Markets showing life after June tax loss selling

Published 09-JUL-2022 22:14 P.M.

|

18 minute read

The financial year has ended and the market seems to be showing signs of life in the first six trading days of FY23.

Every year we expect May and June to be filled with more selling than buying but this year was especially bad.

With a macro backdrop filled with uncertainties from the war in Ukraine to interest rate rises all over the world, selling in the last two months of the financial year was relentless.

With ‘sell in May, go away’ done and the ‘tax loss selling’ in June absorbed it's finally July and the brutal selling pressure seems to have eased.

Across our Portfolio, we are seeing companies moving off of the lows they hit over the last two months, and often moving off very little volume and no news at all.

This is just the way the markets work.

In May and June, there were very few buyers and a whole lot of sellers leading to share prices being smashed.

Only six trading days into the new financial year and the markets seem to be working in the opposite way.

Buy orders are being met with very few sellers leading to unusually high share price moves to the upside.

Some examples across our Portfolio are as follows:

Kuniko Limited (ASX:KNI)

KNI’s share price briefly touched 50c per share towards the end of June, only 6 trading days into FY23 the share price has now settled at 71c per share.

That’s a paper gain of ~42% for the brave investors that were willing to buy into the tax loss selling in June.

On top of this, those who bought in June get the added upside of any good results from the company’s drilling program at its Norwegian cobalt projects where KNI has already intercepted visible cobalt mineralisation.

BPM Minerals (ASX:BPM)

Another of our Investments that’s recovering in the new FY is BPM, which briefly touched a low of 10.5c per share.

At the time, the company was trading at a <$1M enterprise value, a level which we think was motivated purely by tax loss selling and completely unrelated to the company’s fundamentals.

BPM is currently in the middle of drilling its Hawkins Project, along strike from Rumble Resources “Chinook” lead-zinc discovery.

With the share price now around 15.5c per share, those who purchased at the June bottom would already be up ~48% on their investment.

All of this before any of the drilling results from the Hawkins Project and with leverage to re-rate off the back of any surprising drill results.

Oneview Healthcare (ASX:ONE)

Another one of our Portfolio companies that got caught up in the June tax loss selling was ONE, briefly touching a low of 10.5c per share.

The company had no news throughout June, and in May announced the signing of a deal with BJC Health System - one of the largest nonprofit healthcare organisations in the United States.

ONE’s share price closed at 15c per share on Friday representing a ~48% gain for anyone who managed to pick the bottom in June.

Province Resources (ASX:PRL)

Perhaps one of the hardest hit companies in our Portfolio, PRL’s share price touched 5c per share towards the back end of June.

With no news, there were no changes to PRL’s fundamentals yet its share price fell significantly.

In a previous weekend update, we picked this as one of the companies that we thought would see a lot of tax loss selling... and it played out almost like clockwork.

With the share price closing at 9.1c per share yesterday, anyone who had the nerve to venture out into the markets and buy shares in PRL last month would be up around 80% in just a week or two.

With the deadline for the Joint Development Agreement (JDA) with Total Eren set for the 31st of July 2022, we also have some immediate newsflow to look out for which is a positive here.

Elixir Energy (ASX:EXR)

This was another one of our Portfolio companies that ran into some heavy selling in June.

The share price touched a low of 11c towards the middle of last month. Even an MOU with a subsidiary of Japanese Conglomerate SoftBank wasn't enough to re-rate the company’s shares - a sign of just how relentless the selling in June was across the markets.

We covered that MOU in our last EXR note, which you can read here: EXR Inks Green Hydrogen MoU with a SoftBank Subsidiary.

Only a few weeks have passed and EXR is already back up to 16c per share in the first week of July, meaning the share price is now ~45% higher than its June low.

Evolution Energy Minerals (ASX:EV1)

Another of our Portfolio companies that ran into some tax loss selling was EV1, briefly touching a low of 26.5c per share.

The selling came despite EV1 appointing a front end engineering and design (FEED) contractor for its graphite project in Tanzania, another signal to us that the selling was indiscriminate and unrelated to company execution.

Since then, EV1 put out an update on some downstream test work that is currently being done, with the ultimate aim of trying to work out how its graphite could be used to produce high value add products that could fetch multiples of the price that its raw product could be sold for.

We covered that news in our EV1 note earlier this week: EV1’s Graphite Meets Purity Standards – Good for Batteries and Nuclear Energy.

The market seems to have regained momentum and is rewarding these developments, pushing EV1’s share price back up to 37.5c per share to ~42% above the June low.

This phenomenon wasn't limited to these companies, we observed this type of price action across our Portfolio.

There is a quote from famous value investor Benjamin Graham who says, “in the short run, the stock market is a voting machine. Yet, in the long-run, it is a weighing machine”.

The premise behind the quote is that in the short run factors such as geopolitical tensions, interest rate rises, the “sell in May, go away” thinking and even tax loss selling can create downward pressure on company share prices.

But in the long term, share prices will ultimately move in tandem with fundamental changes in a company’s business and based on the progress a company makes with respect to its business objectives.

This has never been more evident than in June when it seemed that no matter what a company did, its share price was sold off.

For those brave enough to dip their toes into the market, times like this present good buying opportunities, as evidenced by the move in PRL’s share price which is already up 82% from its June lows.

With all of this in mind and the new financial year now fully underway, it is time we take stock of the companies in our Portfolio.

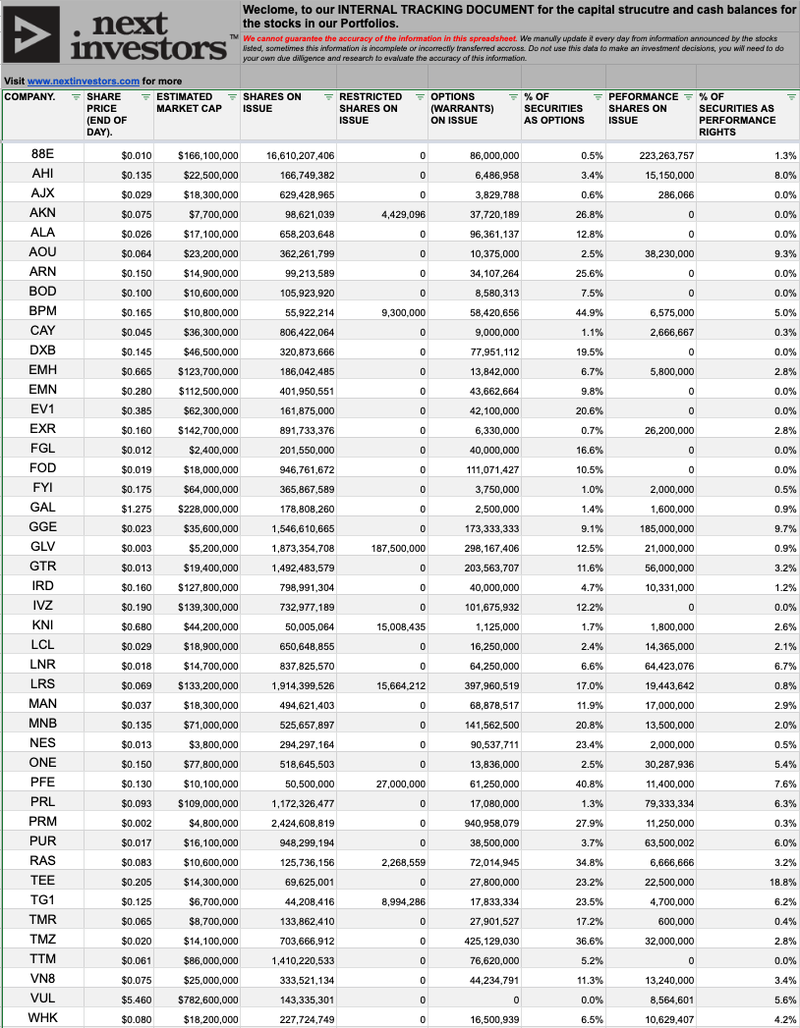

Tracking a Company’s Cap Structure

When investing in lots of companies it is important to get an overview of where each company sits relative to the other.

One way that we do this is by comparing the capital structure. We do this through an internal portfolio management document (which we will share with you today), that gives us a holistic overview of what shares are on issue, options on issue, performance rights and director's holdings.

Each one of these ‘securities’ makes up the capital structure of the business - and it’s important to identify who owns the securities and the potential ‘conditions’ attached to each.

1 Shares on issue.

The most basic form of a security is a share. This is a portion of ownership or ‘equity’ over the company - and gives the holder certain rights.

We track the total number of ‘shares on issue’ as it gives a rough idea of the value of the company.

The ‘market cap’ is the relative value of the company, and you can find it by calculating “number of shares on issue” x “share price”.

Using the market cap can be extremely useful in comparing different companies within the same sector that have different share prices and a different number of shares on issue.

It is our most common form of valuing and comparing companies.

2. Options on issue.

An option is not a share, but a right to purchase a share at a predetermined price within a certain time period.

For example: An investor owns 100,000 options exercisable at 10c expiring 31 December 2022.

Here, the investor has a right to purchase 100,000 shares by paying 10c per share (or $10,000), before the expiration date of 31 December 2022.

Knowing when options expire and the exercise price is important information that helps inform investors of any potential dilution that may be on the horizon.

The option is considered ‘in the money’ if the current share price is above the exercise price of the options.

If there is a large number of options in the money, the company will likely have them exercised.

This can be both good and bad.

Good because it raises money for the company (the investor has to pay a price to convert the options into shares), bad because once the options are exercised, the investor might immediately sell it on market and add a downwards pressure to the share price.

In any case, it’s important to see how many options are on issue at any given time and at what price these are likely to come to market so that we can make an informed investment decision.

3. Performance rights and incentives

Performance rights are also not shares, they are a promise to issue shares to the management of a company if certain performance incentives (called vesting conditions) are met within a certain time period.

When a performance right vests (on successful completion of a milestone) the company will issue shares directly to the holder causing a dillutionary effect which can reduce the market cap of the company.

We like performance rights because it aligns the interest of key management and retail investors.

Generally, there are two types of performance rights:

- Share price incentive: These are performance based incentives that if a company’s share price hits a certain level by a certain time, the directors (and management) will be issued shares.

- Company performance incentive: These are performance incentives that relate to hitting key milestones for the company. For example, delivering a Scoping Study, achieving a minimum JORC resource estimate, or delivering on a sales budget.

Understanding the performance rights help inform investors as to the motivation of the management and the team around them.

We think that companies that have both share price and company performance incentives for their key management tend to have the best balance between company promotion and business execution.

Performance rights are generally proposed at a company’s annual meeting, when the incentives of key management are set, and then voted on by shareholders.

For investors, knowing how many performance rights are on issue and the vesting conditions behind those performance rights can help to frame the interpretation of company decisions.

Below is a screenshot of the capital structures for all of the companies held in our Portfolios, and a link to the internal document that we use to track each company in our Portfolio:

Click here to access our internal document

We track these live as each company announces movements on their registers.

Click on the different tabs at the bottom of the sheet to see details of options, performance shares and director holdings.

Please note: We cannot guarantee the accuracy of the information in this spreadsheet. We manually update it every day from information announced by the stocks listed, sometimes this information is incomplete or incorrectly recorded. Do not rely on this data to make an investment decisions, you will need to do your own due diligence and research to evaluate the accuracy of this information.

⏲️ Upcoming share price catalysts list

Results expected in the near term:

- GGE is drilling its maiden helium well in Utah where it’s aiming to make a commercial helium discovery (memo).

- IN PROGRESS: GGE has confirmed a new helium discovery and is now planning a follow up flow testing program in Q3 2022.

- Update: No progress has been made this week.

- PRL signing a Joint Development Agreement with its partner, Total Eren, to materially de-risk its WA Green Hydrogen Project (memo)

- IN PROGRESS: The signing of the “Joint development agreement” (JDA) with TotalEnergies. PRL’s deadline to sign the JDA is now set at 31 July 2022.

- Update: This week PRL confirmed it had received traditional owner consent over a portion of its project area, we covered this announcement in the following note: PRL Secures Native Title Consent for HyEnergy Project Land Access.

- IVZ to drill its giant gas prospect in Zimbabwe - we have been waiting two years for this event (memo).

- IN PROGRESS: Drilling is now scheduled for August. IVZ says it is considering three separate farm-in offers.

- Update: This week IVZ upgraded its prospective resource by a factor of 2.7x increasing the upside potential for the upcoming drilling program in August, we covered the announcement in the following note: IVZ’s resource is now 2.7x bigger - Drilling in August.

- KNI is drilling its cobalt targets in Norway (memo).

- IN PROGRESS: KNI confirmed that it has completed ~2,500 metres of its total ~3,000m drilling planned.

- Update: No update this week. We are waiting for the assay results from the visible cobalt mineralisation that was intercepted last week, to see our coverage of those intercepts see our last KNI note here:Visible cobalt mineralisation in all 5 drill holes.

- BPM is drilling its lead zinc prospect in the Earaheedy Basin close to Rumble Resources’ recent discovery (memo)

- IN PROGRESS: BPM is completing a ~7,500m AC/RC drilling program at its Hawkins project (along strike from Rumble’s discovery).

- Update: No progress has been made this week.

- PFE is drilling its polymetallic (Hellcat) project (memo)

- IN PROGRESS: PFE is doing 1,700m of diamond drilling across four EM targets at its Hellcat project targeting base/precious metals.

- Update: PFE commenced drilling this week, we covered that announcement in a Quick Take which you can read here: Drilling commences at Hellcat.

- LNR (formerly FNT) commencing drilling for rare earths (memo)

- IN PROGRESS: LNR is still in the process of getting approvals so we are not sure exactly when drilling will occur. It may be later than most on the above list, but we are keeping an eye on progress.

- Update: No progress has been made this week.

🗣️ Quick Takes

Here are this week's Quick Takes:

DXB: Promising results from DXB’s R&D pipeline

GAL: Trading halt for assay results at Norseman PGE discovery

GAL: 💪 IGO & Mark Creasy cornerstone investors in GAL's cap raise

GAL: 📈 Mark Creasy and IGO back $20.4M raise to accelerate drilling

GTR: Nuclear power labelled “Green” by the European Union

LCL: Highly encouraging testwork paves way for Scoping Study

LRS: Gold project option exercised ahead of non-core asset divestment

MNB: Solutions being sought for the food crisis in Africa

PFE: ✅ Drilling commences at Hellcat

PRL: Traditional owner consents secured for green hydrogen project

TMR: More visible gold intercepts, assays coming soon

VUL: Environmental and community support for geothermal project

VUL: Binding agreement with leading Italian geothermal group

Macro (commodities): China considering US$220Bn in infrastructure stimulus

Macro (commodities): VW CEO breaks down batteries and supply chain issues

Macro (hydrogen): Bill Gates backs start-up for hydrogen storage & transportation

Macro (hydrogen): Bill Gates “Green hydrogen would be massive for clean energy”

Macro (gas): EU Parliament to consider gas a "Green" energy source

Macro (gas): Gas shortage the catalyst for a global recession

📰 This week on Next Investors

IVZ’s resource is now 2.7x bigger - Drilling in August

Earlier in the week our 2020 Energy Pick of the Year, Invictus Energy (ASX: IVZ) upgraded its prospective oil and gas resource by 2.7x.

IVZ upgraded its prospective resource at its Mukuyu prospect to a giant 20 trillion cubic feet (Tcf) and 845 million barrels of gas condensate.

A prospective resource that now stands at a total of 4.3 billion barrels of oil equivalent on a gross mean unrisked basis.

This entire prospective resource sits inside a single prospect (Mukuyu-1) across eight stacked targets, meaning there could still be multiple follow up exploration prospects that contribute to an even larger project size.

IVZ’s project was already the largest undrilled conventional oil and gas exploration prospect in onshore Africa.

With the prospective resource now 2.7 times larger, the upside case for IVZ’s project has set it up as one of the largest conventional oil and gas exploration prospects globally.

To put IVZ’s prospective resource upgrade into perspective - and comparing it to actual discoveries and resources - as of 2019, BP’s “Greater Tortue Ahmeyim” discovery in Mauritania was considered one of the largest discoveries in Africa.

That project is currently being developed and is expected to produce ~15 trillion cubic feet of gas over its 30+ year production life.

Another is the Bass Strait, offshore Victoria, which has been Australia’s biggest source of domestic gas supply. At its peak, it had reserves of ~10 trillion cubic feet.

IVZ’s updated prospective resource is almost 3.5x the size of BP’s discovery and nearly 2x the size of one of Australia's most prolific oil and gas fields, the Bass Strait.

Drilling of the Mukuyu-1 well is now expected to commence in August.

📰 Read our full Note: IVZ’s resource is now 2.7x bigger - Drilling in August

PRL Secures Native Title Consent for HyEnergy Project Land Access

This week our 2021 Small Cap Pick of the Year Province Resources (ASX:PRL) made important progress towards tenure for its hydrogen project in WA.

PRL announced that it has secured land access consent from native title groups covering ~870 square kilometres of land.

This 870 square kilometres is part of PRL’s total land holdings in the Gascoyne region, which totals ~2272 square kilometres.

To our knowledge, no other green hydrogen project in Australia has secured this yet - which we think means it is currently one of the most advanced hydrogen projects in Australia.

Land rights and permitting isn’t the ‘sexiest’ part of the project’s life cycle, but we think it is one of the most critical de-risking factors - not only to investors but to potential financing partners like Total Eren.

We think that without certainty over licensing and permitting, partner Total Eren could be reticent to provide major funding to the project.

So the news this week is a big step not only toward the project development but also the major catalyst we are waiting for PRL to execute - Joint Development Agreement (JDA) with Total Eren.

The deadline for the MoU has recently been extended to 31 July 2022, this is the new timeframe for PRL that we are watching out for.

📰 Read our full Note: PRL Secures Native Title Consent for HyEnergy Project Land Access

📰 In our portfolios 🧬 🦉 🏹

🦉Wise-Owl

EV1’s Graphite Meets Purity Standards – Good for Batteries and Nuclear Energy

This week our 2021 Wise-Owl Pick of the Year, Evolution Energy Minerals (ASX:EV1) put out an update on what EV1’s EV1’s downstream strategy will look like.

Preliminary test work results from a partnership with an unnamed US technology partner confirmed that EV1’s Tanzanian graphite has extremely low levels of naturally occurring Molybdenum and Boron which are considered impurities in graphite.

These low levels of impurities differentiate EV1’s graphite and put forward two different potential use cases for EV1’s graphite. The first is in premium performance batteries; the second in the nuclear industry where graphite products sell for up to US$30,000 per tonne.

The results from some impurity analysis work detailed EV1’s graphite as having:

- Molybdenum concentrations <0.5 parts per million – Almost two times below the threshold for graphite used in premium performance batteries. This type of low molybdenum purified graphite currently sells for between US$8,000-$18,000 per tonne.

- Boron concentrations <2 parts per million – Below the threshold for impurities for graphite that can be used in the nuclear industry. A positive first sign that EV1’s graphite may be able to produce qualified purified graphite that sells for approximately US$30,000 per tonne in the nuclear industry.

This means that pending further test work – EV1 is currently on track to sell to BOTH the battery industry AND the nuclear industry.

The impurity analysis is the first stage of testing EV1’s graphite fines product to see if it is suitable for these types of high value add graphite products.

Battery anode test work is ongoing with further results expected in the coming weeks.

The next stage will assess the purification, milling and shaping processes to determine whether EV1’s graphite can achieve the required rates for its product to be suitable for high value add products.

This bid to capture high-margin markets is all part of EV1’s downstream strategy, and we think it promises to add significant value to EV1’s Tanzanian graphite project.

📰 Read our latest full Note: EV1’s Graphite Meets Purity Standards – Good for Batteries and Nuclear Energy

Have a great weekend,

Next Investors

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.