The need for significant investment in rare earths, other critical materials

Published 06-JUN-2022 08:54 A.M.

|

13 minute read

A few investors got hot and bothered this week about a Goldman Sachs report saying lithium's epic run may be coming to an end.

Lithium stocks fell on the day of the report and then bounced back over the next few days (we held all of our positions).

Also, our latest 10 bagger GAL dropped after excitement from their major Palladium-Platinum discovery cooled a bit... but then came right back up as expectations of GAL’s current drilling into the “main target zone” started creeping in.

We are also keenly waiting this weekend for our high risk Investment in PRM & GLV to hit target depth in drilling one of the biggest gas targets drilled by an ASX micro cap in recent decades.

We expect to be either smiling or crying after we find out the binary result as early as Monday.

Even if you aren’t invested in or following PRM and GLV, put them on your watch list for this week as we expect quite a show - the share price should move aggressively up OR down depending on the result.

Or it might not. We already got it wrong when we predicted a pre-drill result run up in PRM and GLV share prices, which was snuffed out a few weeks ago when the broader market corrected.

Today we will also provide a weekly update on our running “upcoming share price catalysts” list and how each stock is tracking.

So while the Goldman report predicted the lithium run slowing, it’s just one opinion out there, with many still believing the battery metals boom has a way to run.

This includes Elon Musk, who in Tesla’s last earnings call asked for more people to get into the lithium mining business.

We believe there is still a long way to run in the broader commodities cycle, especially after years of underinvestment while money cycled into growing internet and tech companies.

Basically for the last 10 years, the majority of investor funds were being deployed to accelerate the growth of social media companies, digital payment platforms, online streaming services, digital marketplaces and phone apps - which of course have been great and changed our lives for the better.

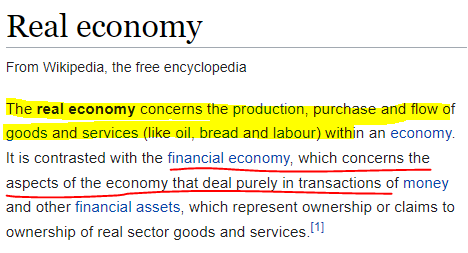

But lagging behind, there was less investment going into “real world stuff” like building new mines, making new mineral discoveries, building steel mills, processing plants, food sources and energy.

Things required for the “real economy”:

This was our key takeaway from a panel discussion and presentation at the All-In podcast’s summit in Miami this week.

We agree that there’s a “big bull market in real stuff” coming.

We like the All-in podcast because we think it’s a leading indicator of what global fund managers will be thinking in the near and medium term - and where they will be putting their money.

The preso we watched is given by a guy called James Litinsky, who was a successful hedge fund manager in the US, but now runs the biggest rare earths mine in the US.

Five years ago he saved this rare earths mine from bankruptcy - back when nobody cared about critical materials.

Now they are of strategic importance.

We’ll share the link to a recording of the presentation where he covers the need for significant investment in rare earths, other critical materials, supply chain, and energy independence in the West over the coming decades.

Here is a summary of our key takeaways from James’ talk in case you don’t have a spare 30 min to watch the full thing:

- The “real economy” has been starved of investment in the West. Most of the incremental commodities capacity over the last decade has come from China which continues to invest in downstream and upstream capacity in the “real economy”.

- Four of the top 10 OEM carmakers (by battery manufacturing capacity) are based in China, as are much of their supply chains.

- More investment in minerals like nickel, copper, cobalt, lithium and rare earths is required to meet future demand for battery manufacturing capacity.

- The world will need 40-50 copper and nickel projects over the next couple of decades, or roughly US$200 billion in CAPEX per annum to satisfy the demand for electrification.

- About to see the “mother of all CAPEX cycles” which may need closer to US$3 trillion invested in delivering new supply over the next decade to satisfy the coming demand.

- Investment in new projects is limited by the cost of capital upstream. Downstream operators, like Tesla who have a much lower cost of capital, may look to move upstream and directly acquire new mining projects.

- The panel discussion makes reference to Tesla’s recent earnings call where Elon Musk said that Tesla is considering “becoming a mining company” by purchasing and operating mines in the critical minerals space. They also mention Elon’s encouragement of entrepreneurs entering the lithium mining industry.

- These minerals will be considered “the new oil”, and countries will need to build up strategic reserves just like they have done so with oil and gas. There are likely to be security risks as a result of geopolitical tensions over a rush to secure supply chains of these minerals.

One thing that really stood out for us was the idea that there could be a merging of downstream operators with upstream mining businesses - basically this means buyers of critical materials actually buying and owning the mines that supply them.

This all comes only a few weeks after a Tesla earnings call where Elon Musk said he was considering getting into the lithium mining and refining business.

Here is a quote from that earnings call:

“I’d certainly encourage entrepreneurs out there who are looking for opportunities to get into the lithium business. Lithium margins right now are practically software margins”

For the CEO of one of the world's largest electric vehicle (EV) makers to be talking up mining this much really says something about supply chains globally.

The specific synergy would come from Tesla being able to leverage its relatively lower cost of capital. Tesla could buy the mine, raise capital and develop a lithium mine/refining business with a much lower cost of capital than say a micro cap junior explorer.

Here in Australia, we have seen first hand the cost of capital issues in developing mines.

In some instances, the government has provided loans to companies where capital markets are unwilling to finance large scale commodities related projects.

Iluka Resources, which was recently loaned $1.3 billion from the federal government, is a prime example.

Here at Next Investors, our team believes that the “critical materials” investment thematic is only just getting started.

From a simple supply-demand perspective, but also from a geopolitical security of supply standpoint.

We think that the future of mining will see operators have some level of presence either via partnerships, direct equity stakes, or joint ventures in downstream manufacturing capacity.

With capital markets avoiding mine developments and the bigger players in the mining industry prioritising dividends instead of re-investment into new supply, we see this gap being bridged by downstream operators.

Again, Here is a link to our current Investments in critical materials.

⏲️ Upcoming potential share price catalysts list

Results expected in the near term:

- The Sasanof companies’ (PRM & GLV) high impact gas drilling event: one of the biggest oil and gas wells drilled in Australia by an ASX junior in decades (memo)

- IN PROGRESS: Drilling of the Sasanof-1 well started last Friday (27 May 2022).

- Update: ⚠️ DRILLING IS ANTICIPATED TO BE COMPLETED OVER THE WEEKEND ⚠️

- GGE is drilling its maiden helium well in Utah where it’s aiming to make a commercial helium discovery (memo)

- IN PROGRESS: GGE has completed its maiden drilling program with a ~203 foot (~62 metre) gas bearing column intercepted.

- Update: GGE is now waiting on a workover rig to arrive which will test the well’s flow rates and the helium concentrations of the well. The results from this should be available to us within ~three weeks and will determine whether or not GGE has made a new helium discovery or not.

- PRL signing a Joint Development Agreement with its partner, Total Eren to materially de-risk its WA Green Hydrogen Project (memo)

- IN PROGRESS: The signing of the “Joint development agreement” (JDA) with TotalEnergies.

- Update: PRL’s deadline to sign its “joint development agreement” (JDA) with Total Eren has been extended to 31 July 2022, adding 2 months to the timeline for this catalyst.

- IVZ is about to drill its giant gas prospect in Zimbabwe - we have been waiting two years for this event (memo)

- IN PROGRESS: Drilling is scheduled for July and IVZ recently updated the market saying it had three separate farm-in offers that were being considered.

- Update: No progress has been made this week.

- KNI is about to drill its cobalt targets in Norway (memo)

- IN PROGRESS: Last week KNI put out an update on the drilling program confirming that it has completed ~1,007 metres of the total ~2,800m drilling planned. We covered the update in a Quick Take which you can read here.

- Update: Drilling is still ongoing and KNI expects the assays from the drilling to be turned around in the next ~90 days.

- BPM is about to drill its lead zinc prospect in the Earaheedy Basin close to Rumble Resources’ recent discovery (memo)

- IN PROGRESS: Three weeks ago, BPM announced that its ~7,500m AC/RC drilling program had commenced at the Hawkins project (along strike from Rumble’s discovery). This is a drill campaign we have been waiting for since May last year and we should start to see some of the first results from this over the coming weeks.

- Update: No progress has been made this week.

- LNR (formerly FNT) commencing drilling for rare earths (memo)

- IN PROGRESS: LNR is still in the process of getting approvals, so we are not sure exactly when the actual drilling will occur - this may be later than most of the above list but we are keeping an eye on progress.

- Update: No progress has been made this week.

🗣️ Quick Takes

Here are this week's Quick Takes:

DXB: First patient recruited in rare kidney disease Phase 3 trial

FYI: Commences next phase of HPA project development with Alcoa

GAL: Rhodium picked up in assays, discovery now more valuable

KNI: Share Purchase Plan closes raising $533k

LRS: Infill drilling reveals more spodumene bearing pegmatites

PUR: Four new gold prospects at Commando

PRM/GLV: Sasanof-1 primary target to be drilled between 2nd and 5th June

TMR: 2022 drilling program commenced at its Canadian gold project

TMZ: Drill targets identified, rig on its way

Next Investors: ESG and Our Portfolio Companies

Next Investors: Educational Article - What is an ASX listed shell?

Macro: Is copper the next battery material to go exponential?

Macro: China stimulus to add fuel to the commodity supercycle fire?

Macro: Fund managers committing $16 trillion to meet net-zero targets

Macro: All-In podcast discusses “critical minerals”

Macro: Lithium market faces structural supply side issues

📰 In this week: 🧬 🦉 🏹

🏹 Catalyst Hunter

Prominence Energy (ASX: PRM) and Global Oil and Gas (ASX: GLV).

On Monday we reported that drilling had begun at the Sasanof-1 exploration well.

At the time, the drill bit had reached the ocean floor at around 1,000m water depth and started drilling through the first 1,000m of rock which sits between the ocean floor and the primary target area.

The primary target reservoir stretches 500m, at a total depth of between 2,000m and 2,500m below sea level.

A progress update on Friday from GLV explained that the Sasanof-1 well is now being readied to drill into the primary target zone this weekend.

That means that come Monday, we should know whether our Investments PRM and GLV have an ownership stake in a new Australian gas discovery.

We set the following as our expectations for the drilling program:

- Bullish case (Exceptional result) = Gas columns measuring greater than 20m.

- Base case (Good result) = Gas columns measuring between 10 and 20m.

- Bearish case (Poor result) = Gas columns measuring less than 10m.

With GLV’s progress update on Friday, we now know that drilling through the target reservoir sand section is anticipated to occur over the weekend. We’ll be watching closely for an update and hopefully news of a gas discovery on Monday morning.

This well has been ranked amongst the Top 20 Highest Impact Wells happening anywhere on the planet in 2022 — rarely do we see ASX listed micro caps with exposure to oil & gas exploration events this big.

However, offshore gas exploration is risky and there are far from any guarantees of a new discovery.

📰 Read our Friday update Note: Drilling results to come in over the weekend

📰 Read our full Monday Note: PRM & GLV’s Offshore Drilling has Begun. Here’s what we’re Watching for Next

Grand Gulf Energy (ASX: GGE)

GGE this week reported that it had intercepted a gas structure at its Red Helium Project in Utah, USA.

The now completed drilling at the Jesse #1A well intercepted a gross gas column measuring ~203 feet (~62 metres). The 203 foot intercept was made across a primary target that GGE previously estimated to be 8,100 feet to 8,300 feet deep. This means that GGE has effectively intercepted gas columns throughout the entire primary target area.

This was the first of the three key pieces of information that GGE needs in order to announce a new helium discovery:

- A proven gas system ✅

- Flow Rates - An outcome is due in about 3 weeks 🔄

- Helium concentrations - An outcome is due in about 3 weeks 🔄

GGE has secured a workover rig that is expected to be on site at the Jesse #1A well location to start flow rate testing in around two weeks.

All that’s left to announce a new helium discovery is for GGE to prove a commercially viable raw gas flow rate and commercially viable helium concentrations in this gas.

📰 Read our full Note: GGE Hits Gas Column. Flow Rate and Helium Concentration to be Tested Next

🧬 Finfeed

Dimerix (ASX:DXB)

On Tuesday, Dimerix (ASX: DXB) reported that it had achieved a significant milestone — its first patient recruited in its ACTION3 phase 3 pivotal clinical trial of DMX-200 in the treatment of FSGS kidney disease.

FSGS, or Focal segmental glomerulosclerosis, is characterised by a dysfunction in the part of the kidney that filters blood. It is a rare disease with no existing registered treatment options specifically for sufferers.

With its first patient recruited, DXB’s Phase 3 FSGS trial is now underway.The clinical trial is the last major step before commercialisation and to reach this point DXB has done a lot of legwork, including getting ethics/regulatory approval in 12 key jurisdictions.

DXB was most approved to conduct trials in the US — an important market for DXB’s treatment as that is where a large portion of patients reside.

There’s a pressing need for a treatment, especially in the US, where FSGS has an outsized impact on the US healthcare system. Patients suffering from FSGS usually require a kidney transplant — an expensive option that’s not available to everyone.

We initially Invested in DXB at 20c in August 2021 and the share price is currently sitting at 16 cents, or 20% below our entry point after biotechs across the board were hammered over the past four months. DXB remains well funded through to completion of the Phase 3 FSGS trial with ~$16.8 cash at the bank as of 30 March 2022, which we think should help it weather the storm should the general malaise for biotechs over the last four months continue.

📰 Read our full Note: DXB Recruits First Patient, Gets FDA IND Approval

Have a great weekend,

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.