Emyria (ASX: EMD) is an integrated clinical drug development and care delivery company.

The primary area of focus is on psychedelic assisted therapies on PTSD using MDMA.

What is the macro theme?

We think psychedelic assisted therapy and psychedelic clinical trials have the potential to reshape care and treatments for difficult to treat neuropsychiatric disorders such as complex trauma, depression, anxiety, chronic pain and Parkinson’s disease.

As more patients become aware of their options, and the regulatory environment eases, we think companies that can deliver these types of treatments, services and clinical trials will attract capital.

Our Big Bet for EMD

EMD re-rates to a +$300M market cap by making a breakthrough with one or more of its clinical trial programs (MDMA, psilocybin, ketamine, CBD) while rapidly growing the footprint of its mental health treatment clinics.

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our EMD Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

Why did we invest in EMD?

EMD now has a commercialisation deal with Australia’s largest private health insurance company Medibank

EMD signed a 2-year deal with Medibank, Australia’s largest private health insurance company.

This deal means that Medibank will fund the full costs of any eligible members who utilise EMD’s PTSD care programs.

The deal will see EMD cover around $30,000 per patient, per year, and underpins EMD’s ambition to scale up its mental health platform nationally.

EMD has Authorised Prescriber Status (approvals) from the TGA to deliver MDMA-assisted therapies

Authorised Prescriber status is what is needed for any organisation or individual to administer psychedelic assisted therapy.

It is not easy to get and requires multiple submissions to the TGA, ethics approval, a tried and tested protocol for therapy delivery and strict guidelines on how the treatment can be administered.

This status provides a significant regulatory advantage to EMD compared to anyone else trying to enter the space.

Australia is leading the charge globally in new age treatments for mental health

In 2023 Australia’s drug regulator, the TGA, announced the legalisation of various controlled substances for medical use in therapy.

This was a world first.

This provides the perfect regulatory environment for a company like EMD to develop and validate its business model.

EMD has published clinical data that shows its treatment works

In 2023 EMD launched a clinical trial for MDMA-assisted therapy.

From that study EMD was able to show that its treatment reduces PTSD symptoms by more than 50%.

And patients continued to improve six months after the assisted therapy was complete.

EMD has the means to deliver its care through its physical clinics

As part of EMD’s integrated care model, EMD needs to provide access to physical sites for its physicians to undertake EMD’s approved therapy.

Right now EMD owns and operates the Empax Centre in Perth.

But EMD has also been able to open up satellite centres within hospitals expanding its capacity into the Perth Clinic.

EMD is in discussion to launch these satellite sites on the East Coast, which will provide the means for EMD to expand nationally.

While EMD will set up some core sites that it owns, it can also lease these sites from different hospitals.

EMD’s Chairman Greg Hutchinson has scaled up clinics before with ~$13B-capped Sonic Healthcare

EMD’s Chairman Greg Hutchinson led the scale up of Sonic HealthPlus to over 7,000 active clients across 40 different clinic locations.

Sonic HealthPlus is now the largest provider of occupational and community medical services in Australia…

If there is anyone that is able to deliver the “scale up” business model for EMD, it's the Chairman, Greg Hutchinson.

(At EMD’s 3.5 cent placement in November last year Greg put in $1M, at the most recent placement at 2.5 cents, Greg put in $197k).

EMD has the opportunity to move into the US

As EMD is able to scale up its business and secure more payer agreements, we think this will create a significant moat around the business.

We think that if it is able to validate its business here in Australia, it could potentially take that business model and replicate it in the US.

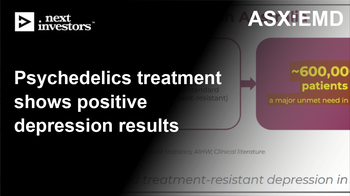

~24M people suffer from PTSD in the US.

The cost of PTSD-related anxiety disorders is more than US$42.3 billion annually in the US.

And the FDA commissioner recently said on News Nation that research on psychedelic treatment is a “Top Priority” for the organisation.

This actually provides an advantage for EMD, as it is able to accelerate its business here in Australia, while potential competitors in the US are in limbo waiting on the regulatory environment to change.

By that time we hope that EMD is seen as a powerhouse in the industry and can transfer all of its learnings overseas.

EMD has the ability to expand into different mental health conditions, and different drugs

While EMD is currently focused on MDMA assisted therapy for PTSD the company also has the opportunity to target different drugs (like psilocybin and ketamine).

AND eventually start treating different disorders like treatment resistant depression, parkinson's disease and Bipolar disorder.

As more therapies are developed in the pipeline, EMD will be able to offer patients are broader range of care and target different markets.

What do we expect EMD to deliver?

Objective #1: Scale up services to more sites

We want to see EMD partner with more hospitals and care centres to deliver its care offering.

Milestones

New site opened

New site opened

New site opened

Objective #2: Secure more payer agreements

Now that the company has secured a 2-year deal with Medibank, Australia’s largest private health insurance company, we want to see EMD secure more payer agreements.

Milestones

Payer Agreement 1 - Medibank

Payer Agreement 2

Payer Agreement 3

Objective #3: Secure more MDMA

One of the big bottlenecks for EMD to deliver its care is the supply of medical grade MDMA. We want to see the company identify both short term and long term supply opportunities.

Milestones

Supply Agreement 1

Supply Agreement 2

Develop own MDMA-analogues for use in its own clinics

Objective #4: Expand care offering to new indications and/or new drug therapies

We want to see EMD expand its assisted therapy programs to psilocybin and ketamine, also for different mental health conditions like anxiety, treatment resistant depression etc…

Milestones

Commence clinical trial on ONE new indication or drug.

What could go wrong?

Regulatory Risk

EMD is working in a heavily regulated space.

The regulatory changes that allow EMD to operate in the field of psychedelic therapies are new and could be reversed. A regulator could step in and intervene either across the industry or specifically in relation to EMD.

Small caps often need to raise cash to fund their growth.

Whilst EMD is generating revenue now, it is still making a loss (it spends more cash than it brings in).

If EMD is unable to develop a self-sustaining business model with positive operating cash flow, this could force EMD to raise capital in the future, likely at a discount to market prices to secure funds.

There is always the possibility that broader market sentiment gets worse and shares as a whole trade lower, taking EMD’s share price with it. Alternatively, there could be further sector specific pain ahead. For example, the biotech sector sells down.

What is our investment plan?

We have not sold a single share in EMD since we initiated coverage in 2023.

Our Investment Plan for EMD is to hold on to a majority of our position to see the company execute on its business strategy over the next two to three years.

If the company’s share price materially re-rates in the medium term due to the scale up efforts we may look to sell up to ~20% of our holding. See our general hold policy for more details.

Disclosure: Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 15,888,332 EMD Shares and 5,822,221 EMD Options and Company’s staff own 561,667 and 138,889 Options at the time of publishing this Investment Memo. The Company has been engaged by EMD to share our commentary on the progress of our Investment in EMD over time. (6,250,000 shares and 2,083,333 options are subject to shareholder approval)

Investment Memo:

Emyria

(ASX:EMD)

-

LIVE

Opened: 04-Sep-2023

Shares Held at Open: 5,666,667

What does EMD do?

Emyria (ASX: EMD) is an integrated clinical drug development and care delivery company.

EMD’s primary area of focus is on psychedelic assisted therapies using MDMA, ketamine and psilocybin to treat difficult mental health problems in innovative ways. It also has cannabidiol (CBD) treatments in its clinical pipeline for anxiety and complex pain.

What is the macro theme?

We think psychedelic assisted therapy and psychedelic clinical trials have the potential to reshape care and treatments for difficult to treat neuropsychiatric disorders such as complex trauma, depression, anxiety, chronic pain and Parkinson’s disease.

As more patients become aware of their options, and the regulatory environment eases, we think companies that can deliver these types of treatments, services and clinical trials will attract capital.

EMD re-rates to a +$300M market cap by making a breakthrough with one or more of its clinical trial programs (MDMA, psilocybin, ketamine, CBD) while rapidly growing the footprint of its mental health treatment clinics.

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our EMD Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

Why did we invest in EMD?

Australia leading the charge globally in new age treatments for mental health

Following the Therapeutic Goods Administration’s decision, which came into force in July 2023, Australia now has the regulatory environment needed for a company like EMD to work.

This decision put EMD and Australia potentially years ahead of other jurisdictions like the US.

EMD at the forefront of psychedelic assisted treatment

EMD has the infrastructure needed to provide psychedelic treatments.

EMD owns actual brick and mortar clinics where patients are treated.

These clinics are where practitioners like psychiatrists work - currently under TGA rules, these treatments can only be prescribed by specifically authorised psychiatrists.

EMD is creating novel MDMA products

EMD has partnered with UWA to develop a number of different novel MDMA treatments to harness the therapeutic aspects of the drug - in particular with Parkinson’s disease.

Drug development can be very lucrative, if EMD proves that it is safe and effective in a clinical setting.

EMD’s unparalleled access to patient data and AI partnership

Through its clinics EMD has access to opt-in patient data and uses state of the art data insights generated by a technology platform called Palantir Foundry. This data is used to inform better care practices and drug development opportunities.

Clinics delivering revenue

EMD provides mental health care services to patients, which generates revenue for the company and subsidises its R&D. The company made $1.6M last FY, targeting $5.7M this FY.

CBD “Side bets” provides a catalyst

EMD is currently in a Phase 3 clinical trial for an over-the-counter CBD treatment for anxiety.

The company has a commercial partner lined up to oversee marketing, distribution and sales. Any positive outcome here will drive immediate value back to EMD shareholders.

EMD management ‘dream team’

We think EMD’s Board and Management are highly qualified, well respected and provide the necessary governance structure to support a far larger organisation.

EMD’s market cap provides an attractive entry point

At our Initial Entry Price of 7.5 cents, EMD has a market cap of ~$25M. Other operators in the space are capped at many multiples of EMD, indicating plenty of room for growth.

What do we expect EMD to deliver?

Objective #1: Gather important data from MDMA mental health trial

We want to see EMD deliver its MDMA assisted therapy. EMD has already recruited its first patient and secured key approvals from the Office of Drug Control and Therapeutic Goods Administration.

Complete patient recruitment for Phase 2b trial (MDMA)

Complete Phase 2b trial for MDMA

Objective #2: Develop novel MDMA treatments

We expect EMD to continue its clinical trial work and drug development, which includes preclinical tests on MDMA analogues (animal studies) for faster acting MDMA and MDMA “without the high” for Parkinson’s disease.

Whilst we didn't necessarily Invest for its CBD clinical trials, a successful outcome will deliver immediate value to shareholders.

EMD is currently in a Phase 3 trial for its CBD over the counter treatment for stress and anxiety.

It has a commercialisation agreement in place with Aspen Australia if the trial is successful and the drug is registered with the TGA.

EMD is also developing a highly potent CBD treatment for complex pain & anxiety to take to Phase 1 trials.

Milestones

Results for the Phase 3 trial for low-dose CBD for stress and anxiety

Register CBD treatment with the TGA for over the counter use

Begin: Phase 1 trial of high-potency CBD treatment

Results: Phase 1 trial of high-potency CBD treatment

Objective #5: Scale clinical health services & engage payers

We want to see EMD open new clinics and/or licence its treatments and care models to create scale. To do this we expect EMD to get a major payer in healthcare or an industry body to help fund treatments.

Objective #6: Expand Intellectual Property and build partnerships

EMD needs to secure further patent protection for its treatments (such as MDMA analogues), continue to work with major healthcare bodies to support registration of its treatments and find commercialisation partners.

Milestones

Patent application

Patent grant

Commercialisation partner secured

What could go wrong?

Adverse patient outcome risk

Given the psychedelic therapies that EMD will administer are still being fully understood, there could be a greater risk of adverse patient outcomes.

Were adverse patient outcomes to occur, aside from the direct negative impact to patients, it is possible the media and social sentiment could turn on the industry and EMD.

Alternatively, this could happen even if EMD does everything properly, i.e another less scrupulous business or operator attracts negative publicity.

Regulatory risk

The regulatory changes that allow EMD to operate in the field of psychedelic therapies are new and could be reversed. A regulator could step in and intervene either across the industry or specifically in relation to EMD. A change of government could also bring about a regulatory reversal.

EMD will need to move quickly to establish its presence in the market. If progress is slow, another care provider or alternative treatments could emerge hurting EMD’s prospects.

There is a chance that one or more of EMD’s clinical trials fail to meet their primary or secondary endpoints, meaning the treatments fail to satisfy the criteria of the studies. Any clinical trial results, if negative, could hurt the EMD share price.

Funding risk

Small caps often need to raise cash to fund their growth. Whilst EMD is generating revenue now, it is still making a loss - i.e. it spends more cash than it brings in. If EMD is unable to develop a self-sustaining business model with positive operating cash flow, this could force EMD to raise capital in the future, likely at a discount to market prices to secure funds.

There is always the possibility that broader market sentiment gets worse and shares as a whole trade lower, taking EMD’s share price with it. Alternatively, there could be further sector specific pain ahead. For example, the biotech sector sells down.

What is our investment plan?

Our Investment Plan for EMD is to hold on to a majority of our position to see the company execute on its business strategy over the next two to three years.

If the company’s share price materially re-rates in the medium term due to the results of the CBD Phase 3 trial, a breakthrough in the MDMA technology, a macro triggering event or any other unknown reason, we may look to sell up to ~20% of our holding. See our general hold policy for more details.

We also intend to fully participate in the EMD rights issue.

Disclosure: Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 5,666,667 EMD shares and 2,833,334 EMD options at the time of publishing this memo. The Company has been engaged by EMD to share our commentary on the progress of our Investment in EMD over time.