PRL and Total Eren Split. What happens next for PRL?

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 20,402,926 PRL shares, and the Company’s staff own 200,000 PRL shares at the time of publishing this article. The Company has been engaged by PRL to share our commentary on the progress of our Investment in PRL over time.

Hydrogen is being touted as the ‘next generation gas’ and a potential solution to net zero emissions targets set by governments around the world.

Over the last three years, there’s been a groundswell of new and proposed projects, and billions of dollars of capital pouring into green hydrogen.

Australia does not want to be left behind.

Our 2021 Small Cap Pick of the Year Province Resources (ASX:PRL) is on an ambitious pathway to generate 550,000 tonnes of green hydrogen per year from solar and wind power generated in Western Australia.

This could be worth billions of dollars a year in clean energy generation.

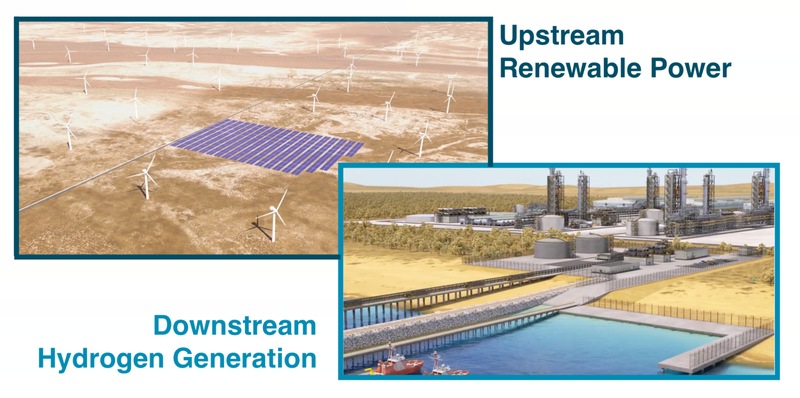

Green hydrogen is created by “electrolyzing” water using clean energy. This clean energy can be generated by wind, solar or hydro.

A big green hydrogen project like PRL’s requires large upfront CAPEX to build the clean energy supply, plus community, government, stakeholder approvals to build it.

PRL has been leading the charge on securing all required stakeholder approvals and permits needed to develop this project.

In April 2021 we named PRL as our Small Cap Pick of the Year on the back of an MoU signed with Total Eren to fund the upstream power generation and lead the build of the project. Total Eren is partly owned by the A$240BN French oil major Total SA.

The market also liked this news and the PRL share price reflected it.

A little under a year later, PRL completed a Scoping Study and then signed a binding term sheet with Total Eren to give it time to execute a 50/50 JV over the project.

Earlier this week, the six month deadline for that term sheet came around and PRL announced that a JV with Total Eren will not be entered into.

While this news was disappointing for long term PRL holders like us, it’s the kind of risk that can and does materialise in small cap investing.

The day the news broke, PRL updated investors on a conference call giving some more details on Total Eren’s departure and the forward plan for PRL.

Our key takeaways were that PRL felt that Total Eren was moving too slowly and that there are various other interested parties that can be engaged when the exclusivity clause in the Total Eren MoU expires on April 17th.

With PRL now back to 100% ownership of the project, we expect the company to move more quickly in progressing its green hydrogen project.

PRL had already attracted interest from a major partner in Total Eren, so we are confident that it can do it again with other potential partners. This time with a more advanced project, and including lessons learned on adding protections against slow partner movement.

On the back of this week's news that the PRL and Total Eren Joint Venture will not be proceeding, today we will share our updated PRL Investment Memo on what we want to see from PRL over the next 12 months.

We will also share our assessment of how PRL performed against our initial Investment Memo, including our retrospective commentary on each of our original reasons for Investing, objectives we wanted to see, potential risks and execution of our Investment plan.

But first, Here are the key points from the PRL investor call:

- For now PRL is back to 100% ownership and control - PRL is back to 100% ownership over the HyEnergy project and will move forward with feasibility studies without Total Eren.

- Other parties are interested - PRL has previously been approached by other interested third parties, but couldn't explore that interest because of exclusivity in the Total deal.

- Exclusivity with Total expires on 17th April - PRL can start talking to other parties after 17 April 2023 when the exclusivity arrangement with Total Eren expires. This ‘coming out of exclusivity’ date may be a share price catalyst in its own right.

- Clear timelines established - PRL expects to deliver Pre Feasibility Studies (PFS) on BOTH the upstream and downstream components of its project by Q3 2023.

- PRL remains well funded with $17.8M in the bank at Dec 31st - we think this is more than enough cash to see through the completion of the upstream and downstream PFSs. This healthy cash balance gives it time for discussions with potential new partners.

- PRL has made significant progress in aligning stakeholders in the region - PRL has been working closely with all levels of government, native title groups, pastoralists and the local community on this project, and the desire to get this project off the ground is very high. This is a clear advantage compared to any other new entrant into the area.

- PRL retains a strong land tenure position in the Gascoyne region - PRL is advanced in land tenure, with native title agreements and holding Section 91 licences.

On the same day as the Total Eren departure news, PRL released an announcement regarding the appointment of global professional services firm GHD to complete the downstream Pre Feasibility Study (PFS) for its green hydrogen project.

In the conference call, we learned from PRL Managing Director David Frances that the plan is to complete the upstream PFS (renewable energy generation) in parallel with a downstream PFS (green hydrogen generation). A contract award for the upstream component is due soon.

Both are expected to be completed in Q3 2023.

Click here to learn more about feasibility studies.

This is a good example of how PRL can more rapidly advance the project (and communicate progress to shareholders) now that Total Eren is no longer involved.

As a quick reminder, the upstream component of the project is the wind and solar power generation capacity of up to 8GW to feed into the downstream electrolyser capacity of 5.2GW.

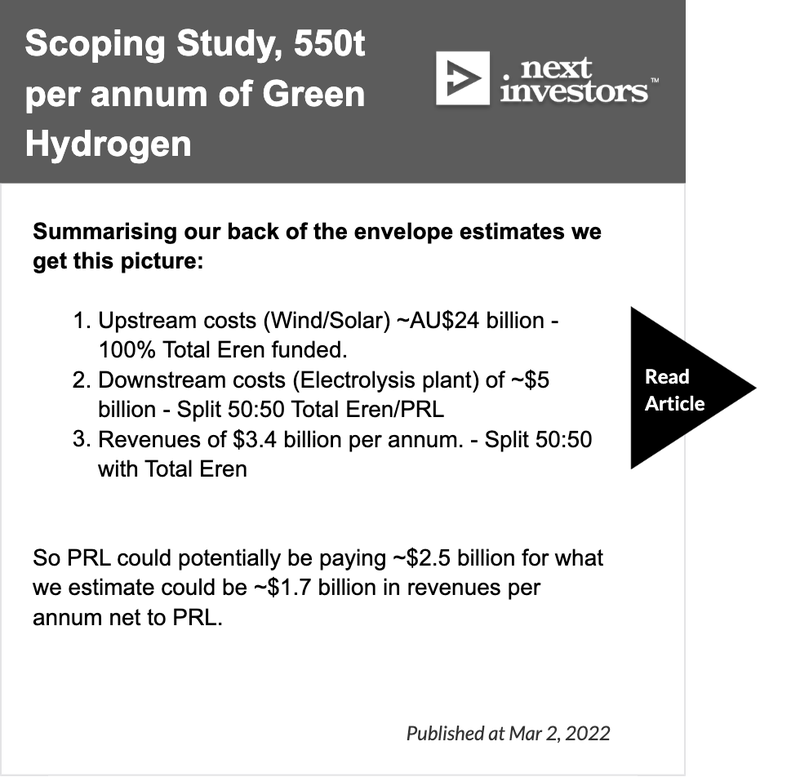

As per the PRL Scoping Study, which we covered in March of last year, the project will produce roughly 550t per annum of green hydrogen (read the article here).

The goal of the PFS work will be to refine PRL’s understanding of how to develop the project and production numbers could change in the PFS.

The electrolyser capacity will split water into green hydrogen — the good news is that electrolyser costs are expected to come down in the coming years.

So the projected cost of the downstream side of PRL’s projects should evolve for the better over time - the initial figures in the scoping study lead us to our own back of the envelope CAPEX calculation of ~$4.9BN coming down to ~$3.2BN.

While the upstream wind and solar power generation CAPEX we placed at roughly ~$24BN.

We want to stress that these are just our rough estimates based on data that other projects have released publicly. We would expect significant changes to our assumptions as PRL advances the project in the coming years.

Here is a summary of our early stage back of the envelope calculations, click through to the article to see the full breakdown:

Without being too precise on the numbers, any way you look at it, a significant amount of capital (in the tens of billions of dollars) is needed to build this project. But, also, a significant amount of revenue could be generated from the project.

As we have said before: this is a large scale project, and it will likely need to attract large scale partners with deep pockets.

There is a big push from major oil and gas companies to move into the renewable energy space as governments put regulations in place to move away from fossil fuels.

Oil majors look at hydrogen as the next potential opportunity for energy prosperity. Those oil majors have the financing muscles to take on a project of the scale PRL is working on.

With the PRL investor conference call revealing the interest of other parties, we expect there to be more concrete newsflow on potential partners from the end of the exclusivity period on 17 April of this year.

Previously, we drew an analogy between PRL’s project and the North West Shelf Project at the advent of the era of natural gas (read the take here).

We think that analogy still holds.

As of 2017, the total investment in the Northwest Shelf Project since the late 1970s stood at $34BN - so projects of the scale PRL is planning are not without precedent.

While on the face of it, it is disappointing news this week, our view is that PRL’s and Total Eren’s split and failure to reach a Joint Venture agreement could now allow room for a new and more committed, faster moving partner to emerge.

The question then is...who might it be.

Our retrospective PRL Investment Memo review:

A large part of our first PRL Investment Memo centred around the company's MOU with Total Eren.

Now that PRL has gone back to 100% ownership of the project and Total Eren is no longer involved, we think this week's news is a trigger for a new PRL Investment Memo.

As part of the new Memo process we have also gone back and done a retrospective review of PRL’s performance against our first Memo. We like to go back and assess our Investments, plus our assumptions and reasons for investing after the fact, as it makes us better investors next time around.

Below we have:

- Our retrospective review of PRL Investment Memo #1 - our evaluation of how PRL performed against our first Investment Memo. Our commentary on the Initial PRL Investment Memo is in red text.

- Our NEW PRL Investment Memo - this will detail what we want to see the company achieve over the next ~ 12 months, why we are still Invested in PRL and the key risks from this point forward.

Our retrospective PRL Investment Memo review:

- Investment Memo: Province Resources (ASX:PRL) - CLOSED

- Shares Held at Open (12-Jan-2022): 24,000,000

- Shares Held at Close (10-Mar-2023): 20,402,926

- Reason Memo Closed: Major catalyst - Total Eren and PRL Joint Venture did not proceed.

What is the macro theme?

Decarbonisation using the latest green hydrogen technology.

As the world looks to cut its greenhouse gas emissions, green hydrogen may prove to be a major building block of a net-zero economy.

Industrial applications and large transport (like buses and trucks), and heavy industry applications like steel mills are the most likely candidates to start using this technology in the near future.

[Sentiment = Strong]

If 2021 was the year when green hydrogen was announced as a potential fuel of the future, 2022 was the year that governments put into place the mechanisms to make it happen.

In 2022, 680 large-scale hydrogen project proposals (equivalent to US$240BN in direct investment through 2030) have been put forward - with around 10% reaching final investment decisions in that year.

The Australian government has indicated that hydrogen will play a major role in Australia’s energy mix and a key part of achieving net zero emissions by 2050, while in the US, the government has provided attractive tax credits to encourage green hydrogen production.

Why did we invest in PRL?

Ideal location for the project

PRL's project is located in the Gascoyne region of WA, next to the town of Carnarvon. Gascoyne is a particularly sunny and windy area (ideal for green energy support) and coastal (important to build a hydrogen plant to undertake hydrolysis). The town of Carnarvon also has a gas pipeline.

[Grade - A]

PRL still intends to build the project in the Gascoyne region of WA and has built strong relationships with native title groups and pastoral land owners in the area.

The beneficial conditions for hydrogen production have not changed in the last 12 months.

Australia is aiming for net zero emissions by 2050

With particular targeted investments in hydrogen we think PRL can be part of the solution.

[Grade - A]

With Labour in power and the Greens holding the balance in the Senate there is a strong push from the Australian government towards renewable energy.

However, with cost of living pressures increasing from high energy prices there is an indication that fossil fuels may be around for longer as a bridging fuel.

This gives the Australian government a strong incentive to support the fast development of green hydrogen and renewable energy projects as an alternative fuel source to meet the sustainability goals.

Joint Venture Possibility

PRL has a pathway to financing through their potential joint venture partner Total Eren.

[Grade - F]

PRL is now progressing the HyEnergy project without Total Eren.

This makes the pathway to financing less certain, as the company will need to find a new JV to support the upstream, renewable energy, part of its project.

However, the partnership with Total Eren did open some significant doors for the company, establishing its credibility as a serious player in the green hydrogen space in Australia.

This set the tone for the project as one of critical importance to the hydrogen industry in WA. PRL continues to maintain a strong relationship with the WA government even after Total Eren’s departure.

An Experienced Team

Project set up by the people behind Vulcan Energy Resources (one of our most successful investments)

[Grade - Unchanged]

What do we expect PRL to deliver?

Objective #1: Scoping study

Deliver scoping study to better determine the commerciality of PRL’s project.

[Grade - A]

PRL delivered a Scoping Study in March 2022 which proposes to generate 550,000 tonnes of renewable-based hydrogen per year.

We provided a deep dive look at the scoping study here: https://nextinvestors.com/articles/prl-announces-scoping-study-550t-annum-green-hydrogen/

Objective #2: Secure key stakeholder support

Secure land tenure and key stakeholder support for the project, including a Heritage Agreement, Environmental Impact Assessment and other necessary permits so that the project can proceed.

[Grade - A]

PRL secured key tenure agreements including Section 91 and agreements with pastoral land owners over the project area.

While PRL waits for the WA government to provide more certainty on the “diversification leases” these are the best options that PRL has to secure tenure over the project.

These agreements are effectively PRL’s “moat” for the project and for the region and come from multiple years of community engagement.

Objective #3: Begin Pre-Feasibility Study (PFS)

With a Scoping Study, land tenure and stakeholder support, the start of the PFS would enable PRL to get to work on understanding the specific factors needed in development to deliver an economic green hydrogen project in WA.

[Grade - A]

Once PRL secured the section 91 land access agreements it could access the project area and start collecting valuable data for the PFS.

With Total Eren now out of the picture, the company has hired global professional services firm GHD to complete a downstream PFS which is expected to be finished in Q3 2023.

We also expect the upstream PFS contract to be awarded soon with both studies due for completion in Q3-2023.

Objective #4: Solidify commitment from Total Eren

With PRL announcing the completion of the scoping study on 2nd March 2022, we next want to see PRL solidify its commitment from Total Eren to further develop the project.

[Grade - F]

PRL is now progressing the HyEnergy project without Total Eren.

It's not all doom and gloom though, with a revert to 100% control, and no exclusivity arrangements, we may see more newsflow, quicker progress, and conversations with new partners in the future.

What could go wrong?

Project Development Risk

Total Eren decides that after the Scoping Study has been completed that the project is not economically viable, and as such, chooses to abandon the project.

[Increased]

Although we got the reason wrong here (Total didn’t ”abandon the project because it wasn’t economically viable”) the general risk of the “JV not being entered into” did actually materialise.

After the Scoping Study, Total Eren was happy enough with the project to sign a binding joint venture agreement.

However, PRL decided to develop the project through to the feasibility stages alone.

Without a large organisation backing the project there is a greater risk that PRL will not find a partner to develop the project with, however, the company can now move more nimbly and make decisions quicker to progress the project forward.

Hydrogen Market Risk

Hydrogen is a very new technology, and there are currently limited uses. Hydrogen is not easily transportable, it is extremely flammable and has also not been adopted on a large scale. If the hydrogen market doesn't materialise, PRL may struggle to secure financing for its project - and sell its hydrogen at a commercial scale.

[Unchanged]

There have been some significant advancements in hydrogen technology, in particular with regards to electrolysers.

However, the shipping and storage limitations of liquid hydrogen still remain a big question mark over the industry.

Regulatory Risk

If PRL can't secure the key permits for the project to go ahead (including heritage agreement, environmental impact assessment and the new development permit). This risk is increased for PRL because there are no regulations that exist for hydrogen projects, and governments will need to update laws to fit this emerging market.

[Decreased]

PRL has spent a lot of time securing tenure over the project including section 91 licences and agreements with pastoral land owners.

The Australian government has a strong incentive to make hydrogen work in order to achieve the ambitious net zero emissions targets set, which means that governments are working together with projects to support the hydrogen industry.

What is our investment plan?

PRL is our second biggest holding behind Vulcan Energy Resources (ASX:VUL). PRL has delivered several impressive announcements since February and is up over 500% since we first invested over 12 months ago in August 2020.

After PRL delivered a number of material announcements and rose over 500%, we sold a portion of our holding to recoup our investment outlays.

We intend to hold our position now until the results of the Scoping Study are announced and re-evaluate our investment plan from there.

[Grade - A]

After the Scoping Study was completed and the share price consolidated, we progressively sold down around ~21% of our Total Holdings at a volume weighted average price of ~9.5 cents, Taking some Profit as the company had further partially de-risked the project.

The majority of our PRL position was held in expectation of a re-rate on a joint venture being entered into with Total Eren, but unfortunately the project development risk subsequently materialised, and was reflected in the share price.

Read more about our trading policy here: https://nextinvestors.com/disclosure-policy/

Our NEW PRL Investment Memo:

Today we will be launching our NEW 2023 PRL Investment Memo, where you can find:

- Why we are Invested in PRL

- Our long term bet - what we think the upside Investment case for PRL is.

- The key objectives we want to see PRL achieve over the next 12 months

- The key risks to our Investment thesis

- Our Investment Plan

Click here to see our NEW Investment Memo

Why we are Invested in PRL:

Australia is aiming for net zero emissions by 2050

In 2019 Australia launched its National Hydrogen Strategy with the ultimate view of ensuring Australia remains on a path to be a global hydrogen leader by 2030.

Just like Australia led to global dominance in lithium production, we think Australia could be a global hydrogen superpower in the future with the government committing $526M in funding to build 8 regional hydrogen hubs around the country.

Large scale clean energy project

According to its Scoping Study, PRL intends to produce 550,000 tonnes of green hydrogen annually, with 8GW of renewable energy with around half of the renewable energy generated sold back to the grid.

The scale of the project is such that if the project is successful, it could earn PRL (or a future acquirer) billions of dollars a year in green hydrogen and renewable energy generation.

PRL’s land tenure position and completed Scoping Study means the company’s project is a lot more advanced than industry peers’. This makes PRL’s green hydrogen project more attractive as a development opportunity when capital starts pouring into the hydrogen space.

100% ownership of project

As a small cap company currently with 100% ownership of the project, PRL can progress its projects a lot quicker than a larger company as it has fewer competing priorities. 100% ownership means PRL can commence discussions with potential partners this year, which will be needed for financing capital intensive developments.

What we want to see is for PRL to farm down parts of the project ownership to funding and development partners, and PRL ends up holding a free carried percentage of the total project.

Ideal location for a green hydrogen project

PRL's project is located in the Gascoyne region of WA, next to the town of Carnarvon. The Gascoyne region is a particularly sunny and windy part of the world (ideal for green energy generation) and it's on the coast (important to build a hydrogen plant to undertake hydrolysis). The Dampier to Bunbury gas pipeline runs past the town of Carnarvon.

Strong relationships with stakeholders has led to advanced land tenure position

We think PRL’s local stakeholder relationships give it a three year headstart on any other company looking to develop a giant green hydrogen project.

For the past three years PRL has been working closely with the WA government, native title holders, landowners and the regional government to build its position in the Carnarvon.

We understand all stakeholders are strongly motivated to see this project get into development.

These relationships have solidified PRL’s land tenure position with section 91 licences and native title agreements in place to support the green hydrogen project.

Current strong cash balance

PRL had $17.8M in cash at 31 Dec 2022 and is fully funded to the completion of a Pre Feasibility Study (PFS) on the upstream and downstream components of its project, and likely some runway beyond this. Given the current mood of investors for speculative stocks, we see this as a big advantage for a company of PRL’s size.

Our long term “Big Bet”

“To see PRL progress its green hydrogen project to the point of development or a takeover (whichever comes first) and re-rate to a $500m+ market cap.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved, and it will require a significant amount of luck. There is no guarantee that it will ever come true. Some of these risks we list in our PRL Investment Memo.

What we want to see PRL achieve over the next 12 months

Objective #1: Complete Pre Feasibility Studies (PFS)

We want to see PRL complete a PFS on both the upstream (renewable energy) and downstream (electrolysers) components of its green hydrogen project. PRL expects these to be completed in Q3 2023.

Milestones:

🔄 Completed PFS (Downstream)

🔲 Award contract for upstream PFS

🔲 Completed PFS (Upstream)

Objective #2: Land tenure progress

We want to see PRL make progress on its land tenure position at all levels including native titles, land access agreements and with section 88 leases at the government level.

Milestones:

🔄 Secure more native title agreements

🔄 Secure more land access agreements

🔲 Legislative progress with section 88 government licenses (Diversification Lease).

Objective #3: Secure a new project partner to advance the project

On its most recent investor call PRL said it had “been approached by various parties” but that due to its MOU with Total Eren “were unable to engage or entertain any discussions”. After its exclusivity arrangement with Total Eren expires on 17 April 2023, PRL will be open to explore these expressions of interest. We hope this leads to a new project partner coming on board.

Milestones:

🔲 Secure a new project partner

The key risks to our Investment Thesis:

Funding risk

PRL has not released any project economics to the market yet. However, we previously estimated that PRL’s project could cost around A$29BN for both the upstream renewable power generation and downstream hydrogen production.

These were our own estimates based on other projects of a similar size and nature around the world, and don’t take into account any technological advancements over the coming years.

PRL is a small $46M capped company. To secure the billions of dollars of funding required it will need to find project partners prepared to invest this kind of capital into the project.

PRL can mitigate this risk by finding a larger project partner and progressing its feasibility studies to provide with more certainty the economics of the project.

What we want to see is for PRL to farm down parts of the project ownership to funding and development partners, and PRL ends up holding a free carried percentage of the total project.

The risk is that PRL won’t be able to find and sign on a suitable partner/s.

Land tenure risk

PRL’s project is dependent on multiple stakeholders agreeing to give the company access to a large land footprint.

There is always a risk that one of these parties (native title groups, landowners or government) decide to refuse permits, permits are delayed, or any other regulatory hiccup occurs. This could delay development of the project or, in a worst case scenario, put it at risk entirely.

Green Hydrogen commercialisation risk

While the global hydrogen industry is already operational, green hydrogen projects of the size PRL is planning are still in the feasibility/development stage.

There are question marks still around the economics of shipping green hydrogen for export and limited use cases of the technology for now.

For green hydrogen to be commercially viable for domestic use, there will also need to be big upgrades to pipelines and other infrastructure to get the hydrogen to market.

Market risk (macro)

A market wide sell-off would impact PRL significantly given the company is not producing any revenues and is still a while away from commercialising its project.

If global share markets fall further, investors will look to sell higher risk early stage investments first, like PRL, which could lead to the share price de-rating significantly from current levels.

Our Investment Plan

At the date of this memo we hold 20,402,926 shares in PRL, and it continues to be one of our largest holdings by value (it was our second largest until the recent share price weakness).

We have held a position in PRL for over 2.5 years, and have achieved Free Carry on each Investment and Taken some Profit since the Scoping Study was announced in March last year.

We will hold the current position while PRL works through the objectives set out in this memo, and re-asses in the second half of the year. If the share price materially re-rates on the back of a new JV partner or PFS we may look to sell a further 5% to 10% of the position.

Read more about our trading policy here: https://nextinvestors.com/disclosure-policy/

Who might now be interested in partnering with PRL?

One of the key things we will be looking for in any future PRL partnership arrangements will be experience in bringing large scale, capital intensive projects into production.

Potential partners could include international energy companies, major industrial gas and chemical companies or other international conglomerates.

With the WA government facilitating PRL’s project with its “Lead Agency” status, there could even be an opportunity for this relationship to advance and for PRL to source some level of public funding for the project in the future.

We note that around the world, some of the biggest players in green hydrogen project development are:

- BP - capped at ~US$120BN, BP now has a 40.5% stake in the Australian Renewable Energy Hub (formerly the Australian Renewable Energy Hub)

- Shell - capped at US$181BN via their recently acquired 35% stake in Oman’s green hydrogen project

- Saudi Aramco - the Saudi Arabian oil supermajor (US$1.9 trillion capped) has been exploring green hydrogen projects and Saudi Arabian government has announced its intention to build the world’s largest green hydrogen project

- Air Products - a US$63BN American industrial and chemical which has a JV with Saudi Arabia’s main energy company for their green hydrogen project

- Linde - a US$170BN capped multinational industrial gas and chemical company which has become a leader in hydrogen technology patent filings.

This list is not exhaustive, but it gives a sense of the size of some of the companies that are pursuing green hydrogen projects, and partnerships could vary in size.

And again at this stage, we know that PRL’s exclusivity arrangement ends 17th April of this year.

From that date onwards it is possible that partnership arrangements may emerge from the existing “interested parties” or new parties not currently on PRL’s radar. It might not happen immediately, but it's definitely something we will be watching for.

Green hydrogen news

Below we’ve summarised green hydrogen macro news that we’ve been reading, which explains how the hydrogen macro landscape has evolved recently:

Key takeaways:

- Shell has joined the Green Energy Oman consortium as lead operating partner, taking a 35% stake in the renewable hydrogen project

- 25 GW of solar and wind power (upstream), 14 GW of electrolyzers (downstream) for 1.8 million mt/year of hydrogen

- Follows BP’s acquisition of a 40.5% stake in Australian Renewable Energy Hub (formerly the Australian Renewable Energy Hub), which was completed in December 2022

Key takeaways:

- The Red Sea hydrogen plant is a JV signed in 2020 between US-based Air Products, the Saudi ACWA Power and the Neom company with production slated for 2026

- Target of 650 tonnes of green hydrogen a day (237,250 tonnes per annum)

- In September 2020, Saudi Arabia became the first country to export ammonia to Japan

Key takeaways:

- Total hydrogen demand can reach 600 to 660 million tons by 2050, abating more than 20 percent of global emissions

- Green steel could cost $515 per ton of crude steel -a premium of $45 per ton of carbon by 2030

- More than 680 large-scale projects have been announced around the world representing more than $240 billion in mature investments

- Green hydrogen costs could fall by 50% by 2030

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.