How to read assays and drilling results for beginners

Published 27-APR-2023 10:00 A.M.

|

7 minute read

So, the company that you have just invested in announced some much anticipated drilling results.

This is an exciting time for junior exploration investments and the results can confirm a mineral discovery.

The one problem is that if you don’t know what you’re reading or what to expect then you can be caught in a trap of thinking bad results are great or great results are nothing special.

Usually, people will look at the market reaction to an announcement to tell them whether or not drilling results are good, but this can be a bad idea.

Drilling results always need to be seen within the context of expectations, your expectations, set before the drilling programme.

We have a great article detailing “expectation setting” for drill results which you can read here:

🎓Expectation setting leading up to drilling programs

Before setting expectations however it is important that you are able to read and interpret drilling results within the context of a drilling programme and the company’s overall exploration strategy.

What is a drilling programme?

Mining companies in the “exploration” or “definition” phase of development will undertake drilling programs to either make a new discovery or increase the size of their deposit.

These form a part of the overall exploration strategy of the company.

Drill rigs are used to penetrate the ground and pull out a drilling sample, which are logged by a geologist and taken to the lab to get tested.

Here is a photo of ‘drill cores’ from a drilling programme:

Together, these logs and lab results form the basis of a drilling result for that particular hole.

Drilling results, also known as assays, are reported to the stock market by the company and can move share prices up OR down depending on whether they exceed market expectations or break market expectations.

When these results are announced it is important that you can understand and interpret them within the context of your expectations for the drilling programme.

How to read mining drilling results?

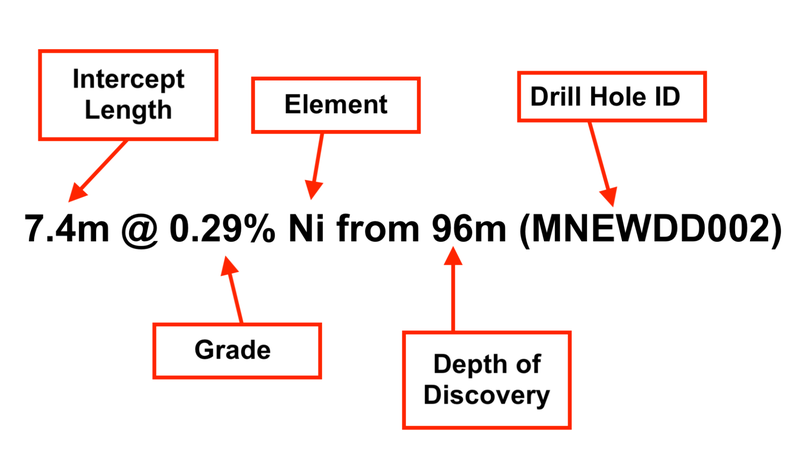

Drill results (also known as assays) are often presented in single sentences like this 7.4m @ 0.29% Ni from 96m (MNEWDD002).

Each datapoint provides a different bit of information about the drill hole.

Using the above intercept as an example:

- 7.4m - This describes the length of mineralisation intercepted

- @0.29% - This describes the grade of mineralisation

- Ni - This is the type of metal intercepted (in this example it is Nickel (Ni).

- From 96m - This refers to the depth at which the mineralisation starts.

- (MNWEDD002) - This refers to the drillhole name (details are in the JORC table).

All of these come together to tell the story of the intercept.

In this case, the company hit 7.4m of nickel mineralisation with an average grade over the intercept of 0.29% from a depth of 96m.

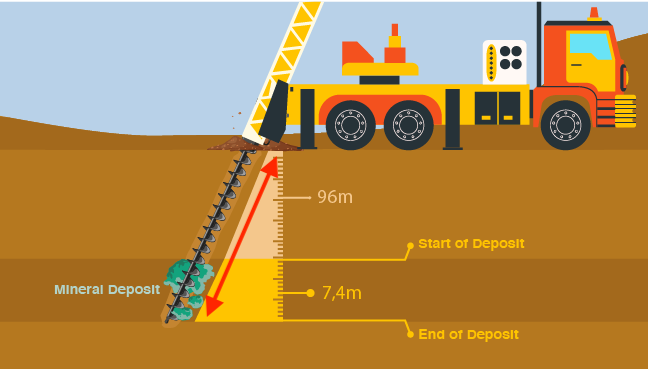

Here is what it looks like in reality:

While it sounds relatively simple, it is important to understand each datapoint in detail.

Why does the length of an intercept matter?

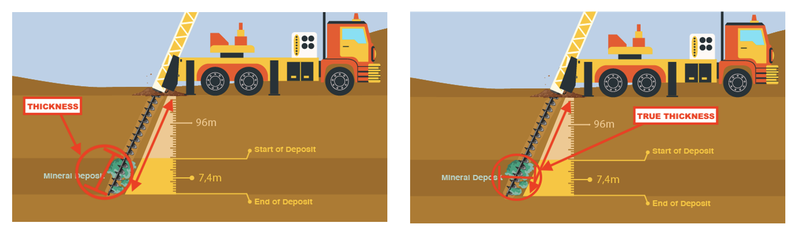

At a very high level the length of an intercept is a reference to the thickness of mineralisation found.

The thicker the mineralisation the bigger the potential discovery is likely to be.

Typically, companies will report thickness based on one direction of drill hole, which doesn't take into account the angle at which a company is drilling.

A more representative (and more technical) measure is “true thickness” looks at incorporating the angle of drilling as well as the length of the intercept.

The difference between thickness and true thickness becomes more important depending on the angle at which a company is drilling.

If the company intercepts 100m of mineralisation but drills a vertical hole then it is less material than if it hit 50m of mineralisation at a 45 degree angle.

The hole drilled at an angle indicates that the mineralisation extends both vertically AND horizontally.

Here is a visual explanation of the difference between thickness and “true thickness”.

How to understand the grade of mineralisation

The grade of the mineralisation talks to the concentration of the metal/mineral in each intercept.

The higher the grade, the better chance that the discovery is economic.

Using the example from earlier, the average grade of nickel mineralisation in the drill core over the 7.4m is ~0.29%.

The main thing to note is that the grade presented in the assay is the AVERAGE grade of mineralisation, not the total grade of mineralisation.

When it comes to building out a resource, finding high-grade drilling intercepts are important, because low grade drilling intercepts may be excluded from the resource estimation.

You can read more about this in our article: 🎓Cut-off grades explained.

Why does the type of metal/mineral matter?

Before the drilling programme and as part of the company’s exploration strategy, the company will outline what mineral they are looking for.

Minerals discovered have different prices and values in the market, which means that commercial grades for one mineral are different to another.

For example, a commercial gold discovery could have grades of 2% but the same grades for iron ore (a bulk commodity) would not be commercial.

When reading company drilling results it’s important to understand what grade represents a commercial discovery for the company.

Identifying this is one of the most difficult parts of reading drilling results, as “what is a commercial discovery” depends on lots of factors.

This is often more of an art than a science, and is different for all commodities.

That said, there are ways in which you can evaluate whether a drill result is “good” by comparing it against your initial expectations for the drilling campaign that you have hopefully set BEFORE the drilling results were announced.

These expectations will likely be based on the current price of the commodity, other drill holes in the area, the type of drilling done (infill versus extensional), where the drill hole sits within the deposit and drilling results from other successful mines in the area.

If you would like to learn more about setting drilling expectations read this:

🎓Expectation setting leading up to drilling programs

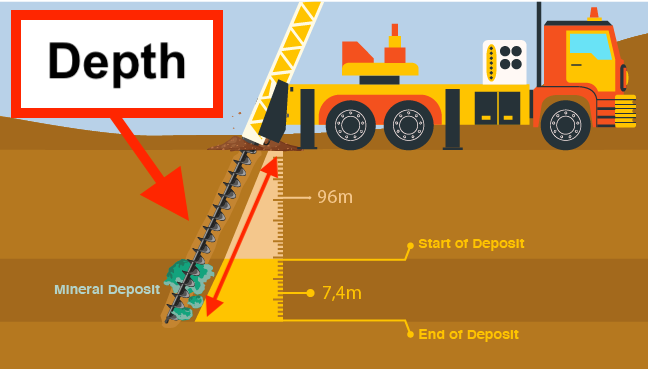

What does the “depth of mineralisation” mean?

The depth of mineralisation refers to the depth at which the mineralisation starts based on that particular drill hole.

Using the example from earlier, the 7.4m thick intercept would start from a depth of 96m.

The depth matters because it will ultimately impact the overall project economics of a new discovery.

If a discovery is made at shallow depth then it could be amenable to a low cost open pit mining operation.

If the discovery is made deep underground then it will need to be mined using underground mining methods which can be more costly.

Depth isn't the only thing that matters when evaluating a commercial discovery, the grade, the length of a deposit all impact the economic viability of a mining project, and depth alone should never be used to judge the value of an intercept.

What is a drill hole ID?

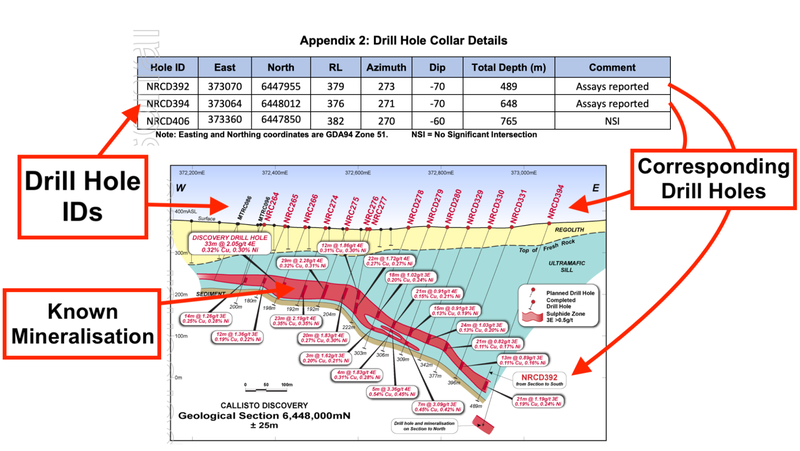

All drill holes are given a name or ID which can be found in the back of drilling result announcements in the JORC table.

These IDs matter because you can then see where the hole fits on the the company’s deposit:

Where the hole is drilled matters to the story of the deposit.

If the hole is drilled, and mineralisation is intercepted in an area where mineralisation does not currently exist, this is a good thing as it potentially ‘extends’ the deposit.

However, if the hole drilled is between two holes of known mineralisation (also known as an “infill” hole or “infill drilling”) then there is no extensional ‘upside’ to the discovery and the drill result is often priced into the stocks.

The identification numbers are also used to keep a clean record of every drill hole so as to avoid confusion when it comes time to model out a resource or help use existing drilling data to plan future drill programs.

How to know if a drill result is good or bad?

Almost always, after a results announcement, investors are left thinking “are these drilling results good?” OR “how should i feel about these results?”.

Both are very difficult questions to answer, because the answers depend on a lot of factors.

The most important of which is whether or not the drill results met your expectations which were set BEFORE going into the drill program.

Without expectations it is important to objectively judge a set of results and so we make sure to always record your bull, base and bear case scenarios before a company starts drilling.

🎓 To see how we set expectations going into material announcements like drill results check out the following: Expectation setting leading up to drilling programs

Most importantly, when looking at drill results, look at them within the context of all the holes that have been drilled to date. Don’t just look at one in isolation.

It’s important to look at the drilling results that “hit” AND the drilling results that “missed” from a programme.

Maps will give you a great indication of where the mineralisation occurs and what to expect from future drilling programs - and you can see the drill results from holes that are yet to be announced (which can build more excitement into the story).

You won’t always get it right, and setting drilling expectations takes time and practice. But, if you start early, you can quickly improve your skills and knowledge in understanding junior mining investments.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.