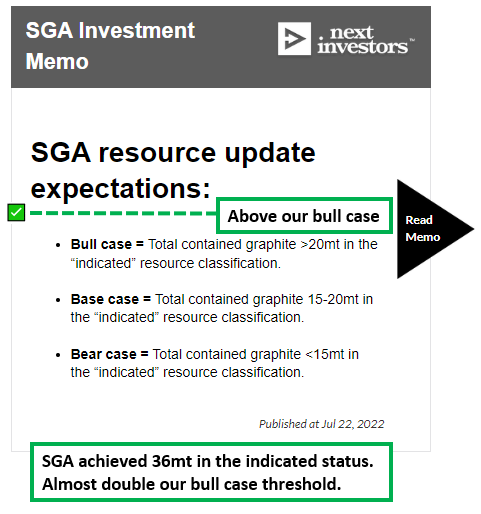

SGA beats our bull case expectation for its graphite resource upgrade

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 4,354,500 SGA shares and 1,466,250 SGA options, the Company’s staff own 50,000 SGA shares and 12,500 options at the time of publishing this article. The Company has been engaged by SGA to share our commentary on the progress of our Investment in SGA over time.

It’s almost double our “bull case” expectation.

In July last year we set our bull, base and bear cases of what we wanted to see from our 2022 Small Cap Pick of the Year Sarytogan Graphite (ASX:SGA) for its graphite resource upgrade.

Our bull case was >20Mt of indicated graphite - this was our best case scenario for what we wanted to see SGA deliver.

Today SGA announced an upgrade of almost double our bull case, lifting 36Mt of its contained graphite into the “indicated” classification.

An “Indicated” resource basically means that the characteristics of the resource can be estimated with a “reasonable” level of confidence, as compared to “Inferred” which has a “low” level of confidence.

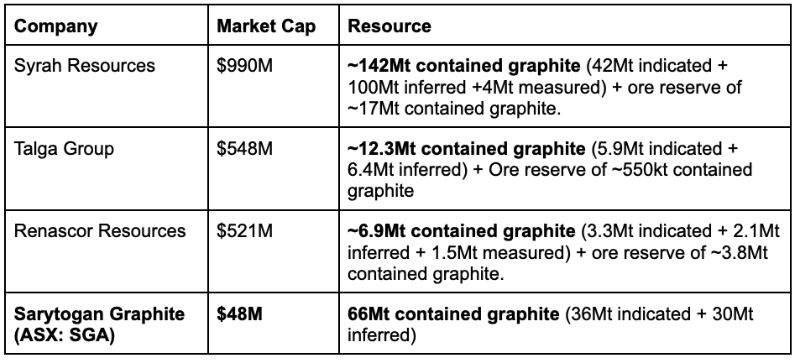

Aside from the highest grade, SGA also had the second largest contained graphite resource on the ASX, second only to $990M-capped graphite producer, Syrah Resources.

Now SGA has taken over half of its JORC resource from “inferred” into the “indicated” status - basically upgrading the confidence level of the giant resource estimate.

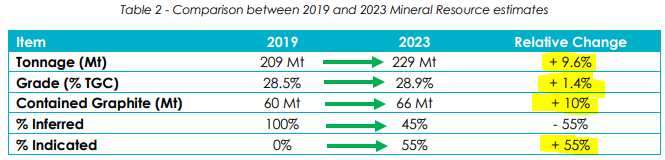

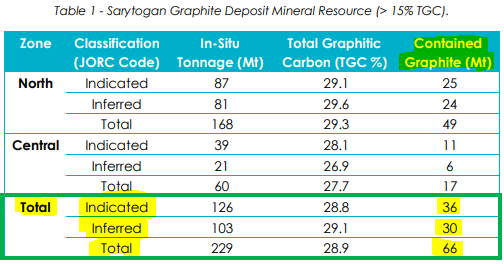

SGA now has a 229Mt resource with graphite grades of 28.9% for a total of 66Mt of contained graphite - 36Mt of which now sits in the “indicated category”.

Having an indicated resource matters because it is the first major input into a pre feasibility study (PFS) and helps when it comes to financing the project in the future.

With ~55% of the SGA’s giant resource now in the “indicated status”, SGA can now plug the JORC resource into a PFS and start to model overall project economics.

SGA has today kicked off the PFS.

Our take on SGA’s resource upgrade

SGA listed on the ASX back in July 2022 with the target of upgrading its already giant resource from inferred into indicated status.

To do this, the company had to run an extensive drill program to collect the drilling data needed to upgrade its resource classification.

Going into that drill program, we set our bull/bear/base case expectations for the amount of resource that SGA would upgrade to the higher confidence interval.

When setting our expectations we were mindful that these sorts of exercises typically end in resources getting smaller and more often than not only a small percentage being upgraded into indicated.

When setting our expectations, we wanted to see SGA convert one third of its contained graphite from ‘inferred’ to ‘indicated’ status.

SGA has beaten our bull case expectation significantly and improved on all aspects of its resource estimate:

1) Resource update BEAT our bull case expectation. Our bull case was to see >20Mt in the indicated classification, SGA brought over 36mt to indicated status. This was just under DOUBLE our bull case threshold.

2) Resource improved on all parameters. SGA increased the tonnage of the JORC resource by ~10%, the grade by 1.4%, and the contained graphite tonnage by ~10%. Most importantly, it took 55% (over half) of the resource from inferred into the indicated status.

3) SGA still has the ASX’s highest grade, 2nd largest by contained graphite resource. SGA now has a 229Mt resource at a graphite grade of 28.9% for a total of 66Mt contained graphite.

SGA’s resource vs other ASX graphite stocks

After major catalysts like today’s, it's important to put some context around SGA’s upgraded resource, and see how it stacks up compared to other graphite stocks on the ASX.

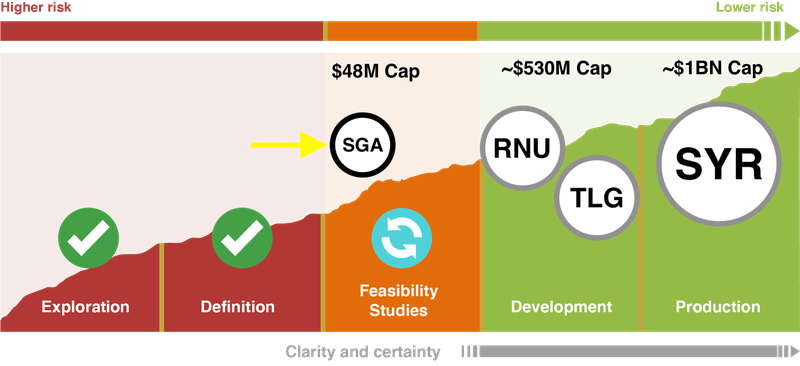

SGA is currently capped at $48M, a fraction of where its peers trade — despite having a giant (now largely ‘inferred’) graphite resource.

Below is our peer comparison listing the market caps of Syrah Resources, Talga Group, and Renascor Resources and each of their graphite resources.

First off, it's worth noting that all three peers listed below are all at a more advanced stage than SGA in terms of project development.

Syrah is producing graphite right now, Talga and Renascor have ore reserves and are closer to production and have more advanced downstream strategies.

SGA has:

- ~5.3x the contained graphite of Talga

- ~9.5x more contained graphite than Renascor,

- but trades at ~1/11th of both their market caps.

We think that the differential in market valuations shows how SGA can grow as it continues to develop its graphite business.

With its resource upgrade complete, SGA is now in a position to move its project from “definition” stage into the “feasibility studies” stage.

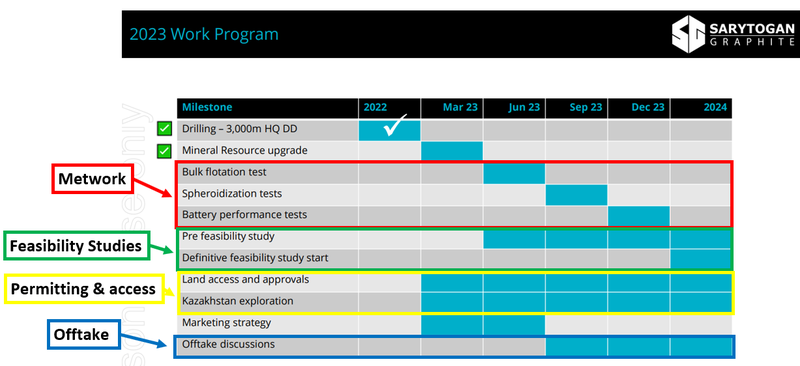

With a busy 2023 ahead we will be watching for newsflow from the following:

- Feasibility studies - This will lay out the economics behind SGA’s project. SGA is currently tendering out a pre feasibility study (PFS) to potential contractors. This work should kick off in Q3 and run for 12-18 months.

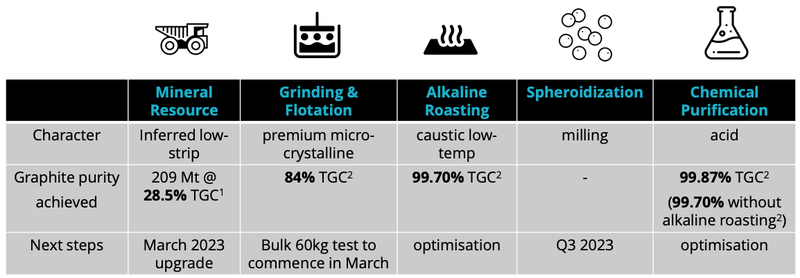

- Metwork progress - So far SGA has managed to achieve graphite purity levels of 99.87%. Ultimately, it is chasing 99.95% graphite purity to sell into the high value battery anode market. This work is currently ongoing. We think it will be a major catalyst if SGA can crack 99.95% purity in metwork.

- Offtake discussions - This will be important when it comes time to try and move SGA’s project from definition into the development stage. This type of newsflow usually acts as a major catalyst as it provides industry validation for a project.

All of this forms the basis for our Big Bet for SGA which is:

Our SGA “Big Bet”

“Given this graphite project’s strategic location in between China and Europe, we hope that if SGA proves out the size and economic extractability of the resource, it will generate interest from major mining companies, leading to a takeover of SGA for $1 billion+.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our SGA Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

For a quick summary of SGA’s progress over time see our SGA Progress Tracker:

What’s Next?

Ongoing metwork 🔄

SGA continues to work with its processing partners to achieve the required Uncoated Spherical Graphite (USpG) specifications of 99.95% purity in spherical graphite balls of 5-20 micron in size.

SGA has already achieved 99.87% but is chasing that all-important 99.95%+ purity level.

Achieving these specifications will be key to accessing the battery anode market with a high priced spherical graphite product.

We think that this will be the major catalyst for SGA and the final step validating SGA’s giant resource as suitable for use in the lithium ion battery industry.

To get this done SGA has already delivered a bulk sample to its German lab partner.

SGA will be running a bulk flotation program through Q2-2023 to then feed into the spheroidization program in Q3-2023 ahead of battery performance tests in Q4 2023.

We touched on all of this in our last SGA note: SGA Scaling up its High Value Battery Quality Graphite Aspirations.

We do note that there is no guarantee that SGA will be able to achieve these required specifications and/or it may not be able to scale the processing solution to a size/scale that is required for its project.

Permitting and access 🔄

The on-ground SGA team in Kazakhstan, including six geologists, is busy securing land access and approvals. It is also undertaking some exploration work, leveraging swathes of historical data left by past exploration in Kazakhstan by the Russians.

What are the current risks in SGA?

While SGA has made breakthroughs on the metwork front, the company still has a lot of work to do before its project is ready to be put into development.

We think the key reason why SGA is being valued at just a fraction of its peers is a combination of:

- Ongoing metwork - SGA is working to produce 99.95%+ purity graphite that is suitable for sale into the battery anode markets.

- Project is early in the feasibility stage - SGA has just completed the “resource definition stage” and is now preparing to put the project into the “feasibility study stage”.

As a result, there are still risks that the company needs to address, some of which we list in our SGA Investment Memo.

We are also mindful that SGA's project is still early in the feasibility stage and like all small cap stocks with no revenue, the company may look to raise additional capital at some point in the future.

SGA had $5M in cash at December 31st 2022, which is a decent amount given the work they have planned, however ‘funding risk’ never completely goes away, and is part and parcel of small cap mining stocks.

To see the risks in detail check out the Memo here, or click on the image below:

Our 2022 SGA Investment Memo

Below is our Investment Memo for SGA, where you can find a short, high level summary of our reasons for Investing.

In our SGA Investment Memo, you’ll find:

- Key objectives went want to see SGA achieve

- Why we are Invested in SGA

- What the key risks to our Investment Thesis are

- Our Investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.