ONE 2023 Full Year Results Out - Plus Some Surprises…

Disclosure: S3 Consortium Pty Ltd (The Company) and Associated Entities own 7,933,333 ONE shares at the time of publishing this article. The Company has been engaged by ONE to share our commentary on the progress of our Investment in ONE over time.

A new contract with a major US hospital group, Mercy Health.

The first purchase order through a recently signed US distribution partner.

Plus a new 100-strong team ready to sell and support into the US market?

... AND a breakthrough mobile based product that allows patients to access the product on their phone was launched yesterday.

Six weeks ago we covered Oneview Healthcare’s (ASX:ONE) quarterly results when the share price was at 24c.

Over the last few weeks ONE has been comfortably trading between 30c and 35c.

ONE is a health tech company that provides hospital patients a “virtual care and digital control centre” at their bedside.

ONE’s products are cloud-hosted, patient dashboards that help make hospitals more efficient and patients more engaged in their own care.

ONE is currently our largest holding and has been enjoying a slow and steady share price rise over the last 10 months.

The market looks like it is rewarding the progress ONE made in 2023 laying the groundwork for a jump in growth during 2024.

The two key drivers: its new partner $32BN Baxter International AND its Bring Your Own Device (BYOD) mobile app which brings ONE’s products into mobile users’ palms.

This morning ONE presented its full year results in an investors call, and provided some outlook for the year ahead (and a couple of surprises).

Today we provide our summary and key takeaways from the ONE investor call.

First, here is the 60 second summary:

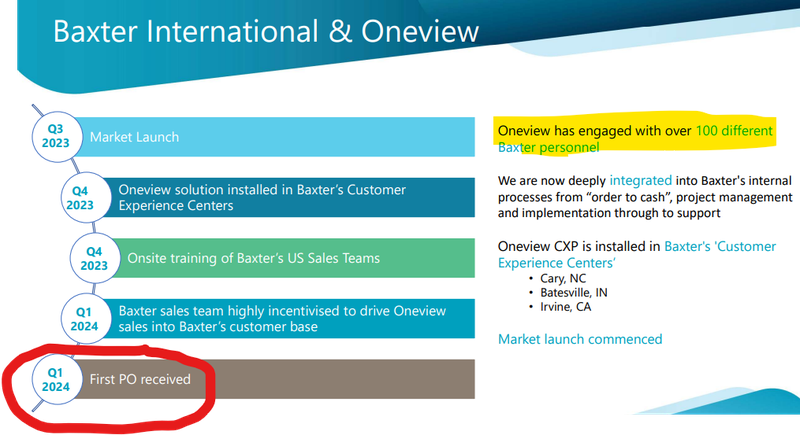

- First purchase order received from reseller partnership with $32BN Baxter (who owns 75% of the US hospital bed market).

- 100 Baxter personnel engaged with ONE on how to sell/support/upsell it to their prospects and clients.

- New major US hospital Mercy Health signed. First deployment next month, with 2,800 additional beds in advanced negotiations.

- BYOD Product is now launched as “MyStay” and is being used by a prestigious US hospital right now.

- ONE going ‘elephant hunting’ in 2024 - aiming to sign BIG, hard to convince clients with large lifetime customer value potential. Any breakthroughs here could further re-rate the ONE share price.

A recording of today’s investor call is available on the ONE website under the “investor” section - or you can just click this link to listen to it directly.

Our key takeaways from today’s conference call

First Baxter International Purchase Order is in $32BN capped Baxter International is the largest hospital bed supplier in the US.

ONE signed a “Value Added Reseller Agreement” with Baxter in November 2023.

The idea and synergy is that Baxter and their giant sales team will sell and upsell ONE tech along with Baxter’s existing suite of hospital room products.

Baxter now has 100 staff trained up on how to sell and support ONE’s products into their huge customer base.

Today we learned that ONE’s first Baxter purchase order is now in.

(Source)

So why is this a big deal?

Many of us will have been invested in companies that sign a “partnership deal” with a major group as a sales channel that promises lots of new sales...

But we have seen many of these partnerships that sound great, but don’t translate to new contracts or revenue.

To receive a purchase order from the Baxter partnership only a few months after the deal was done is highly encouraging for the future prospects of the partnership.

We also learned that Baxter has an incentive structure set up to make sure more ONE product sales happen.

ONE also has a separate incentive structure as well for Baxter’s sales reps and account executives.

This will further help ONE build market share.

We expect big things from the ONE’s Value Added Reseller Agreement with Baxter. (Read more about the initial deal with Baxter here)

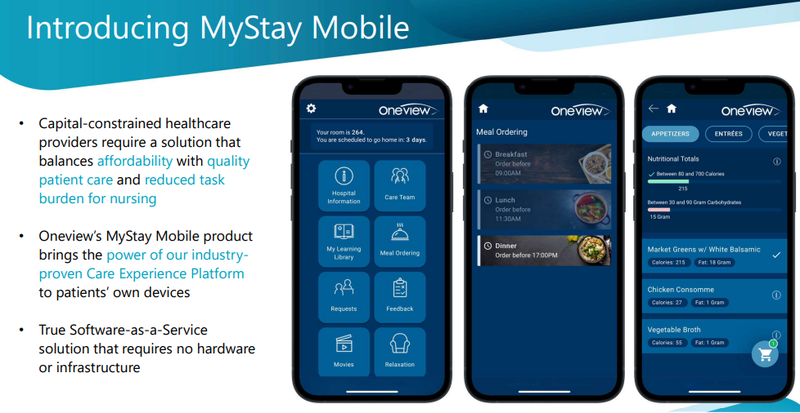

BYOD is now called “MyStay” and was launched yesterday

ONE’s web browser based product now has a name - it’s called “MyStay” instead of just Bring Your Own Device (BYOD).

This is what it looks like:

(Source)

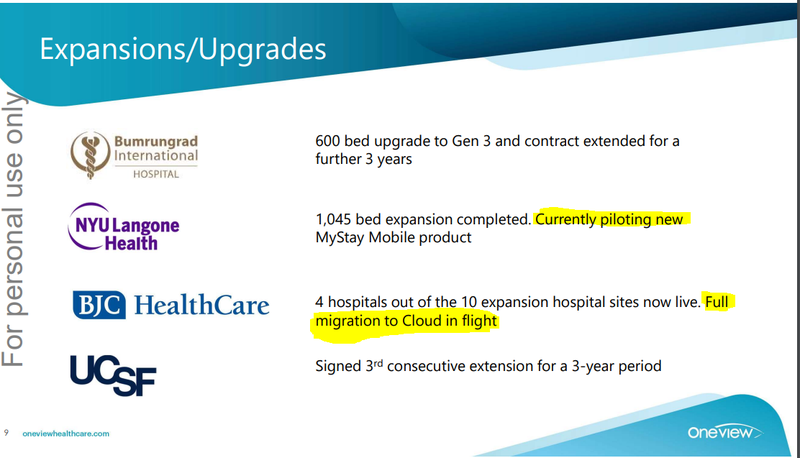

A ~1k bed pilot program is underway with NYU Langone - one of the most prestigious hospitals in the US and a long-term ONE client.

This is very important for ONE as it will help the company transition into a true Software as a Service (SaaS) model, with deep market penetration.

These kinds of tech companies can be highly valued by the market.

ONE CEO James Fitter noted that 70% of US hospitals DON’T HAVE a Customer Experience Platform (CXP) - this is what ONE specialises in.

As a result, selling ONE’s product is one of the best avenues Baxter has for growth.

Importantly, the Baxter Value Added Reseller Agreement now includes “MyStay” and between Baxter’s reach and MyStay’s scalability, we think this will supercharge ONE’s contracted beds over the coming quarters.

“MyStay” is a very clear value proposition for hospitals

Any spending decision that a hospital makes needs to have some sort of direct/indirect Return on Investment - the ROI.

Some industries call that a ‘business case’ or ‘value proposition’.

It could be an increase in revenues or a way to reduce costs.

James touched on the immediate value propositions that ONE is able to show hospitals when it is looking to make new sales.

The two key points he made was as follows:

- MyStay digital meal ordering - James mentioned that digital meal ordering typically has a ~95% adoption rate and results in ~87% reduction in food waste. This gives hospitals a quick easy win which at scale could lead to big cost savings/efficiency gains.

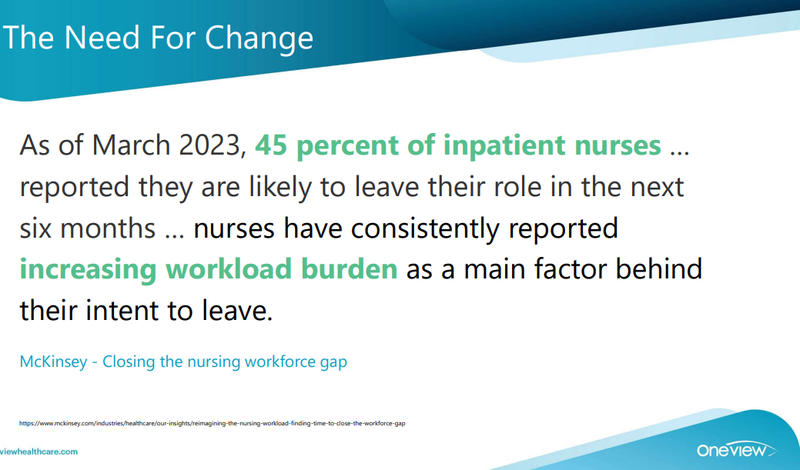

- Nurse time is precious - James also mentioned that every time food is ordered ~3 minutes of nurse time is wasted. This could help solve a real problem for hospitals which is the difficulty to find and retain nursing staff.

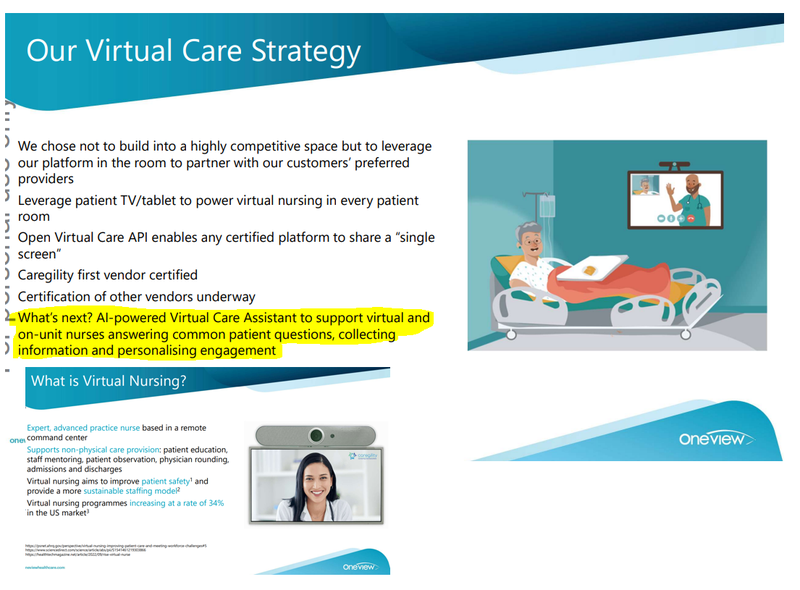

On the nurse shortage issue, ONE also touched on its “virtual nursing” strategy and how it fits into its overall virtual care strategy.

The following slide gave us a pretty good idea of where ONE is looking to take its product in the future - an almost “control room” like product offering for hospitals that we think could exponentially reduce the workload of nurses & help solve a major problem for hospitals all over the world.

Especially if ONE’s MyStay app is adopted by patients.

Artificial Intelligence (AI) also got a solid mention in today’s ONE call...

AI is a big investment thematic right now, and particularly in the healthtech space.

Today, we learned that AI is driving ONE’s product development - meaning faster product upgrades, more new features.

ONE is also looking at external applications of AI and ONE CEO James Fitter is now enrolled in an Oxford University AI course for executives - a sign of ONE’s commitment to harnessing the power of AI.

The product innovation doesn’t stop there for the company - ONE is also working on Virtual Care products, something ONE’s clients are actively seeking.

We think given ONE’s strong reputation and relationship with prestigious US hospitals, its new product innovations will be well received and continue to drive sales.

Long term customers all showing interest in ONE’s cloud product

ONE spoke about the progress being made with its long term customers.

James mentioned all have shown an interest in moving over to ONE’s cloud product.

(A few years ago, ONE invested in moving its technology from on premise servers to being cloud hosted, making it easier for hospitals to buy and roll out the ONE technology, and enable a “land and expand” sales strategy” - we explain in more detail here).

NYU Langone is currently piloting the MyStay BYOD product, and BJC Healthcare are already doing a full migration to the cloud.

What we think that means for ONE...

At the end of the day it comes down to the benefits a SAAS product offers.

Any new customer that signs up or switches to ONE’s SAAS product means higher margins on revenues.

James touched on the difference between a typical hardware sale compared to a SAAS sale and said:

“Selling hardware is very much about selling a product at a mark up and that mark up is under pressure when a customer has a limited CAPEX budget - like hospitals do.”

James mentioned that a move to cloud and its MyStay product could take the business’ “Blended margin into the mid 80%”.

ONE’s BYOD “MyStay” product solves integration problems

James mentioned that the pushback at the sales level is never about the value proposition of ONE’s products but is almost always at the CAPEX required to integrate.

When it comes to capital expenditure, hospitals will tend to prioritise hardware like new MRI machines or renewing ageing medical devices over patient experience.

This dilemma makes it harder for hospitals to commit to buying ONE’s hardware products.

Despite that, ONE has managed to build a very decent orderbook...

Now with the “MyStay” product, ONE is taking away perhaps the biggest friction factor when it comes to making new sales.

Instead of having to convince a hospital to make a large CAPEX decision, all ONE has to do is convince the hospital to make a subscription payment.

James was later asked about the differences between onboarding a customer for hardware vs “MyStay” and he mentioned that deploying ONE’s hardware solution would come with CAPEX costs upwards of $250,000 in the first year.

BYOD on the other hand has no upfront capital or hardware cost under a more simplified subscription model.

When it comes to sales, ONE is in the “elephant hunting business” as James put it.

This means ONE is trying to sign BIG, hard to convince clients with large lifetime customer value potential.

We think the MyStay product will be a game changer for ONE when it comes to getting big hospital networks to make a purchasing decision, especially when the cost of implementation is relatively modest.

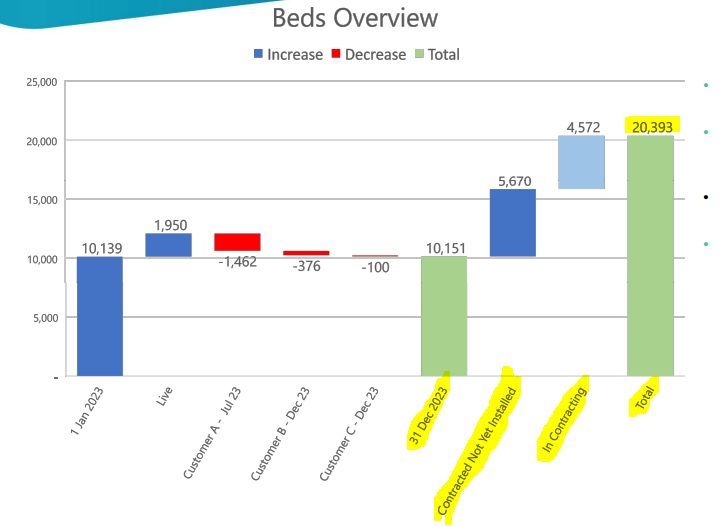

$15M in contract value re-signed - 2.8K beds to come online.

As Investors, our #1 Objective that we wanted to see ONE achieve in 2024 is to hit 25,000 contracted beds.

ONE had ~10,151 beds installed and operational at 31 December 2023 with ~5,070 contracted but not yet initiated.

That's a total of ~15,200 beds.

In addition to that, ONE confirmed ~4,572 beds were at the negotiation stage - which means ONE has in its pipeline right now a path to ~20,000+ beds installed by the end of 2024.

Today ONE mentioned that a new contract had been signed with Mercy Health (a large healthcare network across primarily the southern US.

First deployment is next month, with an additional 2,800 beds in contract negotiation.

This deal would go a long way for ONE to hit its sales goals.

We mentioned in our ONE Investment Memo that we want to see the company hit 25,000+ beds by the end of this year.

And considering the MyStay product was only launched yesterday, we think ONE has a good chance of achieving that target.

ONE also touched on the new customer wins which sees ONE add €11.7M in total lifetime contract value and €1.9M in annual recurring revenues to the business’ top line numbers.

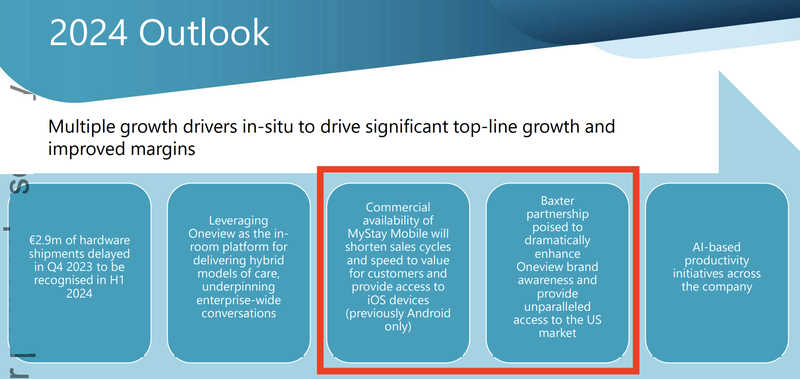

ONE’s 2024 outlook

One thing that we always look out for on these conference calls is the 12-month guidance and outlook from the management team.

ONE made it very clear that a large part of the company’s direction in 2024 would be around the launch and distribution of its “MyStay” product.

Two of the five “pillars” focused on the MyStay product:

- Shortening the sales cycle with low CAPEX integration costs.

- The Baxter partnership to increase ONE’s brand awareness and access to the US market.

What could go wrong?

In the short term, the three key risks to our ONE Investment Thesis are “Sales Risk”, “Distribution Partner Risk” and “Market Risk”.

Sales Risk because there is always a chance ONE could lose key clients which could impact revenues negatively.

There is also a chance it takes a lot longer to secure new sales which could impact the growth trajectory of the company and in turn the perception of the market for how much growth there is ahead for the company.

Both scenarios would negatively impact ONE’s share price.

Distribution Partner Risk because a large part of ONE’s strategy is to sell its products through a distribution partner like Baxter.

Although ONE has a strong relationship with this companies, if they move slowly - or don’t prioritise ONE’s products when making a sale - then it could reduce the sales outcomes for ONE.

Market Risk is always a factor for ONE because tech valuations can be volatile when the overall market is choppy.

Tech stocks could fall in value again.

Even if ONE does everything right from an operational standpoint, the market could always sell off or favour different sectors.

To see more risks to our ONE Investment Thesis, check out our ONE Investment Memo here.

Our ONE Investment Memo

In our ONE Investment Memo you’ll find:

- ONE’’s macro thematic

- Why we Invested in ONE

- Our ONE “Big Bet” - what we think the upside Investment case for ONE is

- The key objectives we want to see ONE achieve

- The key risks to our Investment thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.