Quarterly Report Reviews for our Investments

Published 29-APR-2023 13:00 P.M.

|

31 minute read

Being publicly listed means a company needs to be transparent with progress and financials.

Small cap companies (pre-profit) are required to report to the market on a quarterly basis.

The quarterly report includes financial statements, management commentary on the company's progress, and maybe also some “forward looking statements”.

The key thing we look for is how much money the company has left.

A company's share price generally stagnates when the market is expecting a capital raise, especially in a broadly negative market.

A healthy cash balance is important to help the share price react to a good news announcement.

Based on a small cap company's plan, we have a general idea of the next “big announcement” the market is waiting for.

In the quarterly reports we also look for any clues in the management commentary about the progress or timing of the company's next major milestone.

This could be an upcoming drill result, JORC resource or economic study in resources.

In biotechs we eagerly anticipate results of clinical trials.

For tech it’s usually big contracts or increased revenue numbers.

These are key material announcements that can re-rate share prices if they beat market expectations.

Quarterly reporting happens at the end of every quarter. It marks a time when most small cap companies need to reveal their cash balances and update the market on what they are up to.

This week marked the final trading week for April which is the deadline for ASX small caps to reveal their quarterly report.

We spent the last few days reading the March quarterly reports across all of our Investments.

Below is a summary of each companies:

- cash balance (as at March 31st);

- what they achieved in Jan-March quarter; and

- what key news we are expecting next that could re-rate the share price if the news exceeds the markets expectations.

Here is the list, featuring all our Investments across our Next Investors, Wise Owl, Catalyst Hunter and Finfeed Portfolios (in alphabetical order by company name).

88 Energy (ASX: 88E)

Cash: $26.3M

Shares Held: 20,687,632

88E’s major accomplishment for the quarter was the drilling of its Hickory-1 well - see our take on the drill results here.

We suspect that some of the drill costs from the Hickory-1 well are still yet to be paid so the next quarterly cash balance should be more representative of the company’s cash position.

Next Catalyst: The next 6-9 months will be about preparing for the flow test 88E is planning at Hickory-1 in late 2023/early 2024.

Alexium International Group (ASX:AJX)

Cash: US$577K

Shares Held: 6,178,333

In terms of revenues, the company had a relatively neutral quarter and cited “soft conditions” in the US bedding market as a reason for the lack of growth in revenues.

The positives were in the “outlook” section of the quarterly report where AJX detailed its move from the development/testing stage to commercialisation for some of its new technologies across the mattress/bedding and military industries.

The report was quite comprehensive in outlining the company’s product lines and commercialisation plans going forward - it’s worth a read.

Next Catalyst: More commercial deals / revenue

Arovella Therapeutics (ASX:ALA)

Cash: $3.25M

Shares Held: 18,226,579

The big news for the quarter was the new data the company presented at a conference held by the American Association for Cancer Research (AACR) - see our take on that news here.

At the same time ALA and $803M-capped Imugene also progressed their partnership after successful in vitro trials (test tube trials) - see our take on that news here.

Next Catalyst: Results from the ALA/Imugene in vivo (animal) studies

AuKing Mining (ASX:AKN)

Cash: $5.28M

Shares Held: 1,515,152

AKN has a healthy cash balance, having raised $2.2M during the quarter as part of the placement to acquire a suite of Tanzanian exploration assets.

The key milestone delivered during the quarter was completing the acquisition in January.

However, two of the key Prospecting Licences (PLs) acquired, hosting highly prospective uranium ground, were subsequently revoked by the Tanzanian government apparently due to a malfunction in the licence allocation system.

AKN has lodged an appeal with the Tanzanian Minister for Mines, and are hopeful of receiving a favourable decision in the near term that would reinstate these PLs.

Meanwhile, the company has commenced a 4,400m drilling campaign at its Manyoni Uranium Project in central Tanzania, with the aim to “provide the basis for an updated resource estimate” — a precursor for development activities.

Next Catalyst: Return of two key prospecting licences (timeframe unknown)

BOD Science (ASX: BOD)

Cash: $3.33M

Shares Held: 3,535,112

Looking at its financial performance, BOD’s operating cash expenses improved 10% to ~$1M from the previous quarter.

Cash receipts grew 66% to $813k in this quarter, despite a 49% drop in sales revenue to $261k. A $500k initial cash payment for exclusive supply agreement with Arrotex Pharmaceuticals helped bolster receipts.

As a result, BOD held ~$3.3M in cash at 31 March 2023 - a healthy position that provides plenty of runway to complete its most pressing clinical trials that are now underway.

On the operations front, we are particularly interested in progress with BOD’s Phase IIb clinical trial for its new CBD insomnia product for the Australian pharmacy-only (Schedule 3) market.

In March, the trial reached a major study milestone with ‘Last patient, First visit’ indicating the completion of the trial screening and randomisation phase i.e. all patients have been recruited for the insomnia treatment trial.

BOD is also progressing its acquisition of the Aqua Phase technology, which we believe will be completed by 30 June 2023.

Next Catalyst: Results of Phase IIb clinical trial for insomnia / compete Aqua Phase acquisition

BPM Minerals (ASX: BPM)

Cash: $4.2M

Shares Held: 1,670,000

BPM’s cash position is strong relative to its tiny ~$5M market cap, at current market prices the company’s Enterprise Value (EV) is ~$1M.

Next for BPM is a drill program at its Claw gold project along strike from $1.7BN Capricorn Metals Mount Gibson gold mine, with heritage results due this quarter.

With the gold price close to all time highs any success at Claw could be good for BPM’s share price.

Next Catalyst: Drilling Claw gold project (Q3)

Canyon Resources (ASX:CAY)

Cash: $12M

Shares Held: 3,000,000

CAY is in quiet execution mode as investors wait patiently for the mining permit to be granted by the Cameroon government.

Without this permit, we expect the company to be in a limbo state as investors and offtake partners wait for the project to be de-risked.

Next Catalyst: Mining Permit granted by Cameroon government

Dimerix (ASX:DXB)

Cash: $4.03M

Shares Held: 2,525,000

DXB has continued its strong recruitment momentum with 116 patients now recruited into its Phase III FSGS trial.

This quarter DXB announced that it was in “advanced partnering negotiations” with regards to licensing and commercialising its treatment.

The company spent $4.5M this quarter on its clinical trial, and with less than an estimated quarter of funding left, (according to section 8.5 of the quarterly) it will need capital soon.

What we are waiting for next is an update on the 72nd patient being dosed, which will give us a 35 week ‘clock’ from which to countdown towards interim analysis results.

We are also awaiting the announcement of any partnership deals, which we think would be a material catalyst for the company.

Next Catalyst: Interim analysis results for Phase III FSGS trial

European Metals Holdings (ASX:EMH)

Cash: $16.7M

Shares Held: 261,000

During the March quarter EMH’s Europe based lithium project was declared a “Strategic Project” of the European Commission’s Just Transition Fund (JTF).

The declaration means EMH’s project is now eligible to apply for grants up to a maximum of ~€49M (A$82.5M).

EMH also kicked off its Definitive Feasibility Study (DFS) by appointing consultants DRA Global.

Next Catalyst: Update on DFS and project financing.

Euro Manganese (ASX:EMN)

Share Held: 1,490,000

EMN did not release a quarterly report this week because EMN is on a different reporting cycle in line with its Canadian listing.

The company is in quiet execution mode as it works hard to secure financing and customer offtake agreements for its manganese processing plant in Europe.

The big news for this quarter was that EMN’s Demonstration Plant’s product reached 99.9% Mn purity, which is an important step towards getting EMN in EV batteries

Next Catalyst: Customer offtake agreements / Front End Engineering Design

Elixir Energy (ASX:EXR)

Cash: $11.7M

Shares Held: 2,795,000

The highlight for the quarter related mostly to EXR’s production testing at its Mongolian gas project. EXR flared gas and produced gas at rates in excess of other producing coal bed methane gas projects in China/Mongolia. See our most recent take on this here.

EXR also executed a term sheet with SoftBank Energy to progress its green hydrogen project in Mongolia.

EXR is also gearing up to drill its Daydream-2 well at its QLD gas project later this year - see our latest note on the QLD gas project here.

Next Catalyst: Drill the Daydream-2 well at its QLD gas project

Evolution Energy Minerals (ASX:EV1)

Cash: $6.8M

Share Held: 3,353,000

EV1 delivered an updated Definitive Feasibility Study (DFS) for its graphite project and signed a Framework Agreement with the Tanzanian government.

The key stats from the DFS were as follows:

- Net Present Value (NPV) = US$338M

- Internal Rate Of Return (IRR) = 32%

- CAPEX = US$120M.

- Payback Period = 3.3 years.

Both of these are key hurdles ahead of the major catalyst that we are waiting for: a Final Investment Decision (FID) that would signal a commitment to developing EV1’s project.

To see what we want to see next from EV1 check out our most recent note here.

Next Catalyst: Project funding / updates to downstream graphite processing

FYI Resources (ASX:FYI)

Cash: $9.1M

Shares Held: 1,097,000

The big event for FYI this quarter came in February when Alcoa of Australia withdrew from its Joint Venture Development agreement with FYI on its advanced High Purity Alumina (HPA) project.

As a result, FYI regained 100% of the HPA project, so is fully in control of its development destiny while benefitting from the advances and IP made in conjunction with Alcoa over the past ~2 years.

FYI has a sizeable cash balance, but will need to raise substantial capital, or find alternative funding, in order to progress the HPA Project through to the next key milestone - construction of a demonstration plant.

FYI has made a good start: the latest small scale production run delivered a 15% increase in total product output, thereby demonstrating improvements in process efficiencies and product recovery.

The output and samples will now be used for targeted product marketing to potential customers.

Next Catalyst: Project FEED and financing on HPA Project demo plant

Galileo Mining (ASX:GAL)

Cash: $17.4M

Shares Held: 2,161,544

GAL’s focus for the March quarter was the RC and diamond drill programs at its Calisto discovery.

Over the quarter GAL completed ~ 3,360 metres of RC drilling and 2,650 metres of diamond drilling.

A highlight from the drill program came from GAL’s latest batch of assay results which delivered the thickest intercept at its discovery to date - to see our take on that news click here.

Next Catalyst: Results from step-out drilling at its Calisto discovery.

Grand Gulf Energy (ASX:GGE)

Cash: $5.6M

Shares Held: 25,011,058

During the quarter GGE completed its major drill program for the year (Jesse-2).

Whilst the well allowed GGE to learn a lot more about the reservoir it was testing, the main objective for the well (a flow rate) was not achieved.

Following the drill results the company’s share price is down over 50% with GGE trading at 1.3c per share.

We covered that news with a note earlier this week which you can see here.

Regarding GGE’s cash balance, the company did lock away a small raise of $2.5M at 2.1c per share before the drill results which is a positive (in hindsight).

We expect the company’s cash balance to come down over this quarter with the costs of Jesse-2 likely to be settled in the June quarter.

Next Catalyst: Detailed timeline for drilling Jesse-3 well.

GTI Energy (ASX: GTR)

Cash: $3.4M (rights issue being completed to raise another $1.3M)

Shares Held: 16,662,000

The $3.4M cash balance for GTR doesn't include the $1.3M the company will be receiving from a fully underwritten rights issue - GTR should therefore have ~$4.7M in cash.

GTR expects the underwritten shares from the rights issue to be allocated by the 17th of May.

During the quarter GTR delivered a maiden JORC resource across the first of its Wyoming uranium projects - see our take on that news here.

Next Catalyst: Maiden JORC resource at its Lo Herma project where the company just completed the acquisition of US$15M in drilling data - see our take on what’s next here.

Iron Road (ASX:IRD)

Cash: $0.7M (+$1.5M received subsequent to the quarter’s end)

Shares Held: 1,402,907

It has been relatively quiet at IRD as it seeks a strategic partner to help develop its development-ready, large high-grade iron ore project in South Australia.

However, the company did make progress with its Cape Hardy port asset, which offers part of the logistical solution for its iron ore project.

Recently, IRD announced its selection of renewable energy group Amp Energy (Amp) of Canada as lead developer for its Cape Hardy Green Hydrogen project. They have entered a Strategic Framework Agreement to develop the proposed 5GW project, with a nine-month exclusivity period provided for Amp.

Under the terms of the agreement, IRD has received an upfront ‘exclusivity fee’ payment of $1.5M.

Amp pays a further $1.5M upon execution of detailed transaction documents at the end of the exclusivity period. IRD can receive up to a further $21M in staged payments through to first green hydrogen / ammonia production, after which a perpetual royalty stream would kick in.

Next Catalyst: Complete sale of Cape Hardy port asset.

Invictus Energy (ASX: IVZ)

Cash: $3.3M ($10M raised after the quarter ended - total cash ~$13.3M)

Shares Held: 4,025,435

IVZ recently completed a $10M placement at 12c per share, adding to its $3.3M cash balance. IVZ has also promised to raise some more via a share purchase plan open to all shareholders.

IVZ also laid out a timeline for the drilling of Mukuyu-2 which it expects to be in Q3-2023. See our take on what’s next for IVZ here.

We will also be releasing a new IVZ Investment Memo in the lead-up to drilling so be on the lookout for this over the coming weeks.

Next Catalyst: Drilling Mukuyu-2 (Q3)

Kuniko (ASX:KNI)

Cash: $4.0M

Shares Held: 2,582,223

The focus for the quarter was the three drill programs KNI ran across its Norwegian battery metals projects.

All three drill programs are now complete and so the next stage is waiting to see what comes up in the assay results.

During the quarter, KNI added lithium projects in the James Bay region in Canada to its portfolio. We covered that news in a recent KNI note here.

This week KNI delivered some unexpected high grade, shallow cobalt intercept - its biggest hit yet and more assays still to come - read more here

Next Catalyst: Assay results from the company's three drill programs in Norway.

Lanthanein Resources (ASX:LNR)

Cash: $5.28M

Shares Held: 22,323,582

During the quarter, LNR completed fieldwork and heritage surveys across its rare earths project in WA.

Next LNR is gearing up to run a 10,000m drill program split across ironstone/carbonatite targets - the same type of rocks that host both Hastings Technology Metals and Dreadnought Resources discoveries.

LNR expects drilling to start this quarter - to see our take on the upcoming drill programs and what we want to see LNR achieve in our latest note here.

Next Catalyst: Drilling to start at its Gascoyne rare earths project.

Latin Resources (ASX: LRS)

Cash: $21.032M (+$37.1M raised in April, total: $58.132M)

Shares Held: 4,335,000

Post quarter-end, LRS completed a $37.1M capital raise at 10.5c per share.

After the cap raise LRS should now have ~$58M cash on hand which is a sizeable amount of cash especially given its market cap of $341M.

The highlights from the raise was that LRS managed to bank a large amount of cash at basically no discount to its market price (LRS was trading at 11c per share before the raise).

On top of this, LRS’s share price has rallied since the raise with investors who would have been waiting to enter in the next funding round now forced to build positions on market.

Well played by LRS in an otherwise tough environment for companies looking to raise capital.

LRS has more than eight drill rigs on site as it finished ~65,000m of drilling in the lead up to an upgrade to its JORC resource and a feasibility study.

LRS is looking to follow in the footsteps of its $5.5BN-capped neighbour Sigma Lithium which progressed its project (also in Brazil) from a similar stage as LRS’s and is now about to start production.

Ultimately we hope LRS can do the same thing in the long run.

Next Catalyst: Upgraded JORC lithium resource

Los Cerros (ASX: LCL)

Cash: $8.7M

Shares Held: 9,755,814

Having raised $2.2M during the quarter via a rights issue to existing shareholders, LCL had $8.7M cash at bank at 31 March.

This is more than enough to fund the planned drilling programs at its new Papua New Guinea projects this year, including its currently underway 3,000m of drilling at the Kusi target. After Kusi, LCL intends to drill test the Veri Veri project where creek boulders of massive nickel sulphides assayed up to 45.8% nickel.

However, the company has multiple more compelling targets across its 3,867km2 of exploration claims that it wants to advance concurrently. To do so, LCL is seeking joint venture partners while directing its own capital to drilling at the primary targets at Kusi and Veri Veri.

Next Catalyst: More assays at PNG Copper-Gold project

Lycaon Resources (ASX:LYN)

Cash: $2.7M

Shares Held: 2,631,250

LYN has been one of the companies in our Portfolio whose share price has slowly come down despite the company building toward major catalysts.

LYN has drill programs planned at its nickel-copper-PGE projects in WA this quarter, and is also working on approvals to drill its niobium-rare earths target.

Despite the progress toward two major drill programs, LYN trades with a market cap of $5.3M and has $2.7M cash in the bank, giving it an Enterprise Value (EV) of just $2.6M.

Next Catalyst: drill programs planned at its nickel-copper-PGE projects in WA

Mandrake Resources (ASX:MAN)

Cash: $18.3M

Shares Held: 3,150,000

Perhaps one of the strongest cash balances (relative to market cap) of our Portfolio companies, MAN had $18.3M in cash at the end of the March quarter.

During the quarter MAN organically originated its lithium project in the USA (Utah). We like this approach because it means MAN didn't need to pay anyone for the projects.

Since first announcing the new project MAN has already staked additional ground, increasing the project area by ~50%.

With the project attracting a 5.85% cornerstone investment from $328M Galan Lithium we are looking forward to MAN developing the project from the ground up.

For now, the project is still in its relatively early stages - check out our first note on the new project here.

Next Catalyst: Exploration target for US lithium project

Megado Minerals (ASX:MEG)

Cash: $328K

Shares Held: 9,740,545

MEG ended the quarter with a relatively low cash balance, BUT this doesn’t include the $2.7M capital raise the company completed post-acquisition of its new James Bay lithium project in Canada.

MEG completed the acquisition and capital raise, with shares issued earlier this week.

MEG also has a rare earths project in Idaho, USA, that we expect it will drill before the James Bay project.

Next Catalyst: Ground reconnaissance work at James Bay to build up drill targets.

Minbos Resources (ASX: MNB)

Cash: $12.32M

Shares Held: 8,645,000

MNB was active this quarter with the equipment for its Phosphate Plant arriving in Angola.

The company updated the market on the plant optimisation and flowsheet work, resulting in a material reduction in CAPEX.

Offtake discussions are continuing for MNB’s fertiliser and the remaining funding of ~US$30M is currently being pursued.

On the Green Ammonia front the company announced the results of a technical study with a timeframe on a PFS to be announced in the coming weeks.

We visited MNB’s site this quarter which you can read about here: On the Ground in Angola: Our MNB Site Visit.

Next Catalyst: Offtake deal / project financing / construction started (Phosphate Project), PFS commenced (Ammonia Project)

Noble Helium (ASX:NHE)

Cash: $3M

Shares Held: 4,166,307

NHE had a relatively big quarter in which it completed seismic surveys, secured a drill rig and progressed farm out discussions for its helium project in Tanzania.

NHE expects to be drilling two wells at its project, targeting a combined ~16.5bcf (billion cubic feet) of helium in Q3 2023.

Next Catalyst: Between now and the drilling in Q3 we expect financing of the well to be a major catalyst for NHE.

Okapi Resources (ASX:OKR)

Cash: $2.7M

Shares Held: 2,633,352

OKR’s March quarter marked a turning point for the company with the completion of its investment for a material stake in uranium enrichment technology company ‘Ubaryon’.

OKR paid $3.1M for its 19.9% position in Ubaryon — a key reason for its relatively high cash burn in the quarter.

Next Catalyst: Airborne Geophysics results from Canadian uranium projects

Oneview Healthcare (ASX:ONE)

Cash: $7.04M

Shares Held: 7,965,000

Our healthtech Investment and 2021 Tech Pick of the Year, Oneview Healthcare (ASX:ONE) exceeded our #1 Objective for the company when it released its quarterly report on Friday.

Over the quarter, ONE added three more hospitals as long term clients:

- Catholic Health (the big one signed today, 800 beds, 5 year contract)

- University of Miami Health System (81 beds, 5 year contract)

- Adeney Private Hospital (42 rooms, 5 year contract)

Plus, there are another four hospitals in “late-stage contract negotiation” which could add up to 3,000 more beds — tacking on ~20% more total contracted beds to ONE.

This sales momentum comes at a very good time, as positive broader tech sentiment lifted in recent weeks following a negative 2022 for all things tech.

📰 See our full Note: ONE delivers on 15,000 contracted beds milestone

Next Catalyst: More contracts announced, hopefully big ones.

Panterra Minerals (ASX:PFE)

Cash: $3.1M

Shares Held: 2,410,000

This quarter was all about the manganese for PFE.

The company announced the results of its first round of drilling 45km from Element 25’s 263Mt manganese resource in WA.

The results sat within our “base case” expectations for drilling. PFE has since returned to finish the drilling program at the other three areas of manganese outcropping last week.

Next, we anticipate drilling to be completed early next month and hope to see some visual results announced, with assays due in Q3, and with $3M in the bank, we think PFE is in a strong position to re-rate off strong drill results.

Read our expectations for the drilling program here: Drilling underway at WA manganese project

Next Catalyst: Manganese drilling results (Q3)

Province Resources (ASX: PRL)

Cash: $16.5M

Shares Held: 20,402,926

During the quarter the partnership with Total Eren was terminated - we covered that news here.

PRL is now suspended from trading until the company completes a Pre Feasibility Study (PFS) for its Green Hydrogen project as the company re-complies with the ASX listing rules.

The ASX has a rule that a company’s main undertaking needs to match the nature of its activities and expenditure.

Given the HyEnergy project is PRL’s main undertaking, but PRL is still classified as a “resource exploration “ company, PRL now needs to “re-comply with the ASX listing rules”.

This is fairly common when the nature of a company's business changes, and usually takes a couple of months.

The company expects to come out of suspension when the PFS is completed around July 2023.

Next Catalyst: PFS completion for its green hydrogen project.

Pursuit Minerals (ASX:PUR)

Cash: $4M

Shares Held: 18,915,999

During the quarter PUR completed the acquisition of its Argentinian lithium project which sits inside the lithium triangle in South America.

PUR expects exploration programs on the project to start in May.

Next Catalyst: First pass exploration work to commence.

Ragusa Minerals (ASX: RAS)

Cash: $2.35M

Shares Held: 990,000

This was another quarterly that surprised us.

We expected RAS’s cash balance to come down significantly after last year’s drill program.

To the contrary, RAS retained a relatively high cash balance of $2.35M for a micro cap stock.

Up next for RAS are the results from a small drill program at its NT lithium project - see our take on what we want to see from that program here.

Next Catalyst: Results from NT lithium drill program.

Sarytogan Graphite (ASX:SGA)

Cash: $4.2M (+ $5M raised in April, Total: $9.2M)

Shares Held: 4,354,500

SGA just recently raised $5M via a placement at 33c per share. SGA should now have ~$9.2M in cash as it pushes toward completing its Pre-Feasibility Study (PFS) for its graphite project in Kazakhstan.

The big news for the quarter was the upgraded JORC resource which exceeded even our bull case expectations - see our coverage of that news here.

Next Catalyst: Metwork updates to produce (battery grade) 99.95%+ graphite purity

TechGen Metals (ASX:TG1)

Cash: $1.5M

Shares Held: 2,331,081

TG1 is gearing up for a drill program at its NSW gold project this quarter, and should have enough in the bank to do it.

The highlight from the quarterly was the soil sampling results which hit gold grades as high as ~10g/t.

Going into the drill program we put out an updated TG1 Investment Memo which you can read here.

Next Catalyst: Drilling commencing at NSW gold project

Tempus Resources (ASX: TMR)

Cash: $280K

Shares Held: 8,148,000

During the March quarter, TMR received all of the assays from its 2022 drill program — a total of ~40 holes.

With all of the assay results in TMR continued to work toward delivering a maiden JORC compliant gold resource estimate for its Canadian gold project.

TMR expects the updated resource estimate to be released in the current quarter.

We are excited about TMR’s upcoming JORC resource and 2023 drill program, but the market is punishing the share price due to TMR's low cash balance and anticipation of a cap raise.

On a more positive note - the gold price is having a solid run.

Next Catalyst: Maiden JORC resource estimate.

The Original Juice Co. (ASX:OJC)

Cash: $1.4M

Shares Held: 1,810,715

The Original Juice Co (ASX:OJC), formerly The Food Revolution Group (ASX:FOD) changed its name and stock ticker this quarter, and conducted a 4:1 share consolidation.

The company was operating cash flow positive for the quarter with gross revenue up YoY by 19% - a strong result.

OJC’s brands performed well, with the Juice Lab range capturing 79% of market share in supermarkets.

The company is at the final stage of tender for export juices, which are expected “to be announced to market in the first week of May”.

Next Catalyst: Export deal / increase product distribution

Top End Energy (ASX:TEE)

Cash: $4.0M

Shares Held: 3,725,000

The big news this quarter was the native title approvals for the company’s priority permits near the Beetaloo Basin in the Northern Territory - we covered that news here.

Next Catalyst: We are waiting for TEE to receive its exploration permit so the company can start exploration work.

Titan Minerals (ASX: TTM)

Cash: US$193K

Shares Held: 3,899,250

TTM delivered some relatively strong drill results from its Copper Ridge project with intercepts measuring up to 186m with grades up to ~0.5% copper equivalent.

This wasn't enough to send the company’s share price higher - we suspect that was because of TTM's low cash balance it looks like the company will need to raise capital soon.

With a loan facility due in May, and only US$193K in cash, the next major bit of news we want to see is some sort of financing locked away for TTM.

The silver lining is that TTM has looming cash to come from asset sales including US$1.05M from its recent sale of the Jerusalen Project and US$2.5M from the Zaruma Project.

Next Catalyst: Results from drilling at the Dynasty gold project and a capital raise.

Tyranna Resources (ASX:TYX)

Cash: $910K

Shares Held: 37,950,000

TYX just went into a trading halt earlier this week pending “an announcement regarding a “material funding transaction”.

We note that these types of trading halts would usually say “pending a capital raise,” so it will be interesting to see what type of funding agreement TYX has locked away.

After the last drill campaign finished, the market was expecting a TYX cap raise, so there was a lot of selling pressure likely in anticipation of a discounted capital raise, so it will be interesting to see more details on this “material funding transaction”.

Whatever comes from the announcement we will cover it with a note so be on the lookout for this.

Next Catalyst: Funding for next drilling campaign at Angolan lithium project

Vonex (ASX:VN8)

Shares Held: 3,273,182

VN8 did not release a quarterly report this week because the company has elected to report on a half-yearly cycle, which is a benefit enjoyed for operating cash flow positive for more than 4 quarters.

Next Catalyst: Revenue growth and acquisition integration

Vulcan Energy Resources (ASX: VUL)

Cash: €112M (A$186M)

Shares Held: 118,650

The big news for the quarter was the phase one Definitive Feasibility Study (DFS) which delivered a 250% increase in estimated Net Present Value (NPV) relative to the Pre-Feasibility Study from 2021.

The key stats from the study are as follows:

- NPV of €3.9BN (pre-tax)

- Internal Rate of Return (IRR) of 34% (pre-tax)

- CAPEX of €1.5BN

- Capital payback of 3.5 years

Just last week VUL signed a term sheet with Nobian GmbH to form a 50/50 joint venture over VUL’s Central Lithium Plant (CLP).

Under the deal Nobian would contribute ~€161M (approximately A$265M) toward building the plant, with VUL expecting to finance its 50% of the project through debt facilities.

Next Catalyst: Continue to secure financing for project development

Whitehawk (ASX:WHK)

Cash: US$1.02M (~A$1.54M)

Shares Held: 6,828,547

WHK’s contract signings are usually relatively big for a technology company, which leads to lumpy revenue and cash flow.

WHK reported receipts from customers of US$25,000 for the quarter, but it invoiced US$879K during the quarter, with US$446K in receivables due at the quarter end on 31 March.

WHK has multiple new potential contracts and contract extensions in the pipeline that we hope can be converted to revenues.

Many of these are with large, slow-moving US federal government departments and multinational companies so take time to get locked away.

WHK also continues to develop its sales pipeline and partnerships with consulting groups, and major industry leaders the likes of Amazon Web Services, Peraton, and Dun & Bradstreet.

Next Catalyst: Contract announcements

That ends the summary of all our current Investments

If there is another company that we have covered in the past but is not featured here it may have been moved to our “bottom drawer Portfolio”.

You can also check our holdings on all companies at any time here

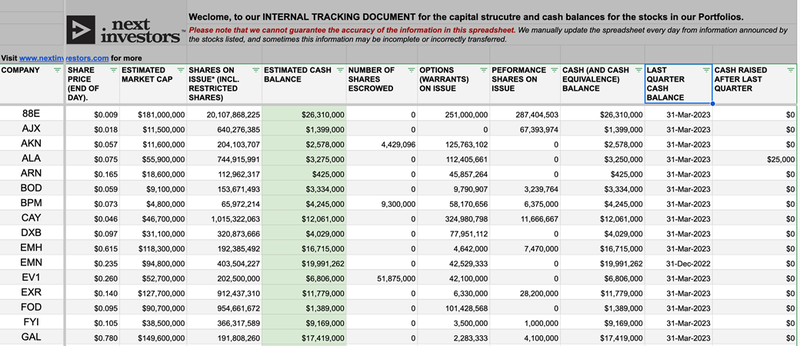

Check out our Capital Structure document

With the quarterlies coming out, we have updated our “Capital Structure” doc with the latest company cash balances and shares on issue.

We’ve already covered why it’s important to track a company's cash balance, BUT It’s also important to track the “shares on issue” of each company to keep an eye on the ongoing levels of dilution.

Click here OR on the image below to see the spreadsheet.

This week’s Quick Takes 🗣️

LNR: Rare earths drilling to start in coming days

GTR: Second US based JORC uranium resource this quarter

NHE: String of Pearls: two leads become one larger lead

New Educational 🎓

How to read assays and drilling results for beginners

Macro News - What we are reading 📰

Battery materials

Trudeau suggests China uses slave labour in lithium production

European automakers demand South32’s higher-cost ‘green aluminium’

Copper

Gold

Central banks bought the most gold on record last year, WGC says

Lithium

Elon Musk urges entrepreneurs 'please refine lithium' as EVs face choke point

Australian lithium sector can win from Chile’s own goal

This week in our Portfolios 🧬 🦉 🏹

Kuniko (ASX:KNI)

On Monday, our European and North American critical minerals Investment, Kuniko (ASX:KNI) “accidentally” stumbled on a high grade zone of cobalt mineralisation much closer to the surface than expected

This result now warrants further exploration to see just how big it is...and to test if similar high-grade, near-to-surface zones exist nearby.

The result suggests that KNI is well on track to exceed our bull case drilling expectations for this project, as outlined in our KNI Investment Memo back in January.

Our view is that this result dramatically upgrades the potential viability of KNI’s Norwegian cobalt project, as it aims to eventually establish an ethical, domestic source of cobalt for the EU.

📰 See our full Note: KNI delivers unexpected high grade, shallow intercept - biggest hit yet

Grand Gulf Energy (ASX:GGE)

Our US helium Investment, Grand Gulf Energy (ASX:GGE 🇦🇺 | OTC:GRGUF 🇺🇸) finished its 2023 drill program.

GGE announced the results of its second helium well, which was drilled taking into account lessons learnt from its discovery well it drilled last year.

The market was hoping that this well would deliver a commercially viable helium flow rate - enough to allow GGE to hook it into existing helium processing infrastructure nearby.

The well flowed helium to surface, recording high concentrations of up to 0.9% helium, and it extended GGE’s proven helium system by ~1.5 miles from its first discovery.

Whilst a flow rate was recorded — a maximum of 0.03 mmcf/day — this was not enough to warrant an immediate move into development and production. This may change in the future with more stimulation work on the well to increase the flow rate.

On the next well, Jesse-3, GGE will hopefully finally hit the reservoir in the sweet spot to deliver enough of a flow rate such that it makes commercial sense to plug it into the existing processing infrastructure... and start generating cash flow.

📰 See our full Note: GGE extends helium discovery - but not a commercial reservoir... yet

Techgen Metals (ASX:TG1)

Our microcap explorer Techgen Metals (ASX:TG1) is just a few weeks away from drill testing a theory that the company’s gold discovery last year is just the “tip of the iceberg”..

We’ll soon see whether this microcap company’s discovery has serious size/scale potential.

Now with the gold price back up near record highs, we think that the stars may align for TG1 if it can deliver on its intrusive theory with some strong drill results.

We also put out our NEW TG1 Investment Memo where you can find:

- Why we are Invested in TG1

- Our long term bet - what we think is the upside Investment case for TG1

- The key objectives we want to see TG1 achieve over the next 12 months

- The key risks to our Investment thesis

- Our Investment Plan

📰 See our full Note: What we want to see from gold explorer TG1 over the next 12 months

Los Cerros (ASX:LCL)

With gold explorers potentially about to swing back into investor favour, our gold Investment Los Cerros (ASX:LCL) could be drilling at just the right time.

LCL is currently drilling a 18 hole, 3,000m campaign to determine the extent of the gold mineralisation that’s already been encountered at one of its new projects in Papua New Guinea.

LCL this week reported high grade results from its first drill hole. So far, so good.

This first diamond drill hole returned a 15.2m intersection grading 4.45g/t gold (from 138.2m deep), which sat within a broader interval of 76.4m grading 1.34g/t gold (from 106.9m).

The first drill hole confirms LCL’s theory that its gold mineralisation is continuous... and it could well be widespread.

PNG is one of the few regions on the planet that can still deliver new, big, high grade gold discoveries.

📰 See our full Note: LCL hits high grade gold on first hole - 17 more to come

Oneview Healthcare (ASX:ONE)

Our healthtech Investment and 2021 Tech Pick of the Year, Oneview Healthcare (ASX:ONE) exceeded our #1 Objective for the company when it released its quarterly report on Friday.

Over the quarter, ONE added three more hospitals as long term clients:

- Catholic Health (the big one signed today, 800 beds, 5 year contract)

- University of Miami Health System (81 beds, 5 year contract)

- Adeney Private Hospital (42 rooms, 5 year contract)

Plus, there are another four hospitals in “late-stage contract negotiation” which could add up to 3,000 more beds — tacking on ~20% more total contracted beds to ONE.

This sales momentum comes at a very good time, as positive broader tech sentiment lifted in recent weeks following a negative 2022 for all things tech.

📰 See our full Note: ONE delivers on 15,000 contracted beds milestone

⏲️ Upcoming potential share price catalysts

Updates this week:

- GGE: Drilling its US helium project looking for a commercially viable flow rate.

- GGE put out drill results from its Jesse-2 well, while the news fundamentally improved its helium projects potential, GGE didnt manage to deliver a commercially viable flow rate. See our take on the news here.

- KNI: Drilling 3/3 of its Norwegian battery metals projects in Europe.

- KNI hit shallow, high grade cobalt mineralisation at its Skuterud cobalt project in Norway. See our take on the news here.

- LCL: Maiden drilling underway at primary PNG copper-gold target.

- LCL released the first batch of assays from its drill program delivering high grade gold - as expected. See our take on the news here.

- TG1: Drilling at its NSW gold project in May.

- No news from TG1 this week but we put out an updated TG1 Investment Memo where we laid out what we wanted to see the company do over the next 12 months. See our NEW TG1 Investment Memo here.

No material news this week:

- NHE: Scheduled to drill two targets at its helium project in Tanzania (Q3 2023).

- TTM: Drilling campaign at flagship Dynasty gold project.

- LNR: >10,000m drill program at rare earths project in WA.

- GTR: Maiden resource estimates across two of its uranium projects in Wyoming, USA.

- IVZ: Drilling oil & gas target in Zimbabwe, Myuku-2 (Q3, 2023).

- DXB: Interim Analysis of Phase III Clinical Trial on FSGS (Q4 2023).

- GAL: Drilling at its Callisto PGE discovery in WA.

- TMR: Maiden JORC resource estimate for its Canadian gold project.

- BOD: Phase III clinical trial for CBD insomnia treatment.

Have a great weekend,

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.