Our new Investment. Battery materials bottom? Summary of the key media events this week.

Published 23-JUL-2022 10:28 A.M.

|

13 minute read

We’re gonna say it - battery materials are back.

After a rough couple of months, it’s been a very eventful 72 hours around the world for the battery materials and electric vehicles investing thematic.

On Thursday, Tesla surprised the market by beating revenue expectations and forecasting 50% sales growth for the coming year, triggering a run on battery materials stocks.

Last night Ford announced a barrage of deals for battery materials - agreements with companies for lithium, nickel, aluminium, copper and graphite.

Just a few hours ago, Volkswagen fired its CEO for slow progress on its electric vehicle push, assuring its investors it will accelerate its move to electric.

All underlined by a statement last week from US Energy Secretary Jennifer Granholm saying the US will back miners to stop China's “weaponisation” of battery materials.

The perfect backdrop for our latest Investment.

Yesterday, we announced our new Investment in the battery materials sector: Sarytogan Graphite Ltd (ASX: SGA).

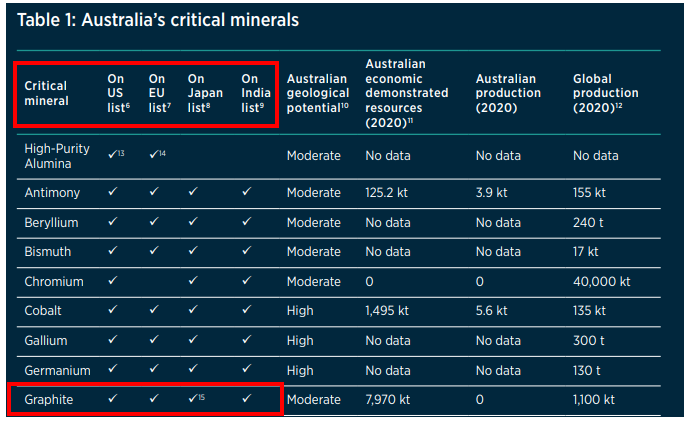

Graphite makes up 28% of an EV lithium ion battery by weight.

It comprises 95% of a battery’s anode and cannot be substituted.

As such, graphite demand is expected to be five times greater than current levels by 2050.

Such is its importance - graphite is on the strategic critical mineral list of the US, European Union, Japan, India and Australia.

SGA owns 100% of a giant graphite resource in central Kazakhstan.

Kazakhstan is strategically located right between EV making powers Europe and China.

SGA has the highest grade graphite resource and second largest graphite resource of any ASX-listed company.

As long term holders, our big bet is that we want to see SGA develop its giant graphite resource, which we believe has the potential to catch the interest of major miners and become a world-class graphite mining operation.

Here is our SGA Investment Memo - including why we Invested, the risks and our Investment plan.

We’ve been building our Portfolio around the battery materials theme since 2019 when battery materials were unloved.

We believe it will be a 10+ year thematic.

After a huge run in 2020 and 2021, it appears we have just lived through a short term blip on the long term battery materials journey (we hope... anything can happen in the current markets).

Global markets fell hard in May and June, with battery materials stocks falling harder than most after meteoric rises over the last two years.

It never was going to go up in a straight line forever, and we see this pullback after an extreme run as healthy.

Remember that the same happened after the first battery materials run in 2018 and the subsequent fall, leading to a “battery materials winter” for much of 2019.

The 2018 battery materials run was primarily early excitement for the sector, well before all the major car companies were scrambling to secure supply and making real investments in electrification.

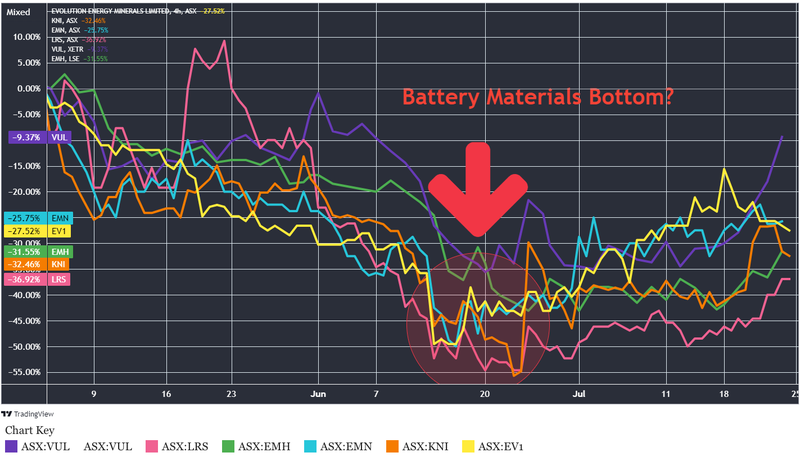

Here’s how our battery materials Investments have fared over the past couple of months.

With a bit of help from a slowly rebounding market, we think Tesla’s results, combined with the Ford deals and the US government’s public position, were enough to move the needle on the following six of our battery materials companies from their June lows.

Below are the share price changes between 23 June - 23 July close):

Vulcan Energy Resources (ASX: VUL) + ~37.1% - (memo)

Latin Resources (ASX: LRS) + ~39% (memo)

European Metals Holdings (ASX: EMH) + ~16.9% (memo)

Euro Manganese (ASX: EMN) + ~29.1% (memo)

Kuniko (ASX: KNI) + ~52.5% (memo)

Evolution Energy Minerals (ASX: EV1) + ~27.4% (memo)

This is encouraging to see after we vowed not to do any selling while the market was in “peak fear” back in June - long term investing in small cap stocks can be a white knuckle ride.

Granted, these stocks had been savagely sold off in the lead up to the new financial year, with tax loss selling, inflation, growth fears and war all playing a role.

And you can see just how bad the selling got in six of our portfolio companies between early June and the mid-June lows, with the bounce playing out through to the close of markets this Friday:

A complete list of our battery materials Investments is available on our Portfolio page.

And because of the factors covered today, and we’re going out on a limb here, but we’re going to say it anyway:

Is this the battery materials bottom?

Battery materials media review from the last week

Key takeaways:

- Tesla reported dip in earnings but managed to top estimates

- Tesla plans to increase vehicle deliveries by 50% on average annually over multiple years

- Tesla posted adjusted earnings of $2.27 a share, besting the $1.83 a share average of analysts’ estimates

- Elon Musk said, “We have the potential for a record-breaking second half of the year...The past few years have been quite a few force majeures, and it’s been kind of supply chain hell for several years”

Key takeaways:

- On Thursday, Ford announced a series of deals to secure battery raw materials, inking deals with Chinese battery maker CATL, Rio Tinto and Ioneer.

- Ford aims to increase global EV production to 600,000 vehicles by late 2023 and >2 million by the end of 2026.

- Ford is very bullish on EV uptake - it expects a compound annual growth rate for EVs to top 90% through 2026, more than doubling the forecast industry growth rate.

- Ford is adding lithium iron phosphate (LFP) cell chemistry for EV batteries to its portfolio, as well as the traditional nickel cobalt manganese (NCM) battery chemistry.

- Agreements with companies include Ioneer (lithium), Vale (Nickel), China's Huayou Cobalt and BHP (nickel), Rio (aluminium, copper) and Syrah Resources (graphite)

Key takeaways:

- Chief Executive Officer Herbert Diess will be succeeded by Oliver Blume, CEO of VW’s sports-car maker Porsche AG

- The removal of Diess came after “internal strife” over the group's slow progress in developing core software for the company’s new generation of electric vehicles.

- Car executives of big traditional automakers are under pressure to get ahead of new rivals, many from Silicon Valley, which have cash reserves and aren’t held back by capital-intensive legacy gasoline-powered vehicles.

Key takeaways:

- Nations have raised concerns over the global concentration of refining and production capacity for critical materials like lithium, rare earths and cobalt.

- The US sees China’s dominance over battery metals processing and manufacturing as a key threat to its national interest. As such, Joe Biden invoked the 1950 Defense Production Act to encourage domestic production of these materials.

- The Department of Energy’s loan program is already providing support to ASX listed battery materials producers with $107M loan provided to Syrah Resources (graphite, Mozambique)

Key takeaways:

- Australia produces about half of all unprocessed lithium supplies. Australia accounts for just 7% of the refined lithium supply.

- According to Tesla Inc. Chair Robyn Denholm, Australia needs to add capacity in refining and manufacturing to help the world meet the surging demand for batteries.

- Nearly US$14 billion in lithium investment is needed to supply planned EV production capacity by 2025

- EVs accounted for 2.4% of new passenger vehicle sales in Australia last year, compared to 4.5% in the U.S. and 20% in the European Union.

Key takeaways:

- Joe Biden has signed an executive order requiring that half of all new vehicle sales be electric by 2030, and the EU is also seeking to have at least 30 million zero-emission vehicles by 2030

- IEA believes mineral demand for use in EVs and battery storage must grow at least 30 times by 2040

- Graphite is the largest component in lithium-ion batteries by weight (20-30%) however, due to losses in the manufacturing process, it takes 30 times more graphite than lithium to make EV batteries.

- Graphite accounts for nearly 53.8% of the mineral demand in batteries - and EV contains more than 200 pounds (>90 kg) of coated spherical purified graphite (CSPG).

- Last year, nearly 60% of the world’s mined graphite production also came from China.

Key takeaways:

- China dominates the entire graphite anode supply chain end-to-end.

- Four companies are responsible for half of global anode material production. The top-six companies are all Chinese and account for two-thirds of global production capacity. The largest players include Ningbo Shanshan (China), BTR New Energy Materials (China), and Shanghai Putailai New Energy Technology (China).

- In March 2022, the United States invoked the Defence Production Act to rapidly boost US production of critical minerals for EV and storage batteries, focussing on lithium, nickel, cobalt, graphite and manganese.

- The United States plays a more minor role in the global EV battery supply chain, with only 10% of EV production and 7% of battery production capacity.

⏲️ Upcoming potential share price catalysts list

Results expected in the near term:

- GGE is drilling its maiden helium well in Utah, aiming to make a commercial helium discovery (memo).

- IN PROGRESS: GGE has confirmed a new helium discovery and is planning a follow up flow testing program in Q3 2022.

- Update: This week, GGE re-iterated guidance for the upcoming flow testing program, confirming that the rig would be on site in ~ mid August.

- PRL signing a Joint Development Agreement with its partner, Total Eren, to materially de-risk its WA Green Hydrogen Project (memo)

- IN PROGRESS: The signing of the “Joint development agreement” (JDA) with TotalEnergies. PRL’s deadline to sign the JDA is now set for 31 July 2022.

- Update: No progress.

- IVZ to drill its giant gas prospect in Zimbabwe - we have been waiting two years for this event (memo).

- IN PROGRESS: Drilling is scheduled for mid-August. IVZ says it is considering three separate farm-in offers.

- Update: IVZ posted on their official LinkedIn page earlier in the week that the rig has begun to arrive at the drill site piece by piece in a large truck convoy. IVZ will need to assemble the rig in anticipation of the first drill well scheduled for mid-August.

- KNI is drilling its cobalt targets in Norway (memo).

- IN PROGRESS: KNI has completed its first cobalt drilling program in Norway, hitting visible cobalt in 7 out of the eight holes at their highest priority target as part of its expanded 11 diamond drillhole campaign.

- Update: With the drilling program complete, we are watching closely to see what comes of the assay results and whether these visible cobalt intercepts translate into an economic discovery. See our latest KNI note here: KNI kept drilling after it kept seeing visible cobalt - assay results should get interesting.

- BPM is drilling its lead zinc prospect in WA’s Earaheedy Basin close to Rumble Resources’ recent discovery (memo)

- IN PROGRESS: Drilling is now complete, and assays from the program are pending.

- Update: BPM initially planned for a ~7,500m AC/RC drilling program but instead completed ~3,740m of drilling. On site, XRF readings confirmed lead-zinc mineralisation across five key areas of interest. Once assays come in, BPM will identify key target areas and re-enter the project. See our coverage of the drilling program here: BPM Sees Lead-Zinc Along Strike From Rumble, Assay Results Next.

- PFE is drilling its polymetallic (Hellcat) project (memo)

- IN PROGRESS: PFE is doing 1,700m of diamond drilling across four EM targets at its Hellcat project targeting base/precious metals. Drilling has commenced.

- Update: No progress.

- LNR (formerly FNT) commencing drilling for rare earths (memo)

- IN PROGRESS: LNR is still in the process of getting approvals, so we are not sure exactly when drilling will occur. It may be later than most on the above list, but we are keeping an eye on progress.

- Update: No progress.

🗣️ Quick Takes

Here are this week's Quick Takes:

EMN: Euro Manganese Joins the Global Battery Alliance

EV1: 24% more yield from graphite? Elite purity?

EV1: EV1’s battery cycling testwork - graphite is “super-premium”

GGE: Helium project ownership increases to 70%

LCL: More high grade gold hits for Los Cerros

MNB: First tranche of placement shares issued

MNB: World's biggest phosphate exporter considering quotas

MNB: BlackRock’s Larry Fink worried about food supply

PRL: Australia - “the new Saudi Arabia of green energy and minerals"?

TEE: More domestic gas needed to fix the east coast crisis

TG1: Company presentation - Three drilling programs back to back

TTM: Managing Director increases shareholding

Macro (lithium): Tesla profit jumps, ASX lithium stocks jump

Macro (helium): Samsung may build US$200B of chip facilities in Texas

General: Noosa Mining Investor Conference round-up

📰 This week on Next Investors

⚠️NEW INVESTMENT ALERT⚠️

SGA: Our Latest Investment

On Friday, we announced the latest addition to the Next Investors Portfolio, Sarytogan Graphite Ltd (ASX: SGA).

SGA owns 100% of a giant graphite resource in central Kazakhstan, which has the highest grade graphite resource and second largest graphite resource of any ASX-listed company.

SGA began trading on the ASX on Monday, having raised $8.65M during its IPO. We participated in the IPO after having earlier invested during pre IPO seed raises.

As long term holders, our big bet is that we want to see SGA develop its giant graphite resource, which we believe has the potential to catch the interest of major miners and become a world-class graphite mining operation.

📰 Read our full Note: Our Latest Investment is...

KNI sees visible cobalt in first drill program

This week our European battery metals exploration investment Kuniko (ASX: KNI), has completed itsfirst cobalt drilling program at its Norwegian cobalt project.

The expanded 11 diamond drillhole campaign centred around three key targets identified using modern geophysics/geochemical surveying.

Interestingly KNI hit visible cobalt in seven of the eight holes drilled at its highest priority target, where historical drilling had completely missed the geophysical target.

KNI also hit visible cobalt mineralisation 280m along strike to the north of the high priority target in another drillhole which could signal an increase in the potential strike zone.

KNI has now defined a mineralised zone open to depth and along strike to the north.

We now await assay results, which are due in late September, at which point we should have a better grip on whether KNI has made an economic cobalt discovery.

📰 Read our full Note: KNI kept drilling after it kept seeing visible cobalt - assay results should get interesting

BPM Sees Lead-Zinc Along Strike From Rumble, Assay Results Next

Our micro cap exploration investment BPM Minerals (ASX: BPM), has completed its first ever drilling program at its lead-zinc project, 40km northwest along strike from Rumble Resources’ lead-zinc discovery in WA.

Portable XRF readings confirmed lead-zinc mineralisation across five key areas of interest.

This was within the same rock formations (Frere/Yelma) and around the same depths where Rumble first made its discovery in April 2021.

Rumble’s initial discovery intercept was from a depth of only 62m, while BPM’s intercepts all sit within depths of 40m-100m.

We also noted that BPM fell short of the 7,500m of drilling it had initially planned, which marks a shift in exploration strategy - but we don't mind seeing this.

The decision to stop drilling early was not because BPM didn't hit anything of interest.

BPM’s smaller drilling run will give it time to work out what it has found and maintain cash reserves to drill again armed with more information.

With current market sentiment for cash burning explorers low and capital harder to come by, by taking this approach, BPM can preserve capital and drill only the BEST targets based on a better understanding of its project.

As soon as the assays from this first round of drilling come in, the company plans to put together a set of key target areas and re-enter the project.

📰 Read our full Note: BPM Sees Lead-Zinc Along Strike From Rumble, Assay Results Next.

Have a great weekend,

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.