What does it take for a stock to 10-bag?

Published 03-MAY-2025 12:36 P.M.

|

14 minute read

- Commentary: A nice distraction from geopolitics and tariffs - a biotech 10 bagger. List of companies that could have a big announcement coming... or rerate off upcoming drill results.

- The other usual stuff: in tomorrow’s Sunday Edition

With Trump tariff talk fatigue starting to creep in...

Here is something different.

A story of hope.

A story of perseverance.

Good fortune.

(And a small cap Investment that actually worked)

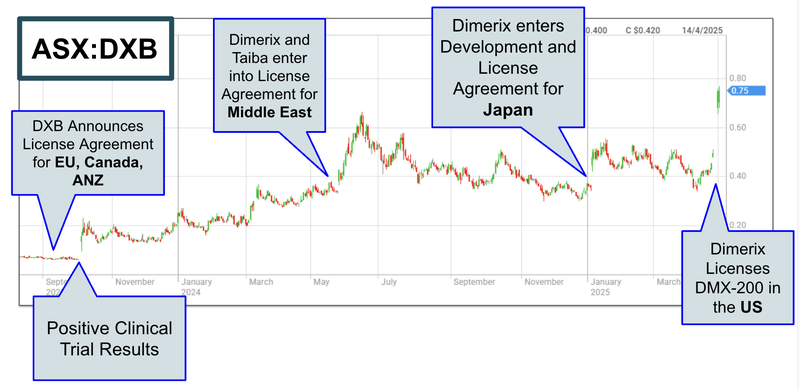

It was a big week for our biotech Investment Dimerix (ASX:DXB).

Up 50% on huge volumes from news of a US licensing deal that could be worth up to $1BN.

DXB is up nearly 1,000% since its 8 cent cap raise in May 2023.

What does it actually take for a stock to 10-bag?

Each journey is different.

Everyone wants it to happen to their stocks, so it’s worth going back to take a look at how a “10x” happens.

Good execution by management, a lot of time, a lot of patience and a little bit of luck.

It requires multiple objectives being achieved, usually a few dilutive capital raises and extended success in achieving objectives to “sustainably” re-rate over time.

And at least one “exceeds market expectations" announcement.

The pathway is not linear either.

Some of our best ever Investments had been down from our Initial Entry Prices at some point...

Including DXB.

Vulcan Energy Resources for example, ended up being an 86-bagger at its peak, but was once down ~40% from where we got in ( and it’s still up ~2,130% today)

Latin Resources was at one point down ~33% for us but at its peak was up 2,332% before eventually being acquired for $560M.

However, many of our attempts at hitting a 10x return go down... and stay down.

But that's all part of the risk when investing in the micro cap end of the market.

Especially over the last couple of years of bearish sentiment in the smaller end means unearthing a sustained 10x winner has been rare.

On Wednesday, our 2021 Biotech Pick of the Year DXB hit the 10-bagger status (caveat: From our second entry of 8 cents, which came with free attaching options to incentivise investors to go into the raise).

So what delivered this week's re-rate in DXB?

DXB signed a US licensing deal worth up to ~A$1BN to commercialise its Phase III drug for a rare kidney disease.

The US is the biggest market to sell pharmaceutical products into and DXB’s move on the news reflects this.

That news took DXB from ~49c to ~77c, - a 55% move.

But the DXB story is more than just this one catalyst.

We have been Invested in DXB for almost four years now and the company has had many ups and downs (then ups again) since then.

(we have sold some along the way and its delivered good returns over the last 18 months, in hindsight we should have hung on to more for this current rerate)

There are some useful insights that can be taken from DXB’s 10x, in how one or two big catalysts from a low base can restore the market’s faith in a story...

Even from the depths of a dreaded “crunch raise”.

The DXB Story, from 20c down to 8c up to... ~80c.

In August 2021 we announced DXB as our Biotech Pick of the Year and Invested in a 20c placement.

In this placement the company raised $20M to get through its Phase 3 clinical trial for FSGS.

(FSGS is a rare kidney disease with a $1Bn+ per year market size potential).

DXB’s share price initially ran up...

But several months later the challenges of running a big phase 3 trial for a rare disease materialised.

It was becoming clear that DXB would not have enough cash to make it through to the interim results.

And the market started figuring out there would be no major catalyst coming to move the share price without another capital raise.

The market (as it always does) priced DXB on a “need to raise” basis and sent the share price down to as low as 5.2c in June 2023...

This was a ~75% drop from our Initial Entry Price.

Then the company launched a cap raise at 8c in May 2023 with two sets of free attaching options (ouch for existing shareholders... like us).

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Looking at the chart, In hindsight it seems like an obvious raise to go in to, (of course)...

But that 8c round, when things were looking bleak, was very difficult to press the “send cash” button in netbank.

When a stock is down 75% from an Initial Entry Price we inevitably start to question our own conviction...

(and decisions)

And the last thing you feel like doing is putting more cash into another placement.

At the time it was also the depths of the bear market for biotech companies AND liquidity in general...

That September/October 2023 time period was as hard a time to get a cap raise closed as we have seen in a while now.

This was a snippet from one of our weekend emails in October 2023 which really summarises how bad the feeling around markets were...

Look at that headline from the AFR...

DXB’s trials were progressing just like the company had said it would do, the only thing that had changed was market expectations around timelines and costs...

Our Investment Thesis was technically still intact...

(how many times have you seen a company say they will do the thing for a certain amount of cash, then cash runs out before the thing is done?)

So we put some cash into the 8c DXB placement to average down our Investment

(even though averaging down hardly ever works out well... looking at you TMR and EV1)

Two months later, DXB announced its first commercialisation deal...

up to €132M ($232M) in milestone payments with Advanz Pharma for the EU, the UK, Switzerland, Canada, Australia, and New Zealand.

Then $120.5M in milestone payments for the Middle East from a company called Taiba, and a further ¥10.5BN ($111M) for Japan.

While sentiment for DXB was at an all time low, DXB turned around the company's fortunes by wrong-footing the market with a big catalyst that far exceeded expectations.

The market was pricing in ANOTHER capital raise...

And instead DXB announced US$10M in non-dillutive funding and a commercialisation deal.

Then DXB continued to follow up with more and more licensing deals as well as positive interim trial results.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Each of these deals provided DXB with an upfront payment, meaning that it only had to do one more cap raise to get through to the next stage of results.

(Phase 3 trials are expensive, but if they are successful commercialisation deals bring money and share price increases)

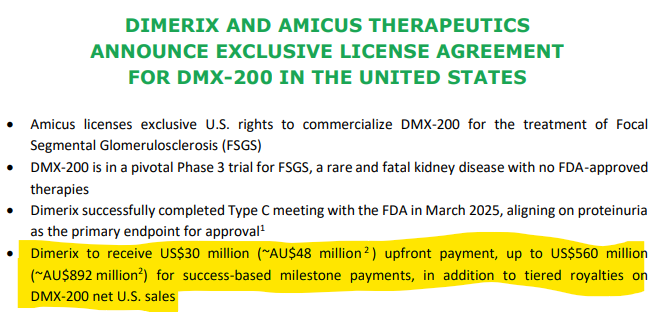

The news this week is the biggest achievement for the company so far, securing a licensing deal in the US for up to A$1Bn (on success based milestone achievements).

Not bad at all, well done DXB.

(Source)

You can check out DXB’s CEO and MD Nina Webster talk through the deal in this webinar that was released on Thursday.

Still to come DXB has:

- Licensing deal to sell into China

- Results from its Phase 3 clinical trials (scheduled for August this year)

- FDA approval

DXB was capped at $423M at Friday’s close.

The DXB story is one of surprising deals and catalysts that wrongfooted the market at the right time.

(maybe it's about time to add another biotech to our portfolio... If you have an idea for the “next DXB” please respond to this email and we will take a look at it)

And it got us thinking...

What are the other companies in our portfolio where “one big announcement that exceeds market expectations" can kick off serious momentum for the company...

Which of our Investments have “potential” deals that could land at any time?

OneView Healthcare (ASX:ONE)

About: Health tech company that provides hospital patients a “virtual care and digital control centre” at their bedside.

Catalyst: Major deal with large US hospital network

Our Take: Back in 2023 ONE signed a “value-added reseller” deal with a major hospital bed seller, the US$16B-capped NASDAQ listed Baxter. (Baxter also sell a bunch of other medical related stuff to hospitals)

This reseller deal was signed two years ago.

Given the typical sales cycles into a hospital is around two years, ONE could see a major growth step-up in the next six months if some key hospital network deals land, which we think could be driven by its partner Baxter.

Condor Energy (ASX:CND)

About: Surrounded by supermajor TotalEnergies, CND has announced a 1TCF gas resource and 3 billion barrel prospective oil resource (100% owned basis) on its offshore acreage in Peru.

Catalyst: Farm-in partner for drilling program

Our Take: Although CND has published some big prospective resource numbers, we think that the market is waiting for a line of sight towards a maiden drilling program. CND has announced that there are a number of interested parties in its dataroom and any partnership deal could be a big catalyst for the company.

AML3D (ASX:AL3)

About: AL3 supplies metal 3D printing systems to speed up defense, aviation, and shipbuilding supply chains and domestic manufacturing, in the US and Australia.

Catalyst: Large US-based Purchase Agreement

Our Take: In November last year AL3 raised $30M to scale up its business in the US and in Europe. Given the urgent need of the US Navy to ramp up shipbuilding, and the US-China trade tensions that are incentivising domestic manufacturing, we think AL3 is in a strong position to secure large deals.

RocketBoots (ASX:ROC)

About: ROC sells “Vision Artificial Intelligence” technology to retail supermarkets and commercial banks to analyse and respond to in-store customer behaviours.

Catalyst: Large multi-site deal

Our Take: If ROC is able to close one of the large contracts it says it “Advanced Pipeline” it could have its product in thousands of stores through just one deal. At a price point of $3,500 per store, one deal could be in the millions of dollars in recurring free cash flow.

These deals take a very long time to secure and the market gets bored waiting which gets priced into companies share price, but if $12M ROC can pull one off, it could provide incredibly “sticky” recurring revenue and a rerate for the company.

EchoIQ (ASX:EIQ)

About: Echo IQ (ASX:EIQ) has an FDA cleared technology that uses AI to provide enhanced detection of heart diseases.

Catalyst: Licencing deal with device manufacturers

Our Take: Now that EIQ has secured FDA clearance for Aortic Stenosis (a particular heart disease), we think that EIQ will be busy talking to companies like device manufacturers that have a direct interest in diagnosing more heart conditions. At any point in time a major “licensing deal” could be announced by EIQ, a big “watch this space”.

Whitehawk (ASX:WHK)

About: USA based cybersecurity micro cap, providing cyber risk products, services and solutions.

Catalyst: Large cybersecurity deal

Our Take: Last month WHK announced that it had secured a key sub-contractor position in a US $920M deal with the US Government. Although there was no specific revenue to WHK in the announcement just yet, the share price more than doubled on the announcement. This tells us that there is money on the sidelines waiting for WHK to deliver a material revenue-generating deal.

Global Uranium & Enrichment (ASX:GUE)

About: GUE is a uranium explorer with projects across a number of uranium districts in the USA & Canada. GUE also has a cornerstone investment in a private uranium enrichment technology company.

Catalyst: Deal on GUE’s private uranium enrichment technology.

Our Take: GUE is one of only two uranium enrichment exposures on the ASX (the other is capped at half a billion dollars) and there is a precedent for re-rates in share prices once big partnership deals are signed for enrichment tech on the ASX... GUE has given guidance for a deal to happen before the end of this half - and there is only about 8 weeks left.

(plus the U price had its first strong uptick after a year of downtrend)

Titan Minerals (ASX:TTM)

About: 3.1M oz gold and 22M oz silver JORC resource in Ecuador.

Potential Catalyst: Acquisition / Takeover? Pure speculation from us here, but hear us out...

Our Take: Last week CMOC announced a deal to acquire Ecuador junior Lumina gold for US$420M in an all cash deal. TTM’s neighbour Sunstone Metals has mentioned corporate interest in its Ecuador project too.

We have also seen Gina Rinehart's Hancock Prospecting partner with one of TTM’s assets before in a deal worth US$120M.

This is pure speculation but based on the above, could TTM be swept up in this new interest in the region with a takeover offer, JV or substantial cash injection given the gold price is trading near all time highs?

Emyria (ASX:EMD)

About: EMD delivers and develops psychedelic assisted therapies to improve mental health .

Catalyst: Agreement with a major insurer or government healthcare organisation to fund psychedelic therapies for their members.

Our Take: EMD is currently in negotiations with insurance companies to fund psychedelic therapies for its members. These negotiations have been going on for months now and it is hard to predict if and when this news could come. Based on the latest quarterly EMD said they could be “launching funded pilots” within the coming months.

Pantera Lithium (ASX:PFE)

About: PFE controls 26,000+ leased acres in the lithium region of the “Smackover” in the USA.

Potential Catalyst: Acquisition / Takeover. Again pure speculation from us - but here’s the case for it.

Our Take: The battle over lithium production rights in the region appears to be heating up with Exxon Mobil winning a regulatory battle against Occidental Petroleum for lithium rights on acreage in the region. This indicates just how much value Exxon sees in land rights in the Smackover Region (where PFE has 26,000+ leased acres).

We think that it is a possibility that PFE’s larger neighbours start to take an interest in making an offer to PFE for its exclusive land package in the region.

If PFE can deliver some FOMO inducing results it could flush out any potential M&A interest, in our opinion.

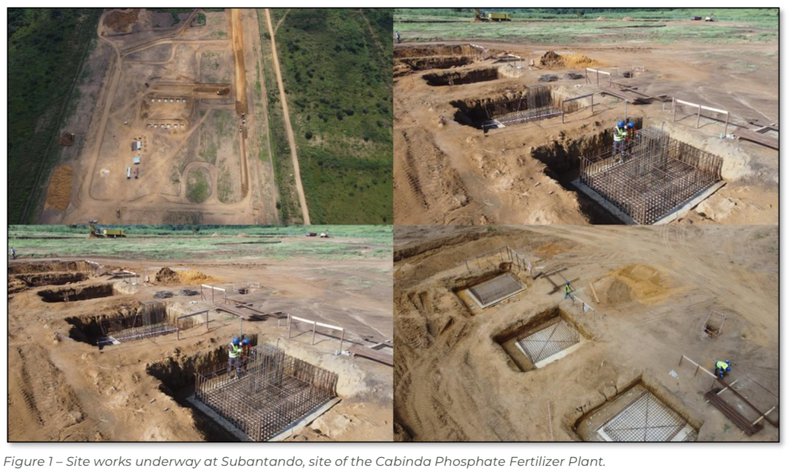

Minbos Resources (ASX:MNB)

About: Construction ready phosphate and development stage green ammonia projects in Angola.

Catalyst: Finalise funding agreement & secure offtake.

Our Take: It’s getting real, MNB is right now constructing its phosphate plant in Angola. The challenge is that there is one more financing hurdle for MNB to clear, which is contingent on an offtake deal with Angola's Largest food aggregator - Grupo Carrinho. MNB’s share price has come off a fair bit over the last 12-18 months which is likely because the market is pricing in more delays (which had become typical for MNB... hey, it's Angola).

If MNB can get its project fully funded it could be a catalyst for a positive re-rate in MNB’s valuation, against market expectations.

Here is an update from MNB’s quarterly showing the progress with the plant construction:

Drilling catalysts to watch as well

As well as potentially imminent “deals”, drilling results can also deliver strong share price catalysts. Here’s a few select ones in our portfolio.

Mithril Silver & Gold (ASX:MTH)

About: MTH is looking to more than double a 373k ounce gold and 11 million ounce silver JORC resource in Mexico.

Catalyst: Drilling Results from greenfields “Target 2” exploration.

Our Take: An exceptional drill results from MTH’s first target area back in September led to a ~700% move in MTH’s share price. Now for the first time ever, MTH is drilling regional targets where the company could make entirely new discoveries similar in size (even bigger maybe?) than its current JORC resource.

Solis Minerals (ASX:SLM)

About: SLM is a microcap copper explorer in Peru. SLM has secured 1 of 2 key permits to start its drilling program (commencing “imminently”).

Catalyst: Make a copper discovery

Our Take: With back-to-back copper drilling across four targets scheduled for this year, a single strong hit could turn sentiment fast for SLM... like we saw with regional peer AusQuest - up 700%+ on a discovery.

Sun Silver (ASX:SS1)

About: Largest pre-production silver asset on the ASX with a 480M ounce silver equivalent JORC resource in Nevada, USA.

Potential Catalyst: Metwork Results / Drill results

Our Take: In the short term we think the market will cycle in and out of SS1 as the silver price moves up and down BUT a positive metwork or drilling announcement could be the unexpected catalyst to trigger a sustained re-rate of the stock.

Are you a s708 sophisticated investor?

If you qualify as a sophisticated investor and would like to see “s708 only” sophisticated investor opportunities: Subscribe to Next Cap Raise.

You will need to send us a valid certificate from a qualified accountant confirming you qualify as a sophisticated investor.

Have a great weekend,

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.