The full year results are in, how did our telco investment VN8 fare?

Our telco investment Vonex (ASX:VN8) released its full year results yesterday. We like what we saw, with the company successfully ticking off several key milestones.

VN8 is an Australian telco that services small to medium enterprises. It also has a wholesale business that allows companies to white label its communications technology.

We like that VN8 is rapidly growing across key financial and operational metrics, as confirmed by its now released annual report. Importantly, VN8 has crossed into cash flow positive territory for the second half of 2021 — a stepping stone on the path towards ultimately delivering dividends.

We initially added VN8 to our portfolio last September, seeking exposure to communication services at a time when trusted business interconnectivity became crucial for companies adjusting to pandemic work life.

We supported the company’s aggressive acquisition strategy to snap up market share and broaden its domestic footprint, leading to three acquisitions over the past 18 months.

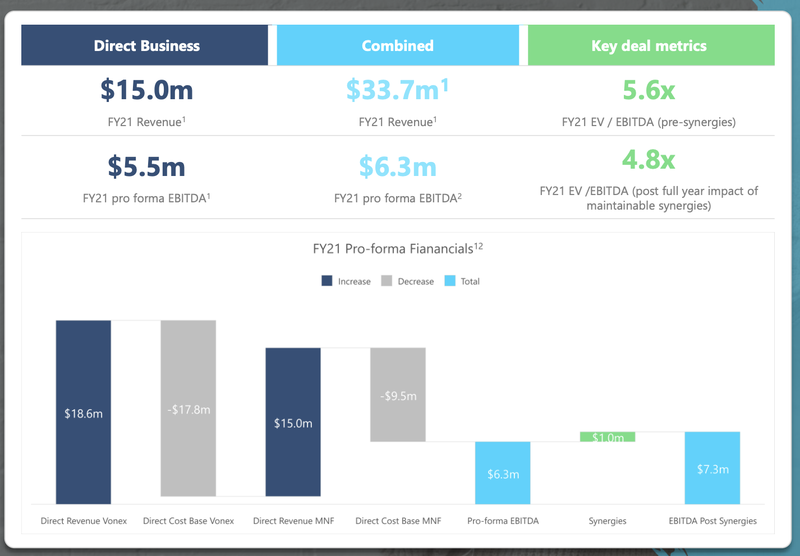

We increased our shareholding after VN8’s recently completed its $31M acquisition of part of MNF Group’s Direct Business. The Direct Business sells cloud phone, internet and mobile services to SME and residential customers in Australia and brings over 5,000 new business customers to VN8's platform.

We considered the deal transformative for VN8, given the size of the transaction (at time of announcement the acquisition cost was greater than VN8’s market cap) and capacity to substantially increase VN8’s customer base, national reach, and importantly, revenues and cross-selling opportunities.

That said, there are a few things we’d like to see improve in the year ahead as well — trimming more fat on costs and successful integration of the acquisitions, for a start.

So let’s take a look under the hood of VN8’s FY21 results. How did they fare?

FY21 Gross Revenue Up 25%

VN8’s annual result was within our expectations for a business aggressively pursuing market share growth via acquisitions.

During the COVID-disrupted year, VN8 provided uninterrupted connectivity for its customers. It leveraged this environment, lifting its gross revenues by 25%, to exceed $19.2 million.

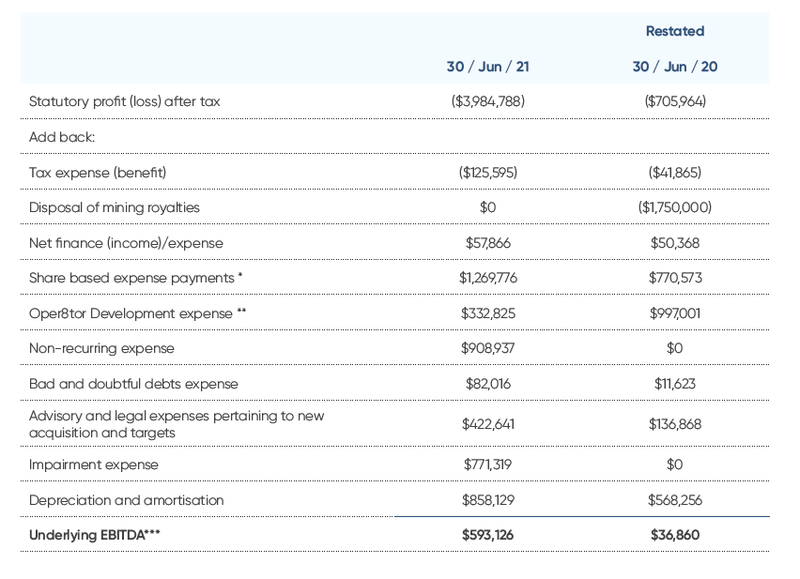

This was counterbalanced by a statutory loss of $3.98M — 464% greater than a year earlier.

While on the surface that loss appears disappointing, we’re more interested in what lies underneath.

Let’s take a closer look at the underlying EBITDA, which provides a superior form guide for future performance.

Strip out non-recurring costs, such as expenses related to hibernated divisions (e.g. Oper8tor), one-off acquisition expenses and extraordinary items, and VN8 delivered underlying earnings (EBITDA) of $593,126. This makes it back-to-back years of profits for VN8.

This figure also doesn’t include any contribution from the MNF Direct Business that was acquired last month or a full year of earnings from its second acquisition, Nextel.

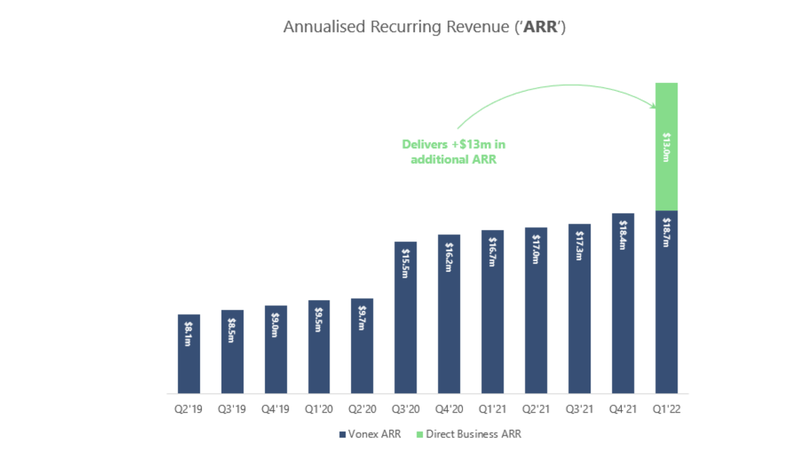

We are encouraged by VN8’s gains across key metrics including annual recurring revenue, underlying earnings and private branch exchange (PBX) customers. Note that these are wholesale NBN and 4G mobile broadband services via a “white label” model.

Given that only one of the three acquisitions, 2SG, has contributed to the full 12 months, we anticipate quite a bit of growth ahead as the Nextel and MNF Direct Business acquisitions are digested for a full year.

Here’s the impact of integration of VN8 and its recent acquisition (MNF Direct Business) on key metrics:

What’s on the horizon?

With VN8’s first acquisition (2SG) and second acquisition (Nextel) already integrated, we’re likely to see VN8 bed down and complete integration of its third (MNF Direct Business) acquisitions.

There are plenty of synergies between all three businesses, including cross selling opportunities and a larger channel partner network to work with, which should realise topline gains fairly quickly. As such, we expect to see quite a bit of organic growth in the upcoming quarters.

Could there be another acquisition for VN8?

Perhaps, though we wouldn’t expect anything of the scale of the MNF Direct Business until it has been fully integrated into VN8.

Could VN8 become a target for acquisition?

We suspect this to be VN8’s ultimate outcome, given several similar occurrences within the sector. It was reported on Monday, that large telco Aussie Broadband (ASX:ABB) was considering several acquisition targets.

As to when VN8 could be consumed by one of the bigger players? Well, this fits within the ‘how long is a piece of NBN cable’ box.

What to look out for

- Integration of MNF Group Direct Business

- Build on strong organic growth through selective acquisition.

- Strong revenue growth from VN8’s first acquisition (2SG Wholesale Services)

- Full year cash flow positive

✅ Acquisition 1: Incorporation Complete (2SG)

✅ Portfolio Initiation

✅ 2SG Wholesale 5G services selected by Optus as a key 5G partner

🟥 Oper8r app discontinued

✅ Acquisition 2: Acquisition Complete (Nextel)

✅ Wholesale Agreement with Orange

✅ Acquisition 2: Incorporation Complete (Nextel)

✅ Acquisition 3: Acquisition Announced (MNF Group Direct Business)

✅ $14M Cap Raise @11c ($12M Insto, $2M SPP)

✅ Acquisition 3: Acquisition Complete (MNF Group Direct Business)

➡️🔄 Acquisition 3: Incorporation into Business (MNF Group Direct Business)

➡️🔲 Acquisition 4 - Announced

🔲 Acquisition 4 - Complete Transaction

🔲 Acquisition 4 - Incorporate into business

🔲 Acquisition 4 - Revenue Growth

🔲 Unexpected Positive Announcement 1

🔲 Unexpected Positive Announcement 2

🔲 Unexpected Positive Announcement 3

🔲 50,000 PBX Customers

🔲 75,000 PBX Customers

🔲 100,000 PBX Customers

✅ Annual recurring revenue hits $25M

🔲 Annual recurring revenue hits $50M

➡️🔲 [NEW] Positive EBIDTA FY22

✅ Cashflow positive for half year

➡️🔲 Cashflow positive for full year

🔲 Vonex acquired by larger telco company

Here is our VN8 investment strategy

✅ Initial Investment: @14c

✅ Increase Investment: @11c

🔲 Increase Investment

🔲 Price increases 500% from initial entry

🔲 Price increases 1000% from initial entry

🔲 Price increases 2000% from initial entry

✅ 12 Month Capital Gain Discount

🔲 Free Carry

🔲 Take Profit

🔲 Hold remaining Position for next 2+ years

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.