TTM now targeting a 5 million ounce gold resource? Plus first results from copper JV with Gina Rinehart…

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 1,492,723 TTM shares at the time of publishing this article. The Company has been engaged by TTM to share our commentary on the progress of our Investment in TTM over time.

Titan Minerals (ASX:TTM) is now targeting a +5 million ounce gold resource.

(According to the front page of a presentation released this morning)

TTM also has a large copper porphyry project where a subsidiary of Gina Rinehart’s Hancock Prospecting is spending US$120M to earn-in 80% of the project.

This morning, TTM announced the first drill assays back from Gina Rinehart's team.

Over 735m of mineralisation at copper equivalent grades of 0.23%.

This is a very big intercept by any copper porphyry standards.

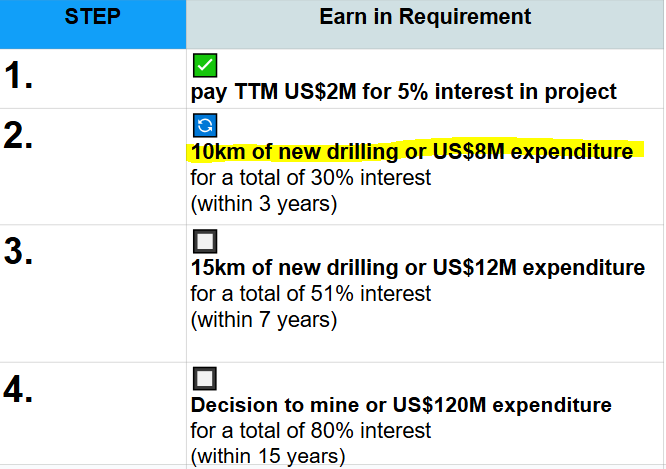

Gina’s subsidiary Hanrine is currently in the second stage of the earn-in JV with and it appears to have plans to go straight into stage 3 of the earn-in JV in Q3-2025 with 15,000m more drilling.

Our Investment TTM is free carried for 20% on this giant copper project until Hanrine declares a “decision to mine” OR spends the full US$120M on the project - whichever comes first.

“Free carried” basically means TTM gets US$120M invested to progress the project in return for 80%, but they keep 20% of it without having to spend anything.

(Read today's TTM copper results announcement here)

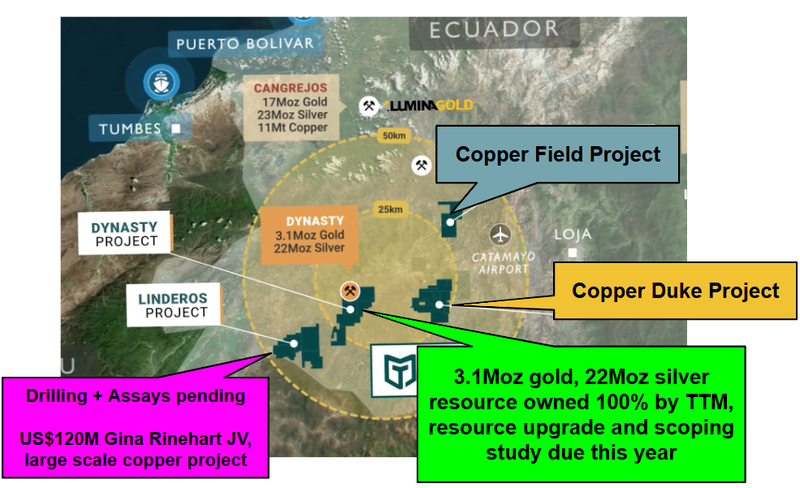

While Gina’s Hanrine funds all of that work on the copper project, TTM can spend its own time and cash adding to its already very big gold-silver project called Dynasty in the south of Ecuador.

At Dynasty, TTM has a 3.1M oz gold and 22M oz silver JORC resource.

TTM has been drilling that project since November 2024 and is expecting to upgrade its JORC resource by mid-year.

(Hopefully closer to that 5M ounce+ target TTM revealed in today’s presentation)

Right now, TTM is capped at $100M and we think the market is mispricing TTM’s assets.

Especially with the look through valuation of TTM’s 20% free carried interest in the copper JV with Hanrine being ~US$30M (A$47M).

At the moment the market is valuing TTM’s 3.1m gold ounces at ~US$22 enterprise value per ounce and the ~22m ounces of silver at $0 per ounce...

The market is placing no value on TTM’s JV with Hanrine (Gina) and no value on TTM’s two other assets - where we think a Hanrine style JV deal could be replicated.

Part of the reason we think there may be a disconnect between TTM’s valuation and commodity prices is down to a lack of market awareness about Ecuador’s growing prominence as a mining jurisdiction.

But we think very recent Mergers and Acquisitions (M&A) activity in TTM’s neighborhood will change that...

M&A in Ecuador shows where valuations are heading...

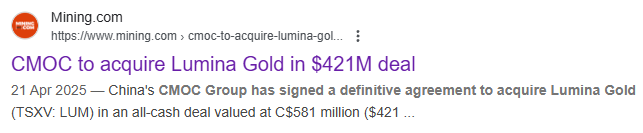

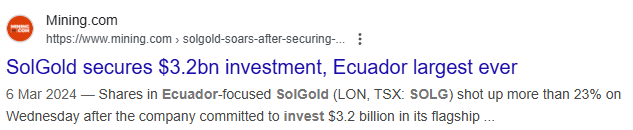

Two weeks ago Ecuador gold-copper player - Lumina Gold - was taken out by CMOC for US$420M (A$655M).

(Source)

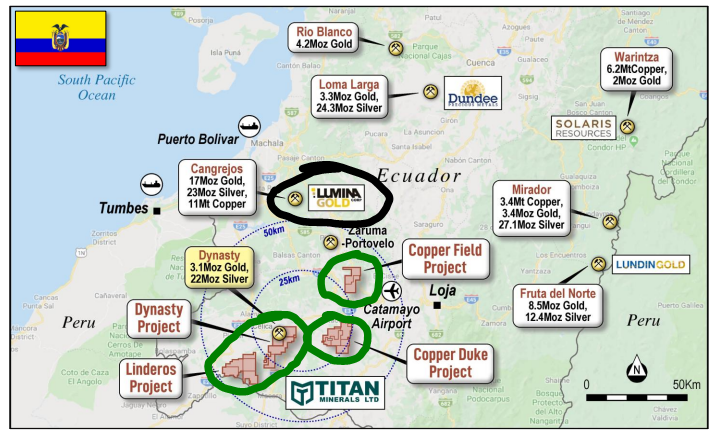

Lumina is a single asset company with a giant copper-gold porphyry project.

(one of the top 30 biggest in the world).

It is the type of project that Gina Rinehart would likely have been looking for when her subsidiary group Hanrine signed that US$120M Joint Venture deal with TTM.

(and who knows, maybe with some more drilling it could become that big).

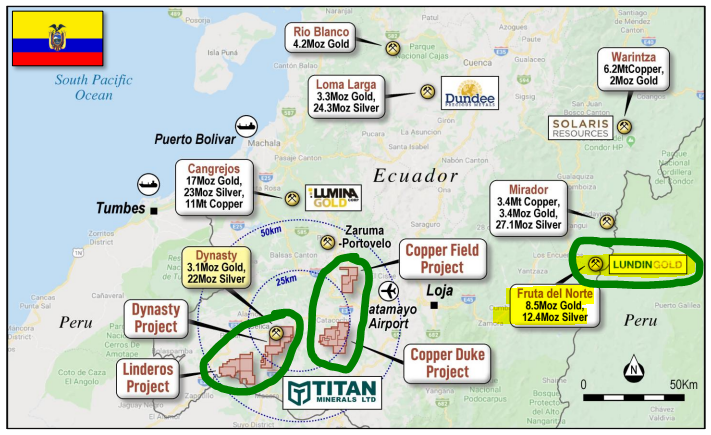

Here is where that Lumina asset sits relative to TTM’s portfolio of projects:

The biggest takeaway for us from that Lumina deal is that M&A is becoming real in Ecuador.

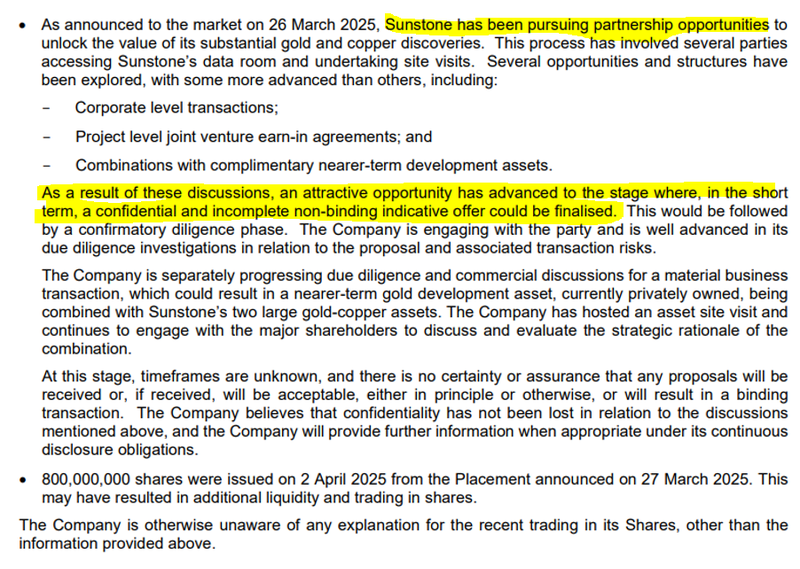

We also noticed recently that TTM’s neighbour Sunstone Metals said that corporate interest was a potential reason for an unexplained price run...

Sunstone’s share price is up almost 300% in the last month or so - and the ASX gave them a “please explain why your price is going up on no news?” request.

Reason given for the share price run:

(Source: Sun Stone Response to ASX price query 3rd April 2025)

Sunstone’s latest updates keep talking about how close they are to a finalised deal...

Is there a chance these same groups are running the ruler over TTM?

So far Gina has come in for one of TTM’s projects with that US$120M earn-in JV.

But we think there is still a lot of value in TTM’s remaining three assets.

Especially in TTM’s Dynasty project which is 100% owned.

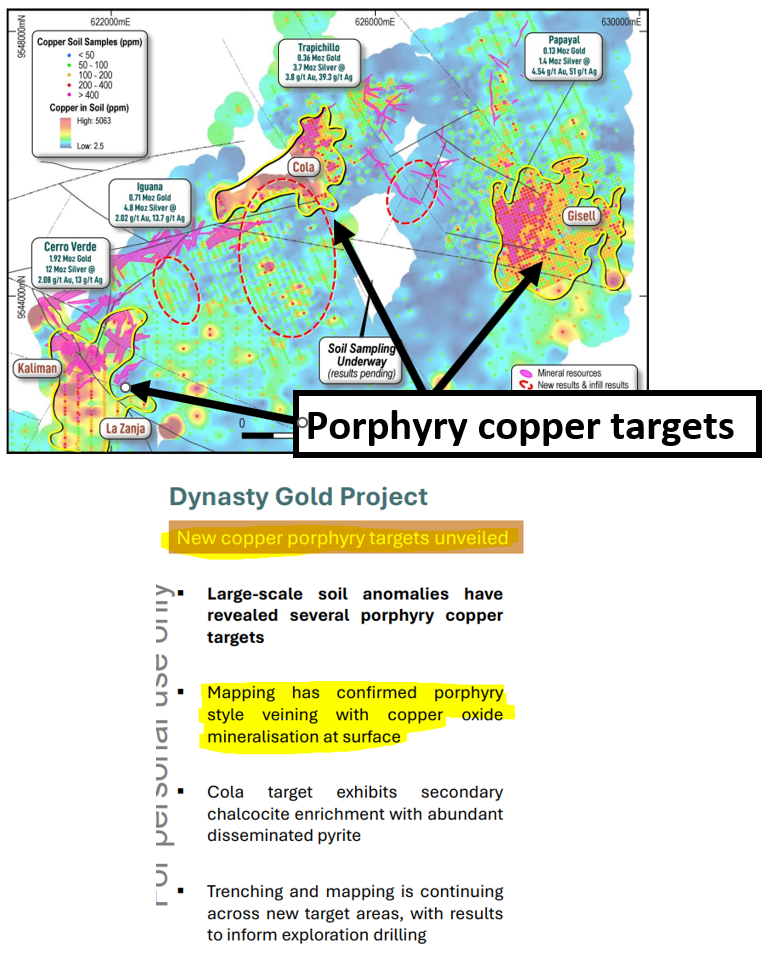

In the new presentation TTM released today, they even teased out the copper porphyry potential at Dynasty which is exactly what a potential strategic partner wants to see when coming into M&A deals.

The “free, untapped” exploration upside that they can go in and drill out.

So far, TTM hasn’t drilled any of the porphyry copper potential at Dynasty...

(It certainly appears that TTM are talking about porphyry copper more in today’s updated preso).

(Source)

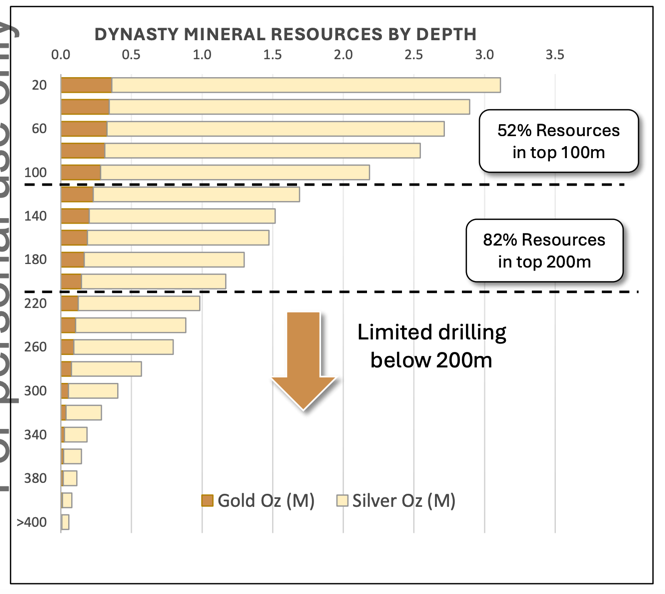

AND let's not forget that most of TTM’s drilling to date has been down to a maximum depth of just ~200m...

(Source)

All of this is pure speculation, but based on the above, could TTM be swept up in this new interest in the region with a takeover offer, JV or substantial cash injection given the gold price is trading near all time highs?

Obviously, this is not the main reason we are Invested in TTM.

Waiting around for M&A deals to happen can sometimes weigh down a company's share price, and months spent trying to finalise deal terms can mean millions of dollars spent on paperwork rather than progressing any of a company's projects.

Generally to attract M&A, it’s better for a company to press on towards development, rather than put up a “for sale” sign and wait around for a buyer.

First and foremost we are Invested in TTM to see the company drill out and grow its project’s resources.

The bigger they get the harder TTM will be to ignore...

Ecuador copper & gold in favour amongst the major miners...

One of the highest grade gold mines in the world is operating in Ecuador right now.

The project is owned by ~A$16BN capped Lundin Gold - it's actually their cornerstone asset.

Lundin was built off the back of Fruta Del Norte’s success - back in 2016 when the project was in the feasibility study stage Lundin’s share price was less than CAD$5 per share.

Since then, Lundin has raised billions of dollars, built its project and is producing almost half a million ounces of gold per annum.

Now Lundin Gold’s share price is ~CAD$60.55 per share and it has a market cap of ~A$16BN.

(in the last ~12 months Lundin’s share price has almost tripled - which is good for juniors in Ecuador because it means Lundin will have more firepower with a bigger market cap)

Here is where Lundin's Fruta Del Norte sits relative to TTM’s assets:

More recently, Ecuador has also started attracting interest from major miners for copper.

Last year SolGold signed a US$3.2BN deal with the Ecuador government for its Cascabel copper-gold project.

That SolGold deal was the biggest ever mining investment commitment in Ecuador’s history AND it was completely separate to the ~US$311M SolGold had committed to previously.

(Source)

That move triggered rumours of BHP corporate interest in SolGold.

(BHP is already a shareholder of SolGold and its pretty well known they are on the lookout for more copper exposure)

(Source)

Gina Rinehart, who controls one of the world’s biggest private mining groups (& TTM’s joint venture partner at Linderos) is also pushing itself into Ecuador.

Before the deal with TTM, Gina invested US$120 million for a 49% stake in six different projects, partnering with Ecuador’s national mining company, ENAMI (51%).

Now the latest deal is by CMOC to acquire Lunima gold for ~A$655M.

CMOC is one of the big Chinese mining conglomerates...

Lumina’s project is in the same part of Ecuador as TTM’s projects.

Overall, we think the moves by the bigger miners into Ecuador can only be good for the country.

Once they go in and work with the government to develop the industry, it makes juniors like TTM more attractive for the mid-tier miners AND for the majors looking to increase in-country presence.

It also makes it easier for juniors like TTM to finance their assets now that more deep pocketed players are watching what they are doing.

What’s next for TTM?

More drilling at Dynasty gold project 🔄

TTM has ~2,000m left to drill at its Dynasty gold project after rain delays in the field in Ecuador.

We expect the company to complete this drilling over the coming months and set itself up for a resource upgrade.

Resource upgrade/update at Dynasty 🔲

By mid-year we expect TTM to publish a resource upgrade over its Dynasty Project.

Today’s presentation said 5M ounces+ is the target, so hopefully this year's upgrade gets us closer to that target.

(Source)

More drilling at the Linderos Copper project (Gina JV) 🔄

Today’s announcement mentioned that more drilling was “currently underway” on this project as part of stage 2 of the earn-in agreement with Gina.

We are looking forward to seeing some more results over the coming months as the JV is expected to move into stage 3 in Q3-2025.

Here is our mockup of where TTM and Hanrine are with the Linderos JV:

What could go wrong?

With the balance sheet healthy in the medium term, the key risk for now is “exploration risk”.

If TTM is unable to discover more gold over its Dynasty project and publishes a resource upgrade lower than market expectations, it could have a negative impact on the share price.

Poor drill results from the Gina JV could also be negative for TTM’s share price, especially if Hanrine chooses not to proceed with the remainder of the JV earn-in stages.

Exploration / Drilling risk

There is no guarantee that TTM’s extensional drilling programs will be successful and TTM may fail to uncover enough economic mineralisation to justify the expense.

Source: 29 May 2024 TTM Investment Memo

Our TTM Investment Memo:

Our Investment Memo provides a short, high-level summary of our reasons for Investing.

We use this memo to track the progress of all our Investments over time.

Click here to read our TTM Investment Memo where you will find:

- What does TTM do?

- The macro theme for TTM

- Our TTM Big Bet

- What we want to see TTM achieve

- Why we are Invested in TTM

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.