Echo IQ (ASX:EIQ) is a technology company that uses AI to provide early warning and enhanced detection of heart disease.

What is the macro theme?

Heart diseases are the leading cause of death worldwide.

Diagnosis is performed by humans who have to interpret 3D models of the heart, which leads to inaccuracy and delayed or missed diagnosis costs lives.

With 30% of all deaths around the world attributed to cardiovascular disease, we think EIQ solves for a pressing problem as AI increasingly enters the health economy.

Our Big Bet for EIQ

“EIQ re-rates to a >$1BN market cap on successful commercialisation of its heart disease detection technology and/or an acquisition at a multiple of our Initial Entry price.

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our EIQ Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

Why did we invest in EIQ?

The data shows that the AI algorithm works.

EIQ has published three studies since it acquired the technology in 2021.

For the first target condition aortic stenosis, the technology has been shown to accurately identify 100% of severe aortic stenosis patients.

For the second condition, heart failure, the technology has been shown to accurately identify 97% of patients in conjunction with a cardiologist (compared to 46% as the current standard of care).

These are incredibly strong results and underpin the technology's potential.

Imminent share price catalyst in potential aortic stenosis FDA approval.

We expect the FDA is set to make a decision on EIQ’s first target condition, aortic stenosis by the end of September based on our interpretation of typical review timelines.

FDA approval opens the door for EIQ to commercialise its tech.

FDA approvals for algorithms related to health have dramatically increased over the last few years. EIQ’s FDA approval shapes as a key near term catalyst for the stock.

Multi-billion dollar market target for “heart failure” diagnostics assistant.

Over 64 million people suffer from heart failure each year across the world.

And in the US, heart failure costs the US healthcare system roughly $60BN because many of these patients wind up back in hospital within 30 days.

The reimbursement cost for heart failure is US$284 per patient, and at 25% market penetration, EIQ could earn up to ~US$100M in ARR.

There is still a long way to go, given EIQ has not started generating revenue yet - but we like the size of the prize.

Second catalyst for FDA approval on heart failure could be within 12 months.

EIQ recently published very promising data on its AI detection algorithm targeting heart failure.

This data will be used, along with potentially another study, to secure FDA approvals within the next 12 months.

Exclusive commercial access to the world's biggest heart data repository

EIQ has exclusive access to a database of over 1 million echocardiographic records from NEDA (National Echo Database of Australia).

NEDA is the largest echo database in the world and data stretches back to January 2000 and has a replacement cost north of US$300M.

This data is not easily replicable or acquired.

EIQ Chief Research & Strategy Officer, Professor Geoff Strange, is the creator, Director and Chief Investigator of the National Echo Database.

This means EIQ has the right personnel to work with this exclusive data.

Also, considering it took NEDA 24 years to reach this point, we think this gives EIQ a significant moat and competitive advantage over any new market entrants.

Clear pathways to commercialisation in the USA - the biggest healthcare market in the world.

There are two ways that EIQ can make money, one is reimbursement, one is licensing.

Each pathway opens up new avenues to monetisation and can work hand in hand.

Reimbursement involves the acquisition of specific codes which allow hospitals and echo labs (physical location health providers) to claim for reimbursement from US insurance companies.

Licensing on the other hand targets echo machine makers (like Phillips and GE) or Big Pharma (which would be interested in a wave of new patients that EIQ’s tech picks up).

SaaS revenue model, potential to rapidly grow revenue and/or secure large licensing deals.

EIQ is a cloud based platform that will likely operate on a Software as a Service (SaaS) model when initially commercialised.

SaaS tech companies with demonstrated recurring revenue growth over time attract large valuation multiples.

EIQ’s tech platform is already built, meaning software development costs should be low, leading to higher margins on sales.

An ongoing “soft launch” has the product in the hands of an end user via a strategic partnership with a leading US medical Enterprise Cardiovascular Information Systems (CVIS) provider, Scimage, which has over 2000 sites in the US.

We expect this to provide an early opportunity for revenue growth under US reimbursement codes if EIQ secures FDA approval.

Cost savings, 3 seconds until results, removing bias

Health practitioners are under immense stress, and the current method of Trans-Thoracic EchoCardiogram (ultrasound on your chest, or “echo”) takes time.

These echos may be performed and interpreted in suboptimal conditions.

EIQ’s tech strips that out of the equation, delivering results in 3 seconds and also removing unconscious bias in the interpretation of results (for certain conditions, women are more frequently misdiagnosed than men).

What do we expect EIQ to deliver?

Objective #1: Secure FDA approval for aortic stenosis product

FDA approval for aortic stenosis will allow EIQ to commercialise its technology for this product. We want to see this happen by the end of September 2024.

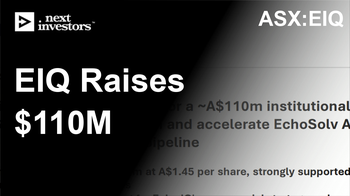

EIQ is a small cap company and is essentially pre-revenue. This means that EIQ may need to raise funds in the future via capital raises that may incur dilution to shareholders.

There may be other companies developing AI products in the medtech space. It is possible for competing products to enter the market.

Key personnel risk

EIQ is reliant on a number of key professionals via its scientific advisory board and board more generally. If these personnel leave it could hurt the company’s prospects.

Market risk

There is always the possibility that broader market sentiment gets worse and shares as a whole trade lower, taking EIQ’s share price with it. Alternatively, there could be further sector specific pain ahead where junior explorers suffer a lot more than the broader market.

What is our investment plan?

We plan to hold a position in EIQ for the next 3-5 years (and beyond) as it progresses its plan to gain significant market penetration in the large US market.

We eventually may look to take some profits by selling up to ~20% of our holding (in line with our holding policy and escrow conditions) if the share price materially rerates on the company successfully delivering on the key objectives listed above.

Disclosure: Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 3,470,000 EIQ Shares and the Company’s staff own 140,000 EIQ shares at the time of publishing this Investment Memo. The Company has been engaged by EIQ to share our commentary on the progress of our Investment in EIQ over time.