Investors Eye ASX Critical Mineral Plays

Published 19-APR-2025 22:21 P.M.

|

13 minute read

- Commentary: China bans rare earths exports critical to western defence supply chains. Rare earths stocks rip. The US launches investigation into critical metal supply chain risks. Gold hits new all time high AGAIN.

- The other usual stuff: in tomorrow’s Sunday Edition.

It’s now been two weeks since the wave of “global uncertainty” properly kicked off.

The USA’s sweeping tariff announcements made on April 2nd shook up markets...

and many long standing trade relationships between countries.

Each day it seems like a big new tariff extension or reversal jolts things again.

Like everyone else in the markets, we have been trying to wade through the evolving chaos...

And try to answer the biggest question early stage investors have right now:

Which small cap stocks will “win” in a post Trump tariff world?

Whether these are real tariffs that actually get put into effect (i.e. against China)?

or even just the threat of tariffs alone (see the EU and many other countries)...

Trump’s tariff announcements are more than enough to really shake things up.

Most investors and market participants (at the bigger end of town) don’t like this new uncertainty.

(which is why gold just keeps hitting new records... another new all time high AGAIN this week).

As investors in early stage stocks, we actually don’t mind the chaos at all.

Firstly, obviously it's great for our gold and silver stocks...

Secondly, after the boring (and sad?) last two years of being early stage resources investors, we think a shake up might at least bring some interest (and buying) into some small cap resource stocks.

It’s certainly better than the grim couple of years of generally expecting sideways or downwards movements.

Critical metals for military and defence applications took centre stage this week.

Will it be like the electric battery metals boom did back in 2020-2021...?

This time the stakes are much higher...

We are talking about national security as opposed to consumer adoption of a new type of car.

With more at stake, comes more urgency... and more capital available to solve the problem.

Especially when governments and their near-unlimited budgets get involved.

(national security is part of their job description)

And we are hoping for capital inflows into the lucky small stocks that happen to have the right project, in the right location, at the right time.

BUT...

Too much uncertainty isn’t a good thing - functioning financial markets rely on investor confidence and certainty.

And we definitely don’t want to see any all out wars happen.

Our perfect scenario for how we are positioned is that uncertainty leads to gold rising over the next 3 to 5 years.

As the US withdraws from its role as the “world police”... other countries must defend themselves... so they spend big to build up their defences AS DETERRENTS... but never actually have to use them in a kinetic war (we truly hope).

And during this defence build up and reshoring of supply chains, stock piling of critical metals ramps up, creating capital inflows into various critical metals projects to bring them into production

like the ones we are Invested in.

Is that too much to ask? We can only hope (and hold).

It would also be great if some of the 2020-2021 battery metals stocks we still hold that overlap with defence metals will get another run...

Anyway,

The above scenario would be great for our Portfolio.

Unfortunately the world doesn’t behave optimally nor within desired time frames for your Portfolio construction.

Recently we floated our analogy of tariffs being like a massive worldwide market and economic “snow globe shake”.

But how do things settle and what kind of investments stand to benefit?

That we DON’T know... yet.

(particularly in the small end of the ASX market, where we are Invested in and focused on)

This week we saw attention and capital flow into rare earths stocks.

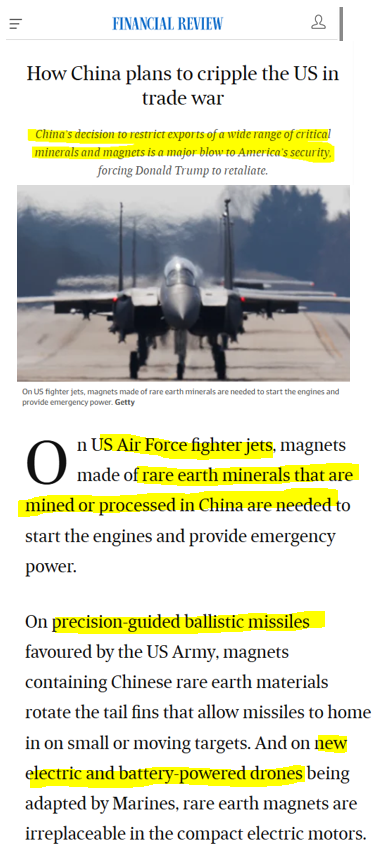

Rare earths stocks surged this week after China announced a rare earths export ban.

Turns out that US air force fighter jets, precision guided ballistic missiles and drones are reliant on rare earths mined or processed, then imported from China:

(Source)

It’s pretty obvious why it’s not ideal to be reliant on your biggest adversary for your defence supply chain...

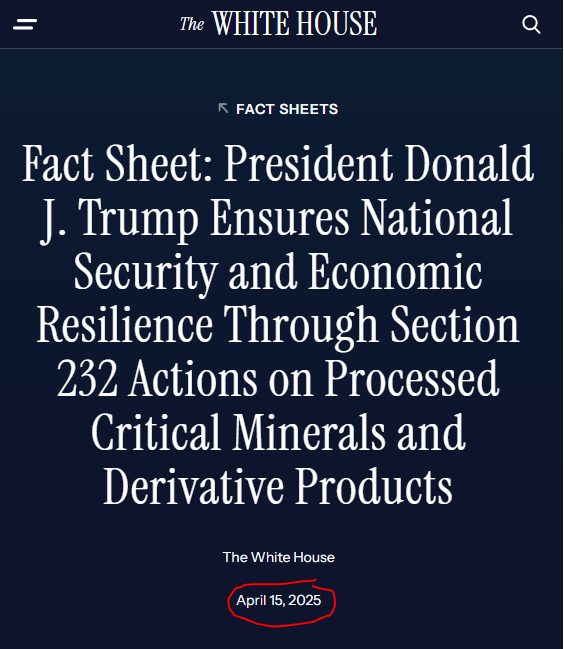

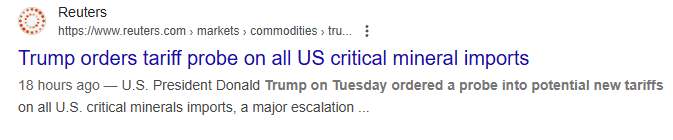

Around 24 hours after China announced this rare earths export ban, Trump announced a government investigation into US critical mineral imports...

The goal is to “evaluate the impact of imports of these materials on America’s security and resilience,”

Basically asking: where is the US over-relying on sourcing metals critical to its military and strategic industrial sectors from adversarial countries?

And what should be done about it?

(Source)

(Source)

(Source)

( uranium mining and processing? Our Investment GUE has a uranium project in the USA and a stake in uranium enrichment technology - they recently did a deal with a US listed company - read more here)

The obvious focus for this new US investigation into critical metal supply chains is on the minerals that are critical for the defence industry.

And we expect recommendations from the investigation will bring capital flowing into certain development stage resource projects where dependence on supply from adversaries is deemed high risk.

(Perhaps some of the ones we are Invested in?)

Especially as the world enters into a period of increased defence spending - supply chains of defence materials will need to be secured.

...like we predicted at the start of the year:

(Read our 2025 Strategy Weekend Edition from January)

Should we have made more new Investments into this space faster over the last 4 months?

Probably.

But global macro themes like this do take a while to properly play out.

And we have been looking at a few new stocks with projects that could emerge as winners once the results (and recommendations) of this investigation are released

There are plenty of different materials that sit in the “critical for defence” bucket.

But the spotlight was very clearly shone on rare earths this week..

There is no doubt about rare earths importance in defence supply chains.

It's actually been a generally known issue for quite a while...

China last initiated a rare earths export ban in 2010-2011, which helped send the Aussie rare earths producer Lynas’ share price from ~70c to $26.60 in the space of two years.

Lynas is starting to move again on the charts after THIS week’s new Chinese rare earths export ban:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Our Investment St George Mining (ASX:SGQ) moved from 1.5c to 2.6c in the space of 10 days.

SGQ is a Brazilian niobium & rare earths developer in the state of Minas Gerais

(same part of Brazil where one of our best ever Investments Latin Resources made its lithium discovery in February 2022 and was acquired by Pilbara Minerals for $560M almost exactly three years later)

This week SGQ released an announcement re-iterating that development studies (ie: plan to build a mine) are underway at their globally significant rare earths resource.

The rare earths story for SGQ has always been bubbling under the surface, and it was one of the key reasons we Invested in SGQ last year.

We like SGQ because it already has an established JORC resource and a genuine shot of quickly moving into development

Plus SGQ are commencing drilling in the next few weeks with the aim to further grow its already large resource.

SGQ’s speed to potential production, just as the rare earths macro heats up, could be a major factor in its success.

This week the market, and the wider world is waking up to the importance of rare earths.

We noticed that rare earths stocks across the board started ripping after the news out of China and the US.

MP materials, the biggest US listed pureplay exposure rallied hard this week - up from ~US$22 per share to a high of ~US$29 per share.

That was a US$1BN+ move in MP’s market cap in only a few days.

(the value of that move alone is enough to buy most of the rare earths names on the ASX outright...)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

For almost 2 years, rare earths have been out of favour with ASX investors - we have even seen a few companies pivot away from the sector entirely.

Good for the companies that picked up assets during the out of favour market, bad for those who exited...

So far, an early winner from the global chaos in our Portfolio is St George Mining (ASX:SGQ).

SGQ picked up its project at what now (in hindsight) looks like the bottom for rare earth projects.

(sort of like how SS1 acquired their giant USA based silver project when silver was out of favour in late 2023)

AND SGQ’s managed to pick up a project that rivals some of the biggest projects in the world.

According to the announcement released by SGQ this week, their rare earths resource size is on par with MP Materials, with a grade on par with Lynas.

Lynas was up ~16% this week - a big move for a company that started the week capped at $7.3BN... yes, billion

SGQ also sits on similar geology (hard rock carbonatite) to both MP Materials and Lynas producing mines.

By the end of this week, Lynas had a market cap of A$8.3BN and MP Materials a market cap of US$4.3BN.

SGQ finished the week with a market cap of A$67M.

This relatively low valuation reflects the stage of development SGQ is at - a much earlier stage versus the established producers.

It also shows the potential upside in SGQ IF it can progress its Brazilian rare earths asset to production (of course it wont be easy - success is no guarantee and development stage resource investing is risky).

And there’s clearly some interest coming into SGQ and market starting to wake up to the scale of its project - up almost 100% in under a week:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

We put out a note on SGQ earlier this week: China bans rare earth exports. SGQ has one of the largest and highest grade hard rock, rare earths resources in the world

Rare Earths the talking point for now... what’s next?

For now the market attention (and capital) has started flowing into rare earths....

The reality is that the “defence materials” macro thematic applies to a larger list of “critical minerals”.

It will be interesting to see the findings of the US critical and metals investigation when they are released.

And which particular critical or defence metals will be suddenly prioritised.

(and how tariffs may be leveraged to help secure that supply from different countries)

You can see the current USA critical materials list here:

This list covers most strategic industrial uses.

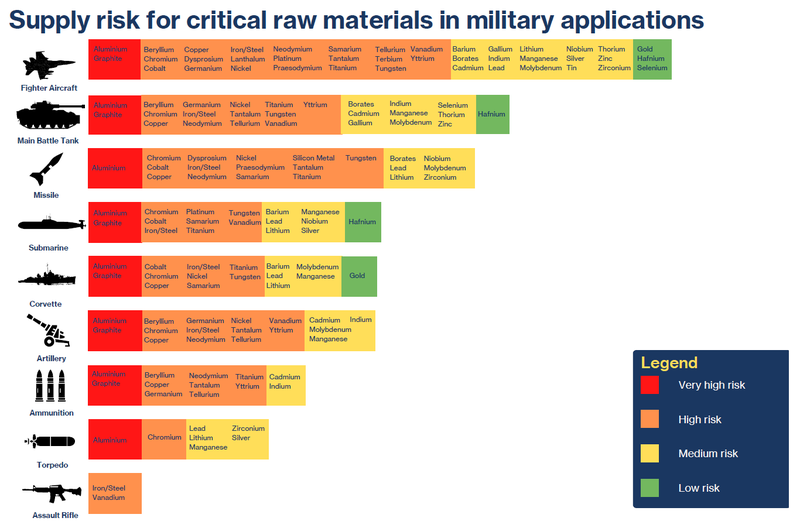

When specifically looking at defence and military metals, the below NATO list summarises it nicely.

At the end of 2024, NATO released a set of 12 “defence-critical raw materials”:

(Source)

(we are looking at a few new companies that we think could become a focus over the near term)

We have already seen aluminium generate some market interest.

Aluminium is shown multiple times in the “red zone”, meaning “very high supply risk”.

Bauxite is used to make industrial aluminium.

Bauxite stocks rallied hard into the end of last year.

(we are Invested in Bauxite developer CAY that looks like it could be in production within 12 months... read our latest CAY note here)

There are still a bunch of different minerals that haven't caught mainstream attention in the current cycle yet - like lithium, graphite, vanadium, tungsten, cobalt etc...

Many of those markets are still trading at all time lows and investor sentiment is as bad as we have seen in a while.

(much like rare earths was only a few weeks ago).

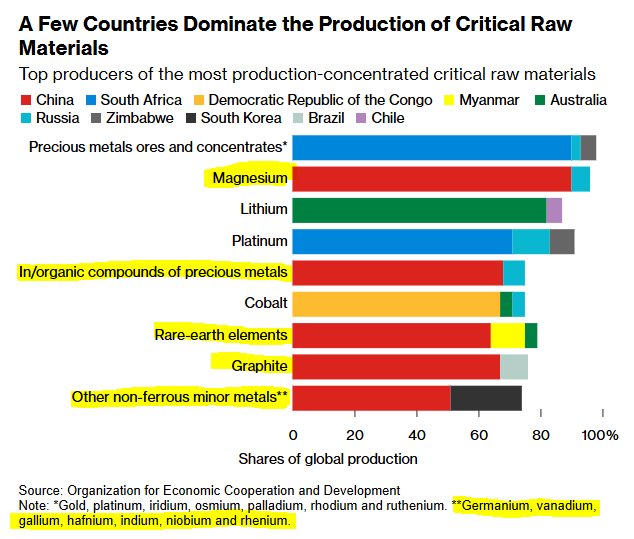

This isn’t just a rare earths story though, there are other critical minerals with just as much concentration risk...

China dominates mining and processing for a lot of these critical minerals.

Just look at magnesium and graphite as well as things like germanium, vanadium, gallium, hafnium, indium, niobium and rhenium:

(Source)

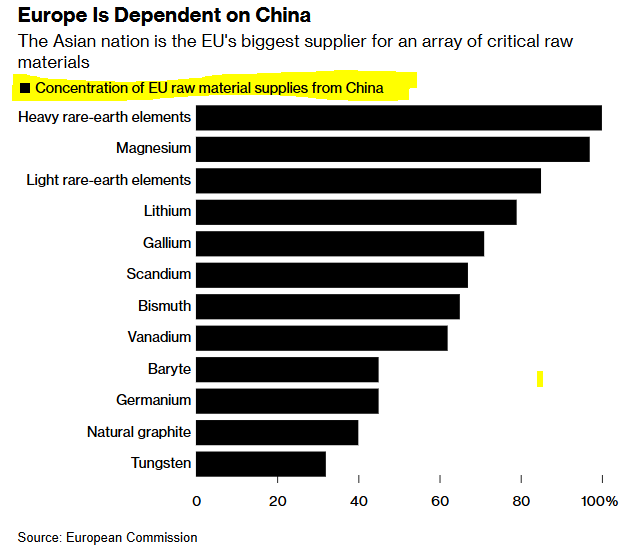

All of the above has been in the context of the US vs China tensions...

When we start to look at China vs anywhere else in the world, the supply concentration is just as bad.

The following chart shows European dependence on China for critical minerals supply:

(Again a familiar story of heavy dependence)

(Source)

Our view is that with every passing week, the likelihood of one of those critical materials becoming a talking point becomes higher.

Especially when we approach the release of the findings and recommendation of the US investigation into critical metals supply chain security that kicked off this week.

We think one of the eventual recommendations is going to be strategic stockpiles of the most “at risk” critical metals.

Which means new mines will get funded.

Eventually we think countries all over the world will look to mandate stockpiling through strategic reserves for the minerals on which they are most import dependent.

If any of the above were to happen then the market's view of these sectors could change very quickly.

(rare earths genuinely stank as a macro theme for the last two years - how quickly that can change in an instant)

Gold hitting new all time highs again

It wouldn’t be a weekend email without us having written about the latest in the gold/silver space.

A round of applause for gold again - it hit another new all time high against the USD:

The reason for the continuous surge?

As always, it’s hard to say for sure but with increased trade war tensions, higher and higher tariffs being thrown around by China and the US probably had something to do with it.

With the US threatening tariffs & sanctions on the rest of the world, it makes it less appealing for countries to hold/hoard and trade in the USD.

Which inevitably reduces demand and in the short term the value of the USD.

It also means capital may start looking for new reserve assets that can be used to settle international trade.

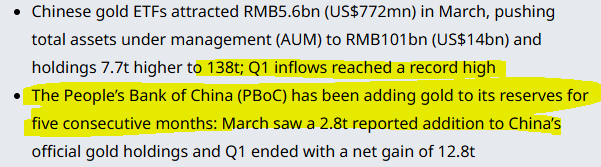

The reserve asset of choice so far looks to be gold.

Chinese Central bank is still a net buyer (for the fifth month running) & Chinese gold ETFs had their biggest inflows EVER in Q1 of this year:

(Source)

More net buying coming into the market means more pressure on gold and silver to the upside.

Silver has been trading sideways and hasn't had that generational run like gold YET.

The following screenshot from a macro strategist we follow sums up the opportunity in silver pretty well:

(Source)

Gold’s been running and still looks very strong, but silver might just be gearing up for a run of its own.

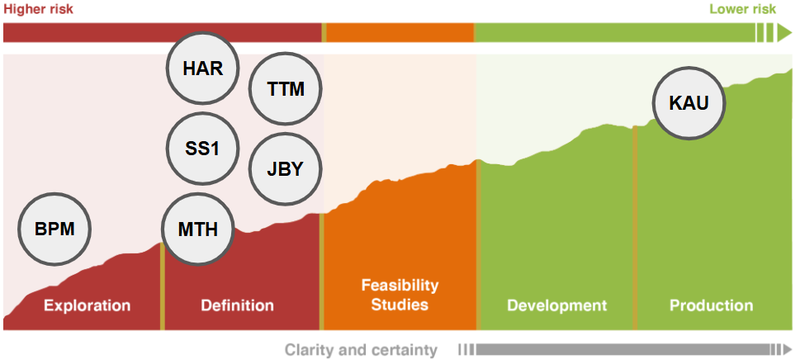

Our Investments in gold/silver are as follows:

- Sun Silver (ASX:SS1) - silver in Nevada, USA (resource definition stage) - read our latest note on SS1

- Mithril Silver and Gold (ASX:MTH) - silver/gold in Mexico (resource definition stage) - read our latest note on MTH

- Kaiser Reef (ASX:KAU) - gold in Victoria/Tasmania (production stage) - read our latest note on KAU

- James Bay Minerals (ASX: JBY) - gold in Nevada, USA (resource definition stage) - read our latest note on JBY

- Titan Minerals (ASX:TTM) - gold in Ecuador (resource definition stage) - read our latest note on TTM

- Haranga Resources (ASX:HAR) - gold in California, USA (resource definition stage) - read our latest note on HAR

- BPM Minerals (ASX:BPM) - gold in WA (exploration stage) - read our latest Quick Take on BPM

For those wanting our deep dive on why we’ve Invested in gold and silver stocks we’ve put our thoughts together in the following e-book:

Are you a s708 sophisticated investor?

If you qualify as a sophisticated investor and would like to see “s708 only” sophisticated investor opportunities: Subscribe to Next Cap Raise.

You will need to send us a valid certificate from a qualified accountant confirming you qualify as a sophisticated investor.

Have a great weekend,

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.