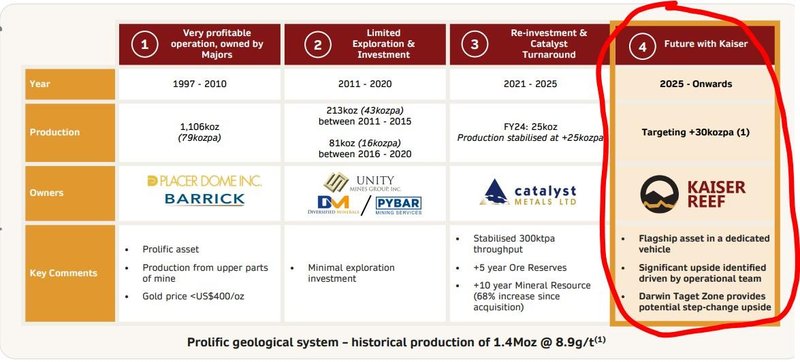

KAU’s new Henty gold mine acquisition produces 6,064 ounces over 3 months. KAU takes ownership in 18 days…?

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 4,981,210 KAU shares and the Company’s staff own 71,000 KAU shares at the time of publishing this article. The Company has been engaged by KAU to share our commentary on the progress of our Investment in KAU over time. Additional placement shares will be included in disclosure post transaction approval vote at upcoming EGM.

The gold headlines don’t stop.

The gold price keeps charging higher and higher.

It's certainly a great time to be a gold producer...

FOUR weeks ago KAU announced it is acquiring the profitable Henty gold mine...

KAU is buying this gold mine from $1.4BN gold producer Catalyst Metals.

KAU will 100% own the Henty gold mine (and its revenue) around 10 days after the EGM to vote through the deal on May 7th.

Today Catalyst (still currently the owner of the Henty mine for the next ~18 days) released quarterly production numbers on KAU’s new gold mine:

(Source - Today's Catalyst Metals quarterly)

The Henty mine produced 6,064 ounces at an All In Sustaining Cost (AISC) of A$3,283/ounce.

At today’s gold price of ~A$5,200/ounce, that is a A$1,900+ margin for every ounce produced.

$12M profit from the mine in a 3 month period...

So the mine KAU is acquiring will soon be spitting out $12M+ profit over 3 months for KAU (currently capped at $60M, $110M post transaction at 18.5c).

That is assuming the gold price stays where it is and doesn't keep running... (or fall)

Things are changing very quickly for gold...

Just four weeks ago when the deal was first announced, the gold price was ~A$4,800/ounce.

Since then the gold price has risen by ~A$400.

(yes, seriously 8% up in just 4 weeks)

Today the gold price is at around A$5,200/ounce.

Just that extra A$400 increase in the price of gold alone, based on today’s CYL quarterly, means Henty would have generated an additional ~$2.4M + in revenue during the March quarter at today's gold price.

And the gold price feels like it could do anything in the near term.

If any of the big investment banks are right with their forecasts, then things could get very interesting for KAU:

- Goldman Sachs has a 2025 forecast of US$3,700/oz (AUD$5,750) (Source)

- Macquarie Group has a 2025 forecast of US$3,500/oz by Q3 (AUD$5,450) (Source)

- JPMorgan has a Q2 2026 forecast of US$4000/oz (AUD$6,220) (Source)

We wrote over the weekend about a flight to gold if the USA makes additional efforts to devalue its currency (read our weekend edition here).

8 days from today, (May 7th) we expect KAU shareholders to vote through the deal and shortly after the Henty mine AND its revenue will be owned by KAU.

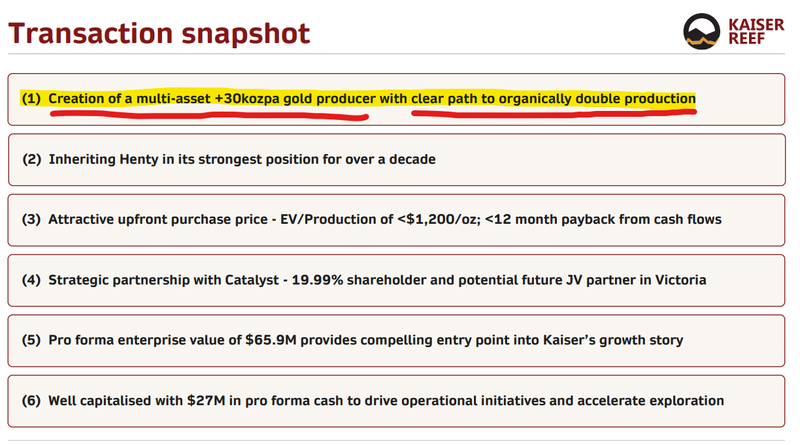

Post acquisition KAU will "become a 30,000 oz producer with pathway to organically double”

KAU already produced ~5,080 oz of gold in the last year from its A1 mine in Victoria.

A1 has historically produced 600,000 ounces, and just reached the Nova (never before mined deepest part of the mine) section of the A1 mine.

If they hit a big gold reef down there it could be massive for KAU’s future production figures.

Here is a video of KAU pouring an 11kg gold bar produced from its A1 mine - watch it here

(Watch KAU’s 11kg gold pour from earlier this month)

A lot of work (and money) has gone into getting to virgin ground on A1, it’s the first time in decades that fresh, never before mined parts of this project are being mined.

The overall bet from KAU is pretty simple:

KAU will have two assets that can work very nicely in a high gold price environment.

Across the two projects, KAU could spit out up to 10,000 ounces of gold each quarter...

At a gold price of A$4,800 that could mean ~$48M a quarter in revenues for KAU (capped at $110M post transaction at 18.5c)...

And if KAU can keep AISC down around $2,600 that could mean ~$22M profit per quarter.

IF the gold price does something silly like spend a couple of years at around A$8,000 per ounce (just speculation by us) then the profit numbers could look really big for KAU.

(keep in mind, the gold price can also fall from its current levels)

Disclaimer* These profit numbers are all speculation on our end, the gold price could fall from here. Production numbers could also be a lot lower than expected OR costs could be higher. A lot will need to go right for KAU to hit the numbers we are saying.

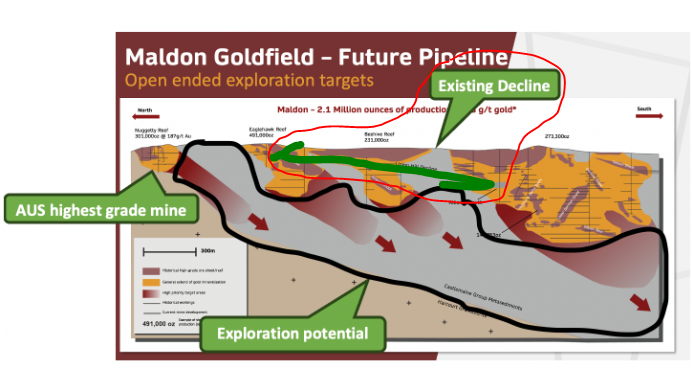

KAU also owns the Maldon mine and processing plant.

The processing plant is where the A1 ore is turned into gold.

Maldon project is where we think there is still a lot of exploration upside.

Australia’s highest grade gold mine was once mined out of KAU’s ground at Maldon.

That mine produced 301,000 ounces of gold at grades of ~187g/t.

It was called the “Nuggety Mine”

A discovery like that is frankly outrageous, we want to see KAU put some of its new cash flows from the Henty mine into exploring for another similar discovery at Maldon.

Being so close to the company’s processing infrastructure at Maldon means any new discovery here has a clear pathway to being turned into gold.

Again, we want to see some of the revenues from the Henty mine and A1 go toward exploration at Maldon.

KAU finding another “Nuggety Mine” would be KAU’s Spartan Resources moment...

Spartan was the company that made a giant, high grade discovery ~50m away from its processing plant and re-rated by 2,000%...

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

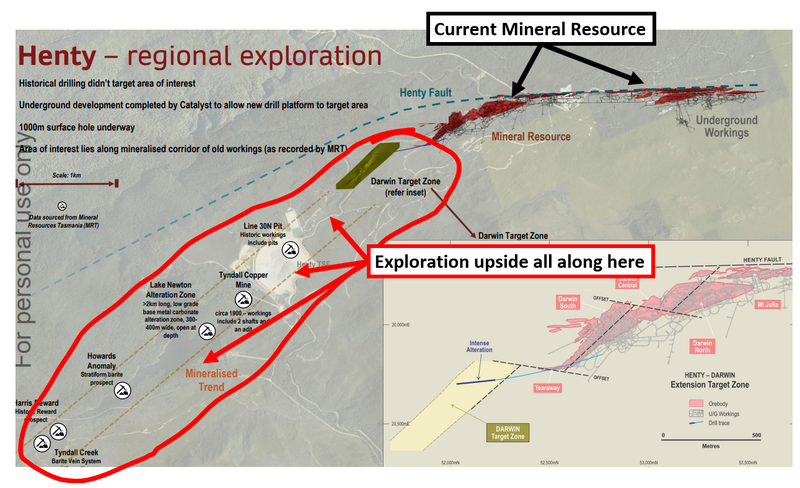

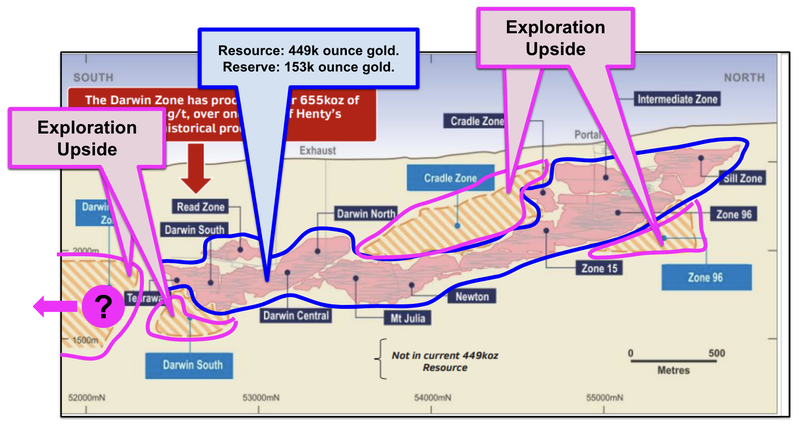

That discovery potential, right next to processing infrastructure, isn't just applicable to Maldon...

KAU’s new acquisition (Henty) also has similar potential.

There is infrastructure with replacement values >$100M ready to process more ore.

Here is a cross-section of the current resource vs all of the exploration upside at Henty:

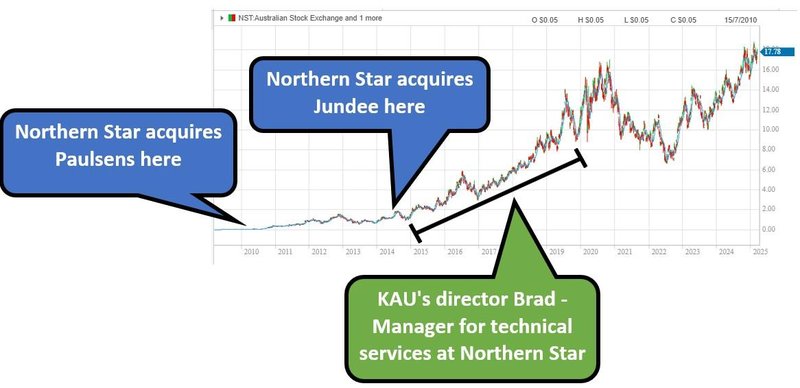

New KAU COO Brad Valiukas has maximised the value of assets like Henty and A1 before...

Brad was at Northern Star as a technical services manager from 2015 to 2019.

During that period Northern Star picked up the Jundee asset off Barrick.

Similar to the acquisition KAU announced today, Jundee was prised out of a bigger company which couldn’t properly realise the value of the asset.

When Northern Star picked it up, it had 2-3 years of mine life left...

To this day (10 years later) that asset still produces over 250k ounces per annum for Northern Star...

During Brad’s time at Northern Star, the company went from $2/share to $9...

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

We are backing Brad to do it all again with KAU.

We also noticed Brad invested $250K in the 14c KAU cap raise, so Brad is backing himself in on this one too...

(other directors put in ~$430k combined)

Here is a video of Brad and KAU’s MD Jonathan Downes explaining the Henty acquisition and how it will turn KAU into 30,000oz per year producer with a clear path to organically double production:

(download the accompanying Henty gold mine acquisition presentation here)

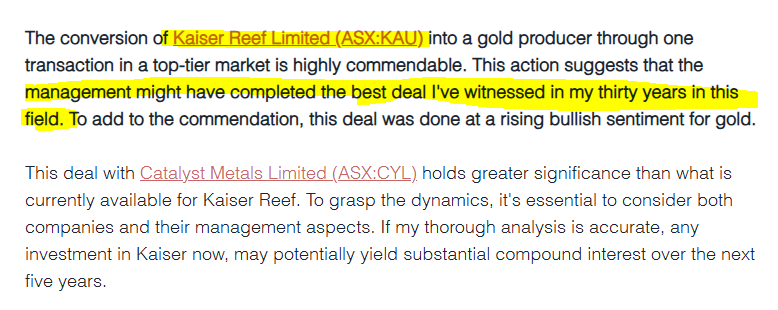

For some more info on Brad and his past work, this KAU write up by Samso that was released 48 hours ago and is a pretty good read if you are a KAU shareholder:

(Read Samso’s full KAU write up here)

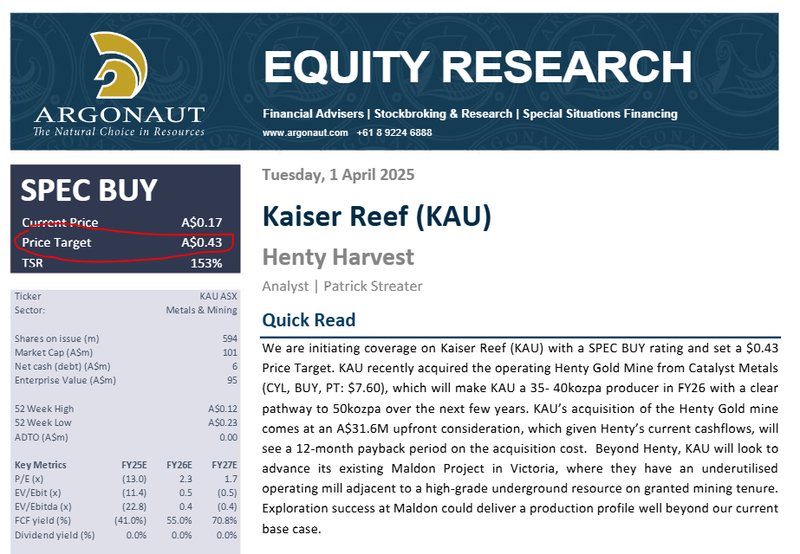

Speaking of bullish predictions on KAU... Argonaut released an analyst report on KAU with a price target of 43c:

(Source)

While that price target does look interesting, we should be clear that analyst price targets are based on a number of assumptions that may be incorrect - they (or us) don't have a crystal ball. It’s definitely possible KAU does not reach these share prices. This is a small cap gold stock. Never invest on a price target alone, and always do your own research.

Transformational acquisitions built the foundations for some of the world’s biggest gold miners:

Big acquisitions in the small cap gold space are pretty common AND there is a long hall of fame of successful gold M&A stories on the ASX.

Some of the biggest gold producers on the ASX were born out of transactions like KAU’s deal today.

(we are hoping that KAU can follow in their footsteps)

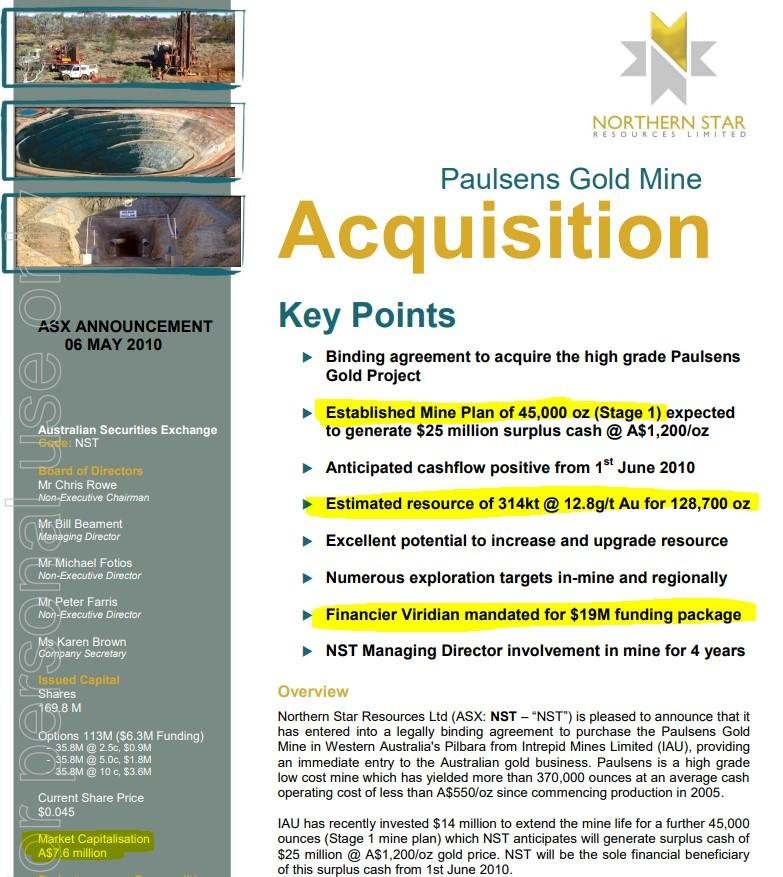

Anyone who has been around markets for 20+ years will remember the Northern Star Paulsens acquisition.

Back then Northern Star was capped at just ~$7.6M, but Northern Star paid up to ~$40M for Paulsens which was a previously producing mine with a modest resource...

Paulsens had been operated as an underground mine and was scheduled to be wound down just before Northern Star came into the project.

The Paulsens deal at the time was a big change in scale/operations by Northern Star.

The market also saw it as way too big for Northern Star to digest.

Similar to KAU’s deal today, the project had a mill, and infrastructure (worth more than Northern Star’s market cap), and Northern Star’s management had their own ideas about how to make money from the project.

Northern Star took that project and went on to become one of the biggest gold miners in the world today (only 15 years after that deal...)

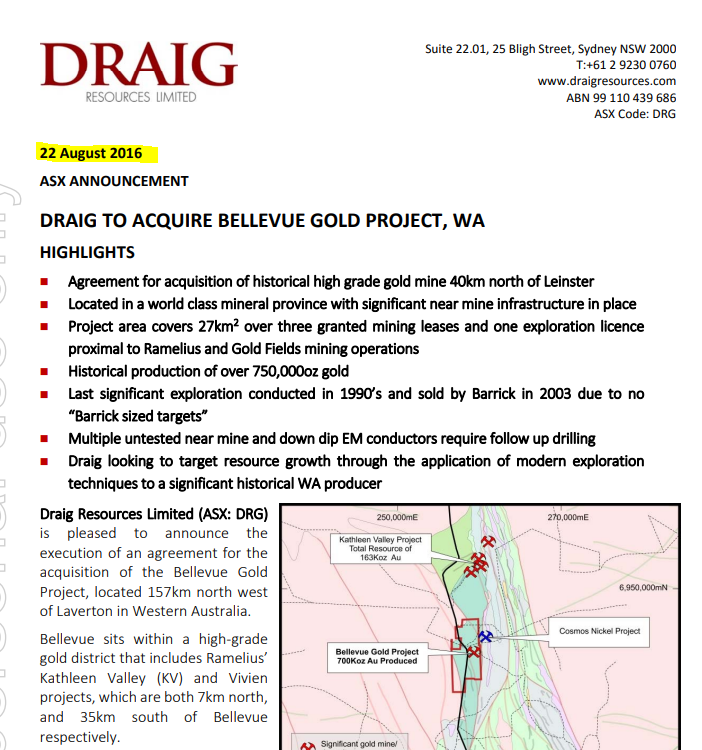

Another more recent example is Bellevue Gold (the old Draig Resources).

(Source)

Draig’s market cap at the time of its acquisition was ~$2M, to get the Bellevue project in, Draig had to pay in excess of its market cap for the asset.

The Bellevue project was again an old mine that had over 700k ounces of historic gold production.

The new team went in, spent the next ~7 years exploring the project aggressively and have now managed to define a >3.2M ounce JORC resource.

At its peak Bellevue’s market cap was >$2BN, today it trades close to $1.3BN.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

The main reason why these big gold deals seem to work in the long run is because they are a faster way for a micro cap to make itself “institution friendly”.

By that we mean, a micro-cap stock can start to pitch itself to deeper-pocketed institutional investors who couldn't invest in the company before because of how small it was.

We have talked about this concept before in one of our weekend emails: Index Inclusion: A Small Cap’s Big Leap

At a very high level all it means is:

- Deep pocketed institutional investors aren't allowed to invest in micro cap stocks because their mandates deem micro caps too “risky” AND because tiny positions aren’t meaningful enough for their investors.

- By growing quickly (through acquisitions), KAU’s market cap can re-rate to a level where these institutions mandates allow them to invest & they can build up big enough positions in the stock.

- The bigger KAU gets the bigger the capital pool gets AND then eventually index buying kicks in and takes control.

The ultimate goal for any junior gold stock is to eventually make it into the GDX or the GDXJ - the two biggest gold miner ETFs (Exchange Traded Funds) in the world.

Between them the two ETFs have over US$20BN invested passively across miners, to make it into the GDX the minimum market cap is US$750M, and to make it into the GDXJ it’s US$150M.

With the current global macro environment, more and more money will flow into gold ETFs and only those companies big enough to benefit from ETF buying will benefit from those capital inflows.

We are hoping KAU’s two producing assets, in a high gold price environment, can re-rate the company’s market cap to a level where it gets included in one of those indexes.

And in the long run in 5 or 10 years' time, we are hoping to look back at KAU’s Henty deal the same way Northern Star and Bellevue shareholders looked at those first few deals....

9 reasons why we like KAU’s new project

These reasons are drawn from our previous note on KAU - (read that note here)

Note: KAU’s acquisition is pending a shareholder vote at an EGM, the below reasons assume that the acquisition proceeds.

- Producing mine with existing resources + reserves base

The Henty gold operation is currently producing ~5,000 to 6,000 ounces of gold per quarter. The project also has 5+ years of mine life in reserves and over 10 years of mine life in resources.

Update: Henty produced 6,064 ounces of gold in the March quarter of 2025.

- The project could generate ~$120M in revenues per annum at today’s gold price

Henty produced 25k ounces in 2024 (KAU is looking to grow this number in 2025). At current gold prices, that would be ~$120M in revenues per annum.

With all in costs averaging ~A$2,500/oz for Henty in 2024, KAU should be able to turn those revenues into free cashflows in the current gold environment.

Update: The gold price is now trading at ~A$5,200 per ounce, 25k ounces of gold would now be ~$130M in revenues.

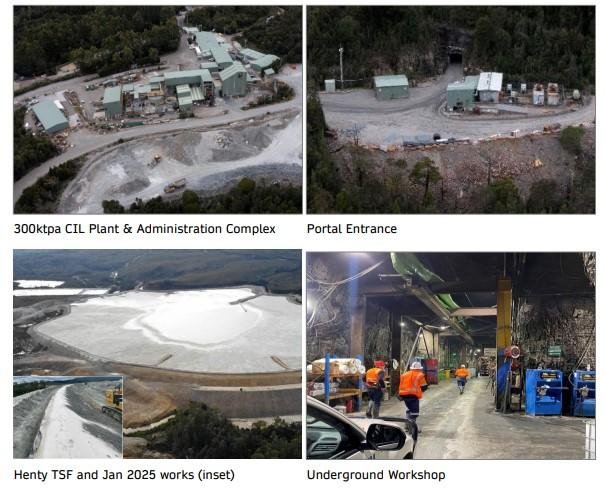

- Henty has $100M+ of existing infrastructure

The Henty Gold Operations has an existing 300ktpa processing plant, a mining fleet/inventory and tailings storage/underground declines with replacement value greater than $100M.

KAU gets to benefit from all the capital that’s gone into the asset to date.

- Exploration potential untapped to date

KAU is taking over the project after previous operators focused on ironing out production efficiencies.

With the cashflow from operations at record gold prices, KAU can drill out the project to extend the project's mine life.

- Acquiring a big gold asset has worked for other ASX companies

Northern Star was capped at $7M when it made its first big acquisition for $40M. 25 years later and several other acquisitions later Northern Star is capped at $20BN.

$1.7BN Bellevue Gold also started with a market cap of ~$2M before making acquisitions to become what it is today. There is a precedent for gold M&A to work in the long run.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

- KAU’s Exec director Brad Valiukas has experience maximising value from assets like these and is now working full time on Henty and A1

Brad was Manager for Technical Services at Northern Star during 2015-2019.

His role was spread across the entire Northern Star portfolio and he helped set up the foundations for assets like Jundee to be the cornerstone of the $20BN producers project portfolio.

Certainly a good guy to have on the KAU team, extracting the most profits from Henty and its Victorian assets.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

- KAU now has two operating mines

KAU will now have adiversified production profile.

Once the A1 mine production lifts to closer to Henty’s production, if one mine has a bad quarter, the other one could fill in the gaps temporarily.

A smoother, more predictable production profile may attract institutional investors who want less volatile gold production exposure.

- KAU market cap can grow to a size where institutional money can come in

The ASX gold space has had a lot of M&A deals get done over the last 12-18 months.

Most of those deals are to grow in size/scale as quickly as possible so that the producers can attract investment from institutional/passive funds.

KAU post-deal will have a market cap of $110M at 18.5c, which is approaching a level where these funds may be able to invest.

- KAU is acquiring a non-core asset from a $1BN company

Vendor of the asset Catalyst looks like it wants to focus all of its time and effort on its WA assets.

KAU can now take Henty and give it the time & capital it needs to be a big part of a company’s portfolio.

What might not be core for a $1BN company, can be a great foundational asset for a <$100M producer like KAU.

What’s next for KAU?

In the short term, we want to see two things:

Acquisition of the Henty Mine in Tasmania finalised

Milestones:

✅ Capital raise

🔄 Shareholder vote to approve the transaction

🔲 Transaction completed

Exploration drilling and increased production at the A1 Mine in Victoria

Milestones:

✅ Drilling commences

🔄 Drilling results

🔄 Decline construction progress

🔄 Mining of virgin ground commence

🔲 Increased average gold grade processed

What are the risks in the short term?

The two key risks for KAU in the short/medium term are “development/delay risk” & “deal completion risk”.

Development delays risk is relevant here because KAU has ongoing costs from operating its processing facility AND on decline development work.

IF decline development is delayed or takes a lot longer than expected it could mean KAU goes longer periods without production revenues.

We think the market could perceive this as a negative and start to price in future capital raises.

Development/delay risk

Should any or all of the above risks materialise, KAU could wind up stuck in

“development purgatory” where newsflow dries up and the project remains stagnant for a prolonged period of time, hurting the share price. Additionally, if delays occur in terms of material newsflow, the market could turn on KAU.

Source: What could go wrong? - KAU Investment Memo 21 October 2024

Deal risk is a new one that sits outside of our Investment Memo.

There is always a risk that the deal does not go ahead for whatever reason. If that were to happen then we would expect the KAU share price to re-rate lower.

We list more risks to our KAU Investment Thesis in our Investment Memohere.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.