ONE: What we are watching out for?

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 7,733,333 ONE shares at the time of publishing this article. The Company has been engaged by ONE to share our commentary on the progress of our Investment in ONE over time.

Oneview Healthcare (ASX:ONE) is currently our largest shareholding.

The reason we hold a large position comes down to our strong conviction that hospitals are well overdue for new technology.

And we think ONE can execute its plan to help deliver it to them.

ONE is a healthcare tech company that provides hospital patients a “virtual care and digital control centre” at their bedside to deliver the best possible patient experience during their hospital stay.

If you or a loved one have ever been to hospital you probably noticed how cruddy and dated the experience was.

(when was the last time you saw an old cathode-ray tube, box style TV... probably in a hospital)

The pressure put on hospitals during the unique circumstances of the 2020 pandemic has accelerated the trend of hospitals transforming with modern technology.

(similar to how “work from home” and “video calls” suddenly became a thing).

Think of ONE’s tech as a single touch screen at your hospital bed where you can:

- Have virtual consultations with relevant medical specialists - local and from around the world.

- Control all aspects of your room - bed, lighting, temperature.

- Order food, watch movies, get a nurses attention - like the screen you get in your airline seat when flying.

- Interact with tailored rehab, education and training videos - for a patients specific health situation, and;

- Monitor your health outcomes - Doctors and nurses will have better info on you, replacing the clipboards, pen and paper currently used for this

All of the different functions you want and need during your hospital stay in one view.

(get it...? Oneview)

Here is what Oneview looks like at the patient's bedside:

And here is that the Oneview interface looks like for a patient:

ONE’s technology connects the patient in the hospital bed to nurses, meal service, medical images and records, educational content, entertainment and other in room systems.

Importantly, ONE’s technology is now also available on a patient’s own mobile phone - more on this in a moment...

From an investment perspective:

ONE sells its technology to hospitals on a yearly recurring licence fee, per hospital bed.

The more hospital beds signed by ONE = the more recurring yearly revenue to ONE.

ONE is currently contracted for 17,808 hospital beds around the world as of April 2024.

(ONE reported $11.6M annualised recurring revenue in their 2023 annual report)

ONE is currently used in nearly 2% of the ~920,000 total hospital beds in the USA.

We want to see them materially increase their US sales.

In June 2023, ONE announced a “value added reseller agreement agreement” with $28BN capped NYSE listed Baxter International.

Baxter sells hospital beds and controls ~75% of the hospital beds in the USA.

We think this partnership could be transformational and a company maker for ONE... IF it delivers the new sales velocity for ONE that we hope it will.

Today we provide a quick update on ONE’s progress against our ONE Investment Memo #2 where we documented why we are Invested in ONE, including:

- Our ONE Big Bet

- Our key objectives for ONE to achieve over 12 to 18 months

- Why we are Invested in ONE

- The key risks to our Investment Thesis

- Our Investment Plan

In summary, the key thing we wanted to see in our first Investment Memo #1 (from 2021) was for ONE to hit 15,000 contracted beds.

ONE is now sitting at 17,808 contracted beds.

Investment Memo #1 objective achieved.

We created our second ONE Investment Memo late last year, with a new objective to see ONE get to 25,000 beds by the end of 2024 through leveraging the newly signed value added reseller agreement with Baxter.

(there is 8 months to go for ONE to hit 25,000 beds...)

Our blue sky scenario for our Investment in ONE is to see it progressively re-rate in its share price similar to $12.2BN capped ASX listed Pro Medicus.

ASX listed Pro Medicus delivers healthtech for the medical imaging sector.

Over a 9 year period between 2015 and today, Pro Medicus’ share price is up ~9,400%.

Past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Pro Medicus delivered this return by steadily increasing recurring revenue and adding more users year after year.

So far, ONE has been doing this, too.

First by successfully hitting our original milestone of 15,000 contracted beds...

And now (hopefully) growing that to 25,000 contracted beds by the end of 2024.

Like ONE, Pro Medicus also sells into the healthcare sector (a long, hard sales cycle), but also enjoys sticky customers once they are signed up.

We have done some very rough calculations based on publicly available info from ONE and Pro Medicus, we have tried to strip out non-recurring revenue.

As of FY23, Pro Medicus had $124M in recurring revenue and recently transitioned its business model to a more recurring revenue model.

With a $12.2BN market cap, we think they are trading at >90x revenue multiple.

ONE is currently at ~A$11.6M annual recurring revenue in FY2023, and trading at just a ~16x multiple.

We think this is because the market wants to see a few consistent years of growth from ONE before rewarding it with a higher revenue multiple.

(which we think ONE will deliver if it can hit 25,000 beds by the end of 2024)

What we want to see from ONE over the next few years is to keep growing its recurring revenue (accelerated by the Baxter re-sale agreement) and demonstrate year on year growth every year.

Hopefully that will cause investors to reward ONE with a higher revenue multiple like they do for Pro Medicus.

How does ONE get there?

The “blue sky” bet for ONE - access ONE tech on your own device...

ONE has launched a “bring your own device” (“BYOD”) solution - where patients can bring their own phone or tablet to a hospital and plug straight into ONE’s platform on arrival.

This BYOD solution is now called “MyStay” and has been formally launched in February of this year.

MyStay would effectively strip out all the difficult hardware supply and installation issues that ONE has diligently worked to overcome over the past few years, and make it way easier for hospitals to adopt the solution.

Hospitals are slow tech adopters, and arranging for mobile tablets to be installed in hospital rooms sounds excruciating.

(yet ONE still managed to deliver 17,808 of them)

Less adoption friction = more and faster sales.

Letting the patient use ONE on their own device makes for a much easier and faster sale for ONE.

We think that if successfully rolled out, ONE’s BYOD mobile solution could take the company’s growth exponential.

Imagine a near ubiquitous patient experience platform accessible by patients in major healthcare markets...

The Baxter deal and the BYOD product are key reasons why we continue to hold a large position in ONE.

Our Initial Entry Price for ONE was at 6 cents, we then Increased our Investment in November 2021 cap raise at 27 cents and again a third time at 18 cents in line with the most recent capital raise.

So again, ONE now has two major avenues to securing more contracted beds:

- Baxter agreement

- “Bring your own device” (“BYOD”) solution

We see both avenues as working together to enable ONE to chase down our new goal for our ONE Investment which is to see it hit 25,000 beds in the next 8 months.

This is the priority Objective in our ONE Investment Memo #2.

(ONE successfully achieved what we wanted in our ONE Investment Memo #1 - you can read our full assessment of how ONE performed against Investment Memo #1 by going to our ONE company page and clicking on the tab in the image below)

We see Pro Medicus as a great model of what successful healthtech looks like on the ASX - and more importantly - this shows where we hope our ONE Investment might go.

Note that just because Pro Medicus had success in the past, is not and should not be taken as an indication of ONE’s success in the future.

With that said, we have high hopes for ONE and our new ONE Investment Memo reflects that...

Now that our ONE investment Memo #2 is almost half way through, here is a progress update on how ONE is tracking against what we wanted to see (Memo progress updated shown in green text):

Our Investment Memo: Oneview Healthcare (ASX:ONE)

Memo Opened: 22 Sep 2023

Shares Held: 8,818,333

What does ONE do?

Oneview Healthcare (ASX:ONE) is a health tech company that provides hospital patients a “virtual care and digital control centre” at their bedside.

ONE’s products are cloud-hosted patient dashboards that help make hospitals more efficient and patients more engaged in their own care.

What is the macro theme behind ONE?

Nursing shortages brought on by the pandemic highlighted the systemic issues in healthcare systems. The trend now is for these institutions to modernise by adopting new healthcare technology.

Big tech companies like Google, Amazon and Microsoft are looking to enter the health tech space and companies with an early-mover advantage should thrive or become takeover targets in their own right.

May 2024 Update:

(Source)

Labour costs make up 60% of US hospital’s spending - luckily, ONE’s products saves nurses time, which incrementally add up to significant savings (something ONE has shown in data).

Our ONE Big Bet

“ONE will sign on enough new hospital beds at an accelerating rate to achieve a $1BN valuation (based on 5x to 10x forward annual recurring revenue) and be acquired by a large health tech provider.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved, and it will require a significant amount of luck. There is no guarantee that it will ever come true. Some of these risks we list in our ONE Investment Memo.

Why do we continue to hold ONE?

Proven tech, liked by customers

ONE is moving into the growth stage having proven out its tech products in a hard to enter sector (hospitals). Customers are sticky and sign long term contracts.

May 2024 update:

ONE has secured two major contract renewals since this memo was released - Bumrungrad and UCSF Health, ONE’s customers are sticky.

Value Added Reseller agreement with largest hospital bed supplier in US

ONE now has an initial 2 year “value added reseller agreement” with the largest hospital bed supplier in the US (Baxter International).

Under the agreement, Baxter will sell ONE’s technology to certain customers in Baxters’ current customer base (~75% of the US hospital bed market). Given the market reach of Baxter, this agreement could unlock significant growth in contracted beds for ONE.

May 2024 update:

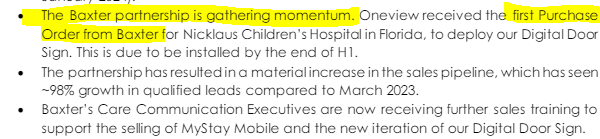

Just recently ONE got its first Purchase Order from the Baxter partnership.

ONE also mentioned in its March quarterly that the Baxter sales team had now been trained to “support the selling of “MyStay Mobile” and ONE’s “Digital Door Sign”.

We are hoping this translates to further sales in the coming months.

Well funded to grow further

ONE completed a $20M placement in July 2023 that should provide the company with the funds it needs to become a sustainable operating cashflow positive business and further penetrate the US healthcare market.

May 2024 update:

ONE ended the March quarter with ~€9.1M (~A$14.8M) cash in the bank.

Considering the company’s current burn rate, ONE should still have at least ~4 quarters of cash to execute its sales strategy. Between now and then we are hoping revenues increase substantially and the burn rate decreases.

Potential faster growth from “bring your own device” (“BYOD”) solution

ONE is developing a platform for patients to use their own phone or tablet.

This upgrade in ONE’s tech could remove the hardware costs associated with setting up ONE in a hospital potentially increasing ONE’s margins, reducing how long it takes for ONE to close a deal - and most importantly, helping hospitals more rapidly improve the patient experience.

May 2024 update:

The MyStay (BYOD) product launched on 26th February this year, after a successful pilot program with NYU Langone Health’s Long Island Community Hospital.

Nursing shortages driving demand for healthcare solutions

Since the pandemic nursing shortages in Australia and the US have worsened.

These shortages put pressure on healthcare systems which causes more stress and ‘burnout’ for existing nurses.

Due to these issues, hospitals are now looking for technology to better improve their healthcare service and reduce the burden on nursing staff.

Although hospitals are notorious technology laggards, we think that the nursing crisis will be the impetus that drives change in these institutions and improves the healthcare system overall.

May 2024 update:

(Source)

Nursing shortages continue to be a major pain point for US hospitals - ONE’s tech helps reduce nurse workloads, delivering labour cost reductions.

What do we expect the company to deliver?

Objective #1: Repeat sales success and hit 25,000 beds

For ONE, ‘contracted beds’ is like an ‘active user’ metric for a tech company. We think this is the basis for judging ONE’s success.

More contracted beds = more revenue.

Building on ONE’s previous 15,000 bed achievement, we want to see ONE hit a total of 25,000 in CY2024, primarily out of the USA.

ONE is projecting growth of 20-25% across this metric in FY23 excluding the potential beds from the Baxter agreement and BYOD solution.

May 2024 Update:

In April, ONE signed a Master Services Agreement with Inova Health System for 1,900 beds.

This large deal instantly tacked on 12% to the company’s bed total bringing it to 17,808 beds.

7,000 more beds in the next 8 months should be do-able if the Baxter partnership delivers (see below)

Objective #2: More deals with major hospital networks through Baxter agreement

We want to see ONE sign more deals with more hospitals.

Given Baxter’s large share of the US hospital bed market - we think Baxter is the ideal partner for ONE to achieve this goal.

Baxter can introduce ONE’s products to major US hospital networks that already have Baxter’s products.

The Baxter value added reseller agreement has started and the market launch is expected in Q3 CY2023, and we are hoping to see sales traction from this agreement in Q1 CY2024.

May 2024 Update:

ONE has seen 98% growth in its sales pipeline as a result of the Baxter partnership - with the first purchase order already in at a prestigious children’s hospital in Florida. (Source)

Baxter’s ~100 person sales team is now trained on ONE’s product and a deal could materialise shortly from the value added reseller agreement between the two companies. (Source)

Objective #3: More progress on BYOD solution

With sales and marketing activities already commenced for the BYOD solution, we expect the product to become available in Q1 CY2024.

This includes the launch of the product through a pilot program in the US with an existing US hospital customer - NYU Langone.

If the pilot program is agreed and is successful, we’d want to see ONE expand the program to eventually capture a large potential market in the US and other key markets.

May 2024 Update:

The MyStay (BYOD) product launched on 26 February this year, after a successful pilot program with NYU Langone Health’s Long Island Community Hospital. (Source)

Product improvements are being rolled out continuously, and we expect the Baxter partnership to increasingly leverage the MyStay (BYOD) solution that ONE provides. (Source)

What could go wrong?

Sales risk

Despite a strong customer retention rate and the endorsement of the product by prestigious hospitals, ONE could lose key clients or not seal as many deals, hurting their revenue and share price.

Large institutions like hospitals don’t tend to adopt new technology very often and the sales cycle can be long. This feature of ONE’s customer base can cause delays in sales that drag out over a long time,

Marco factors in the market including a recession can cause a reduction in spending on new technology, affecting ONE’s ability to make sales.

May 2024 update:

ONE’s sales pipeline is 98% bigger after the Baxter deal, ONE has 8 months to go to hit 25,000 beds (currently at 17,808). Hospital’s can be slow to make decisions, so this risk still exists that it will take longer to hit 25,000, not a big deal if it’s a few months late. (Source)

Distribution partner risk

A key part of ONE’s strategy is to sell its products through a distribution partner like Baxter, Microsoft or Samsung.

Although ONE has a strong relationship with these companies, if they move slowly - or don’t prioritise ONE’s products when making a sale - then it could reduce the sales outcomes for ONE.

May 2024 update:

The Baxter partnership appears to be progressing quickly, and it has already produced a purchase order, and the sales pipeline increased by 98% - so far this is already looking better than Microsoft and Samsung partnerships that have been already in place for a couple of years.

Funding risk

Although ONE raised $20M in July 2023, growth companies need cash to achieve their goals. If ONE doesn’t use the money from this raise wisely, then share price pain could follow. This was ONE’s fourth capital raise since it listed in 2016.

May 2024 update:

ONE ended the March quarter with ~€9.1M (~A$14.8M) cash in the bank. (Source)

It’s a solid amount, but ONE will need to continue to sign large contracts to push towards operating cash flow positive status - and set itself up to be a self-sustaining business.

Technology risk

ONE will need to add functionality to its products over time as the health tech industry advances. The BYOD rollout may not go as planned.

Also, ONE has flagged that a range of additional features are in the pipeline, and the successful roll out of these features could help it reduce this particular risk as hospitals become more advanced.

May 2024 update:

MyStay/BYOD was successfully launched in Feb 2024, we’d be looking for early feedback from customers like NYU Langone.

Market risk

Tech stocks could fall in value again. Even if ONE does everything right from an operational standpoint, the market could always sell off or favour different sectors.

May 2024 update:

Tech stocks are running in the US, especially big tech stocks, this could change but the market risk doesn’t seem to have materialised.

What is our Investment Plan?

We plan to hold a position in ONE for the next 3-5 years (and beyond) as it progresses its plan to gain significant market penetration in the lucrative US healthcare market, and (as always) may look to take some profit by selling up to ~20% of our holding if the company successfully delivers on the key objectives listed above and the share price hopefully re-rates again.

May 2024 update:

ONE continues to be our largest holding and we will continue to manage our position in line with our Investment Plan.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.