Making sense of what's 'in' and what's 'out'

Published 31-OCT-2022 10:39 A.M.

|

13 minute read

If you read the amount of news headlines and articles we do, it can feel a bit overwhelming trying to make sense of it all.

In an increasingly chaotic world full of competing narratives and conflict it can be hard as an investor to identify which macro themes are “in” or “out.”

Let alone choosing the highest quality stocks within those themes.

So last week we used the Gartner hype cycle to explain how we view macro themes.

Understanding where the tailwinds are coming from, or will come from in the future, is a big part of making good, long term investments.

And today, we want to check in on the macro themes that are “in” at the moment, the two themes we will be positioning into for 2023 and finally a new series of investments we plan to make into early stage lithium companies, possibly at the top of the lithium cycle, and why.

These are some of the world’s priorities right now, that are holding investor attention:

- Critical minerals

- Fixing the energy crisis

- Re-shoring of supply chains

Conversely, out of favour macro themes can be a great place to look for bargains as well.

We’re thinking specifically of gold and cannabis stocks that have been badly beaten up.

And is it wise to risk investing in a red hot lithium market at what could well be the “top of the cycle”? Maybe...

Critical minerals/materials

These are the minerals the world needs to decarbonise, or just simply satisfy the most basic demands of local economies. Think copper, nickel, rare earths, lithium, graphite etc... largely battery materials and energy transition metals.

We argue that things like helium are critical as well - given its role in the manufacture of computer chips.

Commodities were a “boring” part of global trade until governments realised they needed them to keep their economies going while achieving energy independence and reaching their net zero emissions targets.

Suddenly the language around commodities changed as both governments and investors began to recognise these minerals as “critical.”

The key demand driver for much of this has been the electric vehicle revolution, starting with Tesla Battery Day, when Elon Musk implored the world for more nickel and highlighted manganese and lithium as key components for success (read our coverage).

Click here to see our battery materials Investments

Other automotive companies followed suit, with Volkswagen presenting at their own “Power Day”, announcing that they would phase out petrol cars by 2025 (read our coverage).

But it's not only EV and battery minerals that were seen as critical.

COP 26 was probably the most important green energy summit in the last few years, the main theme: critical minerals (read our coverage).

Importantly, the leaders who endeavour to make emissions reduction goals into a reality need minerals for electrification of vehicles, building solar and wind farms, green hydrogen projects, improved electricity storage and even nuclear power.

Click here to see our energy transition metals Investments

Securing these commodities is part of the “real economy”, which has been starved of investment (by the west) and will likely bring on the “mother of all CAPEX cycles”. This is evidenced by downstream operators like Tesla moving upstream to secure mineral supply (read our coverage).

In March this year the Australian government released a list of critical minerals (read our coverage), culminating in the US directly funding Australian critical minerals companies.

Despite all the focus on critical minerals, the one thing that governments didn’t foresee in their net zero ambitions was the role that traditional energy would play in bridging the gap...

The Energy Crisis

Spurred by the Russia-Ukraine conflict, energy prices - particularly in Europe - skyrocketed over the past six months.

But we believe that the problems started much before then with the underdevelopment and underinvestment in traditional energy (like oil and natural gas).

Click here to see our traditional energy Investments

Once the war started, and Russian sanctions took effect, it was not until the squeeze on traditional energy supply was apparent (read our coverage).

We watched the Sydney energy conference earlier this year and heard the impacts, especially from Dr Jörg Kukies - State Secretary at the German Federal Chancellery - about the need for more and cheaper energy (read our coverage).

Since then gas prices have reached record highs, with many investors who backed traditional energy making windfall profits (read our coverage).

However, this energy crisis has exacerbated the current inflationary environment which has seen governments cut back on spending, and the urgency to increase the shift towards renewable energy.

Energy prices eased from a record spike in the last two weeks as measures taken by governments are starting to take effect, but these could be short term fixes and there is a lot still to play out as we approach the European winter.

Click here to see our green energy Investments

Beyond the energy crisis - one thing that the Russia-Ukraine conflict has highlighted to governments is the importance of securing a local supply chain, and the national security risk that comes with being reliant on unfriendly nations for critical minerals and energy.

Re-shoring of supply chains

More than ever, governments are looking to sure up their supply chains of critical minerals AND energy.

This can be viewed as either a crisis or opportunity, depending on where you are in the world.

As a mineral rich economy and stable ally to many countries experiencing supply risk, Australia is in an excellent position to take advantage of this development.

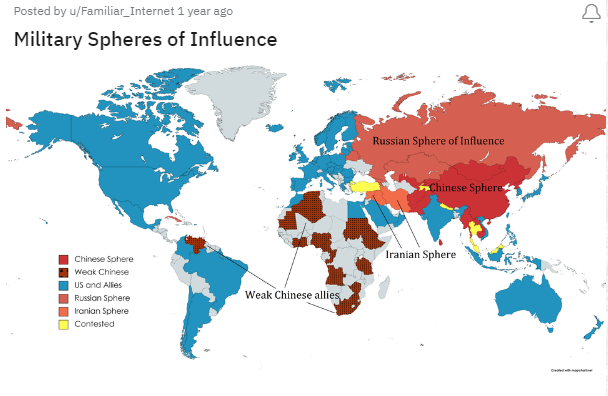

Three weeks ago we presented this map of the world:

We argued that the OPEC production cuts announced in early October helped lay bare the increasing antagonism between the West and its Allies “blue” and emerging challengers to the current world order “red” (read our coverage).

In this environment, we concluded that:

“If you are a blue country and any of your critical resources come from a red country, you need to find and replace that with supply from a blue country.”

Along with critical minerals and the energy crisis, we expect the pressure to re-shore supply chains to increase in the coming years, which could create tailwinds for a number of our Investments.

Cannabis and Gold at bottom of the cycle?

The above “in” macro themes look set to run for a while yet.

But as we explicitly aim to achieve 1,000% re-rates over the long term in our Investments, we’re increasingly drawn to both gold and cannabis stock Investments.

Our thinking here is that these macro themes have been completely deserted by market sentiment and this is where we can achieve significant returns if we can patiently hold until these themes come back to life.

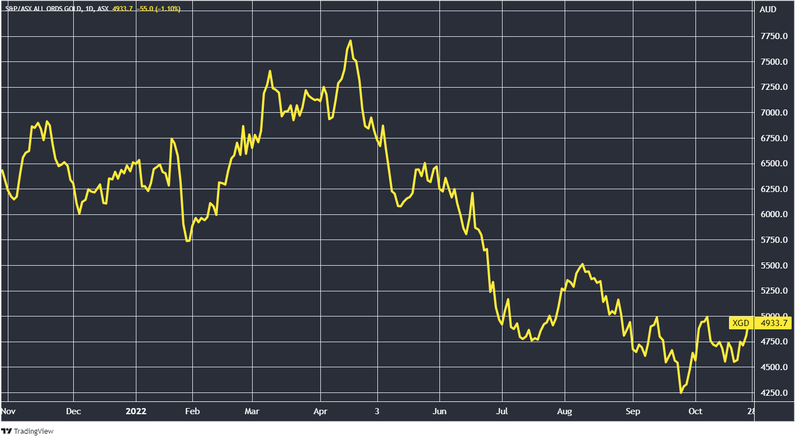

Gold is the classic inflationary environment hedge position and has survived over two millennia.

This is the chart of the S&P/ASX All Ordinaries Gold Index (XGD) over the last year:

Source: Tradingview

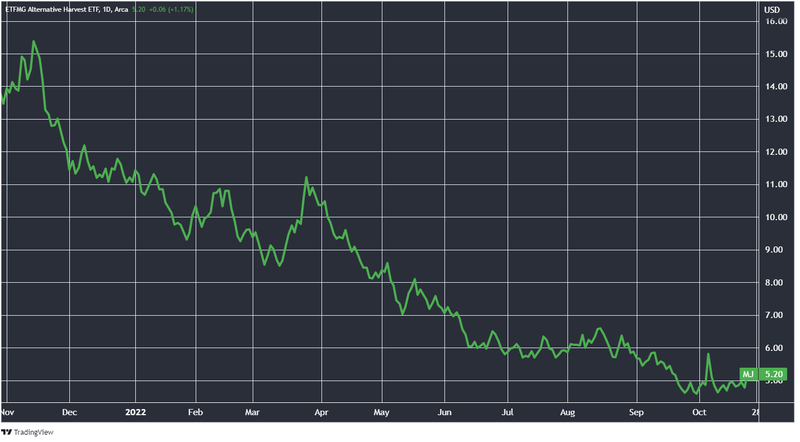

Likewise cannabis (for medical and recreational use) has been around for at least the same timeframe, but it's only now that the legalisation push is really starting to take hold.

As a gauge of cannabis stock sentiment, this is the chart for ETFMG Alternative Harvest ETF (MJ):

Source: Tradingview

The MJ ETF “tracks the Prime Alternative Harvest Index, designed to measure the performance of companies within the cannabis ecosystem benefitting from global medicinal and recreational cannabis legalization initiatives.”

And as you can see its been hammered over the last year - something which may be on the cusp of changing in 2023.

Europe and the US loom as key markets, particularly after US President Joe Biden pardoned a number of low-level cannabis offenders in recent weeks.

Germany is looking at allowing recreational cannabis and promises to be a big market too.

As a result, we’re looking to add to our exposure across gold and cannabis as the cycles for these stocks potentially bottom out.

The lithium boom - more to come or top of cycle?

Lithium is an interesting macro theme to watch. We might even call it a bit confusing.

Lithium demand surged as a key ingredient in batteries over the last 2 years, and the lithium price continues to hit new record highs each month.

Lithium has had a very strong run over the last 2 years, small lithium companies have done extremely well, with some even approaching first production.

But we have been investing in small caps for 20 years and have seen many “hot commodities” quickly cool off as new supply comes online during periods of sustained higher prices and investor excitement wanes.

So the question is - will the lithium boom continue for years to come in a structural demand shift for the commodity, or has the lithium price gotten ahead of itself and will cool off in 2023?

We think the interest in lithium is going to continue, which is why we are planning to take positions in five carefully selected, early stage lithium stocks to hold into 2023 and beyond.

This could be a risky move, as the lithium market appears to be running hot at the moment - and if it does cool off (or even crashes) in 2023, we will be stuck holding onto a few underperforming investments for a while.

But on the flipside, if the lithium market keeps going, and the market continues to reward lithium discoveries during 2023, we are betting that one out of these five lithium bets will deliver a discovery and a 10x return.

Because of the macro theme risk in this strategy, it will be implemented in the Catalyst Hunter portfolio, where we focus on higher risk investments.

So why are we making this bet on lithium in 2023?

Our best investments so far have been in lithium - VUL is still sitting over 3,500% above our initial entry price, but this investment was made in 2019 before the lithium market ran.

Earlier stage lithium explorers are still attracting investor interest if they can deliver a lithium discovery - like our Investment LRS that rerated 9x and raised $35M.

RAS and TYX are looking strong ahead of their initial lithium drilling assay results (fingers crossed they can deliver something).

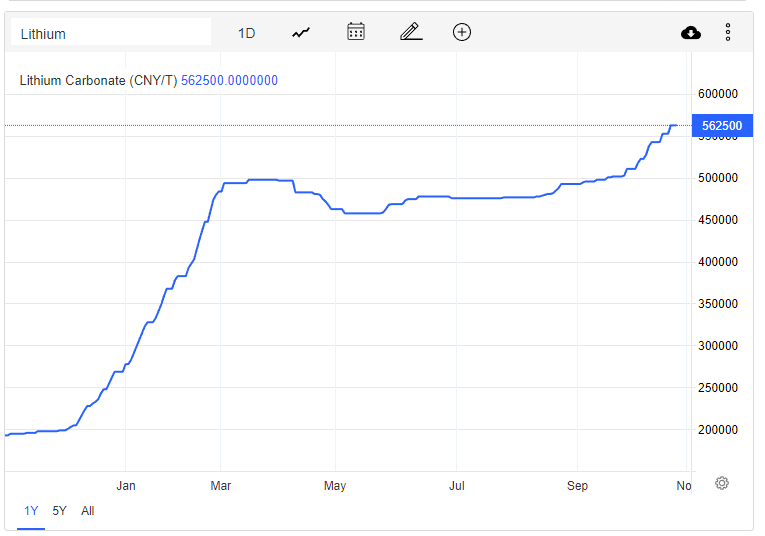

And of course the lithium price just keeps going up... even during a generally awful 2022 on global markets:

Source: (Trading Economics)

Placing a few lithium exploration bets at this stage of a commodity price chart is 100% a risky proposition - so like with our prediction that cannabis and gold will have a run in 2023, we will soon find out if we are right, or receive another expensive small cap lesson.

🗣️ This week’s Quick Takes

VN8: Acquisition of OntheNet completed and board appointments

DXB: Patient Recruitment and quarterly cash flow update

NHE: Noble Helium raises $6.1M - we participated

GAL: Palladium grades increasing; corridor expands

AKN: Drilling campaign completed at Koongie Park base metals project

ALA: ALA narrows focus to iNKT cell therapy

RAS: NT Lithium Project Update

TTM: More promising results from Copper Ridge Porphyry prospect

IRD: $25M grant for proposed Cape Hardy port development stands

PRL: 25% more land under licence for PRL's green hydrogen project

DXB: DXB gets $6M R&D Tax Incentive Rebate

TTM: Promising early results at Ecuadorian gold project

VUL: Highest grade lithium produced to date

CAY: Certificate Of Environmental compliance granted

NHE: 3D Seismic Surveys Kachinga Lead

This week in our Portfolios 🧬 🦉 🏹

Galileo Mining (ASX:GAL)

Given the importance of our GAL Investment in our overall Portfolio, we called on some help to generate 3D models of the mineralised body at its Callisto discovery.

At this stage, GAL is leading the pack to record the best return of 2022 of any Investment in our Portfolios — its discovery in May sent its share price from 20c to as high as $1.95.

If GAL continues delivering results and making new discoveries, it has an excellent chance of extending its gains and holding onto that top spot.

📰 Read our full Note: Understanding it all... in 3D

Invictus Energy (ASX:IVZ)

IVZ is in the middle of a hugely significant drilling event in Zimbabwe.

IVZ’s drill is now at 2,021m out of a planned 3,500m and initial logging has revealed a 10m to 15m potential hydrocarbon interval. This is just from the first 3 out of 7 targets.

AND: a significant seal is in place above the primary targets - which will be drilled next - which addresses one of the key geological risks that had been weighing on the market.

The primary targets are being drilled into now and will take another 3 to 4 weeks.

We’re at a critical stage of our IVZ Investment journey.

You can watch IVZ MD Scott Macmillan walk investors through the drill update announcement here.

📰 Read our full Note: IVZ Drill Update: Regional seal and 10m to 15m potential hydrocarbon interval

Arovella Therapeutics (ASX:ALA)

Our early stage cancer treatment biotech, ALA, is now fully focussed on its iNKT cell therapy after deciding to discontinue its legacy OroMist based products.

The benefit of not pursuing any further work on OroMist products comes in the form of $1.5M annual cost savings.

The move will incur a one off $300k restructuring cost, but we know how hard it can be for small-caps to raise funds so long-term this makes sense.

We think it's a good strategic move for ALA to prioritise its core treatments.

ALA has four big catalysts due to come in by Q2 2023 as it goes after a Phase 1 clinical trial for its lead cancer treatment — we think it could re-rate on any of these catalysts.

📰 Read our full Note: $1.5M annual cost savings allows ALA to focus on what really matters

Evolution Energy Minerals (ASX:EV1)

Our graphite development stock EV1 kicked off 7,500m of exploration drilling on Thursday.

EV1 already has an advanced, development ready project approaching production, that has a well established 18 year mine life.

However, big high-grade shallow discoveries near its existing JORC resource would improve the already strong project economics considerably.

New discoveries could lead to improved project economics by giving EV1 the option to add new resources to the back end of its project (increasing the mine life) or to the front end (highest grade most profitable to mine).

Everyone loves an exploration drilling event.

📰 Read our full Note: EV1 Begins Drilling – Targeting More Shallow High Grade Graphite

⏲️ Upcoming potential share price catalysts

Results expected in the near term:

- IVZ drilling its giant gas prospect in Zimbabwe - we waited two years for this event (memo).

- Update: 2,021m out of a planned 3,500m and initial logging has revealed a 10m to 15m potential hydrocarbon interval. This is just from the first 3 out of 7 targets. AND: a significant seal in place above the primary targets.

- GAL is undertaking a second round of drilling at its Callisto PGE discovery in WA.

- Update: GAL has so far completed 25 diamond core drill holes and GAL expects further assays to be back from the lab from mid-November onwards - the grades are increasing west which is great to see (read our Quick Take).

- BPM: results pending from drilling at its Hawkins lead/zinc prospect in the Earaheedy Basin, close to Rumble Resources’ discovery. (memo)

- Update: Quarterly revealed that assays are “imminent”.

- LNR has recommenced maiden drilling for rare earths along strike from Hastings Technology Metals (memo).

- Update: No material news this week.

- PFE has drilled its polymetallic (Hellcat) project (memo).

- Update: No material news this week.

- PRL: Awaiting final execution of a joint development agreement with Total Eren(memo).

- Update: No material news this week.

- GGE is drilling its maiden helium well in Utah, USA (memo).

- Update: No material news this week.

Have a great weekend,

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.