ONE signs its biggest deal ever

Disclosure: The authors of this article and owners of Next Investors, S3 Consortium Pty Ltd, and Associated Entities, own 8,525,000 ONE shares at the time of publication. S3 Consortium Pty Ltd has been engaged by ONE to share our commentary and opinion on the progress of our Investment in ONE over time.

Our 2021 Tech Pick of the Year and health tech Investment, Oneview Healthcare (ASX:ONE), just took a huge step forward, signing a major deal to get its platform into more US hospitals.

As we’ve been saying, we like investing in small caps (compared to large caps) because just one significant result can have a material impact on the company's business and future prospects.

On that note, ONE today announced its biggest deal ever.

ONE’s latest deal is for 2,441 beds in the BJC HealthCare network, one of the largest healthcare organisations in the US.

ONE’s primary product is a “virtual care and digital control centre” at a hospital patient’s bedside that’s designed to deliver the best possible patient experience during their stay.

ONE generates revenue by charging an annual licence fee on a per bed basis.

Before we Invested in ONE in 2021, it took ONE roughly five years to get to ~10,000 contracted beds.

Today it’s tacked on a further 2,441 contracted beds in a single deal - a material increase of 20% to ONE’s total contracted bed count in one hit.

This deal takes it to 14,283 contracted beds — just shy of the #1 objective we wanted to see from ONE this year, to have 15,000 contracted beds by the end of 2022.

The deal is in the US, the primary market we want to see ONE grow.

And we’re not even at the mid-point of 2022 yet — a very good sign that ONE might significantly exceed our expectations on this objective.

Any bed count above 15,000 during 2022 is a bonus for us, so recently cashed up ONE has seven full months to exceed this number.

ONE’s deal with BJC strikes us as very similar to the breakthrough deal ONE signed with the Kingman Regional Medical Centre in Arizona, part of the prestigious Mayo Clinic network.

But this time, it's bigger. In fact, it’s more than 10 times bigger.

Importantly, ONE now has another USA case study to start working into the lucrative and huge broader USA hospital market which, according to the American Hospital Association survey in 2019, contains 919,559 hospital beds across 6,090 hospitals.

To put it into perspective, in 2020 ONE generated its $7.8M annual recurring revenue from just 9,259 hospital beds.... That’s only about 1% of the total hospital beds in the USA.

As a very rough calc: $7.8M annual recurring revenue divided by 9,249 beds = ~$843 per bed per year.

Using this very rough figure, today’s deal is potentially worth up to ~$2M per year in recurring revenue.

In previous communications about ONE we’ve stressed how the recent capital raise of $20M could facilitate a “land grab” style move, designed to accelerate ONE’s US market penetration.

And in our last note on ONE, we highlighted how ONE’s quarterly revealed it has seen a significant increase in Requests for Information (RFIs) and Requests for Proposal (RFPs) - formal processes for evaluating and potentially purchasing ONE’s tech.

In the tech world, a “land grab” is a bold play to rapidly grow your user base and build top-line revenue, and in turn gobble up market share.

In our view, ONE’s deal announced today is evidence of the early success of that strategy, especially in the giant US market.

We’ve also highlighted how ONE’s deal flow is lumpy, but usually material when it comes through.

Today’s news is in keeping with that theme - but we believe it could be THE pivotal moment for ONE’s trajectory.

ONE is contending with a pandemic-strained US healthcare system, legacy infrastructure and a large volume of legwork that is needed to get US healthcare providers to invest in efficiency gains via technology.

But that healthcare system we think has now woken up to the need for efficiency and ONE’s product is the tool for delivering that efficiency - which was the main point of our last ONE note.

In short, we believe that for ONE to get a healthcare network of BJC’s stature, and a deal of this scope, speaks directly to ONE’s potential to play a major role in the modernisation of patient experience and healthcare service delivery in the US going forward.

The other key proof points we are happy to see today are:

- That BJC was an existing ONE user, so they are happy enough with the product to do a huge expansion.

- BJC are migrating to ONE’s new cloud version - a significant proof point for the new cloud based technology

ONE is now well on its way to smashing through the 15,000 contracted bed marker we laid out in our 2022 ONE Investment Memo.

Contracted beds is a metric that’s like “active users” for most tech companies - it's correlated with revenue growth and we believe it will be the primary measure of ONE’s success.

Importantly, ONE’s customers are sticky and the length of the contracts are long, for example like the Kingman deal, which was for 5 years.

Sticky customers smooth out cash flows for a business and generally, we believe this makes Software as a Service (Saas) companies like ONE appealing to institutional investors.

Here are the details of today’s deal:

- 2,441 beds

- Extension of partnership for a further 6 years

- Represents material increase of 20% in contracted beds

Today's deal means ONE is just shy of the 15k beds target we outlined as ONE’s number one objective for 2022.

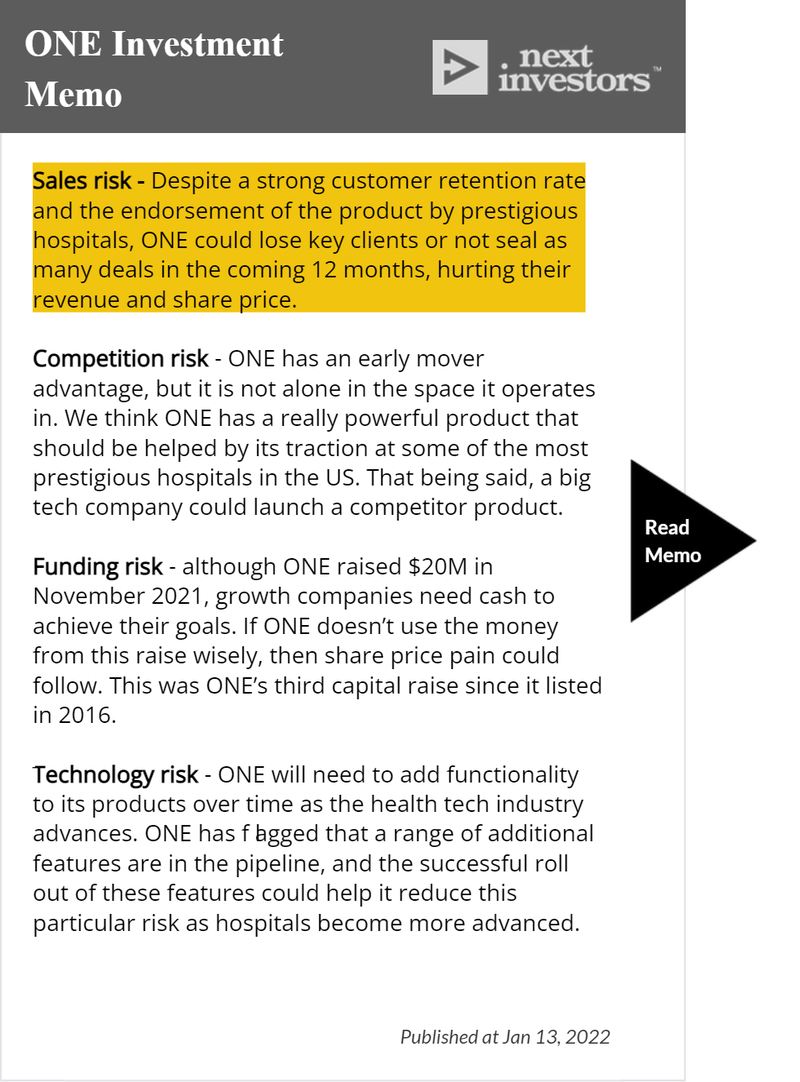

Risks

We see today’s deal as de-risking our ONE investment with regards to sales risk:

Here’s our previous ONE coverage

In March 2021, we announced ONE as our Tech Pick of the Year for 2021.

A few weeks later, we provided our deep dive analysis that outlined the 10 reasons that we invested in ONE.

Then, later that month, we revealed how we expect ONE’s new cloud offering to turbocharge growth of new hospital clients, hospital beds and recurring revenue.

In April, ONE released its quarterly results demonstrating its progress. Revenue was up 64% on the prior year, while costs were down 84%. It also reported that a number of clients had renewed their contracts, a sure sign of confidence in the company and its technology.

Progress continued in May, when New York based hospital NYU Langone, one of the top 10 best hospitals in the USA, delivered an hour long webinar on the benefits they are getting from ONE’s technology.

You can watch clips from that webinar here, or read the transcript.

After having only launched its cloud offering in March, by June, ONE had secured a five year contract with Victoria's largest private health service, Epworth HealthCare, for all 1,440 of its beds.

Just eight days later, ONE announced its second cloud deal, this time with Northern Health in Melbourne — another important proof point that ONE’s cloud strategy was working.

In late-July, ONE reported another quarter of strong growth, which proved to be much better than our expected milestones for the company.

In October 2021, ONE announced a material new 5 year contract for 235 hospital beds worth $2.4M USD, with USA based hospital Kingman, using ONE's new cloud offering, as the first deal under the Microsoft co-sell agreement and using Samsung tablets.

In November, we broke down the ONE ‘land grab’ capital raise. ONE raised $20M in cash that will be used to accelerate sales and adoption, specifically in the US healthcare market.

We then looked at how ONE achieved a record quarter after the cash injection.

And our last piece of coverage, the flood of RFP/RFIs - which was then followed by today’s news.

ONE Investment Memo

In our ONE Investment Memo you’ll find:

- Key objectives for ONE in 2022

- Why we invested in ONE

- What the key risks to our investment thesis are

- Our investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.