Oneview’s Latest Quarterly Shows 3x Increase in RFPs/RFIs

Disclosure: The authors of this article and owners of Next Investors, S3 Consortium Pty Ltd, and associated entities, own 8,525,000 ONE shares at the time of publication. S3 Consortium Pty Ltd has been engaged by ONE to share our commentary and opinion on the progress of our investment in ONE over time.

Our healthtech investment, Oneview Healthcare (ASX:ONE), put out its quarterly report today, which shows a possible future demand surge for its products brought on by the pandemic.

We think the report provides a good look at ONE’s sales pipeline and potential growth trajectory after its recent $20M capital raise:

- The big one for us - 8,630 beds worth of RFIs/RFPs (sales pipeline)

- Cash balance of €11.8M

- Net operating cash outflow of €3.3M ($4.8M)

- OEM (Original Equipment Manufacturer) hardware up-front payments of €1.2M ($1.77M)

- Revenue of €1.6M ($2.37M) vs €2.8M ($4.14M) vs last quarter (down 45%)

Requests for Information (RFIs) and Requests for Proposal (RFPs) are formal processes for evaluating ONE’s tech for implementation in a hospital and an important part of ONE’s sales pipeline.

This is on top of direct to customer sales which ONE says it is actively progressing.

So as of today’s quarterly, that’s a minimum ~3x growth in customer interest as represented by RFP/RFI numbers vs last quarter.

In the last six months, ONE signed a number of big contracts which explains once off, OEM hardware upfront payments of €1.2M ($1.77M) - coverage on these contracts can be found later in this note.

We’ll also do a thorough breakdown of how ONE generates sales later in this note and explain why we’re bullish on their prospects this year.

We also visited the ONE offices this week to get a live demonstration of their tech.

If there’s a single takeaway from that meeting, it’s that ONE’s tech is a comprehensive solution to healthcare inefficiencies.

ONE’s tech gets right into the guts of a healthcare system and makes the patient experience better while giving healthcare workers more time to deliver quality care.

We think this will make it a preferred product for hospitals as a combination of legacy problems and the pressures of the pandemic drive lasting tech-driven change.

We also think that after today’s quarterly, the hospital system has finally woken up to the pressing need for tech-driven change - as evidenced by the RFP/RFI numbers.

Now we are waiting to see if this pipeline converts to contracts towards our 2022 objective for ONE to reach 15,000 contracted beds. By our calcs ONE is currently sitting on about 11,842 beds.

Here’s how we’ll approach today’s note:

- More on today’s ONE quarterly report

- Growth in ONE’s sales pipeline

- Sales and marketing update

- Our ONE site visit

- Introducing ONE’s new Australia MD, Colin Hackwood

- What’s next for ONE?

- Key Risks for ONE

- Our ONE Investment Memo

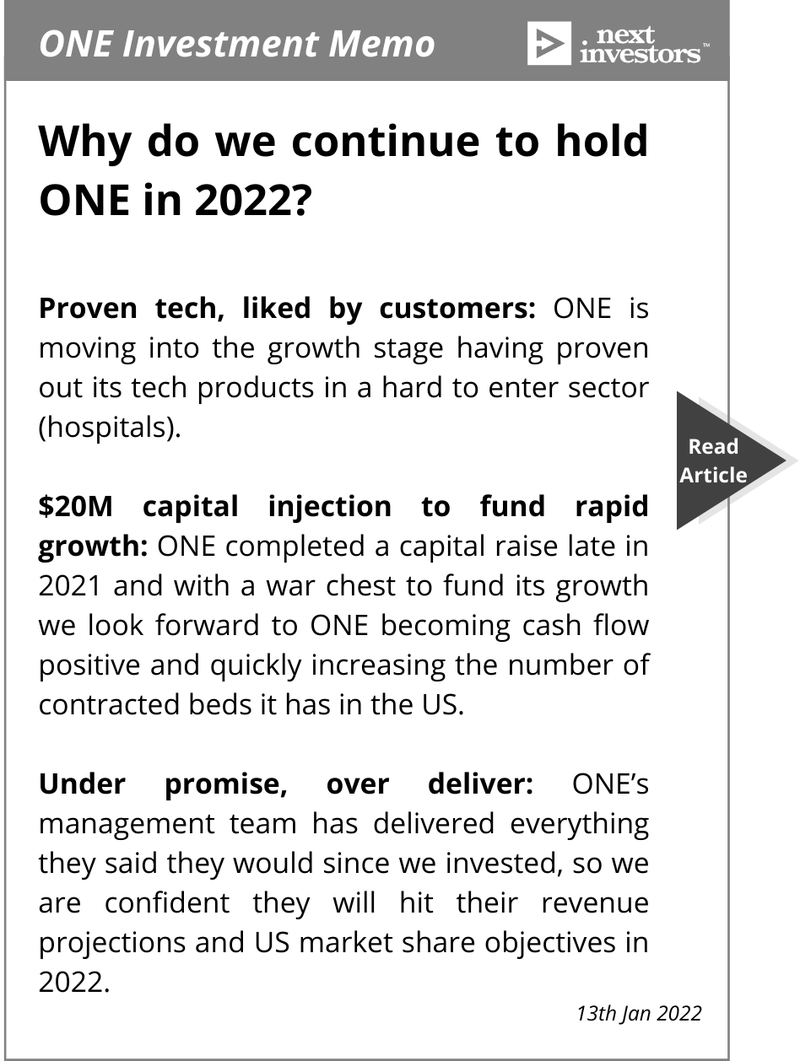

Below is why we continue to hold ONE in 2022:

More on today’s ONE Quarterly:

Here are the key details again from today’s ONE Quarterly:

- The big one for us - 8,630 beds worth of RFIs/RFPs (sales pipeline)

- Cash balance of €11.8M

- Net operating cash outflow of €3.3M ($4.8M)

- Including once off OEM hardware up-front payments of €1.2M ($1.77M)

- Revenue of €1.6M ($2.37M) vs €2.8M ($4.14) vs last quarter (down 45%)

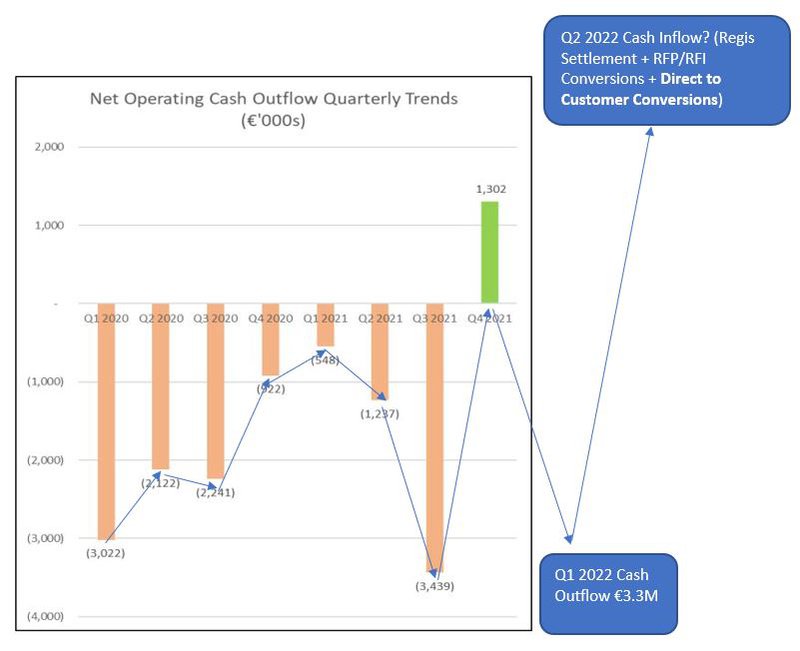

The headline for some casual observers of ONE might read increased cash outflow, revenue down, etc.

But this completely misses the core point of today’s announcement.

As long-term holders of ONE, we’ve often noted how ONE’s dealflow is lumpy.

What happens is that ONE signs a deal (usually five year duration) with most of the hardware costs that ONE incurs front loaded into the first year.

This is a one off cost that won’t appear in subsequent years (for this particular contract at least) which explains the upfront OEM hardware payments of €1.2M ($1.77M).

While this can affect market optics around quarterlies, these are non-recurring costs while ONE’s subsequent revenue from that contract is recurring.

The greater need for hardware is actually a big positive for ONE.

It means the company is paying one off hardware costs for more contracts, that will be recouped in multiples over the duration of the contract, and even MORE if the contract term is extended when it ends.

If last quarter’s breakthrough moment for ONE was operating cash flow positive status (+€1.3M), then despite initial perceptions of today’s result, next quarter for ONE promises to be an even bigger breakthrough.

As a result we feel comfortable with the cash outflow this quarter:

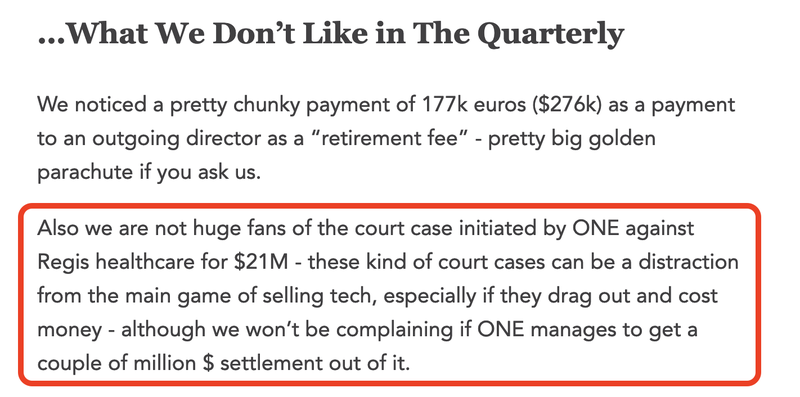

Throw in the fact that ONE settled a long-running legal dispute with Regis for $2M payable to ONE within 30 days from 14 April (these numbers will come through next quarter), and all signs point to a big Q2 for ONE - with more to come.

Back in April 2021 we wrote in our quarterly analysis of ONE that we didn't like that they were pursuing a case against Regis as we thought it would be a distraction and expensive.

Today we are enjoying eating our humble pie... $2M is a great result for the ONE war chest.

Here’s why those RFI/RFP numbers are important:

Why do we think ONE’s sales pipeline is growing?

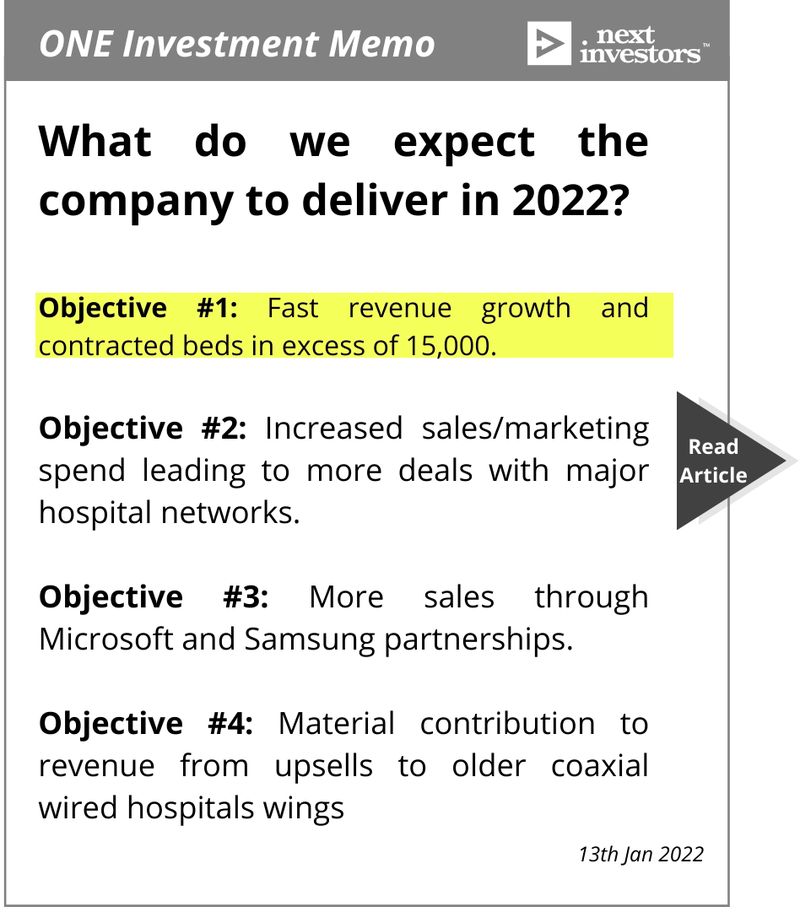

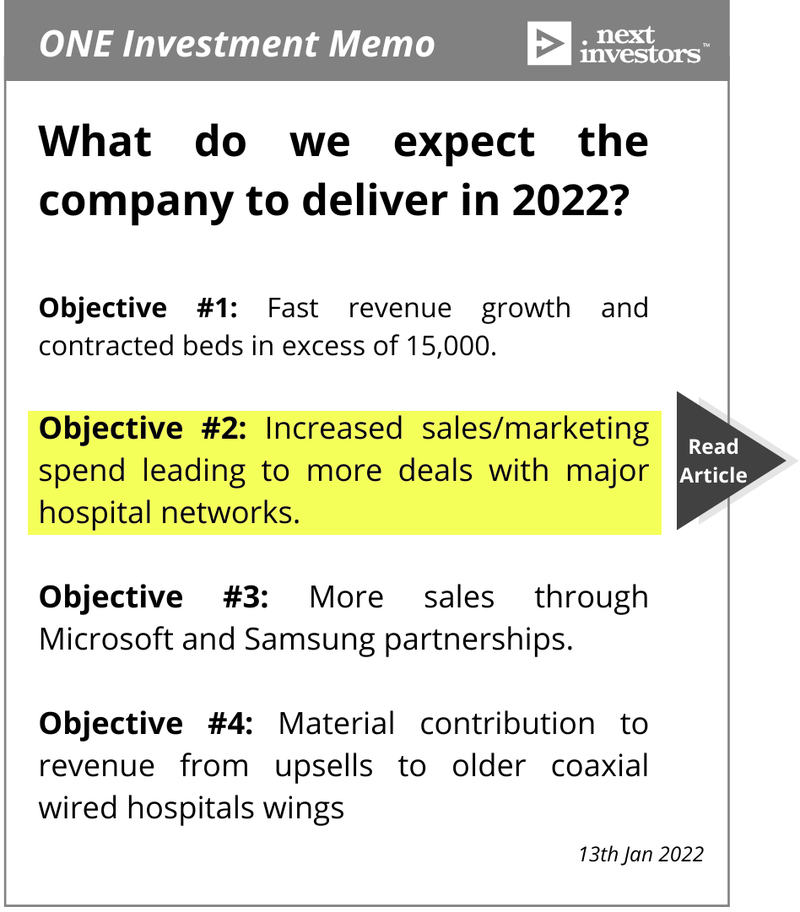

Our big shiny goal for ONE this year is to have a total of 15,000 contracted beds globally:

We think that today’s quarterly points to Objective #1 definitely being achievable given what’s going on in ONE’s sales pipeline.

The sales pipeline is being driven by the fact that the US healthcare market is experiencing immense cost pressures.

There’s a great in-depth summary of these costs available on the American Hospital Association website.

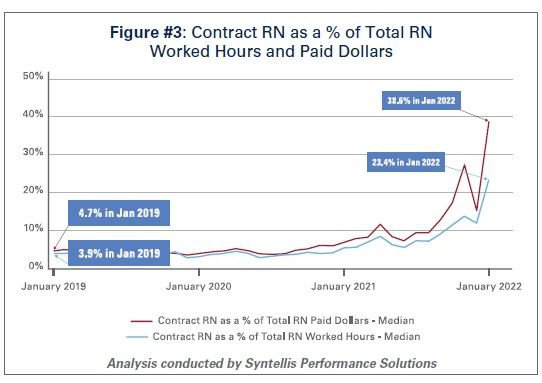

One chart that really stood out for us is this one:

The American Hospital Association notes that: “In 2019, hospitals spent a median of 4.7% of their total nurse labor expenses for contract travel nurses, which skyrocketed to a median of 38.6% in January 2022”

The result:

- Billions of dollars in losses over the last two years for hospitals - over 33% of hospitals are operating on negative margins

- By the end of 2021, total hospital expenses were up 11% vs pre-pandemic levels in 2019

And the human toll:

“High reliance on contract or travel staff prevents hospitals and health systems from investing those costs into their existing employees, leading to low morale and high turnover, which further exacerbates the challenges hospitals and health systems have been facing.”

The pandemic has led many hospital administrators to champion the use of tech to solve these problems.

This has resulted in a large volume of RFPs/RFIs for ONE which are defined as such:

RFI: Request for Information - “is a formal process for gathering information from potential suppliers of a good or service. RFIs are intended to be written by customers and sent to potential suppliers. An RFI is typically the first and most broad series of requests intended to narrow down a list of potential vendor candidates.”

Simple version: RFI is when a hospital wants to know more detail about the technology and how it works, providing specific questions to the tech provider

RFP: Request for Proposal - “is a business document that announces a project, describes it, and solicits bids from qualified contractors to complete it. Most organizations prefer to launch their projects using RFPs, and many governments always use them.

When using an RFP, the entity requesting the bids is responsible for evaluating the feasibility of the bids submitted, the financial health of the bidding companies, and each bidder's ability to undertake the project.”

Simple version: is when a hospital wants a tailored proposal and costs for their specific needs, and RFI often leads to an RFP

The upshot of these definitions:

There are two bureaucratic processes in the US healthcare system ONE is targeting - RFPs are a more advanced step than an RFI - but both are used by hospitals to figure out what products are right for them. The more RFPs there are, the more likely it is a % of them will convert to a successful contract

An RFP is a strong signal from a hospital that they may ultimately buy ONE’s product.

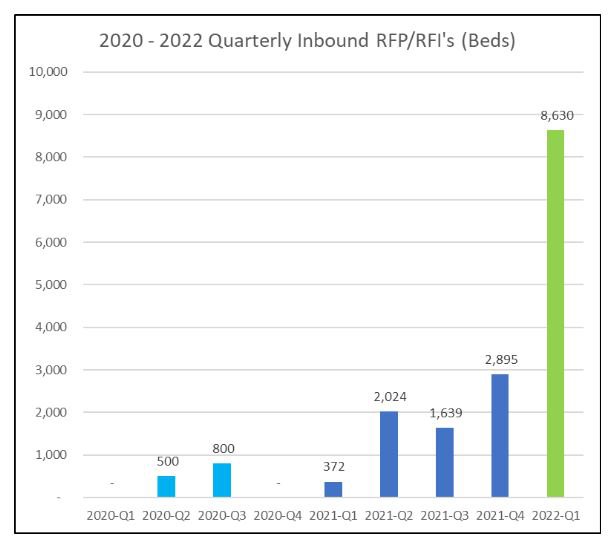

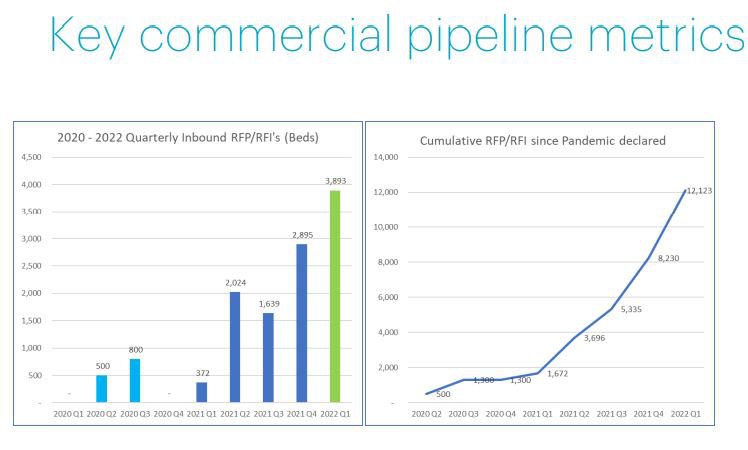

Below is this massive growth in RFI/RFPs received by ONE:

This is a significant leap forward for ONE’s sales pipeline when compared with the half-yearly numbers:

The difference between the two charts is almost 5,000 beds.

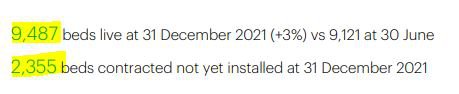

If ONE can convert around half of those Q1 RFP/RFI numbers ALONE then we expect it to smash through our #1 Key Objective (15,000 contracted beds) by the end of this year in light of the latest contracted bed numbers from the half yearly presentation:

That’s a total of 11,842 contracted beds as of Dec 31 2021.

There’s also some interesting language in the quarterly which alludes to another channel in their sales pipeline other than the RFP/RFI channel:

“We also remain engaged with a number of existing and prospective customers that may procure directly without going to RFP.”

Direct to customer sales are a large positive for ONE. The RFP/RFI process is competitive as multiple vendors receive the requests and the hospital assesses the best one. We assume that direct to customer sales have a higher likelihood to close.

Sales and marketing update

The key for ONE is converting on its direct to customer and RFP/RFI channels.

Aiding that cause is an increase in advertising and marketing spend following the most recent capital raise (from half year report):

Increased capital allocation to sales and marketing, we expect will take around six months to convert into new deals. So we expect to see the fruits of that increased spend later in 2022, ideally getting ONE closer to our #1 Key Objective - the 15,000 bed target.

We highlighted sales and marketing spend was important for ONE in our Investment Memo:

We’re now of the view that this Objective is accomplished and there is enough momentum in the sales pipeline now to deliver material increases in revenue going forward.

Our ONE site visit

As we discovered in our site visit to ONE’s offices, ONE’s product has a dual sided appeal:

- It makes the patient experience better

- It helps healthcare workers deliver quality care

It does this with a powerful suite of tools for patients, nurses and hospital administrators.

We got the same sales pitch that ONE gives these administrators.

ONE keeps a detailed record of the time it saves nurses, which in turn shows administrators how they can bring down labour costs in an environment where there is a nursing labour crisis playing out.

Meanwhile, patients get an improved experience via an intuitive interface which looks like this:

Instead of a nurse going room to room taking meal orders - ONE’s product does that.

Instead of nurses repeating the same educational script - ONE’s product replaces that with easily viewable video content, saving more time.

Nurse rounds are accounted for, reducing fall incidence numbers, improving compliance and reducing insurance costs.

Visual representations of nurse rounds allow for quality of care audits for administrators and nurses can provide better quality care when they are in a patient's room.

It all adds up to a better bottom line for hospitals - the initial investment pays for itself over time, and quickly.

That’s why ONE’s customers are extraordinarily sticky - its customer retention rate is 98%.

We know ONE already has a significant foothold in Australian hospitals and its Australia Managing Director should solidify that foothold.

Introducing ONE’s new Australia MD, Colin Hackwood

There’s a nice quick bio of Colin Hackwood which can be found here.

Starting out in nursing, Mr. Hackwood has had leadership roles across the healthcare sector.

In short, Colin’s deep understanding of hospitals we think should be a boon to ONE’s Australian sales.

What’s next for ONE?

Given the RFP/RFI numbers, we’re looking for the following:

- Further sales and revenue growth to hit the 15,000 bed target

- US growth

- Q2 - another cash flow positive quarter

- Additional sales and marketing spend

All of this we think is achievable.

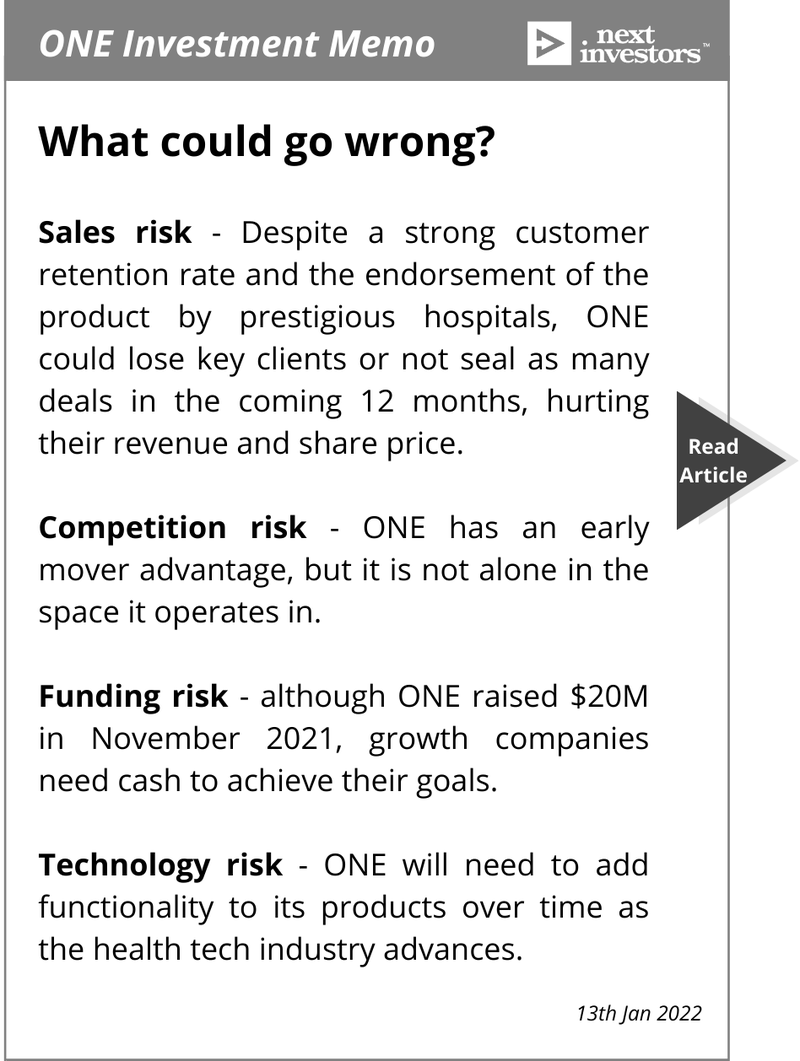

That being said there are a number of risks that may present as well.

Key Risks for ONE

We’ve highlighted the risks for ONE below:

The RFP/RFI numbers help reduce sales risk, but do not eliminate it.

Competition risk is ever present, but our site visit underlined why we think ONE has the best product in the market.

Funding risk we don’t perceive as a significant risk in the immediate future as ONE has a cash balance of Cash balance of €11.8M

Technology risk is also an aspect of ONE’s operations and they may need to increase its spend on new functionality as hospitals expect more from their tech partners.

New to ONE? Here’s our previous coverage

In March 2021, we announced ONE as our Tech Pick of the Year for 2021.

A few weeks later, we provided our deep dive analysis that outlined the 10 reasons that we invested in ONE.

Then, later that month, we revealed how we expect ONE’s new cloud offering to turbocharge growth of new hospital clients, hospital beds and recurring revenue.

In April, ONE released its quarterly results demonstrating its progress. Revenue was up 64% on the prior year, while costs were down 84%. It also reported that a number of clients had renewed their contracts, a sure sign of confidence in the company and its technology.

Progress continued in May, when New York based hospital NYU Langone, one of the top 10 best hospitals in the USA, delivered an hour long webinar on the benefits they are getting from ONE’s technology.

You can watch clips from that webinar here, or read the transcript.

After having only launched its cloud offering in March, by June, ONE had secured a five year contract with Victoria's largest private health service, Epworth HealthCare, for all 1,440 of its beds.

Just eight days later, ONE announced its second cloud deal, this time with Northern Health in Melbourne — another important proof point that ONE’s cloud strategy was working.

In late-July, ONE reported another quarter of strong growth, which proved to be much better than our expected milestones for the company.

In October 2021, ONE announced a material new 5 year contract for 235 hospital beds worth $2.4M USD, with USA based hospital Kingman, using ONE's new cloud offering, as the first deal under the Microsoft co-sell agreement and using Samsung tablets.

In November, we broke down the ONE ‘land grab’ capital raise. ONE raised $20M in cash that will be used to accelerate sales and adoption, specifically in the US healthcare market.

And in our most recent previous coverage of ONE, we looked at how ONE achieved a record quarter after the cash injection.

Our ONE Investment Memo

In our ONE Investment Memo you’ll find:

- Key objectives for ONE in 2022

- Why we invested in ONE

- What the key risks to our investment thesis are

- Our investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.