Currency Wars, Commodities, and Small Caps

Published 26-APR-2025 15:25 P.M.

|

15 minute read

- Commentary: More market chaos, what is the USA’s end game? A Mar-a-Lago accord? History repeats

- The other usual stuff: in tomorrow’s Sunday Edition

The past few weeks have been all about deciphering what the world is going to look like after Trump’s global shake up.

Tariffs, trade wars, DOGE spending cuts etc...

What will it mean for the stock market?

(and more specifically for small ASX stocks... like the ones we Invest in.)

We have been using a “snow globe shake” as the analogy to best describe what is currently going on.

The “end game” of this global shake up appears to be to devalue the US Dollar, revive US manufacturing and industrial bases, develop local critical minerals supplies and increase US competitiveness in global export markets.

To help get a spiralling US $36 trillion national debt under control...

So why all our recent talk about the US?

Why aren’t we talking about the Australian election?

(hey, we do mention Albo agreeing to set up a $1.2Bn national critical minerals stockpile later in this article)

Well, the current actions of the US will likely have a larger impact on our stock Portfolio, so it's important to stay across these developments as small cap ASX investors.

For the past few weeks we have laid out some theories for the potential ASX small cap winners and losers from when the dust eventually settles.

The USA’s plan to achieve its goals seems to be evolving each new day.

Markets and various asset values are jolting up and down as investors enact their own predictions on potential winners and losers, based on any new information they see.

(often from just tweets or sound bites)

Initially, a few weeks ago, came tailwinds for anything with exposure to specialist, US based manufacturing.

(the US wants to bring important manufacturing back to US, especially from China)

Particularly in the defence industry, where manufacturing and supply issues had become apparent and urgent.

Our Investment AL3 supplies 3D printing machines that can quickly and cheaply print complex metal parts for defence ships, planes and submarines.

AL3 has a US based manufacturing hub and specialises in supplying to the defence sector.

(not sure why the AL3 share price isn’t running yet given how perfectly AL3 fits with the USA’s new major and urgent goals around defence supply chains and ship building...)

Then on April 2nd, broad and sweeping “tariffs for everyone” were announced on “Liberation Day”.

After the tariffs were announced and a few new Executive Orders were signed looking to boost critical minerals production in the US - another set of winners became clear.

Critical minerals projects in the US and again... anything that benefits from a depreciating US dollar...

This week we saw TEN USA based resources projects get “fast track” approval to be developed.

SS1’s similarity to one of the projects, and PFE’s proximity to another was very good news - we’ll explain exactly why later.

THEN the markets were thrown off again, with Trump signalling a backstep and a “willingness to deal” with the world.

He announced a 90 day pause on the sweeping tariffs announced on April 2nd.

A window that the US government would use to accelerate discussions with all of the countries it had threatened to place tariffs on (basically everyone).

(even including China in the list of countries it is willing to deal with)

(Source)

That got us thinking about what the real endgame is for the US and the Trump administration.

Is this 90 day window being used to bring all countries to the table to sign a grand new deal?

We think that Trump is trying to devalue the US Dollar and get the $36 Trillion US national debt under control...

But how will he get it done?

While the last few weeks of uncertainty and chaos seems unprecedented, it’s not the first time the US has decided that the global financial system needs a bit of a tweak and a reboot in its favour.

(it reminds us of Ray Dalio’s famous quote along the lines of just because something hasn’t happened in your lifetime, doesn’t mean that something similar hasn’t happened before... watch his video about anticipating the future by studying history here)

There have already been a few times over the last 100 years where the US has decided the global order needs a bit of a reboot (in the USA’s favour of course).

Usually this reboot is in the form of a multi-country agreement on some new currency and trade terms.

The agreement or “accord” is usually named after the location where the deal is signed:

Bretton Woods System (1944):

This agreement, negotiated after World War II, established the rules for commercial relations among 44 countries, including the United States.

It aimed to create a more stable global monetary system with fixed exchange rates and the establishment of the International Monetary Fund (IMF)

The delegation decided that the world’s currencies would no longer be linked to gold but pegged to the U.S. dollar.

The US dollar would be redeemable for gold.

US cancels Bretton Woods (1971)

The USA had been the world’s reserve currency for nearly 30 years.

USA is printing more and more US dollars... but is running out of gold to back them up.

The US president announces the end of the US dollar's convertibility to gold.

The US dollar remains the world’s reserved currency

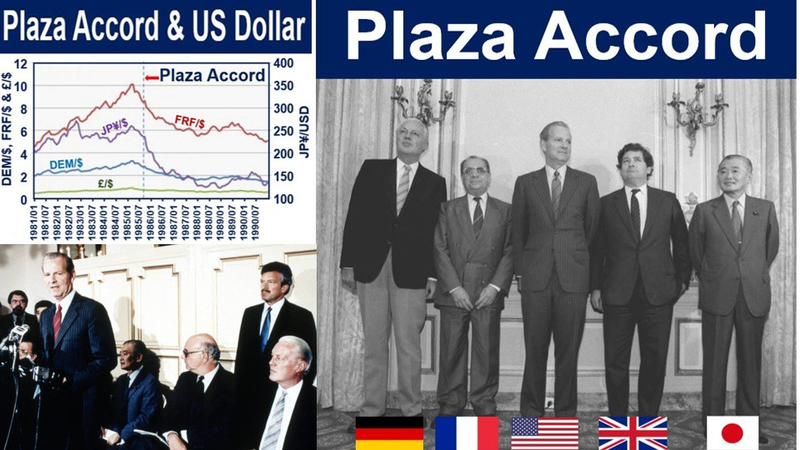

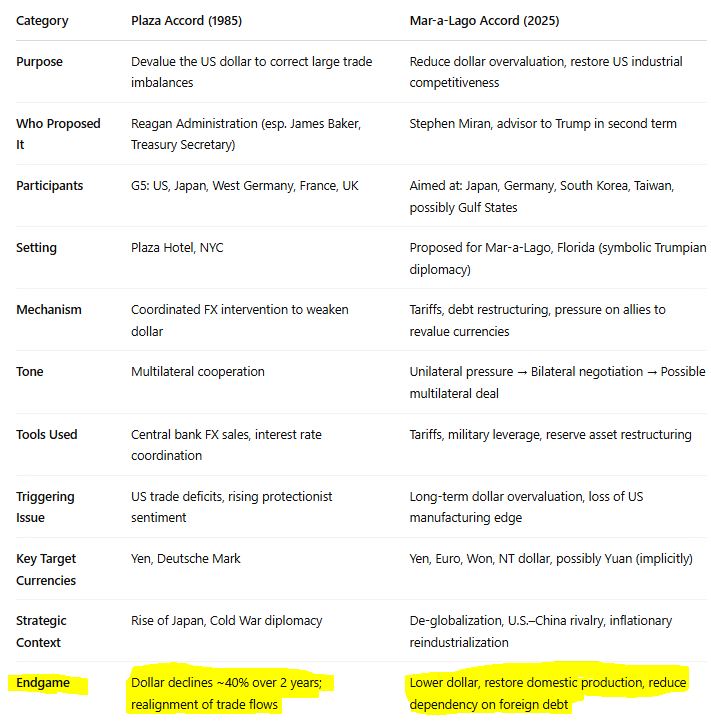

Plaza Accord (1985):

This agreement, signed by France, West Germany, Japan, the United Kingdom, and the United States.

Aimed to depreciate the U.S. dollar against major currencies by intervening in currency markets.

Louvre Accord (1987):

This accord replaced the Plaza Accord and aimed to stabilize the dollar-yen exchange rate.

Is there a new “Mar-a-Lago” Accord for 2025 in the works?

Maybe...

While not an officially recognised agreement, the Mar-a-Lago (Donald Trump’s house) accord has sometimes informally been used to refer to Trump’s proposed set of economic policies that could include a weaker dollar, debt restructuring, and trade realignment.

10 second summary: Why is Trump trying to devalue the US Dollar?

We think that the ultimate goal of the Trump administration is to re-align the global trade balance, re-invigorate domestic supply, restructure its debt and secure its defence industrial base.

A weak US Dollar helps this because...

A low US Dollar means that it is cheaper to import goods from the US.

Cheaper US imports will incentivise domestic manufacturing.

Reduced trade imbalances will help tame the growing US $36 trillion national debt (less borrowing required to finance spending levels)

Domestic manufacturing will help America re-shore critical supply chains - and strengthen defence industrial bases.

This is intended to “make America great again”.

What is Trump’s plan to weaken the US Dollar?

Right now Trump appears to be following the currency devaluation playbook outlined by his appointed Chairman of Economic Advisors, Stephen Miran.

In November, 2024, Stephen wrote a playbook on how to devalue the US Dollar:

A User's Guide to Restructuring the Global Trading System.

In that paper the central view is that the USD is structurally overvalued because of its role as the global reserve currency...

... AND how that overvaluation has led to persistent trade deficits and the erosion of U.S. manufacturing competitiveness.

Which leads over time to an unsustainable accumulation of public and foreign debt.

His strategy to reverse the trade deficit now appears to be being followed by Trump:

- Leveraging US defence support in negotiations regarding economic cooperation with countries...

- Implementing tariffs or at least using them as negotiating tools...

- Aligning currency exchange rates with a coordinated devaluation of the USD.

Sound familiar?

The US has already leveraged defence support in the Ukraine war in exchange for economic cooperation:

(Source)

And Trump has used tariffs as a negotiating tactic:

(Source)

But will Trump follow through with the third part of the plan to coordinate a devaluation of the US Dollar?

And what will it mean for the gold price... and our gold stocks?

Let’s see how that could play out...

How will Trump implement a coordinated effort to devalue the Dollar?

In a nutshell Trump is looking to force the rest of the world to appreciate their currencies to improve US export competitiveness.

In what is being described as a potential new “Mar-a-Lago” accord.

A deal framework is taking inspiration from the Plaza Accord signed back in 1985...

(yep, history does have a habit of repeating itself)

The Plaza Accord was a deal the US signed with the G5 countries TO DEPRECIATE THE USD against major currencies and reduce the US trade deficit and make US exports more competitive...

It was the USA’s way of responding to the rise of the Japanese manufacturing sector back in the 80s...

(like to China’s in 2025)

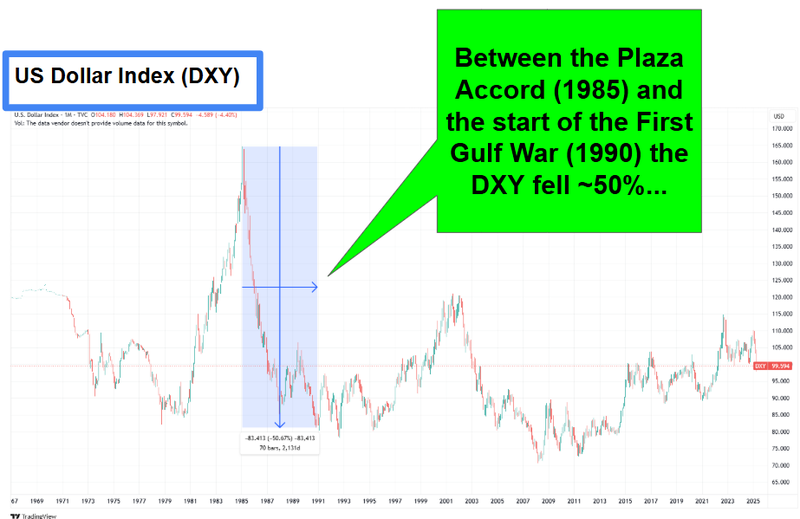

And over the next five years through to the start of the First Gulf War, the plan worked exactly as intended...

The USD (as represented by the Dollar Index, DXY chart) depreciated ~50% against the world’s major currencies:

(The US Dollar Index (DXY) is an index which measures the value of the United States dollar relative to a basket of foreign currencies.)

AND surprise, surprise...

With a ~50% relative fall in the USD, the gold price nearly doubled from US$280 per ounce to US$500 per ounce over the next few years.

Below are some historical figures involved in the Plaza accord and the currency valuation charts:

Now ~40 years later, the US finds itself in a similar position (just swap Japan from 1985 with China today):

- Chinese manufacturing dominating global markets

- US competitiveness in export markets weakened AND

- Most importantly... the USD is structurally overvalued relative to other major currencies.

(important to note that back in 1985 the US national debt was just US $1.8 trillion, it’s now US $36 trillion... a massive jump even when taking inflation into account)

The US has for years been trying to pressure the Chinese into floating their currency and letting it appreciate to a natural level, but the Chinese have resisted and kept an artificially depressed exchange rate intact.

The current stance out of China appears to be resistant to further depreciation of its currency, which is curious to see:

(Source)

This is where things could get really interesting though...

A grand deal for the ages, perhaps?

And probably explains why some investors (and central banks) are front running the potential news and buying up gold.

What is a "Mar-a-Lago Accord" and how will it affect global trade?

Let’s go back to the architect behind the scenes that we mentioned before.

The Chairman of the Council of Economic Advisers Stephen Miran.

Miran is proposing what some outlets have referred to as the "Mar-a-Lago Accord" as a modern analog to the 1985 Plaza Accord - again aimed at doing all of those things discussed above.

Here is a quick side by side breakdown of the similarities of the two (thank you ChatGPT):

A very obvious disclaimer - these are all speculative ideas...

The Trump administration hasn't explicitly talked about a Mar-a-Lago Accord...

we are just reading between the lines...

A 90 day pause to “negotiate a deal”...

Tariff’s being used to force negotiations... etc etc

The following interview with Treasury Secretary Scott Bessent also made us think something is definitely up...

The interviewer asked:

“Are you teasing out a Mar-a-Lago Accord that we should be paying attention for in the future”

Bessent said:

“I’m not sure what you're talking about” with a big grin on his face...

(This is the moment when asked about a Mar-a-Lago accord “I’m not sure what you’re talking about”)

The interviewer then said, “Potentially getting all trading partners together to discuss fair, balanced trade?”

He responded “Well we are doing that over the next 90 days...”

Skip to 9:50 to see the exchange:

Clearly, something bigger is at play, and maybe, the tariffs were Trump’s way of getting “everyone into a room” to negotiate...

(a room at Mar-a-Lago perhaps?)

So how will this all affect the gold price?

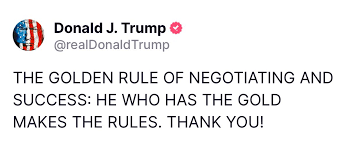

Trump put out this tweet on Truth Social last weekend:

Sent gold price rallying to new highs... up 6% across two trading sessions before coming back.

Reading between the lines of the Trump tweet and the market’s reaction...

The market seems to be pricing in a non-zero chance that the endgame for tariff/trade discussions may result in a USD devaluation...

A USD devaluation means the appreciation of other currencies and even bigger appreciation of assets that can be labelled global “RESERVE” assets...

like gold.

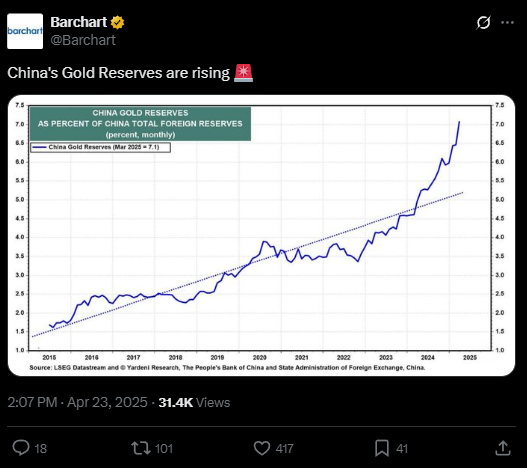

It’s no wonder the Chinese have been stacking gold reserves too...

(Source)

As mentioned earlier, post Plaza Accord in the 1980’s the gold price more than doubled against the USD.

If history was to repeat itself could we get a gold price rally to over US$6,000 per ounce?

No one knows, but if we did we think our small cap gold stocks could perform really well.

(especially KAU which is about to acquire a gold mine that produces over 25,000 ounces of gold per year - read more here. The deal was announced when gold was just $3,000 per ounce)

And JP Morgan’s calls for US$4,000 per ounce could look like coward estimates (versus how bullish it looks from current prices).

(Source)

Critical minerals a winner again this week...

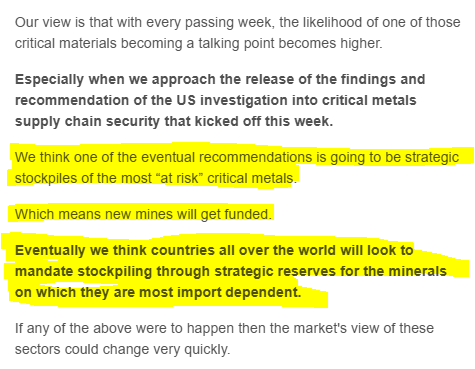

Last week we talked about how we predicted governments around the world would be setting up stockpiles as a trigger for a new wave of demand.

(Source - Weekend Edition 19 April 2025)

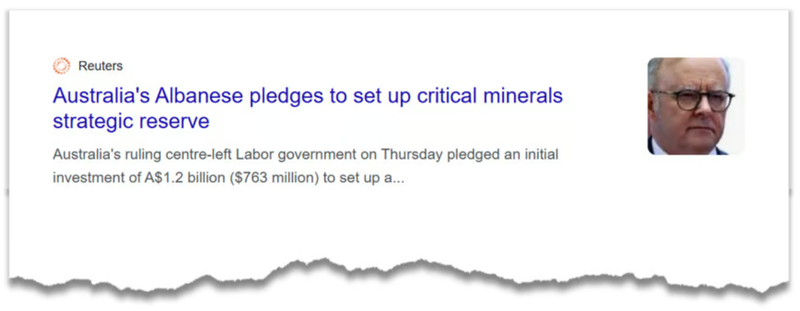

This week right on cue, Australia was one of the first Western countries to make this move.

Current PM Anthony Albanese made a commitment to setup a A$1.2BN national critical minerals stockpile:

(Source)

Just as we said last week, we don't think Australia will be the last to start talking about stockpiles...

Australia benefits from already having a pretty strong domestic mining industry - we are the world’s biggest lithium producers...

In the world’s biggest economy and biggest capital market (the US) the focus is on trying to get domestic production ramped up.

Domestic production comes before stockpiling...

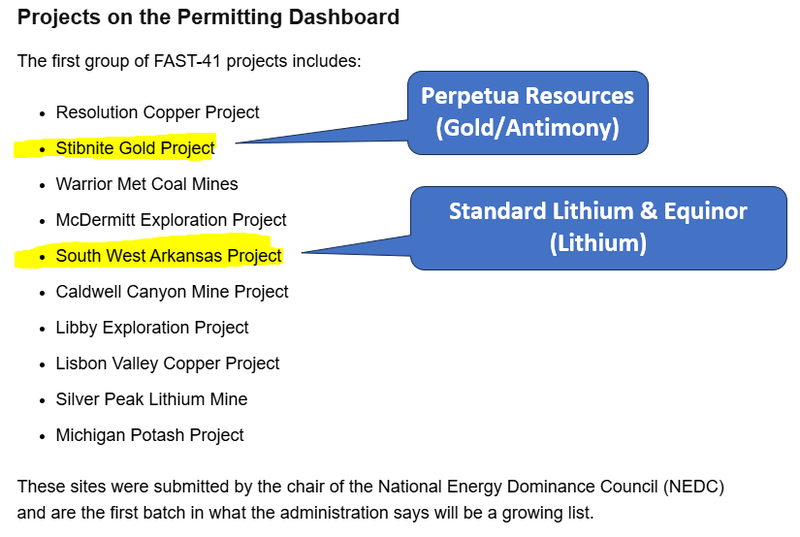

This week: US grants fast track permits to 10 USA based resource projects

The big news out of the US this week was that Trump has selected 10 projects for “fast-track” permitting across a range of minerals.

This included Perpetua Resources gold-antimony project in Idaho and Standard Lithium/Equinor’s lithium project in the Smackover region of Arkansas.

(Source)

Fast permitting is the first order effect of Trump’s Executive Order which was signed only a few weeks ago to try and increase domestic mineral production.

Now, those 10 projects sit on a federal dashboard where permitting is tracked in real time...

The idea is to make the government accountable for permitting timelines.

The two projects that relate to our Portfolio the most were Perpetua’s project and Standard Lithium/Equinor’s project.

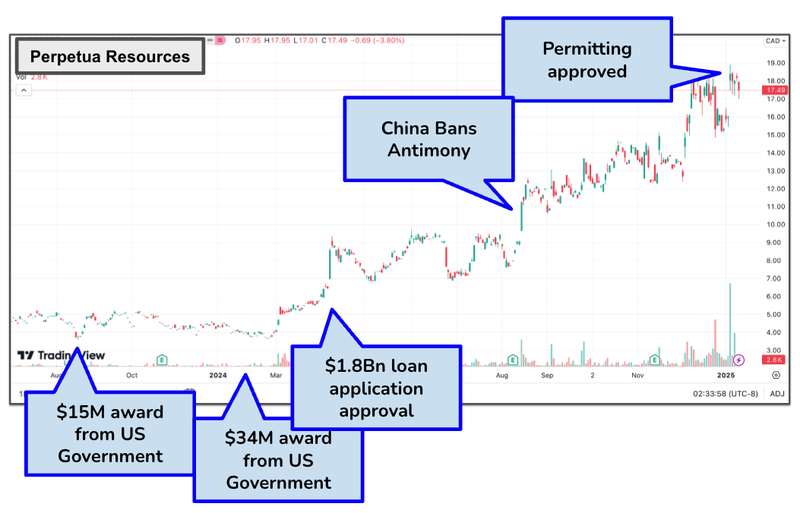

Perpetua’s project is primarily a gold project, but it appears on the list due to its antimony resource.

Antimony is used in stuff like infrared missiles, nuclear weapons and night vision goggles, and mostly as a hardening agent for bullets and tanks.

As a result it is critical in defence supply chains - China introduced export restrictions on antimony in August 2024 and since then the Perpetua Resources share price has climbed higher and higher:

We think our Investment Sun Silver (ASX:SS1) can follow in Perpetua’s footsteps IF it can prove that its project can produce an antimony by-product to its giant silver resource.

So far SS1 has assayed high grade antimony in old drillcores, next it’s all about seeing whether or not that extends across the entire deposit.

We did a deep dive on SS1’s antimony potential for the first time in this August 2024 note:

SS1 announced antimony potential... weeks before antimony became “cool”.

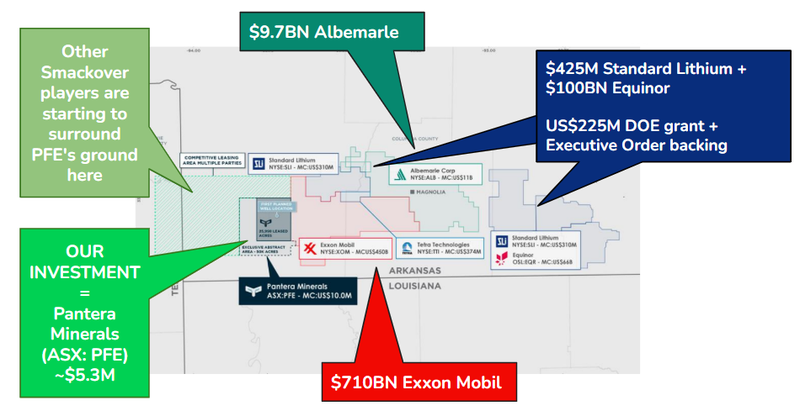

The second one on that list that caught our attention was Standard Lithium and Equinor’s project in the Smackover Formation in Arkansas.

That is the same project that the US Department Of Energy had previously given a US$225M grant to...

The Smackover is also where petrochemical giant Exxon plans to be producing lithium from by 2026/2027.

We are Invested in the only ASX listed company with exposure to the Smackover - Panterra Minerals (ASX:PFE).

We have previously said that we expect the centre for the US Direct Lithium Extraction (DLE) lithium industry to be in the Smackover.

Seeing the US get behind a project in the region is another signal we think this will happen.

Read our latest PFE note here: State of Arkansas to remove sales tax on lithium? $6M capped PFE the only ASX listed player, surrounded by giants

Overall, we think there is a lot more news to come out of the USA that will be good news for companies with assets in the US.

Below are all of our Investments with assets in the US:

- SS1 - Silver-Gold-Antimony in Nevada, USA. Largest pre-development primary silver resource on the ASX.

- JBY - Gold in Nevada, ~1.4M ounce fold equivalent JORC resource and room to grow that further. Immediately adjacent to one of the world’s largest producing gold mines.

- HAR - Gold in California. In the geographic epicentre of one of the biggest gold rushes in history with a target to grow its resource to 1M ounces.

- GUE - Uranium Exploration + Enrichment. A number of uranium exploration tenements in North America and stake in a uranium enrichment technology business.

- GTR - Uranium exploration in Wyoming. Working toward a scoping study on its project.

- 88E - Oil exploration in Alaska, some oil production in Texas and recently signed a ~$60M farm out deal pending a private company’s potential IPO...

- PFE - Lithium exploration in the Smackover Region of Arkansas next to Exxon, Albemarle, and Standard Lithium.

With a potential Mar-a-Lago Accord in the works that could devalue the USD...

The US is trying to solve its crippling debt problem by increasing exports & reducing trade deficits.

Right now, we think gold and silver in the USA will perform the strongest.

Critical minerals projects should start to accelerate soon too.

Are you a s708 sophisticated investor?

If you qualify as a sophisticated investor and would like to see “s708 only” sophisticated investor opportunities: Subscribe to Next Cap Raise.

You will need to send us a valid certificate from a qualified accountant confirming you qualify as a sophisticated investor.

Have a great weekend,

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.