre of industrial metals that are quickly evolving into battery and “energy transition” metals.

So how much further to go in the battery metals run?

Australia is a country immersed in the mining industry.

As an Australian, it’s easy to forget that most people around the world probably haven’t caught on to investing in the raw materials needed to build batteries and electric vehicles.

Most investors interested in the space are likely investing directly in companies that make and sell electric cars.

We are hoping this will soon change as supply chain crunches on battery metals will start to come on the radar of the mainstream investor community.

We like to look at mainstream media coverage of a macro theme as a barometer on broader investor interest in that theme.

Quite simply, the more people that are informed on a thematic the more likely they are to invest in that thematic as the problem to solve intensifies.

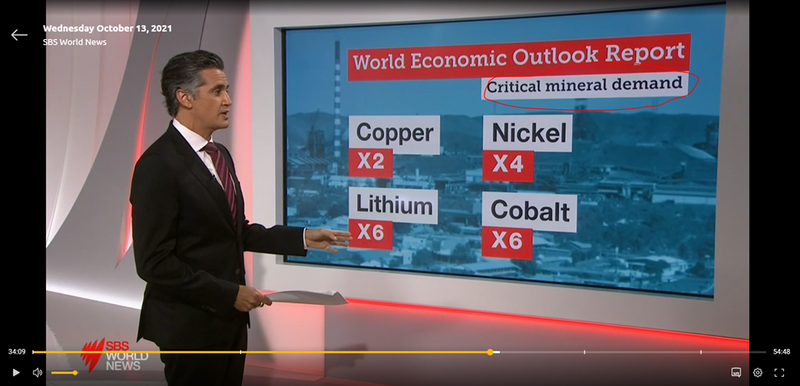

Last year we wrote about mainstream media SBS news talking about crucial battery metals, likely energising an entire new cohort of investors to look into the space:

We also noted when famous “new-age billionaire” Chamath Palihapitiya tweeted that he was closely following materials and mining to provide the raw inputs for batteries and electric vehicles:

Chamath has a decent sized following with 1.5M twitter followers, most likely containing lots of professional investors and fund managers.

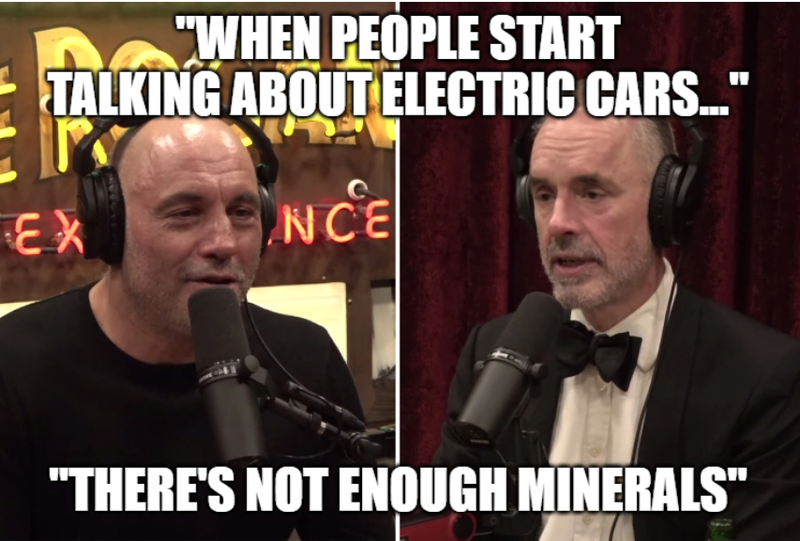

This week we saw two very well known (and followed) public figures acknowledge that there will be a shortage of battery metals as the world looks to switch to electric.

Love them or hate them, Joe Rogan and Jordan Peterson both have HUGE followings and influence.

We were very surprised to hear them discussing our favourite topic of battery metals shortages...

It is estimated the Joe Rogan podcast reaches 11 million viewers per episode.

Last week the host pointed out that it will be nearly impossible to fully switch to electric cars because “there aren’t enough minerals” to build enough batteries to replace all the internal combustion engines.

Here is the key snippet from their discussion from 19m45s into the podcast:

The point we are trying to make is that the shortage of battery metals to deliver the global switch to electric is starting to move into very mainstream discussions - which means more people will become aware of the problem leading to more investment dollars flowing into companies in the battery metals space.

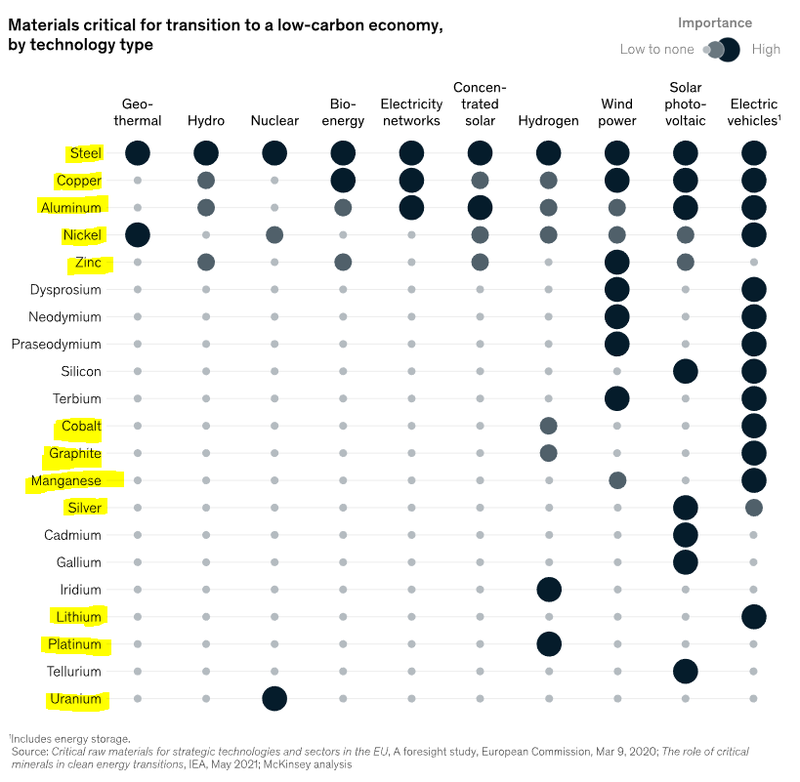

Rogan and Peterson’s off the cuff comments are confirmed by the below table we shared with you two weeks ago from McKinsey showing which key commodities are needed for each green energy initiative.

You can see our current exposures highlighted in yellow below, and also the gaps where we don’t have an investment yet (mostly rare earths):

We have been working hard over the last 6 months and have some new investments coming up in the battery metals space that we hope have the potential to replicate our previous battery metals success.

Here are some of the battery metals commodities we’re looking at investing in with a brief explanation of the macro tailwinds driving them forward:

Copper

Electric vehicles use up to 3.5x more copper than a standard petrol car, copper is already the third most widely used metal in the world - and with further infrastructure stimulus waiting in the wings, we see it as strongly leveraged to the global electrification boom and anticipated commodities super cycle over the coming decade.

Our New Copper Investment: We think AKN is an example of an “under-the-radar” copper play - it has a 6.8MT @1.3% copper JORC resource, but in the past the resource wasn’t economical to extract.

That’s why AKN is trying a new extraction tech that could unlock this sizeable resource and we will know the results in a couple of months.

Here is why we invested in AKN.

Aluminium

Aluminium is also a commodity we’re looking closely at. Aluminum prices are near a 13-year high and it's demand is spread across many industries.

The majority of consumption is weighted towards industries poised to benefit from infrastructure stimulus.

Our Current Aluminium Investment: FYI Resources (ASX:FYI) is focused on developing an innovative and vertically integrated high quality, high-purity alumina for use in various high growth tech applications.

Here is why we invested in FYI

Another Aluminium Investment Coming Soon: We have been working on this new investment for nearly two years and are very excited to add it to our portfolio soon.

Graphite

Graphite is the primary ingredient for just about every electric vehicle (EV) battery - comprising over 50% of every lithium-ion battery (and over 95% of every battery anode).

With more and more customers choosing electric vehicles (EVs), and this trend gathering momentum in an increasingly climate-concerned world, we think that demand for graphite is expected to grow strongly over the next 10-20 years.

Our Current Graphite Investment: Towards the back end of 2021 we made our first investment in the graphite space - here is why we invested in Evolution Energy Minerals (ASX:EV1).

EV1 was our 2021 Pick of the Year in the Wise-Owl portfolio, and we liked the advanced stage of the project, low capex and the strong ESG focus .

Another Graphite Investment Coming Soon: With graphite being a core component in EV battery anodes, we think the market is underestimating how much of it will be needed over the long-run. We will be announcing a new graphite investment in our Next Investor portfolio soon.

Helium

Helium is a critical component in the manufacture of semiconductors, which are critical in modern electric vehicles.

Helium has high thermal conductivity and because of its unique properties as an “inert” gas it does not react with the silicon the semiconductor chips are made from. As a result, these semiconductor chips need helium because it keeps them cool during the manufacturing process and doesn’t react with the core component - silicon.

Semiconductors have become a critical part of the supply-chain across almost all industries from computer chips that power the modern world to cars, smartphones and military equipment.

With heightened geopolitical tensions across the world, the US is currently looking to build out its own domestic supply-chain for semiconductor manufacturing , which are predominantly manufactured in Taiwan.

Our Current Helium Investment: Trying to get in early on this theme we invested in Grand Gulf Energy (ASX:GGE) which is a helium exploration company aiming to make a commercial helium discovery in Utah, USA.

Here is why we invested in GGE and what we want to see from them this year.

Another Helium Investment Coming Soon: We recognise things are moving fast and helium could very quickly become front and centre in investors minds so we have been looking at increasing our exposure to the sector.

We are towards the latter stages of our due diligence on a new helium exploration company that we hope will IPO soon.

Rare Earths

We think Rare Earths are likely going to continue in a similar vein to lithium and graphite - these metals are not just crucial to an impending EV boom - they are increasingly seen as strategic.

From defense applications to permanent magnets and wind turbines, Rare Earths are definitely a priority for us going forward.

We almost made a couple of Rare Earths investments during 2021 but none of them got across the line in the end for various reasons.

If you have a favourite Rare Earths play - please get in touch by responding to this email. We’ve been running through different companies in the space but haven’t found one that we wanted to invest in yet.

Our focus is on making investments in the companies we think have the highest quality assets with the highest probability of success so we are open to companies at all stages of their projects lifecycle - exploration all the way through to production.

We will also look at private assets with a “line of sight” to IPO within 18 months.

As always, we love reading feedback from our readers so if you have any suggestions for investments in any of the sectors we mentioned above, feel free to reach out and share them with us.

📰 This week on Next Investors

To start the week, our gold investment, Los Cerros (ASX:LCL) announced the latest batch of drill results at their main Tesorito gold project in Colombia, which included their customary spectacular hits (2 holes exceeding 88 metres and grades over 1 g/t Au, which is considered high-grade for porphyry systems).

What stood out to us is that LCL has now defined the southern and northern edges of their main project. What this means is that they are now comfortable that they have not missed any massive areas of interest along those edges, and can finally move to the JORC resource estimation stage.

Given how prolific the gold mineralisation has been to date at Tesorito, we are very keen to see just how big the deposit is. Whilst we’re not geologists, we do read what the experts say, and so have devised our own “ranking system” as to our expectations for the total size of the JORC estimate to come.

The answer should be revealed before the new tax year begins.

One correction from our LCL article emailed on Wednesday is that we mistakenly wrote that the first hole to drill “Jabba the Blob” had not found much gold mineralisation. The fact is that the first hole into Jabba has not yet been completed - we anticipate that 3 holes will be completed this quarter, and remain keen to see what drilling unveils here.

📰 Read the full breakdown - LCL finally hits the edge of its giant gold system - JORC resource estimate coming.

To end the week BPM Minerals (ASX:BPM) announced that the Hawkins project had FINALLY been granted, and with a bit of prep work still to do it looks like it will be drilled sometime in H2 this calendar year.

We invested in BPM back in May 2021 because we liked that their lead-zinc project shared heaps of the same geological fundamentals with Rumble Resources’ recent discovery in the Earaheedy basin, WA.

With BPM having secured the rig that Rumble has been using at their discovery and drilling planned for later in the year, BPM can finally get to work on its projects in this part of WA.

Rumble’s lead-zinc discovery in the Earaheedy basin re-rated its share price by 800% and we are invested in BPM, hopeful that they can do the same thing.

📰 Read the full breakdown: BPM’s Lead-Zinc Project Finally Granted - Now They Can Drill It

In our other portfolios 🧬 🦉 🏹

🦉 Wise-Owl

Early in the week Food Revolution Group (ASX:FOD) put out its quarterly report revealing two cash flow positive months in its latest quarterly and announcing the launch of a new product, Plant-Based Protein Smoothies.

With the FOD share price nearing all-time lows we think that the company has been oversold given the strengthening earnings performance and recent slate of new products launched.

In our coverage of the quarterly we do a side-by-side comparison with maggie beer holdings which is trading at an almost 3x higher revenue/enterprise value multiple. We highlight that this is not down to profitability but in our opinion is related to revenue growth.

With the new product launches opening up FOD to new markets we think that the market will ultimately judge FOD based on its ability to grow its revenues and the expansion of its business into new market segments.

📰 Read the full breakdown: FOD on Cusp of Turnaround with Strong Quarterly and New Products

🏹 Catalyst Hunter

⚠️NEW INVESTMENT ALERT⚠️

This week in the Catalyst Hunter portfolio we announced our newest investment - Auking Mining (ASX:AKN).

AKN is looking to develop its 75% owned copper/zinc JORC resource near Halls Creek in WA.

With AKN recently having completed a drilling program there is serious scope for the JORC resource to be upgraded across both of the two deposits that make up AKN’s Copper/Zinc project.

The asset was previously taken to pre feasibility study (PFS) stage but due to metallurgical issues the shallow-high grade copper resource at one of the two deposits couldn't be included. AKN are now looking to resolve this issue and find a way to make the project economically viable.

Outside of the JORC resource and the hunt for a met-work solution we detailed the top 8 reasons for making our investment in our launch note.

📰 Read the full breakdown of our 8 key reasons for investing here: Shallow Copper Resource - waiting to be de-risked through “met work”

🧬 Finfeed

On Tuesday our 2021 Biotech Pick of the Year Dimerix (ASX:DXB) announced that first European regulatory approvals were given for DXB’s kidney disease study in Denmark - much earlier than we expected.

The first approvals in Europe is a big deal because it is the first regulatory approval given for DXB’s trials outside of Australia/NZ, and it effectively moves the timeframes for subsequent milestones forward by around a month.

DXB in the announcement also confirmed that at present they had selected 73 of the planned 75 global sites (97%) across 12 different countries to conduct part 1 of the phase III study, with 5 of those sites being set-up in Australia and 15 planned for Europe, the approvals mean the total number of sites DXB has access to now is at ~20 of the planned 75 sites.

We also discussed where DXB are at with their COVID-19 “side-bet” trials which we expect to receive some newsflow from over the next 6-9 months.

📰 Read the full breakdown: Earlier than Expected - DXB Gets First Regulatory Approval in Europe.

🗣️ Quick takes on key portfolio company events this week:

Vulcan Energy Resources (ASX:VUL)

On Monday VUL came out with a strong announcement with respect to the conversion of it’s binding term sheet with LG Energy Solutions (LGES) into a binding lithium hydroxide offtake agreement.

The agreement follows on from the “binding term sheet” signed on 18 July 2021 which at the time was conditional on the execution of a “Definitive Agreement”. LG Energy Solutions is the second largest battery maker in the world with over 20% market share and direct supply contracts with some of Europe's biggest automakers.

The agreement is for an initial 5-year term commencing on the 1st of January 2025 with an option to extend it for a further 5-years beyond this date. Under the agreement LGES will purchase between 41,000 to 50,000 metric tonnes of battery grade lithium hydroxide over the agreement's 5 year life with pricing being based on the market prices lithium hydroxide.

The offtake agreement being converted from a binding term sheet into an agreement gives VUL more certainty around demand which is a major positive given VUL are quickly progressing the project towards development.

Although this isn't a direct achievement of any of our objectives set out in our 2022 Investment memo, we think that this agreement indirectly assists with VUL’s ability to secure project financing so are pleased with the announcement this week.

Next: We want to see VUL’s demonstration plant operating, DFS completed, and VUL’s listing on the main Frankfurt stock exchange.

Kuniko (ASX:KNI)

Early in the week KNI announced the appointment of 3 geologists that will form the basis for the exploration team in-country in Norway.

We did a brief summary internally of the appointments as follows:

- Trond Brenden-Veisa (Exploration Manager): Over 25 years’ experience across different continents. Was also the exploration manager for Oslo listed Elkem ASA (capped at ~A$3.4 billion) for over 13-years.

- Milena Farajewicz (Exploration Geologist): Over 3 years’ experience with Mawson Resources focussed on gold/cobalt exploration in northern Finland and has been involved in academic research into the cobalt space.

- Harry Guest (Exploration Geologist): Approx 2 years’ experience with Alba Mineral Resources. Academic achievements include a thesis focused on theTrøndelag region of Norway, where Kuniko has its Undal-Nyberget Copper Project.

Overall a team with a decent mix of experience and expertise in this part of the world. The appointment of an in-country exploration team will assist KNI in achieving the objectives we set for them in our 2022 investment memo which is mostly centred around exploration programs.

Next: We want to see KNI drill the high-priority EM targets at its cobalt project.

Elixir Energy (ASX:EXR) -

We don't normally write-up the quarterly’s unless it is for our revenue generating portfolio companies but the EXR quarterly report included some of the Chairman Neil Young’s commentary on EXR's Hydrogen project so we thought we would do a slightly deeper-dive.

Neil in the opening of the quarterly wrote a ~2 page piece on his site-visit to Mongolia after almost 2-years absence due to COVID. One thing that caught our attention was Neil’s commentary around the proximity of EXR’s grounds to China - Expected to be a key export market for Hydrogen in the future.

Neil said that he sees a “key source of competitive advantage in supplying hydrogen in the future will be minimizing the very high costs of delivering hydrogen”. He then said “It is increasingly my view that Gobi H2 (Hydrogen project) is emerging as one the best potential green hydrogen export projects globally”.

It is still relatively early days with EXR’s hydrogen project given the company is still capturing renewable energy resource data but all of what Neil said resonates with our view of the Hydrogen markets, we will be watching to see how EXR’s hydrogen strategy develops over 2022 and have made it one of our key objectives for our 2022 investment memo (coming soon).

We bought more EXR on market a couple of weeks at at 16.5c

Next: For EXR it is all about production testing. We will monitor the project over the next 12 months and provide updates and commentary as it progresses.

Euro Manganese (ASX:EMN)

On Tuesday, EMN announced that the buyback of the 1.2% net smelter royalty (NSR) over its manganese project had been settled through the payment of US$1.8m in cash and the issuance of 4,820,109 in EMN shares for another US$1.8m.

The settlement of the final balance follows an agreement signed in may 2021 with the project vendor to purchase the 1.2% NSR for US$4.5m. The first installment of US$900k was paid upon signing and the remainder has now been settled.

After the recent CAD$8.5m investment from the European Bank for Reconstruction and Development (EBRD), the US$1.8m isn't likely to impact EMN’s cash balance materially which is a positive. As for the 4.8M shares in EMN that were issued, these are being listed on the TSX and will have a 4-month and one day escrow period starting on the 1st of February 2022.

The NSR being extinguished contributes to the delivery of the DFS and should improve the project economics as there will be no allowance made for royalty payments.

The completion of the DFS is a core component of our 2022 investment memo for EMN.

Next: We want to see EMN complete the construction of the demonstration plant and announce the updated DFS.

GTI Resources (ASX:GTR)

Late in the week GTR announced that the terms for the spin-out of its gold assets via a sale process to regener8 resources.

The deal is structured so that upon completion GTR will net 5M in shares of the newly listed entity @20C (valued at $1M), $150k in cash and 1.5M performance rights for a total combined value of ~$1.45M.

We don't mind seeing our portfolio company’s do these sorts of deals as it often means they get rid of any maintenance expenditure that is being incurred upholding the projects and naturally means they dedicate 100% of the company’s capital and time to the core projects, in this case being the uranium projects.

This sits outside of our 2022 investment memo given we are primarily invested in GTR for its uranium project, this shifting of focus away from other assets to us is welcomed news.

Next: We want to see the drilling program at the ISR uranium project in Wyoming completed.

Thomson Resources (ASX:TMZ)

On Friday, TMZ announced the signing of a $5M at the market “equity funding facility”, which is basically $5M in cash that TMZ has access to at any time over the next 12-months.

The facility can be tapped by TMZ at any time with the gross draw-down minus a 6% commission to the financier being issued in shares at the same time.

The facility takes away any impending capital raise risk with TMZ which is a positive and it seems to have been done on the same terms as a placement would have been done with the 6% commission generally representing a similar amount that would have been paid to a broker group to organise a raise.

The capital raised will go a long way towards TMZ fulfilling the first objective listed in our 2022 investment memo (coming soon) which is to see TMZ prove-up a resource >100 million ounces silver equivalent.

Next: We want to see the JORC resources delivered and an updated “global” resource announced that validates the hub and spoke strategy that TMZ is working towards.

Vonex Limited (VN8)

We combed through the 4C of our telco investment, Vonex (VN8) which was released earlier this week. Overall, we think the company is continuing to progress well, snapping up another value accretive business into the fold (South Australia’s Voltech) during the quarter.

The headline figures read well too, with H1 FY22 sales revenue up 67% to $14.94 million, annualised recurring revenue (ARR) more than doubling to sit at ~$34.5 million to start 2022, and the PBX base now exceeding 90,000 customers.

Vonex is now trading around 0.8x ARR (low for the sector), bringing in roughly $7-8m in sales revenue each quarter, and has now demonstrated several quarters of positive cash flow in succession, and so we think there is some upside to be realised if they can continue on this trajectory.

Next: Complete integration of last year’s acquisitions, reflected in continual customer base and sales growth quarter on quarter

Alexium International (ASX:AJX)

Operational cash burn of $535K is acceptable given seasonality in the cold North American winter. We expect AJX sales to pick up in the coming two quarters as the Premier Body Armour partnership evolves. Alexium’s relationship with Serta was solidified by an Innovation Award from the company - so bedding sales should be strong heading into the warmer summer months.

This was the crucial bit of the 4C for us - a letter of intent with Alterna CS for a $3M-$5M line of credit to support AJX’s growth. That suggests that debt rather than equity funding is the way forward for AJX as it moves towards operating cash flow positive status.

The line of credit comes in at 8.25% - not prohibitively high given AJX’s strong top-line revenue - AJX reported 46% revenue growth vs prior corresponding period.

Next: Revenue from body armour segment, increased revenue from bedding sales (particularly Serta) and next quarter, a result that is mighty close to cash-flow positive.

Creso Pharma (ASX:CPH)

This week CPH released its December quarterly reports showing an increase in revenues to $2M - up 74% on the last quarter. Despite revenues being higher, CPH’s had negative operating cash flow of $4.4M. This isn't unexpected to us given the company is still in the growth stage of its lifecycle.

Amongst the more unusual news from the quarterly was the announcement of CPH “Entering the Metaverse” via its landholing in the Sandbox, a digital world. CPH announced that they would be developing a digital replica of their 24,000 sq foot cannabis facility in Nova Scotia in the software.

CPH also announced that they would be developing a virtual stage next-door to the cannabis facility where they can hold virtual concerts/events. It’s a strange marketing play, potentially forward thinking, but also potentially a distraction for the company.

CPH said that the cost of the project so far had been US$150K, if we see CPH being mentioned in the US mainstream news off the back of this then it will come off as significantly cheaper marketing spend versus the costs of traditional marketing initiatives.

Later in the week, CPH also announced the acquisition of a US-based CBD consumer packaged goods company focused on plant-based and CBD products. The business generated US$5.7m in revenues in CY2021 and CPH is paying US$21m upfront via an all-share offer with a maximum deferred consideration component of US$38.5m contingent on certain revenue milestones.

CPH is making moves in the US market but the amount being paid could raise eyebrows - hence the earn out conditions.

Next: We want to see a reduced operating cash burn.

Advanced Human Imaging (ASX:AHI)

This week AHI released its 4C that we hoped would highlight how much cash was generated from the Tinjoy partnership.

Before the deal, AHI came out with what now appear to be lofty predictions for its Tinjoy revenue. Based on AHI’s announcement on August 18th investors expected a revenue commitment of $9M of which AHI would be entitled to 70%.

Given AHI’s history of over-promising and under delivering we set our revenue expectations low for AHI’s Tinjoy partnership predicting about 3% penetration of pre-registered users and about $200K in revenue.

This week it was revealed that AHI had secured $144K in revenues - we don’t know exactly how much of this is associated with Tinjoy.

We hope that AHI is more conservative in the future when setting expectations for its shareholders, as it can damage the trust in the company's ability to deliver in the future.

We like when companies have grand ambitions, and big revenue numbers sound nice, but if expectations can not realistically be met it sets shareholders up for disappointment.

Auroch Minerals (ASX:AOU) - Wise-Owl portfolio

To start the week AOU announced the resignation of its chairman Edward Mason and at the same time the appointment of current non-executive director Michael Edwards as his replacement.

With Michael having over 25 years experience as a geologist and having worked as a corporate advisor for much of his career brings a lot of experience to the AOU board of directors. Most recently Michael was involved in leading the Firefly Resources merger with Gascoyne Resources. He is also the current chairman of Greenstone Resources as well as a non-executive director of De.Mem Limited.

It is interesting to see Edward Mason leave so suddenly given he has been with the company since 2019 but we think freshening up leadership is never a bad thing.

Next: We are watching to see the results from the drilling program at AOU’s nickel projects.

Grand Gulf Energy (ASX:GGE) - Catalyst Hunter portfolio

On Wednesday GGE announced that a surface land use agreement (SLUA) for its planned maiden drilling program had been executed with the private landowners at its helium project and that a preferred drilling contractor had been nominated.

The “SLUA” gives GGE the rights to access the grounds where drilling will take place, this means GGE can start construction works at the well-sites ahead of permitting and rig contracting.

The announcement also detailed that the newly appointed drilling superintendent Doug Frederick had nominated a preferred drilling contractor. We did a deep-dive into his experience with helium projects in this region in our last note on GGE.

We mentioned that Doug’s experience drilling at the Doe Canyon helium field next-door would be instrumental to the drilling program coming up and this nomination is the first sign Doug is bringing that experience to GGE with the nominated contractors being the same ones that were used at Doe-Canyon.

The news this week is another step towards the key objective we set for GGE in our 2022 investment memo, being the drilling of the first well at its helium project.

Next: We want to see permitting complete and a firm rig contract signed leading upto the maiden drilling program.

Aldoro Resources (ASX:ARN) - Catalyst Hunter portfolio

ARN this week completed phase 2 of the drilling program at its lithium/rubidium project, with another 15-holes done and 32 to go.

The drilling program is targeting lithium and rubidium mineralisation, and with all of the drill holes from this second phase of drilling returning pegmatite intercepts everything seems to be progressing nicely for ARN. Ultimately the proof will be in the assay results though.

One of two objectives in our 2022 investment memo (coming soon) was to see ARN get some drilling done targeting lithium/rubidium so we are eager to see what comes from the assay results.

Next: We want to see the assay results from the current round of drilling at ARN’s lithium/rubidium project.

Ragusa Minerals (ASX:RAS) - Catalyst Hunter portfolio

On Friday RAS announced the assay results from its gold project in Zimbabwe with peak intercepts as follows:

- 10.43m @ 2.5 g/t gold from 128m

- 5.17m @ 3.68 g/t gold from 146m

- 13.96m @ 3.61 g/t gold from 172m

The results follow from a 1,236m RC drilling program done in 2021 and look good enough to warrant some level of market interest but this project isn't a reason for our investment in RAS.

As per our 2022 investment memo (coming soon) the main reasons we are invested in RAS are for the WA halloysite project and the company’s Alaskan Gold projects.

Next: We want to see RAS start the maiden drilling program commenced at the WA halloysite project.

🌎 Mainstream Media:

Lithium price rockets 45pc with no end in sight (AFR)

Ford to Spend Up to $20 Billion Reorganizing for Shift to Electric Cars (Bloomberg)

Iron ore miners win export boost (AFR)

Relief rally lifts oil to biggest January gain in decades (AFR)

War tensions another tailwind for commodities (AFR)

Why Russia has never accepted Ukrainian independence (The Economist)

Wall St ends winning run as Facebook forecast halts tech-led recovery (Reuters)

Have a great weekend,

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.