$98M KAU produces 1,200 ounces of gold (~$6.2M) in 10 days…

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 4,796,210 KAU shares and the Company’s staff own 71,000 KAU shares at the time of publishing this article. The Company has been engaged by KAU to share our commentary on the progress of our Investment in KAU over time.

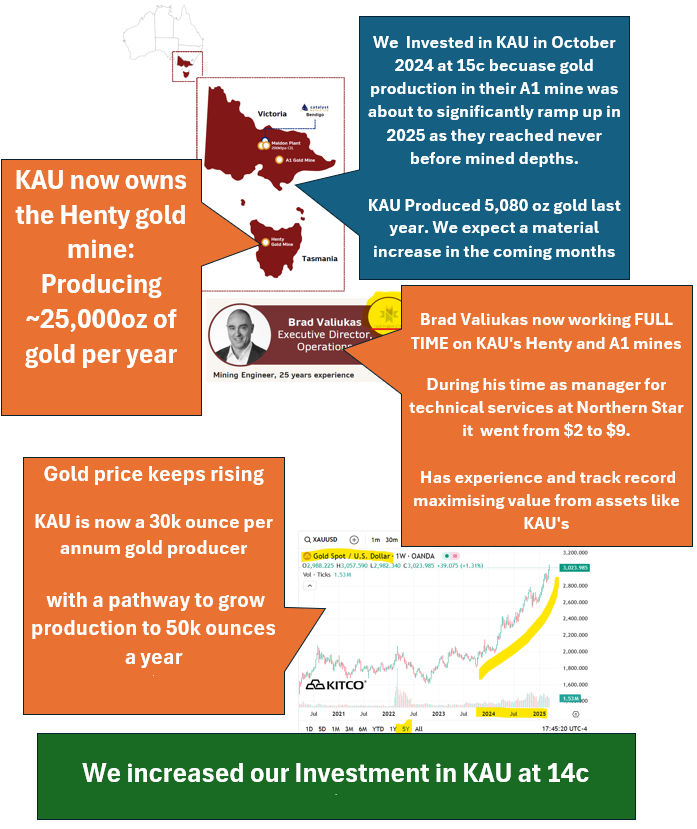

10 days ago, Kaiser Reef (ASX:KAU) completed the acquisition of the 25,000 oz per year producing Henty gold mine in Tasmania.

...adding to its current ~5,000 oz per year producing A1 gold mine in Victoria.

KAU is now a multi-mine, ~30k ounce per annum gold producer.

(That’s $156M of gold over 12 months at today’s prices for $98M capped KAU).

The gold price keeps going up.

And both mines have plenty of near-term exploration upside where success can be instantly monetised...

KAU’s plan is to grow production to a combined 50k ounces a year....

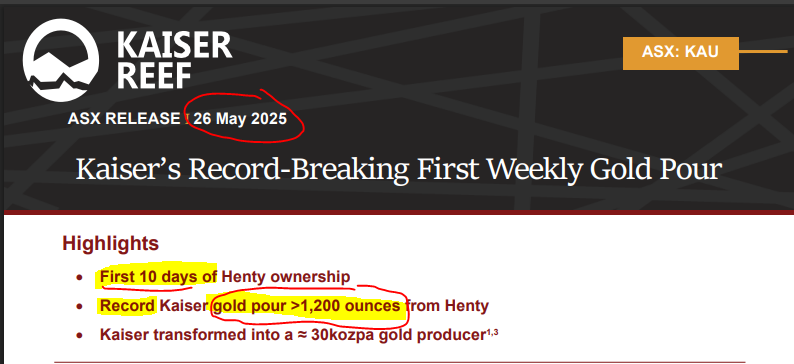

TODAY: KAU announced a record gold pour of over 1,200 ounces of gold from the first 10 days of owning its newly acquired Henty gold mine.

That's $6.2M of gold at today’s gold price of ~A$5,170 per ounce.

And if we take the mine’s previous owner's last reported production “all in cost per ounce” of $3,283 (Source )...

By our rough calcs that’s ~$2.264M profit to KAU in the first 10 days of owning this new mine.

KAU has been saying they expect 25,000 oz per year production from Henty...

By our calcs, 1,200 ounces produced over 10 days announced this morning would be 43,800 ounces over a year.

So this first 10 days of production have far exceeded expectations...

A glorious way to kick off new ownership of this mine for KAU.

But it appears they may have just a higher grade section in the mine - it might keep going for longer... or quickly revert back to average.

It's a great start but we are keeping our expectations set to 25,000 oz per year from Henty for now.

So how is this gold producer that just poured an over-expectation, record ~$6.2M of gold in 10 days, trading at a $98M market cap while gold prices are near all time highs?

Because they only just acquired this mine 10 days ago...

And the news of this record gold pour only came out at ~8:30am AEST this morning.

...so the market hasn’t had a chance to react to it yet.

(at last trade of 16.5c KAU was capped at A$98M, with ~$27M cash and $10M in debt)

KAU’s new gold mine adds more than 8x KAU’s current gold production based on its last quarterly...

(thats using the estimated 25,000 oz per year production guided by KAU, NOT the larger number we extrapolated from the record 10 day gold production announced this morning)

Combined with its expected ramp up in gold production at its existing Victorian assets, KAU’s goal is to grow production to 50,000 ounces a year.

(especially if KAU can regularly pull out over-expectation gold pours from Henty)

Just as gold keeps hitting records highs.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

KAU has acquired the Henty gold mine in Tasmania - a profitable, high grade underground Tasmanian gold mine with over $100M of project infrastructure in place.

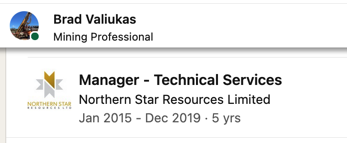

With the Henty acquisition now complete, KAU director Brad Valiukas has moved into the role of full time ‘Director of Operations’.

Here is a photo of Brad in his first week of the role, overseeing the $6.2M (our estimates $2.2M profit) gold pour from the first 10 days at Henty:

(Source)

Brad was Manager for Technical Services at Northern Star Resources during its formative 2015-2019 growth period.

He was in charge of optimising and growing its assets.

...during which period Northern Star’s share price went from ~$2 to $9 per share. Northern Star is now capped at $20BN.

Brad is now full-time at KAU, focused on optimising mine production and reducing costs at KAU’s A1 mine in Victoria and newly acquired Henty mine in Tasmania

(more on these optimisation plans later in this note).

As part of this newly completed acquisition, KAU has also secured a JV partner on its Victorian processing plant and new 19.9% shareholder:

$1.5BN market capped gold producer Catalyst Metals.

The key reasons behind this tie up come down to Catalyst and our Investment KAU being able to work together in the future in a big win-win for both companies.

KAU wanted Catalyst’s Henty gold mine, Catalyst wanted access to KAU’s Victorian gold processing plant.

A win-win.

To get a sense of the company's transforming scale of KAU’s binding acquisition:

We originally invested in KAU at 15c in October because its A1 mine in Victoria was on the cusp of ramping up production during 2025.

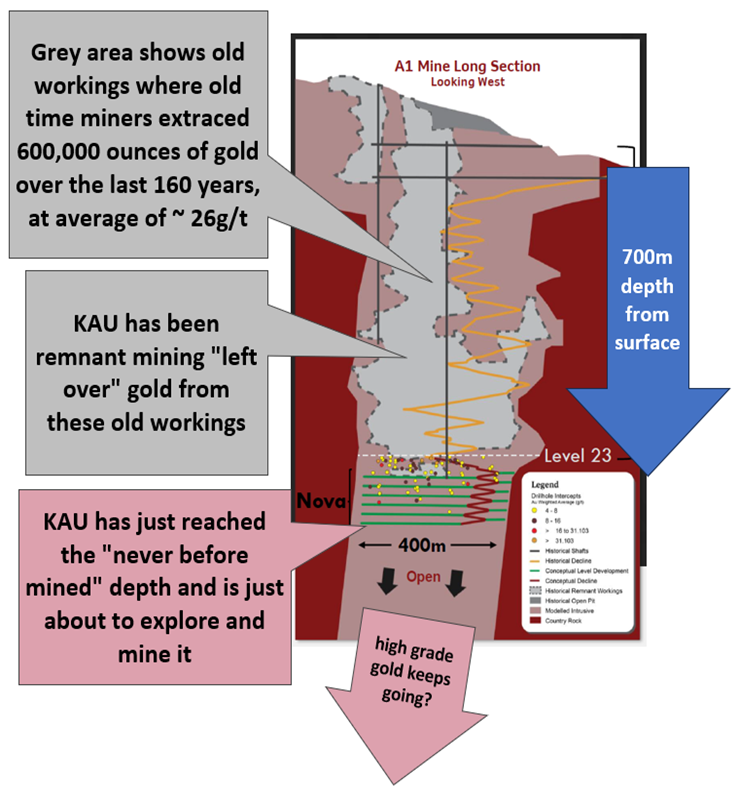

And after years of investment in improving access to the A1 gold mine in Victoria, KAU is just getting to the fresh virgin zone to mine, which means production is only going to grow from here.

KAU’s A1 gold mine produced 551 ounces of gold last quarter.

We are still waiting for the newly reached, “never before mined” levels at A1 to deliver that first high grade, “big production” quarter...

But we think there is a scenario where it could push out 12,000 to 18,000 ounces over a 2-3 quarter period (more on this below).

Victoria is home to one the world’s highest grade gold mines currently in operation, owned by $92BN Agnico Eagle - Fosterville.

When discoveries are made in Victoria, they can be seriously high grade and real cash cows for the companies that own them...

BUT for decades Victoria has been chronically underexplored.

With record gold prices, we think the Victorian gold industry is about to have a renaissance - and KAU’s assets are right in the centre of things.

KAU’s Victorian assets were the reason we first Invested in KAU - long term we think these could become very valuable.

(Especially if new discoveries are made and processing capacity becomes a hot commodity)

Meanwhile at its newly acquired mine in Tasmania, there are also a number of exploration targets for KAU to go after and push the current mine life of ~5 years out further.

So in summary, KAU has just become a multi-asset 30k ounce per year gold producer just as gold prices hit all time highs.

...with near term exploration upside that can be instantly monetised.

And a pathway to grow production to 50k ounces a year.

With gold prices where they are, we think KAU now finally has the cash (and cashflow) to give exploration a proper crack in Victoria AND on its Tasmanian asset.

Now all we need is for one or two of the following to happen for KAU inside the next 6-9 months:

- The gold price to stay where it is (it would be even better if it keeps running),

- Henty to pump out similar quarters to the one that just passed,

- Increased production at the A1 mine, and;

- Exploration success (hopefully new discoveries) across any of its projects.

IF even just a couple of those happen, in 12 months time we think KAU’s valuation could be multiples of where it is today.

The big surprise upside would be if KAU can get a few unexpected big quarters of production out of its Victorian assets.

(after many delays we think the market isn’t pricing in much potential A1 success)

Last quarter KAU’s A1 mine in Victoria produced ~555 ounces of gold.

We think KAU could do multiples of that if things go right in Victoria

(this ramp up in Victorian gold production is what we have been waiting for at A1 since we first Invested in KAU back in October 2024)

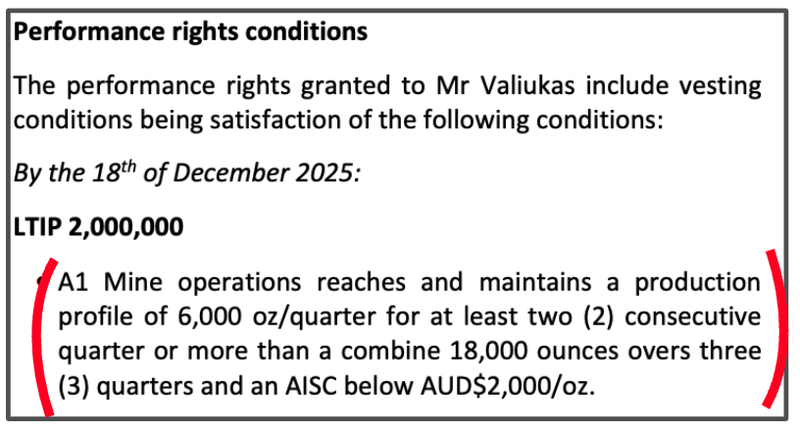

Just for a rough ball park idea of what is possible, KAU’s directors were given the following performance rights that are expiring on the 18th of Dec 2025 (in 7 months from now)...

(Source)

These management bonuses only vest if KAU can push its Victorian A1 gold mine to achieve:

- 6,000 ounces of gold production for 2x consecutive quarters at an all in cost below A$2,000 per ounce.

- 18,000 ounces of gold production over 3 quarters with an all in cost below A$2,000 per ounce.

The first scenario would net KAU ~$36M in profit at today’s gold prices...

... and the second would net KAU ~$54M in profit.

And this is just on KAU’s original Victorian gold mine (A1)

(it doesn't include the expected 25,000 oz per year from KAU’s new Henty mine)

We would gladly take either of those scenarios before December given where KAU’s market cap is right now - $98M market cap at 16.5c where it closed on Friday.

If KAU can get this level of production out of its Victorian assets inside the next 7 months, then it could end up being a big ~9 months for KAU.

Especially if Henty keeps surprising us with the occasional above expectation gold pours.

Now a 30,000 oz per year gold producer - Here’s what KAU owns

KAU is for the first time ever mining virgin sections of its Victorian A1 gold mine, and can now supercharge its cashflows with Henty in Tasmania.

The bet here is the gold price stays at current levels or keeps going up - and KAU becomes extremely profitable.

One year of production (30k ounces) at current gold prices (A$5,200/oz) would be $156M in revenues for KAU.

Henty’s all in sustaining cost for the March quarter was ~$3,283 per ounce.

IF KAU can stabilize all in costs across its two assets to somewhere in the A$3,000-3,500 per ounce range - it could mean ~$50-60M in profits/annum...

(and more if they successfully increase from 30k oz per year to 50k oz per year)

Of course gold mining can be a risky endeavor - the gold price can go down, and costs can go up unexpectedly - success is not a guarantee.

Now that Henty acquisition has been completed 10 days ago, KAU holds:

- Gold mine in Victoria(A1 Mine, 100% owned) - The A1 gold mine is where KAU just started mining never before mined parts of the project. KAU is targeting production of ~20k ounces per annum from this mine.

- Gold mine in Tasmania(Henty, 100% being acquired) - a “plug and play” type asset, already producing ~25k ounces per annum and with over 5+ years of mine life in reserves (10+ in resources).

- Gold exploration in Victoria (Maldon, 100% owned) - Inferred JORC resource of 1.2Mt @ 4.4g/t gold for ~186K ounce gold resource and reserve with exploration upside.

- Gold plant in Victoria (Maldon, option to go 50-50 on this with $1.6BN Catalyst Metals) - Running at 20-30% capacity with the opportunity to ramp up to 350k tonnes per annum. Plants in Victoria are almost impossible to permit nowadays... anyone looking to roll up assets in Victoria could see this as a strategically important asset.

As mentioned, KAU is capped at $98M at its last traded price of 16.5c.

That brings KAU closer to the ~$100M level where the company becomes more investable for institutional funds.

Fund managers don’t (really they can’t) invest in stocks that are too small because of liquidity/size limitations mandated by the fund.

IF KAU can deliver a few strong quarters into record gold prices, there is a chance the stock re-rates to a market cap well above $100-150M which is the level where we think buying from institutional gold funds can come into play.

Our new KAU Investment Memo

With the Henty acquisition now completed and revenues from that mine flowing into KAU’s bank account, we think KAU’s business has changed in a material enough way for us to reset our KAU Investment Memo.

Our Investment Memos summarise our Investments, and include:

- What does KAU do?

- The macro theme for KAU

- Our KAU Big Bet

- Why we are Invested in KAU

- What we want to see KAU achieve

- The key risks to our Investment Thesis

First though, here are the 10 key reasons why we are Invested in KAU:

10 Reasons why we are Invested in KAU

1. The gold price is surging

Gold is trading at all time highs against just about every currency in the world. At the time of writing this, gold is trading at ~A$5,170 per ounce, which is over 100% above its 2021 peak...

2. Two operating assets producing >30k ounces of gold per annum

KAU is now the 100% owner of projects in Tasmania and Victoria that combined produce more than 30,000 ounces of gold per annum. In Tasmania KAU is producing ~25k ounces per annum and in Victoria ~5k ounces per annum.

3. KAU is an unhedged gold producer

Some gold producers commit to sell future gold production at a fixed gold price - which means they do not benefit from rising gold prices (or suffer from falling prices). KAU is NOT hedged, meaning the more the gold price goes up the better off KAU will be. Based on today’s gold price KAU could generate >A$150M in revenues...

4. Projects have combined infrastructure worth >$100M

At its Tasmanian project there is over $100M+ of processing and mine infrastructure. In Victoria, KAU owns one of few fully permitted processing plants in the state. Building a new plant from scratch in either location would take years of permitting and upwards of KAU’s current market cap.

5. KAU’s processing infrastructure in Victoria is strategically important

A new processing plant in Victoria would be extremely hard to get permitted and built from scratch. We think a big part of the reason KAU’s Henty deal went through is because of the value $1.5BN Catalyst Metals saw in the Victorian plant - Catalyst is now KAU’s biggest shareholder owning 19.99% of the company.

6. KAU’s plan is to increase production to >50k ounces per annum

The current plan for KAU is to increase processing capacity in Tasmania by ~30% which could add upwards of 10,000 ounces of production per annum. Ultimately the goal is to increase production across both its Tasmanian and Victoria assets to that ~50k ounces per annum run rate.

7. Exploration upside right next to existing infrastructure

We like that KAU’s projects still have a lot of untapped exploration upside. The major benefit is that any big discovery can be commercialised using the company’s existing processing infrastructure.

8. Previous investors/owners have done all the heavy lifting for KAU

We think this applies to all of KAU’s assets. In Tasmania the heavy lifting was done by Catalyst Metals over the last few years. In Victoria, the heavy lifting was done by the previous owners who have been mining remnant ore for 40+ years, KAU is the first company to be mining fresh, virgin ground at its A1 mine in Victoria.

9. Acquiring big gold assets has worked for other ASX companies

Northern Star was capped at $7M when it made its first big acquisition for $40M. 25 years later and several other acquisitions later Northern Star is capped at $20BN. Growing quickly through acquisitions also means KAU’s market cap can get to a size where institutional investors are able to invest in the company.

10. KAU’s Director of Operations - Brad Valiukas - has experience maximising value from assets like these and is now working full time on Henty and A1

Brad was Manager for Technical Services at Northern Star during 2015-2019. His role was spread across the entire Northern Star portfolio and he helped set up the foundations for assets like Jundee to be the cornerstone of the $20BN producers project portfolio.

M&A has built some of the ASX’s biggest gold companies - Why we like KAU’s acquisition strategy

Some of the biggest gold producers on the ASX today were born from acquisitions like the one KAU just closed.

Especially the deals where smaller companies took over assets that the existing owners had outgrown.

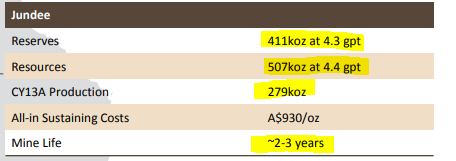

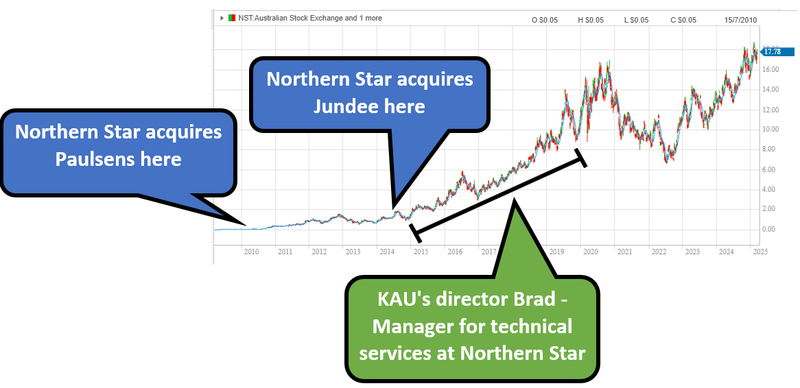

One of the best examples of that was Northern Star’s acquisition of the Jundee gold mine from Barrick...

Jundee was acquired by Northern Star from Barrick for $82.5M. At the time the project had only 2-3 years of mine life left (similar to KAU’s new Henty mine).

(Source - Presentation 13 May 2014)

10+ years later Jundee is STILL producing at ~250k+ ounces of gold per annum and has almost 6M ounces of gold in resources today...

So Northern Star was able to turn that 2-3 year mine life into a project that has printed billions of dollars in cash for the company for over 20+ years...

Something similar to the Jundee story at Northern Star would be the dream scenario for KAU with Henty...

One thing KAU and Northern Star have in common is KAU’s new Director of Operations - Brad Valliukas.

Brad was Manager for Technical Services at Northern Star Resources between 2015 and 2019.

(Source)

He was specifically in charge of optimising and growing the company's assets (including Jundee)...

During which time Northern Star’s share price went from ~$2 to $9 per share.

See our deep dive in Brad’s background here: KAU’s new Director of Operations - he has done something similar before - at Northern Star

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Now we're not saying Brad was solely responsible for Northern Star’s growth.

But it's definitely a good sign when one of the key operations guys was around for an incredible growth story, and is taking all of that experience and lessons learnt to the next venture - KAU.

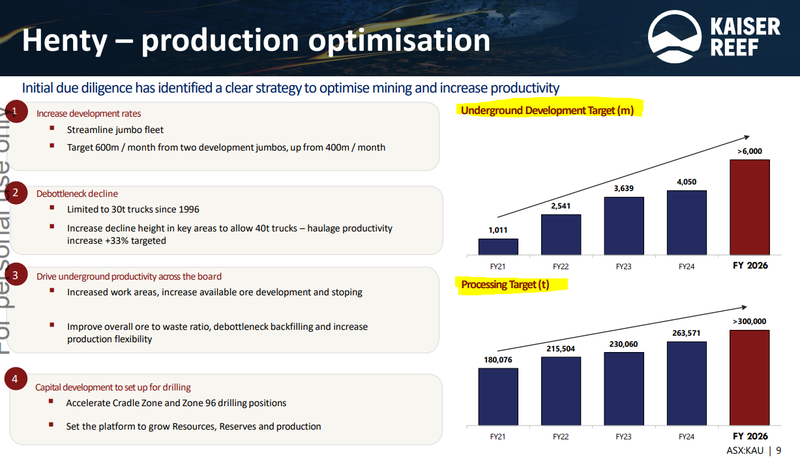

Looking at slide 9 from KAU’s recent investor presentation Brad and the rest of the KAU team clearly have a plan for the Henty asset too..

It's a four stage plan, but the single most important thing we will be looking out for is “processing capacity improvements”:

The current processing capacity at Henty is ~300ktpa.

KAU thinks it can get that to a level >400ktpa AND increase productivity by automating one of the components of the mill.

An extra 100ktpa at the reserve grade of ~4g/t gold would mean KAU could bump up production by ~13,000 ounces of gold a year...

That would be ~$67M more gold at today’s prices if KAU can get processing up to that rate and maintain it.

There is a very clear precedent for acquisitions on the ASX working out in the long run - probably because it gives new teams an opportunity to apply a new way of thinking to maximise the potential of a project.

We also think it's because acquisitions allow smaller companies to grow QUICKLY.

These big gold deals seem to work in the long run because they are a faster way for a micro cap to make itself “institution-friendly”.

A common problem small miners face is they cant access the deeper pocketed institutional investors until they have reached a certain size (often >$100-200m+ market caps).

Here’s how it is and how it relates to KAU now - at a very high level it means is:

- Deep pocketed institutional investors aren't “allowed” to invest in micro cap stocks (less than $100-200M) because their mandates deem micro caps too “risky” AND because tiny positions aren’t meaningful enough for their investors.

- By growing quickly (through acquisitions), KAU’s market cap can re-rate to a level where these institutions mandates allow them to invest & they can build up big enough positions in the stock.

- The bigger KAU gets, the bigger the available capital pool gets AND then eventually index buying kicks in and takes control.

So far KAU has executed on this strategy pretty well......

KAU initially listed on the ASX with a number of exploration assets in NSW.

Then later in 2020 KAU bought the company’s Victorian assets (Maldon and A1).

Those assets took the company to the ~$40-50M market cap that it was only a few months ago.

KAU then used that market cap to acquire the Henty mine and is now capped at ~$100M.

The big win would be KAU being able to expand life of mine, and make Henty its cornerstone asset to take it to a market cap of over ~$200M market cap and above.

Production rates will be a key driver of whether or not KAU can achieve that, but we think exploration can also play a big role...

Exploration is still a big part of the story with producing ounces

One thing successful ASX gold producers have in common is that they used existing cashflows to fund exploration.

Dig up the gold, sell the gold, find more gold... rinse and repeat.

Any big, new, high grade gold discoveries can be quickly monetised.

...and the market likes that.

Exploration success has kept many gold mines producing well beyond the initial mine life identified by the discovered resource or reserve.

Hundreds of millions of dollars in capital is spent on project infrastructure, and so operators are incentivised to do as much drilling in and around the project to try and make new discoveries.

New discoveries that can feed straight into the existing infrastructure.

As mentioned earlier, at Northern Star’s Jundee mine, a 2-3 year mine life has become over 10 years of production with exploration success.

14 years after Northern Star acquired the project, they produced ~270k ounces in one year - at today’s gold prices that's over A$1.2BN in gold...

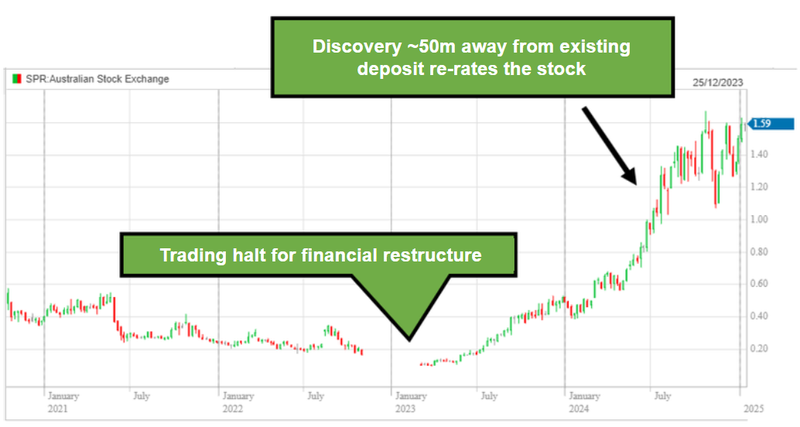

A more recent success story on the ASX has been Spartan Resources (the old Gascoyne Resources).

Spartan went from 10c to ~$1.80 per share.

Spartan is now an M&A target of Ramelius Resources in a deal worth up to $4.2BN.

Spartan (Gascoyne) had been restructured multiple times before in 2022 it drilled a hole ~50m away from its existing JORC resource (which had been producing gold for years) changed the company’s fortunes.

Previous drilling had missed a giant discovery, literally a stone's throw away from its old open pit...

Spartan’s new discovery and all the drilling after it took the company to a market cap close to $2BN.

Past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Exploration upside is still a big part of the KAU’s story on the asset being acquired today and its Victorian assets.

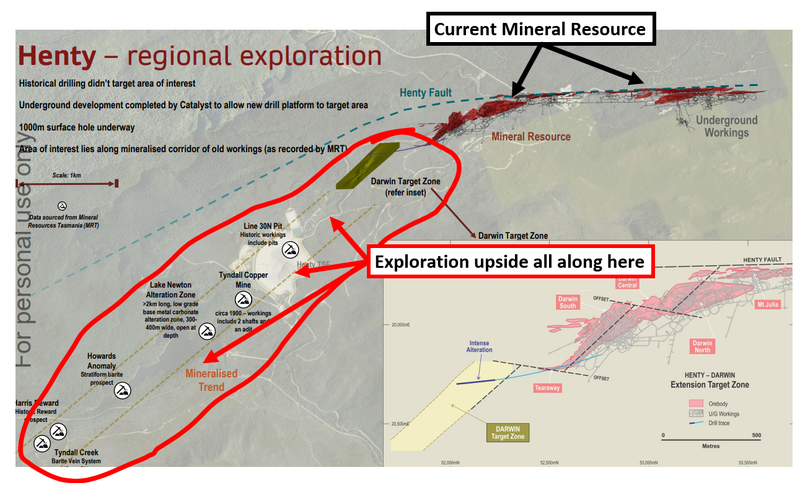

Here are the parts of KAU’s Tasmanian project that are open for exploring:

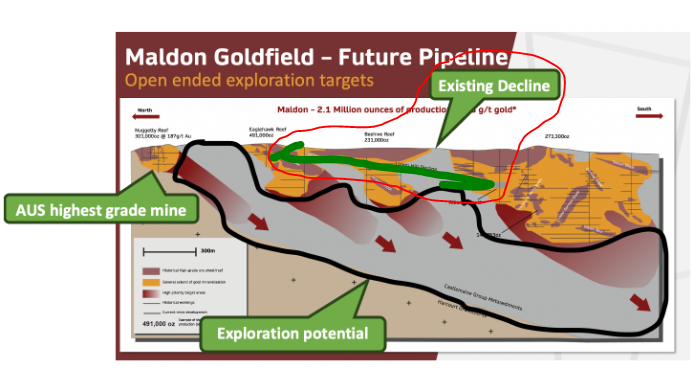

And here is a visual of KAU’s Maldon assets in Victoria next door to its processing plant that haven't had any widescale exploration done on them:

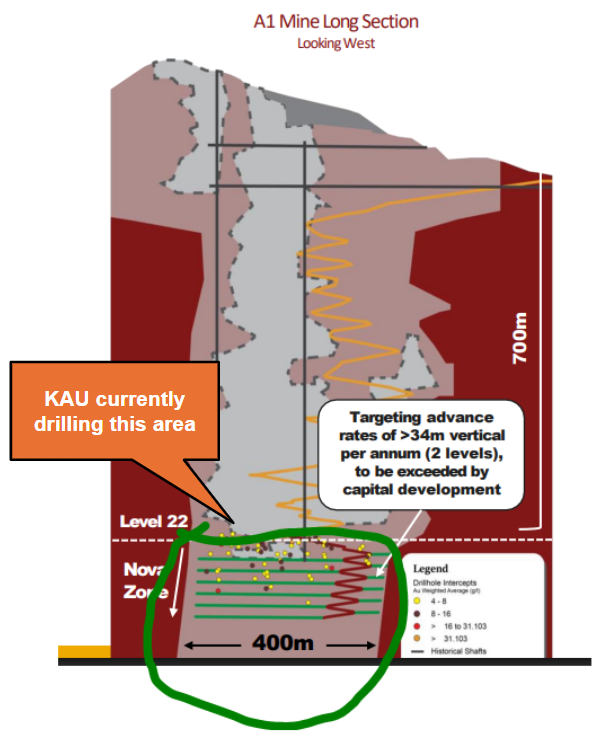

And of course, there is A1 - where any major new discovery could actually be mined fairly quickly:

We are hoping the cashflow from both its Henty and A1 mines can be used to run bigger exploration programs across its projects and (fingers crossed) make new discoveries.

KAU is leveraged to increasing gold prices as an unhedged producer

Usually small/mid and large cap gold companies all tend to take out a certain level of “hedging” when they have operating assets.

A lot of the costs of operating these assets are fixed, so the producers want certainty on a certain level of revenues, so they pick the safe option and lock in prices for a certain level of production.

I.e a producer might lock in a A$5,000 per ounce price for the next 20,000 ounces they produce.

If the gold prices falls, it looks like a genius decision.

but when gold prices are running, hedged producers miss out on the upside.

One of the reasons we are Invested in KAU is because it is completely unhedged.

Meaning it has 100% exposure to an increasing gold price.

And we think the gold price is going higher over the coming years...

And we think gold price could keep running

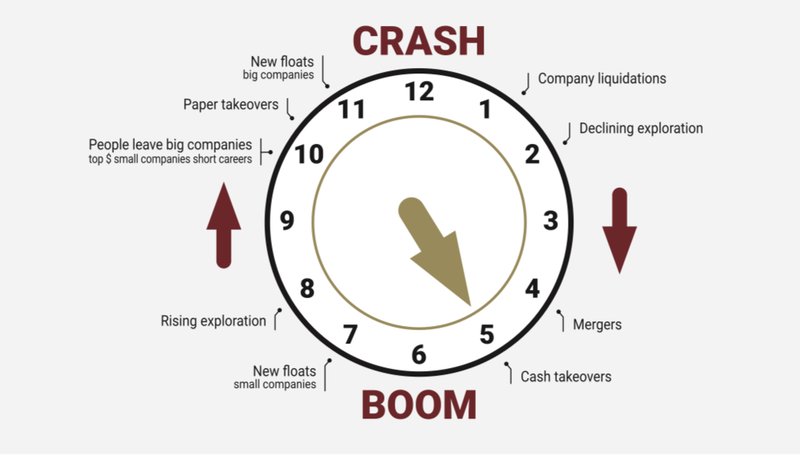

Lion Selection Group - a listed investment company that invests in gold companies thinks we are about to enter “boom times” in the sector.

In their latest quarterly, they put the gold industry at 5 o’clock, just before 6 (when boom times begin):

We think that the boom times could coincide with a further run in gold prices for three reasons:

US debt is still a big problem

US debt is growing every day. It now stands at US $36 trillion dollars.

The bigger that number gets the more difficult it becomes to hold USD as a reserve asset.

...and there are rumblings of increasing the US “debt ceiling” yet again.

(The “debt ceiling” is a cap set by lawmakers on the amount of money the Treasury can borrow to meet federal spending obligations.)

Some even suggesting to remove the debt ceiling alltogether... (Source)

Rising government debt creates a tempting situation for governments to devalue their currency (print more money) to help pay it off...

Which makes the gold price go up versus that currency.

The US debt situation has become so serious that ratings agency Moody’s just cut the US credit rating overnight for the first time since the year 1919...

Moody’s decision to downgrade, in their own words was down to (Source):

“the increase over more than a decade in government debt and interest payment ratios to levels that are significantly higher than similarly rated sovereigns”

(Source)

The US looks like it wants to devalue the USD to make its domestic manufacturing sector more competitive

We did a deep dive on a potential ‘Mar A-Lago accord’ that could trigger a devaluation overnight...

Read that here: Currency Wars, Commodities, and Small Caps

There is precedent for this type of controlled devaluation - the US did it back in 1985 with the Plaza Accord.

Between 1985-1990 the gold price almost doubled.

The same thing could happen again...

Tariffs, sanctions and capital controls mean the world is looking for safety in new assets outside of the US dollar

An example of this is the world's biggest buyer of US treasuries - China.

Chinese gold buying is currently at record highs - both its central bank and its citizens.

The Chinese central bank for example, has been a net buyer for over 6 straight months.

(Source)

Read more about Gold and Silver in our Ebook Here

Our New KAU Investment Memo:

What does KAU do?

Kaiser Reef (ASX:KAU) is a high-grade gold producer and explorer with projects in Tasmania and Victoria.

KAU’s projects combined produce >25k ounces of gold per annum.

What is the macro theme?

Gold is a precious metal that is often used as a hedge against inflation, which remains persistently high, and the gold price is trading at all-time highs at the time of this memo.

Our Big Bet for KAU

“KAU can grow production at both of its projects in Tasmania and Victoria to >50k ounces per annum. Using that cashflow KAU can fund exploration OR M&A that leads to a re-rate in the company’s market cap to above $1BN”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our KAU Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

Why are we Invested in KAU?

- The gold price is surging

- Two operating assets producing >30k ounces of gold per annum

- KAU is an unhedged gold producer

- Projects have combined infrastructure worth >$100M

- KAU’s processing infrastructure in Victoria is strategically important

- KAU’s plan is to increase production to >50k ounces per annum

- Exploration upside right next to existing infrastructure

- Previous investors/owners have done all the heavy lifting for KAU

- Acquiring big gold assets has worked for other ASX companies

- KAU’s Director of Operations - Brad Valiukas - has experience maximising value from assets like these and is now working full time on Henty and A1

What do we expect KAU to deliver?

Objective #1: Increase production at the Henty mine in Tasmania

- We want to see KAU increase its mining rates as well as increase the capacity of its processing plant to ~400ktpa.

Milestones:

🔲 Increased development rates

🔲 Processing plant improvements

🔲 Production increases above 25k ounces (annualised)

🔲 Production increases above 35k ounces (annualised)

Objective #2: Increase production from the A1 mine in Victoria

- KAU is the first company to be mining fresh, never before touched ground at A1 in over 40 years. We are hoping that means production rates increase well above the rates achieved while mining remnant (leftover) ore.

Milestones:

🔲 Increased development in never before mined areas

🔲 Quarterly production above 2k ounces

🔲 Quarterly production above 3k ounces

🔲 Quarterly production above 4k ounces

Objective #3: Exploration at the Maldon project in Victoria

- We want to see KAU drill out the Maldon project and (fingers crossed) make new discoveries close to its existing 250ktpa processing plant.

Milestones:

🔲 Drilling starts

🔲 Drilling results

Objective #4: Exploration at the Henty mine in Tasmania

- We want to see KAU use its cashflow from the Henty mine to increase the projects resource/reserves and extend its mine life. The ideal scenario would be unexpected NEW high grade discoveries close to the company’s processing plant.

Milestones:

🔲 Drilling starts

🔲 Drilling results

What could go wrong?

Production Risk

The ability of the KAU to achieve production targets or meet operating and capital expenditure estimates on a timely basis cannot be assured.

As a producer, KAU is subject to risks such as but not limited to, labour costs and availability, energy prices as well as KAU’s internal ability to forecast costs like these and budget effectively.

Debt Risk

KAU took out a $10M loan to finance the acquisition of the Henty Mine. Having debt means KAU now has an element of “default risk”.

There is always a chance that KAU isn't able to operate its assets profitably enough to repay its debt. This scenario would re-rate KAU’s share price lower significantly.

Commodity Price Risk

KAU is an unhedged gold producer, meaning all of its production is sold at, or close to, the spot price for gold at any given time. Any material fall in the gold price could hurt KAU’s share price significantly.

Exploration risk

There is no guarantee that KAU’s drill programs are successful, and KAU may fail to find economic gold deposits.

Market risk

There is always the possibility that broader market sentiment gets worse and shares as a whole trade lower, taking KAU’s share price with it. Alternatively, there could be further sector specific pain ahead where junior explorers suffer a lot more than the broader market.

Development/delay risk

Both of KAU’s operating assets are underground mines where decline development work usually determines production rates. Any material delays to decline developments could mean lower production which we think would be a negative to KAU’s current market cap.

What is our Investment Plan?

We are Invested in KAU to see it grow production across its two projects in Tasmania and Victoria.

Our plan is to hold the majority of our position in KAU for 3 to 5 years which we hope is enough time to see KAU materially increase gold production (see “our long term bet” above).

After 12 months we will apply our standard de-risking strategy.

We may look to sell up to 20% of our holding if the company delivers on one or more of our Investment Memo objectives and/or the share price materially re-rates.

Any sell downs will be in accordance with our trading and hold policy disclosure.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.