New Acquisition for VN8 as “Hunt for Growth” Strategy Continues

Disclosure: The authors of this article and owners of Next Investors, S3 Consortium Pty Ltd, and associated entities, own 3,273,182 VN8 shares at the time of publication. S3 Consortium Pty Ltd has been engaged by VN8 to share our commentary and opinion on the progress of our investment in VN8 over time.

Four acquisitions in 19 months...

Our small cap telco investment Vonex (ASX:VN8) is continuing to follow the tried and tested telco playbook of rapid growth through acquisitions of smaller entities.

The goal for VN8 is to get bigger by claiming and retaining market share through buying smaller telcos - which will hopefully lead to VN8 getting taken out by a bigger telco player themselves.

Yesterday, VN8 announced its latest acquisition - this time it's South Australian telco Voiteck that will soon be incorporated into the VN8 group.

For those new to the story, VN8 provides telecommunication solutions primarily for Australian small and medium enterprises (SME).

VN8 has a significant footprint in NSW, Victoria, Queensland and WA - and with yesterday’s deal it has now got a foothold in the SA market.

Here are all the key details on VN8’s latest acquisition - we will unpack the deal in more detail below.

Key deal metrics:

- Voiteck has ~ 1,000 customers and over 10,000 PBX users - which increases VN8’s users to over 90,000 post transactions.

- In the 12-month period to 30 September 2021, Voiteck delivered:

- pro forma EBITDA of $600k;

- revenue of $3.3M; and

- annualised recurring revenue (ARR) of $2.6M.

Acquisition consideration to be paid by VN8:

- Total upfront consideration of $2.75M comprises $2.2M cash, and $0.55M in escrowed VN8 shares.

- Cash to be paid using VN8’s existing cash reserves, deal to be completed in January 2022.

- The upfront consideration represents a < 4.5x multiple of Voiteck’s pro forma EBITDA

- Acquisition is double digit earnings accretive on a full year basis

- Additional consideration of up to $2.75M may be paid to vendors subject to the realisation of certain synergies and EBITDA growth targets delivered in FY22 and FY23.

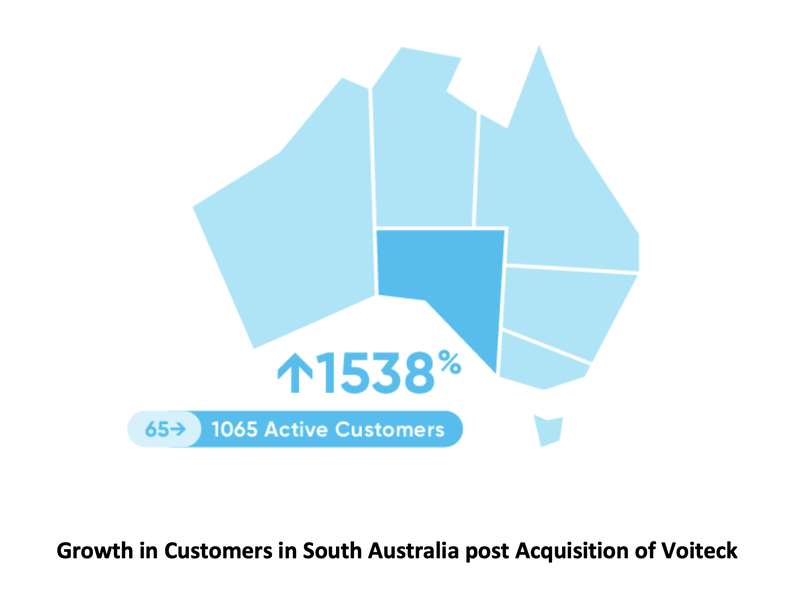

What we like about this acquisition is that Voiteck resembles a mini-VN8 in many respects, which should aid in its integration - it has “an established presence across several niche verticals”. However Voiteck is focused primarily within the South Australian market, which essentially fastracks VN8 expansion into this under-penetrated market.

We also like that the founder and head of Voiteck, Declan O’Callaghan, joins VN8 as part of the deal, which will help with the integration and further penetration of the SA market.

In a nutshell, rather than VN8 expand into SA as a fairly new market entrant, the Voiteck acquisition accelerates customer acquisition and provides multiple cross selling opportunities across a much broader channel partner network.

As we’ve mentioned, VN8’s strategy is simple - accelerate growth through complementary acquisitions - and yesterday’s deal continues the execution of the strategy.

VN8’s ‘hunt-for-growth’ strategy is already paying off on its top line with strong sales growth, and across several financial and operational metrics we track (more on these later).

What we’d like to see in the year ahead is the strategy to deliver across VN8’s bottom line too - with VN8 able to successfully deliver a full cashflow and EBITDA positive FY this year.

We put together a short investment memo on the reasons for our investment in VN8 - which you can read here.

Let’s take a closer look at what the new acquisition looks like and its impact on VN8 going forward.

As we mentioned in our last note, we want to see further VN8 growth, both organically and via acquisitions. The key metrics we track on these fronts are:

- Annual Recurring Revenue - the amount of recurrent revenue we expect based on regular retainers and/or subscriptions payments.

- PBX customers - PBX stands for Private Branch Exchange, which is a private telephone network used within a SME.

- EBITDA - earnings before interest, taxes, depreciation, and amortisation, is a simple measure of core profitability.

To date, VN8’s acquisitions are improving sales fairly quickly. Last quarter, VN8 delivered its best ever sales revenue result, up 47% year-on-year to $6.54M for the 3 months to 30 September 2021.

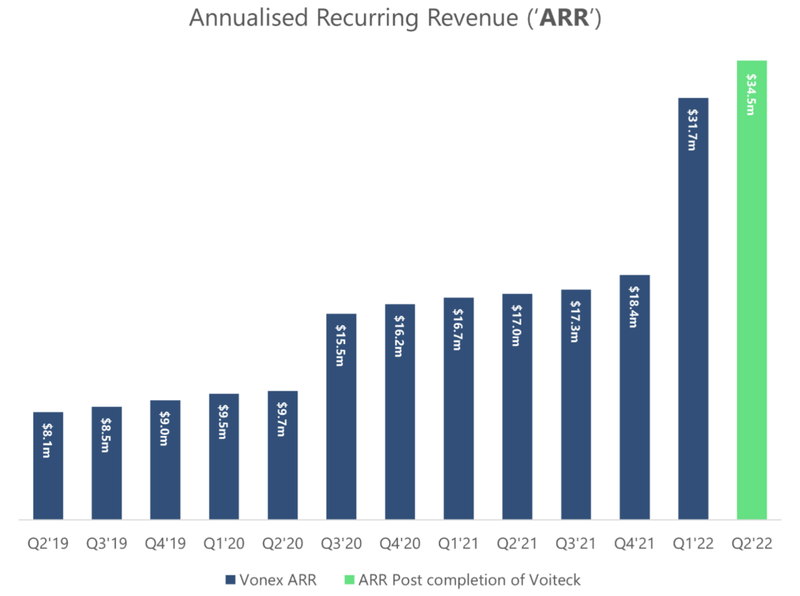

Following VN8’s biggest, most transformative acquisition to date, the $31M MNF Direct Business transaction that was announced last quarter, ARR jumped up substantially to $32M, whilst PBX users surpassed 80,000. We still havent seen a full year with MNF Direct under VN8 yet so we look forward to continued progress here.

With yesterday’s announcement of the Voiteck addition, the end result post competition of the acquisition is a modest step up in ARR to $34.5M:

The Voiteck acquisition is to be transacted at 4.5x EBITDA and is double-digit earnings per share (EPS) accretive on a full year basis, which we consider a fair exchange, which should not take too long to pay back the upfront consideration of ~$2.75M.

As we mentioned above, this latest acquisition brings the VN8 customer base to near full mainland Australia coverage - with VN8 now having sizable market share in South Australia adding to its existing Queensland, NSW, Victoria and West Australian presence.

Growth in customer base

PBX customers are set to exceed 90,000 following the transaction - considering that at the start of the year, VN8 had under half this figure, it seems that the “growth via acquisitions” is certainly fast tracking VN8’s market share and new market penetration.

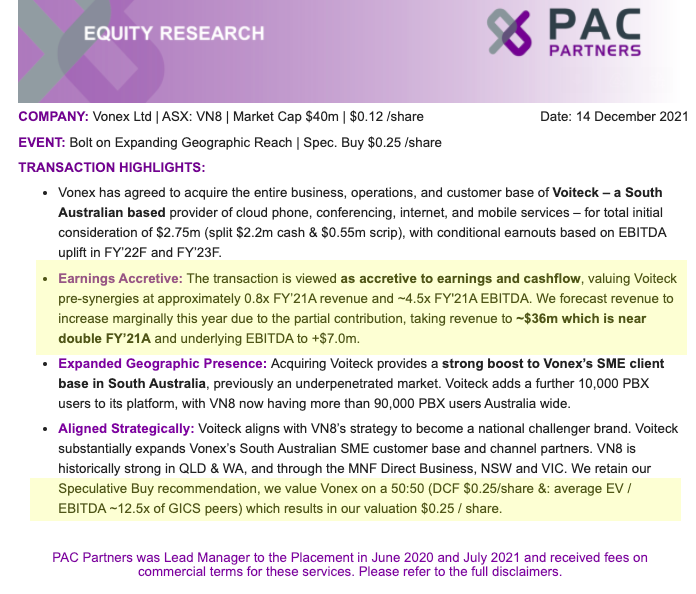

We note stockbroker PAC Partners also considers the merits of this transaction in detail in its latest research report.

In the report, PAC Partners anticipates VN8’s group revenues to reach ~$36M, almost double FY21’s result. They also project net profit after tax (NPAT) to swing from a $4M loss last year to a $4M profit in this current year.

PAC Partners also retained its “Speculative Buy” recommendation on VN8 with a 25 cents per share price target (about double what VN8 is currently trading at).

Of course we should add some caution here - analyst price targets are no guarantee of eventuating. We recommend reading the entire report - VN8 Bolt on Expanding Geographic Reach - and the disclosures before forming a view here.

What we’d like to see next

Overall, we like the progress VN8 is making, and expect to see stronger earnings growth as the newest (Voiteck) and biggest (MNF Direct) acquisitions are integrated in the following months ahead.

We think by mid-2022, both acquisitions should be fully integrated into VN8, and so the full impact on ARR, PBX customers and EBITDA will flow through to the financial reports.

We anticipate that VN8 will reach the 100,000 PBX customers milestone in 2H22, based on current growth and considering the existing acquisitions. This would obviously be brought forward if yet another acquisition was tabled.

Vonex Company Milestones

✅ Acquisition 1: Incorporation Complete (2SG)

✅ Portfolio Initiation

✅ 2SG Wholesale 5G services selected by Optus as a key 5G partner

🟥 Oper8r app discontinued

✅ Acquisition 2: Acquisition Complete (Nextel)

✅ Wholesale Agreement with Orange

✅ Acquisition 2: Incorporation Complete (Nextel)

✅ Acquisition 3: Acquisition Announced (MNF Group Direct Business)

✅ $14M Cap Raise @11c ($12M Insto, $2M SPP)

✅ Acquisition 3: Acquisition Complete (MNF Group Direct Business)

✅ Acquisition 3: Incorporation into Business (MNF Group Direct Business)

✅ Acquisition 4: Acquisition Complete (Voiteck)

🔲 Acquisition 4 - Complete Transaction

🔲 Acquisition 4 - Incorporate into business

🔲 Acquisition 4 - Revenue Growth

✅ 50,000 PBX Customers

✅ 75,000 PBX Customers

🔲 100,000 PBX Customers

🔲 150,000 PBX Customers

✅ Annual recurring revenue hits $25M

🔲 Annual recurring revenue hits $50M

🔲 [NEW] Positive EBITDA FY22

✅ Cash Flow positive for half year

🔲 Cash Flow positive for full year

🔲 Unexpected Announcement 1

🔲 Unexpected Announcement 2

🔲 Unexpected Announcement 3

🔲 Vonex acquired by larger telco company

Here is our VN8 investment strategy

Read our full investment memo on VN8 here.

✅ Initial Investment: @14c

✅ Increase Investment: @11c

🔲 Increase Investment

🔲 Price increases 500% from initial entry

🔲 Price increases 1000% from initial entry

🔲 Price increases 2000% from initial entry

✅ 12 Month Capital Gain Discount

🔲 Free Carry

🔲 Take Profit

🔲 Hold remaining Position for next 2+ years

Disclosure: The authors of this article and owners of Next Investors, S3 Consortium Pty Ltd, and associated entities, own 3,273,182 VN8 shares at the time of publication. S3 Consortium Pty Ltd has been engaged by VN8 to share our commentary and opinion on the progress of our investment in VN8 over time.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.