An Overview of the Different Types of Capital Raising

Published 10-MAY-2025 15:56 P.M.

|

13 minute read

- Commentary: What is an “inflection point” raise? Why we like them. More gold M&A this week - will cashed up gold investors now move to smaller gold stocks? Big US money is coming to critical metals.

Raising money is a big part of capital markets.

(That’s why it’s called the “capital” markets)

Especially in “pre-revenue” companies like the ones we Invest in.

A well-timed capital raise can set up a company for the next phase of development, whether it is a drilling event, clinical trial or new market expansion.

There are a few types of capital raises that we tend to see in the small end of the market:

- Pre-activity raise - The company needs money to undertake some specific activity (drilling, clinical trial or technology development), so they will tap the market for funding to do it.

- Post-results raise - If the outcome is good, the company may quickly raise money to strengthen its balance sheet at a higher share price, to secure the funds to achieve the next derisking or “proving a market” activity.

- “Kick the can down the road” raise - This tends to be a small raise from major shareholders when the company is running out of money and is taking longer to deliver “the thing”... the market has lost some belief, and the share price usually doesn’t necessarily reflect the potential of the assets. This cap raise usually isn’t enough to get “the thing” done, but allows the company to make more progress and win back some market belief before the next raise.

- The Crunch Raise - The company is in a bit of strife due to slow progress or failures. To attract new money, the terms of the capital raise basically need to give new incoming money a huge ownership in the company. This is generally seen as the “reset round” where new shareholders are brought in to breathe life back into the company. Existing shareholders should usually get a chance to participate via a rights issue.

- The Inflection Point Raise - Goals have been achieved, share price is up, the market believes the company is onto something and a large capital raise provides the company with multiple years of runway to expand and grow - to deliver at an “inflection point” where the company moves to the next level.

The Inflection Point Raise is what small cap companies aspire to.

It’s when the company has finally made enough progress and gained enough traction to be onto something “real”.

Raising a large amount of capital gives the management team the proper runway to accelerate their growth.

It is a big milestone.

This week our Investment EchoIQ (ASX:EIQ) secured an important “inflection point” raise.

$17.3M raised at 30 cents, with no options issued.

We participated.

EIQ has an AI-powered algorithm that helps cardiologists detect heart diseases.

The technology has clearance from the FDA and it is being used in hospitals right now in the US.

The product is proven, approved and currently in use in a few hospitals.

The next step - get EIQ’s tech into hundreds of hospitals and turn those partnerships into revenues.

And EIQ evolves from a “med tech development” story to a “velocity of revenue growth” story.

This is what most of the new money raised this week will be used for.

On the morning of the EIQ trading halt, we jumped on a video presentation with EIQ’s CEO Dustin Haines hosted by the lead broker of the raise.

We watch a LOT of different CEO presentations every week.

Dustin’s presentation and concise summary of the EIQ opportunity was genuinely one of the best we have seen in years.

We tried to get a copy or link to the video of this presentation to share today, but unfortunately, it hasn’t come through yet (we’ll keep trying).

EIQ’s CEO Dustin is a great presenter, and the main thing he explained really well was how this particular capital raise will fund EIQ for its next inflection point.

Post capital raise EIQ should have $20M+ which is enough of a cash runway for EIQ to deliver:

- Commercialisation of its AI-based Aortic Stenosis detection technology (get it into many more hospitals)

- FDA clearance for its next product - AI-based Heart Failure detection technology

That means EIQ can now use its giant cash balance to work on integrations into as many hospitals as it can (for its Aortic Stenosis tech)...

AND then once (if) the FDA clearance for the Heart Failure tech comes in (expected later this year), EIQ can flick a switch and distribute that tech to all of the in-place integration partners at the time.

So in 6-9 months time, if everything goes to plan, EIQ will have technology applicable for two heart conditions FDA cleared, integrated into clinics and (hopefully) rapidly growing revenues...

And with this $17.3M raise just completed, it has the capital to deliver these objectives.

Another good illustration of the different types of capital raises is our 2021 Biotech Pick of the Year Dimerix (ASX:DXB).

Last week DXB signed a ~A$1BN licensing deal to sell its Phase 3 rare kidney disease treatment to US patients.

(A big milestone for the company, and we wrote about that deal in detail here: What does it take for a stock to 10-bag?)

Throughout our Investment, DXB had three different raises:

- First, DXB raised $20M at 20 cents to fund the first part of its Phase 3 clinical trial - the “pre-activity raise”.

- Then, when it was clear to the market that DXB would run out of funds to complete the trial, it conducted a “kick the can down the road” raise of $12M at 8 cents.

- Finally, once the interim results came through positive, DXB raised another $20M at 30 cents in an “Inflection Point Raise” to complete the Phase 3 trial.

DXB closed the week at 66 cents, which means that at each point of the journey shareholders could have made money - even though the path is not always linear.

(This doesn't happen all the time, it takes very good execution from management and a bit of luck - but DXB is a good example of when things go right - hats off to DXB CEO/MD Nina Webster on a great result)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Other companies in our Portfolio that recently secured “Inflection Point raises” include:

- AL3 - Raised A$30M to fund operations in the US and scale up sales of metal 3D printing systems to customers like the US Navy.

- ONE - Raised A$20M in November last year to grow US sales of its technology to hospitals to improve the patient and nursing experience.

We hope that a few more of our Investments can secure these larger raises that give management the opportunity to deliver, and grow the value of the company.

In another recent example of a bigger raise for one of our Portfolio stocks was gold producer KAU.

KAU just obtained shareholder approval to acquire a profitable gold mine in Tasmania and raised $30M to complete the transaction.

Post-transaction and capital raise, KAU will be capped at ~$83M and have ~$27M in cash (which includes a $10M loan facility).

With plenty of cash available, its A1 mine in Victoria about to ramp up gold production and an additional 25,000 ounces per year production from its newly acquired mine, we think this could be the “Inflection Point” raise for KAU - (read our full commentary here)

Especially with the gold price delivering some solid gains this week and pushing back towards its all time highs again...

Yellow Metal, Red Hot: Gold M&A is just heating up

This week was another strong week for the gold price.

It went up 5% in one day and is now back into the US$3,300s per ounce.

So when are small gold stocks like the ones we are Invested in going to go up?

Well the money to push their share prices up needs to come from somewhere...

Here’s where we think it will likely come from:

This week we saw yet another mega merger/acquisition in the gold sector.

South African Gold Fields announced a $3.7BN all cash deal for ASX listed Gold Road.

Gold M&A is something we have been talking about for a while now.

Our thesis has always been that the more M&A we see at the big end of town, the more likely the capital from those deals starts to flow down into the smaller end of the market.

If you were an investor in a small gold producer, and just made millions of dollars when your shares were acquired for cash by a gold major, we suspect you’d probably be looking down the food chain to invest in the NEXT up and coming gold acquisition target.

This is where the money will come from:

- High gold prices deliver big gold producers excess cash.

- Big gold producers use this cash to buy smaller gold producers and development stage projects.

- Those shareholders of the acquired companies who receive the acquisition cash look to deploy it into the next batch of up and coming, smaller gold companies (via placements and on market buying)

In a webinar we watched this week hosted by Simon Catt (Catt Calls), legendary investor Eric Sprott said:

“With the gold price so high, major gold producers will net around $160B in pre-tax profits this financial year... that amount will need to be invested somewhere.”

(We’ll share the recording when it becomes available)

We think that M&A is the exact “somewhere” that major gold companies are looking to invest.

First, the mid-caps...

Then, eventually, it flows into the smaller developers.

And then the explorers.

Just inside the last ~3 months on the ASX we have seen:

- Red 5 and Silver Lake Resources merged to become Vault Minerals which is now trading at a market cap of ~$3.3BN.

- Ramelius Resources and Spartan Resources are currently going through a merger process. The combined company will be worth >$4BN.

- Northern Star just completed the $6BN takeover of De Grey Mining.

- And then this week Gold Fields made a $3.7BN all cash scheme of arrangement for Gold Road...

That's ~$17BN in deals settled or about to happen from companies that are all inside the top 15 biggest gold stocks listed on the ASX...

Our view is that the investors who made money on those deals will eventually take some portion of that cash liquidity received from those deals and start looking for the next big gold story.

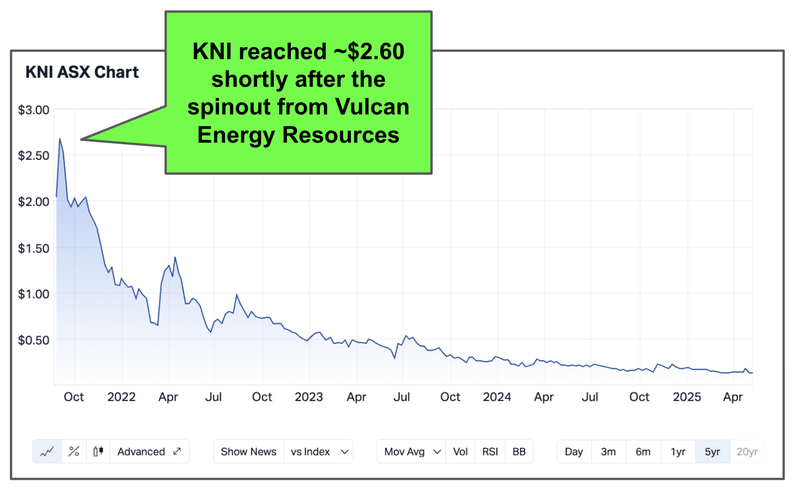

Like when winners from Vulcan Energy Resources piled into KNI...

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

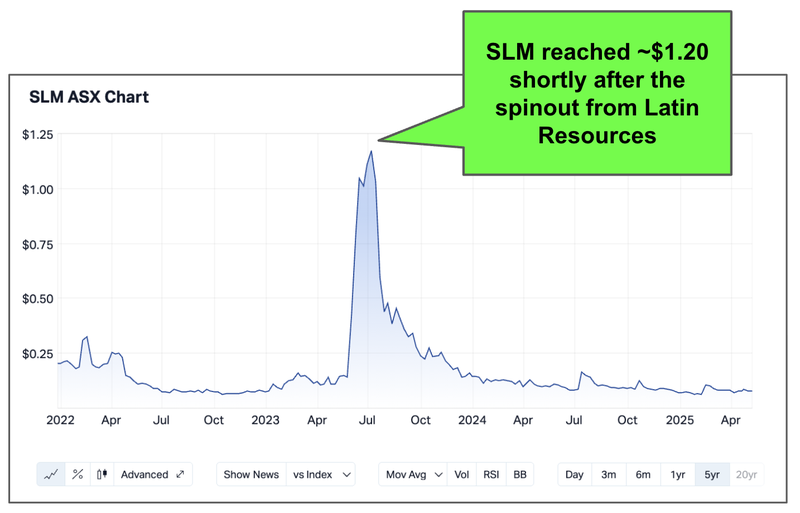

Or winners from Latin Resources piled into SLM.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

It’s easy to forget, but most of the multi-billion dollar gold names we listed above that are being taken over started out as tiny micro caps...

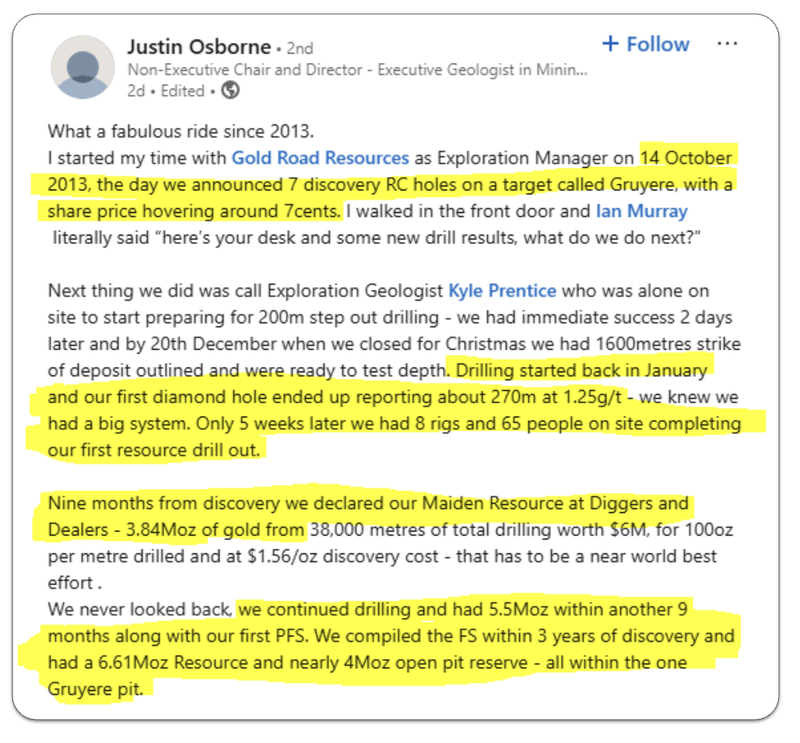

For example, back in 2013, Gold Road’s share price was ~4c per share - a far cry from where it trades today at ~$3.30 per share.

This LinkedIn post from one of Gold Road’s ex-directors was a really good read on how things can come together for a company post-discovery very quickly:

(Source)

In that post he highlighted that the company spent just $6M dollars to define 3.84 Million ounces of gold.

Now that’s efficiency.

De Grey has a similar story.

It was once capped at sub $10M scratching around for a discovery in the Pilbara... then the discovery hole in 2019 and only 6 years later it’s being taken over in a deal worth $6BN.

Even Northern Star (the acquirer of De Grey) was once a tiny micro cap with a market cap <$20M only ~10-15 years ago.

The investors who backed these companies at the right time, ahead of major valuation re-rates, will be sitting on a mix of large chunks of cash and scrip in major gold miners...

These investors will likely be ready to re-deploy some portions of that cash into the next small-mid cap stocks they think can repeat their previous success.

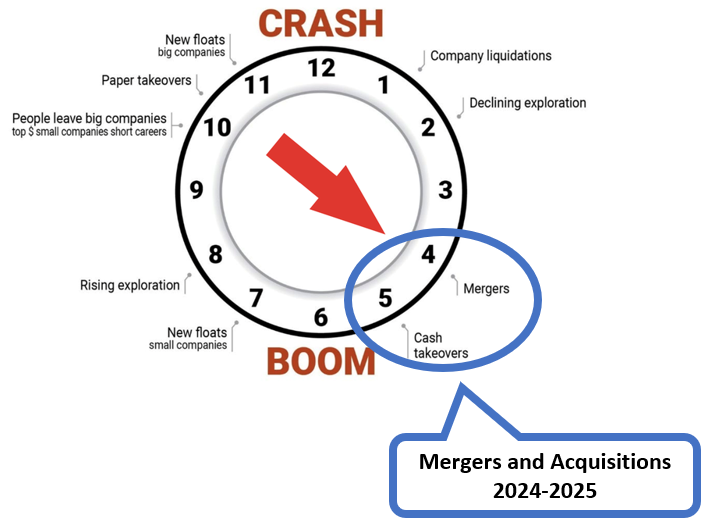

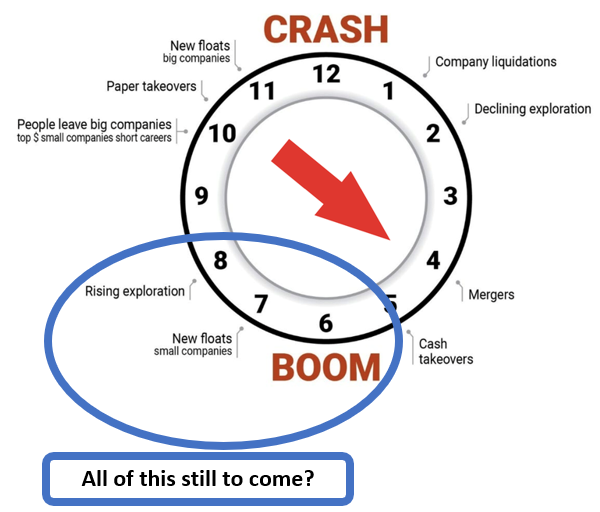

ASX listed, Lion Selection Group’s market “clock” visualises it nicely - first comes the mergers and acquisitions:

Then comes the good times when all that cash starts sloshing around in the rest of the market:

We are seeing a few gold assets being vended into ex-battery metals companies (easier, cheaper and quicker than an IPO)

But keep your eye out for that first gold exploration IPO...

That should be the starting gun for action in the small gold companies.

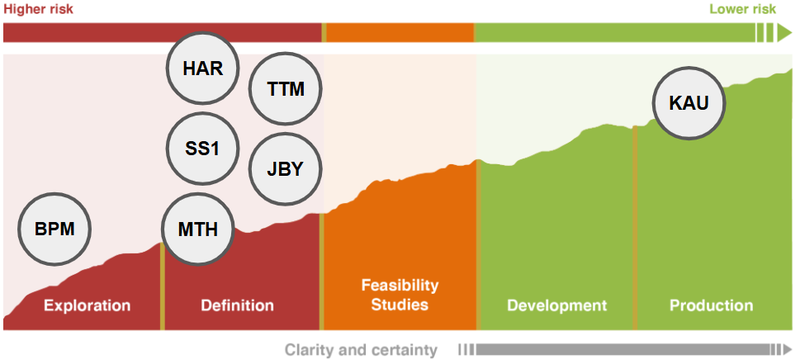

Our take is that there is still a dislocation in company valuations and the gold price around the $20-100M market cap.

Here are the precious metals stocks we are holding in that end of the market:

- Sun Silver (ASX:SS1) - Silver in Nevada, USA (resource definition stage) - read our latest note on SS1

- Mithril Silver and Gold (ASX:MTH) - Silver/gold in Mexico (resource definition stage) - read our latest note on MTH

- Kaiser Reef (ASX:KAU) - Gold in Victoria/Tasmania (production stage) - read our latest note on KAU

- James Bay Minerals (ASX: JBY) - Gold in Nevada, USA (resource definition stage) - read our latest note on JBY

- Titan Minerals (ASX:TTM) - gold in Ecuador (resource definition stage) - read our latest note on TTM

- Haranga Resources (ASX:HAR) - gold in California, USA (resource definition stage) - read our latest note on HAR

- BPM Minerals (ASX:BPM) - Gold in WA (exploration stage) - read our latest Quick Take on BPM

So that's where the money will come from to make small gold stocks go up.

But what about other small stocks?

We recently shared our theory that the money to push up small ASX listed critical metals stocks will come from the giant capital pools in the USA, who are suddenly all about critical metals supply...

US capital making moves on critical minerals projects

The biggest news in the critical metals arena this week was Kobold Metals agreeing to a takeover of the Manono lithium project in the DRC.

(Remember lithium “supernova” AVZ? Manono was their project)

Kobold is a private US company backed by Bill Gates and Jeff Bezos and just recently closed a US$557M series C capital raise...

(Source)

So US tech billionaires are backing a private company to invest over US$1BN into bringing a giant lithium project online...

Manono is one of the biggest, highest grade lithium projects in the world...

We have been talking about how we think the biggest capital market in the world (the US) would soon start cycling capital out of tech stocks and back into real assets (like metals and mining)...

Check out that weekender here: Market Adjusts to Trump's Tariff

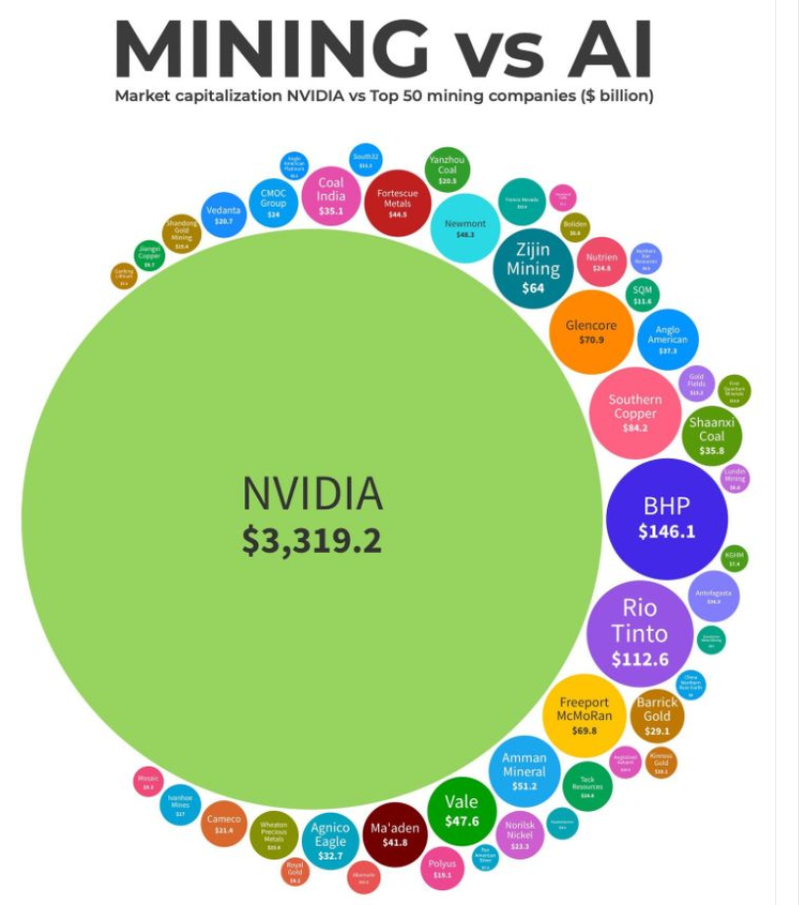

A big part of our thesis was that the massive capital pool in the US (even just a slice of it from the tech industry) could be material for the (relatively) tiny mining/metals industry.

To get an idea of the difference in size here is just one major US tech company, Nvidia vs the mining industry image (in terms of market cap):

(Source, Mining.com October 28, 2024)

The Kobold deal is one of the first mega deals where we are seeing this happen (cash made in big tech moving into metals and mining).

We think the Kobold/AVZ deal could be looked back on in 3-5 years time as the deal that marked the bottom for the lithium/battery metals sector.

Our view is that we are currently experiencing that final capitulation “puke” across the industry.

Companies that held on and tried to stay alive are all starting to throw in the towel, likely because they just can’t tap investors for any more cash...

We think there will be opportunities to pick up advanced projects that have had tens/hundreds of millions in investment for cents on the dollar...

If you have any companies you want us to take a look at, reply to this email with the ticker code and our team will take a look this week.

Are you a s708 sophisticated investor?

If you qualify as a sophisticated investor and would like to see “s708 only” sophisticated investor opportunities: Subscribe to Next Cap Raise.

You will need to send us a valid certificate from a qualified accountant confirming you qualify as a sophisticated investor.

Have a great weekend,

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.