IVZ reaches 10 bagger status, lithium day wrap and more...

Published 21-NOV-2022 10:52 A.M.

|

12 minute read

With a bit of life creeping back into the market, we saw another of our long-term Positions achieve “10 bagger” status this week.

A “10 bagger” is when a stock price increases 1,000% - and they don’t come around very often, especially in a wonky market like we’ve experienced in 2022.

Holding on for a 1,000% increase usually requires a lot of patience, with plenty of ups and downs along the way that will test one's resolve to hold.

That company is our 2020 Energy Pick of The Year Invictus Energy (ASX:IVZ) which released another positive drilling update on Friday.

We’ve been holding a position in IVZ since September 2020 at an Initial Entry Price of 3.8 cents and by Wednesday at midday it had punched to a high of 40.5 cents from Friday’s (last week) low of ~10.5 cents.

It’s white knuckle stuff, as wild swings have moved IVZ shares every which way on the smallest deviation from ultimate success.

Our strategy is that a few of our Investments reach a 1,000% gain from Initial Entry, making up for the inevitable failures that are expected in every small cap portfolio.

So it’s very pleasing to see this goal accomplished again.

IVZ now joins the Next Investors “10 bagger” club of:

- Vulcan Energy Resources (ASX:VUL)

- Euro Manganese (ASX:EMN)

- Province Resources (ASX:PRL)

- Elixir Energy (ASX:EXR)

- Latin Resources (ASX:LRS)

- 88 Energy (ASX:88E)

- Kuniko (ASX:KNI)

A 10x share price rise is our general goal and we have over 40 bets placed which increases the chances of hitting one - also bear in mind these are measured from our Initial Entry Price numbers and are mainly “paper profits”.

Our true realised returns are substantially less when measured in actual “profit taken” - given we always hold a position beyond a share price hitting 10x return and share prices will often come back down off high points.

More to come for IVZ? - we will find out in less than 7 days.

IVZ has so far delivered all but one of the news announcements required to officially declare an “oil & gas discovery” on the first of 14 drill targets in the Cabora Bassa basin.

The final bit of news needed for IVZ to declare a “discovery” is “to bring a hydrocarbon sample to the surface”.

Investors will likely infer that if a “discovery” is announced on the first target means a higher likelihood of success on the other 13 targets, which could result in a share price re-rate if IVZ delivers that critical first basin opening discovery.

According to the IVZ news released on Friday, wireline logging has already indicated multiple gas bearing zones, and we are waiting for the equipment to arrive to test if an oil & gas sample can be brought to the surface.

IVZ says this will take another 5 to 7 days - so hopefully we will find out before next Friday...

How share prices react to an oil & gas discovery is notoriously hard to predict, and is usually a function of how much “expectation of a positive result” is already built into the share price BEFORE the result is announced.

IVZ’s share price took a material downward turn in the weeks leading up to the expected drill result, but has come back strong after a few good announcements ahead of the major news we are hoping for this week - an official discovery.

Other “pre-result” oil & gas explorers we followed like Recon Africa and 88 Energy hit over a $1 billion market cap prior to their drill result, and then came off after failing to bring a sample to surface (note: we weren’t investors in Recon Africa).

IVZ is currently sitting at a sub-$300M market cap pre-result, and to us, it looks like the market is not currently pricing in a discovery when compared to 88 Energy and Recon Africa.

Back in 2012 Africa Oil Corp was trading at around $200M pre-discovery, re-rating to over $1BN when their first discovery was announced.

It’s going to be a big week for IVZ and we expect the share price to make a significant move upwards OR downwards based on whether the next announcement is a discovery or not.

In line with our plan, once IVZ hit the 10x rise last week, we sold 15% of our position to de-risk, but are still holding on to a significantly larger position than usual into the result.

We should know by Friday if holding such a big position into the result was a good move or not...

We also have nearly double the amount of shares sold of 40c options from the last cap raise so we can always buy those shares back in the event of a discovery and material share price re-rate.

Investing in high risk oil & gas drill campaigns is a rollercoaster of emotions and definitely not for the faint of heart - remember to understand the risks and invest only what you are 100% prepared to lose.

Speaking of 10x returns from high risk drilling... New Portfolio Addition coming on Monday.

Some of the team took a trip to Perth late last week to meet a few companies we are looking at Investing in.

The talk of the town is WA1’s recent Niobium and Rare Earths discovery in the West Arunta province in Western Australia.

This confirmed discovery has opened up a new Rare Earths and Niobium province that saw the WA1 share price surge from 13c to a high of over $3 - officially firing the starting gun for other companies to try and make new discoveries in the West Arunta Province.

On Monday we will be adding Lycaon Resources (ASX:LYN) to our Portfolio after they acquired a new Rare Earths and Niobium project near WA1’s discovery.

We are hoping that LYN can make its own Niobium and Rare Earths discovery in the West Arunta province, with drilling expected in mid-late 2023.

Be warned however, drilling an unexplored project is a high risk proposition - if it works (like for WA1) the results can be incredible, but there is a high likelihood it may fail and the share price will come off.

We have also observed that Nearology plays rarely succeed - as we have seen over the years with failed investments in the Fraser Range Nickel rush, the Julimar Province PGE rush and the Earaheedy Basin lead-zinc rush.

But... small cap exploration investing is all about placing bets hoping for one to hit that 10x return, which is what we are doing with LYN.

LYN’s upcoming drilling is certainly high risk for high reward, and like with all our exploration investments we are fully prepared for it to fail.

There is still a while before LYN’s first drill and result, so plenty of room for a share price rise on pre-drill speculation during the first half of 2023 that could offer a chance de-risk, especially if WA1 or its other nearby neighbours deliver more results.

Learn more about how nearology works and our nearology rating scale - we score LYN at between 3 and 4 which is near the best level.

We will be adding LYN to our Catalyst Hunter Portfolio and launching our LYN Investment Memo on Monday.

Lithium hiccup?

This week some of the team attended an event called “Lithium Update by the Experts” in Melbourne which featured keynote speaker Joe “Mr Lithium” Lowry.

The series of presentations also included updates from our existing lithium Investments, Latin Resources (ASX:LRS) and European Metals Holdings (ASX:EMH).

And if there’s one single takeaway about lithium from our note this weekend - it’s that we’re bullish on the battery metal for the rest of the current decade.

That may sound outlandish, particularly as a lithium “crash” has permeated the headlines again.

Hear us out though.

The bull case comes from Canaccord Genuity’s Reg Spencer who presented an economic deep dive on lithium at the start of the “Lithium Update by the Experts” event which laid an excellent foundation for the presentations and subsequent discussions.

Without going too far into the nitty gritty, the model of lithium supply and demand that Reg is working with builds in some key factors (these are our interpretations):

- More supply will take time - the argument that there is a supposed glut of supply slated to come on line in the coming years which will relieve price pressures needs to be counterbalanced by historical facts - the lithium industry has a poor track record of delivering projects into production on time. We saw the charts and the numbers - it always takes longer than expected.

- EV penetration is not the favoured signal of demand growth - rather it is the battery “gigafactories” themselves which need to be taken into account. There are different battery pack sizes and the gigafactory demand is a more closely aligned signal on future demand growth. Look to the factories before the market penetration numbers.

- Growth in demand has been consistently outstripped - Reg, by his own admission, says that his model is probably conservative when it comes to demand growth. Each year it is more, and at some point this underestimation needs to become a forecasting variable.

And of course, Joe Lowry’s presentation was a real highlight. (You can catch Joe’s Podcast here).

Joe was talking about lithium way back when lithium wasn’t popular and wasn’t on investors’ radar - like a lithium hipster.

As perhaps the foremost expert on lithium in the world, Joe’s words carry weight in the industry.

After chewing through the key points, Joe’s presentation built on a common outlook with Cannaccord’s Reg Spencer.

The panel discussion that followed was detailed - Joe shared the stage for a Q&A session with prominent lithium experts, Peter Oliver (ex- Tianqi Lithium Corporation, current Latin Resources) and Ken Brinsden (ex-Pilbara Minerals, currently Patriot Battery Metals)

Here were our key takeaways from Joe’s presentation and the panel discussion:

- Lithium shouldn’t be thought of as a commodity - it’s a specialty chemical and different formulations have different values. In that sense, it’s not like iron ore where it's largely all the same around the world. So processing and quality vary greatly which leads to different prices. This flows through to the mining companies and the concentrates they produce.

- Chinese demand for slightly shorter range vehicles shouldn’t be ignored - just because the West expects certain performance out of their cars doesn’t mean new battery chemistries that favour slightly shorter ranges such as lithium ferro-phosphate (LFP) batteries are without merit. Nickel is important to higher performance chemistries, but lithium remains an irreplaceable constant.

- Geopolitics is less important than performance - this was an overarching theme from the discussion and panel members agreed. China is currently a dominant force in EVs and although Europe is a jurisdiction with extremely fast growth - the underlying price-relative performance of the vehicles is more important than the origins of the battery chemistry and cars. Joe forecasted that more easily deployable, shorter range Chinese LFP chemistries would retain value in a variety of environments.

We note that one of our Investments, Minbos Resources (ASX:MNB), is exposed to the LFP battery market via a Strategic Cooperation Agreement with a syndicate of investors looking at securing phosphate offtakes for this battery chemistry.

In China, LFP batteries command 44% of the EV market and roughly half or more of all Teslas made in the first quarter of this year had phosphate in their batteries.

It’s certainly food for thought in this brave new battery metals world.

And as we’ve hinted at in previous weekend notes, we’re looking to add to our exposure in lithium.

Gold sentiment turning?

Another observation from our trip to Perth is there is a small buzz starting around gold, with talk of beaten down gold explorers being approached with offers of capital from overseas funds.

It’s still early in our prediction that gold will come back in 2023, but some of the early signs are there, and we will likely announce a new gold Investment before the year is out.

As always, we appreciate reader feedback and if you’ve got a company in mind or general market commentary we’d love to hear from you.

You can reach out to us by hitting reply to this email.

🗣️ This week’s Quick Takes

AKN: More copper at Emull - resource update pending.

EXR: Gas flared from pilot production well

GAL: Palladium and nickel grades increasing - 20+ more assays pending

IVZ: More elevated gas shows as total depth reached

IVZ: Preliminary results indicate multiple potential gas bearing zone

PFE: Not much doing from initial Hellcat assays

PFE: PFE Completes Manganese Drilling - Visuals Identified

TG1: First batch of assays from WA copper project

TG1: Rare earths in rock chips?

VN8: VN8 to benefit as Voiteck delivers performance milestone

VUL: Successful in-house lithium extraction tech developed

This week in our Portfolios 🧬 🦉 🏹

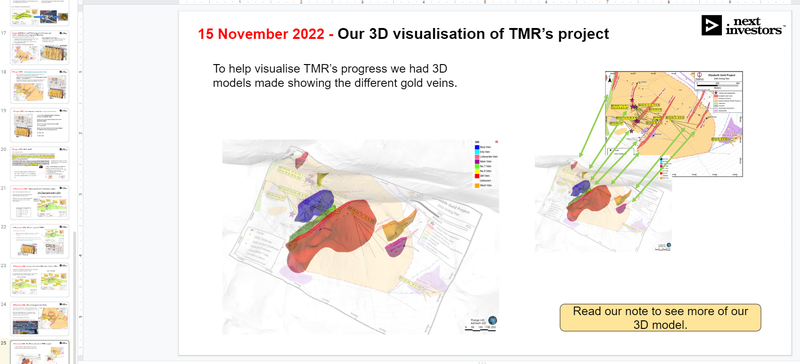

Tempus Resources (ASX: TMR)

This week we put out an update on our long held junior gold exploration Investment Tempus Resources (ASX:TMR).

TMR recently completed its 40-hole 2022 drilling program - one of the companies most successful drilling programs after visible gold intercepts across multiple gold vein systems.

From the 40 holes drilled, TMR has ~21 assay results pending, all due within the coming weeks.

To help us understand what we are looking for with TMR, we created a 3D model using TMR’s publicly available drill hole information.

It’s a great look at what TMR has done so far and where the company is going next:

📰 Read our full Note: TMR’s gold project visualised in 3D

⏲️ Upcoming potential share price catalysts

Updates this week:

- IVZ: drilling its giant gas prospect in Zimbabwe

- This week IVZ put out two updates from its drilling program. The first confirmed elevated gas levels 135x background levels (an increase on the previously reported 65x). Then IVZ confirmed that its wireline logging program had started and that while the company is waiting for equipment needed to finalise testing to arrive, IVZ will continue drilling down to a depth of ~3,800m (beyond the initial 3,500m targeted).

- GAL is undertaking a second round of drilling at its Callisto PGE discovery in WA.

- This week GAL put out a single assay result from the deeper diamond drilling the company is doing to the south of its PGE discovery. The grades were some of the best GAL has hit to date. - see our Quick Take on the news here.

- PFE: Assay results for manganese (Weelarrana) project, and for polymetallic (Hellcat) project.

- This week PFE released the assay results from the Hellcat (polymetallic) project in WA - see our Quick Take on the news here.

No material news this week:

- LNR: Assays pending from rare earths drilling along strike from Hastings Technology Metals

- GTR: Drilling results for uranium in Wyoming, USA.

- TYX: Drilling for lithium in Angola.

- RAS: Drilling for lithium next door to Core Lithium in the Northern Territory.

- PRL: Awaiting final execution of a joint development agreement with Total Eren

- TTM: Drilling its copper porphyry target in Ecuador.

Have a great weekend,

Next Investors.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.