Energy Transition Metals, Raw Materials, McKinsey, Supply and Demand Economics

Published 12-FEB-2022 10:27 A.M.

|

19 minute read

Our most successful investments over the last two years have been in companies developing the raw materials to build the world’s move to a green energy future.

Raw materials to build electric vehicle batteries, wind turbines, solar panels and power grids - we believe demand for these will surge over the next decade.

Some of our biggest wins have come from companies developing these raw materials to feed the energy transition, like Vulcan Energy Resources (4,635%), Euro Manganese (685%), Evolution Energy Minerals (130%) and Kuniko (395%).

In 2017-18 battery metals companies had a bull run on the expectation of a green energy transition coming - but it turned out to be overhyped and they all came back to earth and nobody cared for a while.

That is just how the markets work, they extrapolate long-term trends into shorter timeframes, and when the thematic takes longer than expected to play out investors become exhausted and move on from the stocks due to a lack of progress.

This time around we think the new energy transition is real and going to play out over the next 10-years, and we are constructing our portfolio to be heavy in the raw materials required to build new energy infrastructure.

All the major car companies are allocating huge amounts of capital to go electric, governments are mandating carbon reduction targets, major resource companies like BHP and RIO are trading at all time highs against other market sectors that are falling.

Over the last 2 years, we have seen the world's largest economies commit to '2050 Net Zero' targets and then seen corporate behemoths follow suit.

Readers who have seen two of our latest investments will know we have been banging on about a research report done by management consulting firm McKinsey & Co titled “The raw-materials Challenge: How the metals and mining sector will be at the core of enabling the energy transition”.

This reports list all the different initiatives that countries have taken to reduce carbon and switch to clean energy, and all the raw materials required.

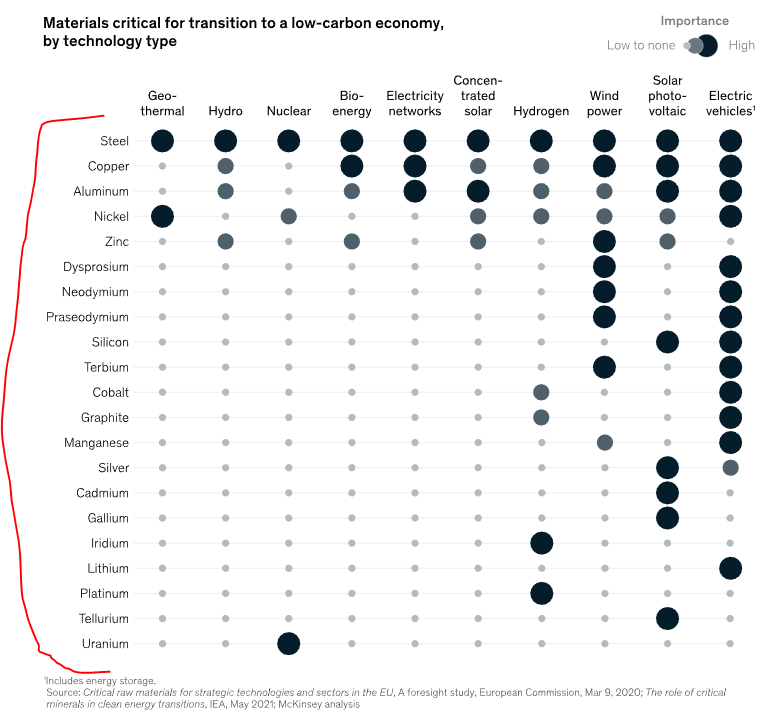

Our goal for 2022 is to gain investment exposure to all the raw materials required for the transition to a low carbon economy.

Think of the below as our “investment shopping list” of what we are targeting for our new energy portfolio:

We have been investing in battery metals for a couple of years so we already have exposure to many of these raw materials (highlighted in yellow below).

Our two latest investments this month have ticked off a couple more raw materials in the chart

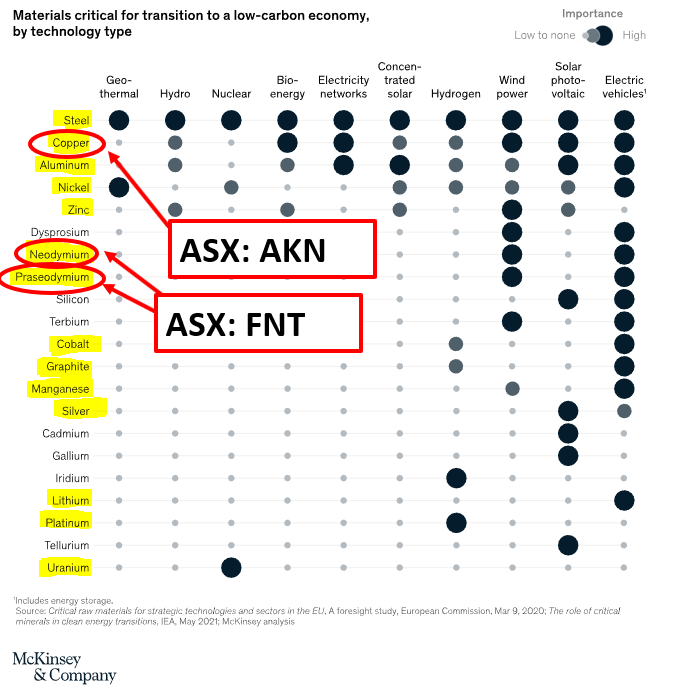

Auking Mining (ASX:AKN) – Established JORC resource copper explorer.

Frontier Resources (ASX: FNT) – Rare earths explorer chasing Neodymium and Praseodymium.

Through Auking Mining (ASX:AKN) we have increased our exposure to copper which has been touted as the “new oil” by Goldman Sachs and through our latest investment announced on Thursday, Frontier Resources (ASX: FNT) we have just added rare earths exposure via Neodymium and Praseodymium to our portfolio.

We plan to launch our latest investment in the Wise-Owl portfolio on Monday morning which will increase our exposure to aluminium.

There is no doubt about the importance of steel and copper, they are used in just about anything that goes through a manufacturing process and doesn’t live on the metaverse.

But we think that the market is under-appreciating the importance of aluminium.

You can see in the McKinsey table that aluminium is heavily used in electricity networks, concentrated solar, solar photovoltaic and electric vehicles (the bigger the ball in the image, the more important the raw material is).

We will announce this new investment on Monday.

This is an ASX stock we ALMOST invested in back in 2020 but decided to wait for the company to deliver a few more milestones before the time was right for us to invest.

We think that time is now.

In the last few months, the company has delivered on these key milestones and we think that the market has completely missed these developments, either because of exhaustion or because the raw material isn’t in the mainstream news as much as say lithium.

We also like this company because it reminds us a lot of our original investment in Minbos Resources (ASX:MNB) (up 400%) in that there has been years of work done on it and lots of investment, it is later stage with a JORC resource and feasibility studies... but like Minbos back in 2020, stale impatient holders who have been on the ride for too many years seem to be depressing the share price.

We look forward to announcing this latest investment on Monday in our Wise-Owl portfolio.

Hint: The company has a Bauxite (Aluminium) Resource in Cameroon...

If you want to see all our current investments in our ‘new energy portfolio’, we have listed them here (just scroll down a bit to see the list):

See all our energy transition raw material investments

Now back to that Mckinsey research report and where those $100’s of billions of dollars in capital expenditure commitments will be flowing into.

Our team has read this many times over so we thought we should put together our takes on the key discussion points that stood-out to us.

1. The transition to a net-zero economy will be metals intensive.

Mckinsey in the report suggests that as the move towards a low-carbon world accelerates the mining sector will be unable to respond to the sheer quantity of raw materials required for the energy transition.

They put this down to two key factors:

- Mining is a capital intensive business

- Building and starting productions in mines takes a long time

This makes a lot of sense, over the last 20+ years mining stocks have been seen as “old economy stocks”. Investors have shunned them in favour of technology stocks which they saw as highly scalable and their way to instant riches.

This dynamic is reflected in the fact that major miner's are resistant to spending on riskier new projects. Almost all of the top ASX-listed miners have shunned making large-scale investments in new mines and instead have paid out their capital to shareholders via dividends.

After all, they need to respond to shareholder demand, and that demand is to give them back some cash so they can pour it into better performing stocks.

The summary is that we have seen decades of under-investment from the major miners and the green energy revolution could expose just how unprepared the world is to meet the raw-material demand that is set to be unleashed over the next 5-10 years.

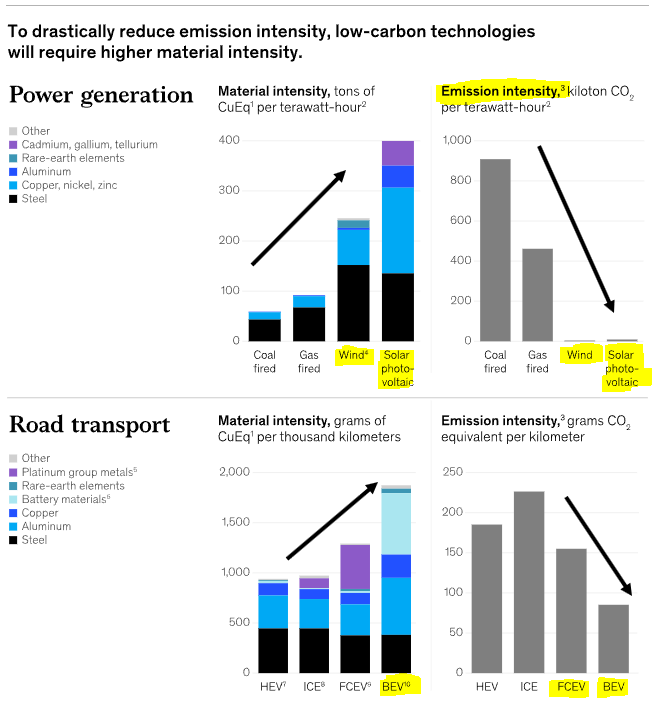

2. Raw materials demand intensity is many multiples higher in a low-carbon world.

McKinsey in the report says that building a low-carbon economy and reducing emissions intensity across various sectors will be materials intensive.

The example they use in the report is that to generate one terawatt-hour of electricity from solar/wind requires 200-300% more metals, versus generating the same terawatt-hour of electricity from a gas-fired power plant.

This might sound counterproductive but even after including the emissions related to mining these materials the emissions intensity across various sectors is drastically reduced.

Basically, for the transition to a low-carbon economy to work, the world needs 2-3x more materials than it would have using older less carbon-friendly technologies.

We definitely haven't seen the supply side react to these projections with 2-3x more capital investment so it will be interesting to see what the market dynamics look like over the next 5-10 years.

Below is the visual representation of what McKinsey are saying:

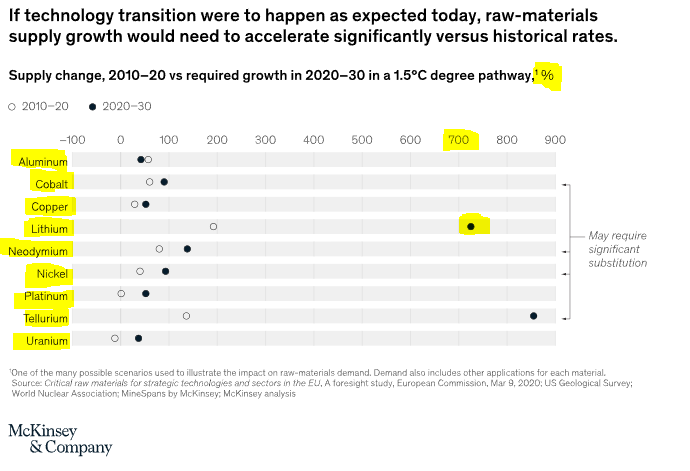

3. Can supply react to this demand quickly enough?

McKinsey in their report doesn't think so.

They use the example of lithium mines, which need to increase by 7x from today’s required growth levels and metals with an even smaller supply like tellurium would need to grow even faster.

As if those numbers aren’t shocking enough, McKinsey also estimates that for copper and nickel alone, the miners globally would need to invest between $250 billion and $350 billion by 2030 to grow and replace the depletion of EXISTING capacity.

The below chart shows in terms of % how much current supply would need to change versus where it is today. That lithium number is especially damning.

4. Price incentives to drive investment decisions.

McKinsey also outlays a theory that for there to be a supply-response and for the big miners to make large-scale investments into new supply prices would need to remain elevated for longer periods of time.

McKinsey in the research report uses copper and nickel as an example, citing consistent copper prices of more than $8,000-10,000 (US$4.50/lb+) metric tonne and nickel above $18,000 (per metric tonne) over long-time horizons would be needed to entice investment in new supply.

With nickel currently trading at US$24,000/tonne and copper at US$4.50/lb we are seeing the early stages of this type of price movement.

The interesting thing is, we are yet to see capital pour into building new mines. The major miners are still busy using their excess cash reserves to pay large dividends and large-scale projects are still not progressing through to construction.

We expect these prices to continue higher until finally, these projects get off the ground, with a large mine taking 5+ years to build. We expect the commodity prices to overshoot and go to levels even we didn't expect.

This all fits in with the commodity supercycle investment theme we have been basing a large part of our investments around.

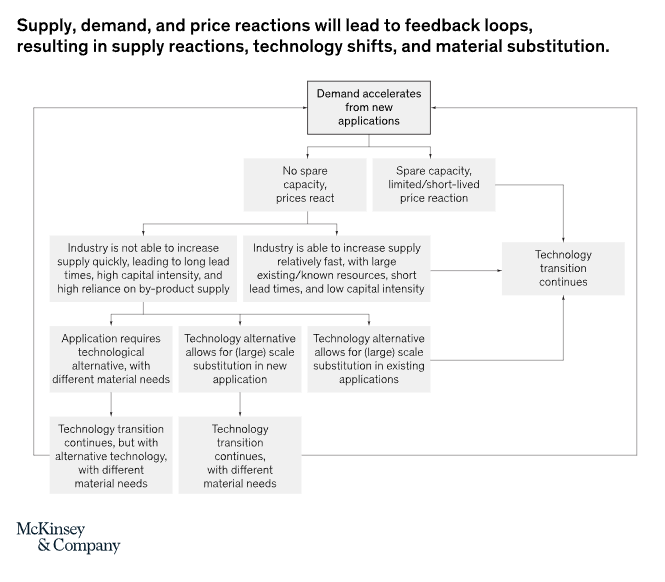

5. How market balance is achieved.

McKinsey ends the report by laying out a framework for how this critical raw materials shortage mess is sorted.

They expect to see:

- Supply responding to prices

- Demand accelerating, prices reacting strongly and substitutions being found via innovation.

We think the first part of this is a given.

The only way supply will respond is if prices increase and we are already seeing the first stages of this with lithium prices at all-time highs, copper near all-time highs, and nickel near all-time highs.

As for the second part, we aren't so sure.

Relying on innovation to get us out of this is seriously optimistic, and it is hard to bet against human ingenuity but we think the fundamentals need sorting out before we can lay our hopes in innovation.

Finding substitutes for steel, copper, aluminium, or lithium is not going to be a walk in the park.

Below is McKinsey's framework as a flowchart.

We expect the world to be playing catch up over the next decade or two on decades of underinvestment in the things physical humans need to survive.

Raw materials.

If you want to see all our current investments in our ‘new energy portfolio’, we have listed them here (just scroll down a bit to see the list):

See all our energy transition raw material investments

📰 This week on Next Investors

It had been a while since we covered Thomson Resources (ASX:TMZ), and what better time to launch the 2022 Investment Memo for TMZ than in line with TMZ’s promising results from metallurgy studies revealing substantial improvement on historical recoveries.

Often overlooked by investors, metallurgy or “met work” is a critical part of mine development and it feeds directly into the project’s economics.

In this article we provide a refresher on TMZ’s ‘Hub and Spoke’ development strategy and a deep dive into the met work recoveries announced by TMZ.

📰 Read Now: TMZ Pressing Ahead with Highest Grade Undeveloped Silver Project in Australia

Back in November 2021, early stage metals exploration company Galileo Mining (ASX:GAL) unexpectedly hit shallow massive sulphides that its AC drill bit could not penetrate at its Norseman Project.

This was positive news, and GAL decided to immediately run some EM surveys around this part of the project to try to understand what this hard rock could be.

The results of this anticipated EM surveying came through on Wednesday and showed that GAL had found TWO highly conductive EM targets of interest.

📰 Read the full breakdown here: AC drilling followed by Strong EM Conductors Under Massive Sulphides - Next Stop RC Drilling

🏹 Catalyst Hunter

On Thursday we launched our latest investment in a sector that we have been looking at for quite a while now.

We announced our initial investment in Frontier Resources (ASX:FNT) which is exploring for rare earths primarily in the Gascoyne region of WA.

FNT’s ground is located directly either side of ~$500M market capped Hasting Technology Metals’ which owns the highest grade NdPr rare earths project listed on the ASX. With a recent $140M loan from a Federal Government Fund Hastings is planning to have its project producing in 2023.

In addition to being next door to Hastings’, FNT’s tenements also border those of Dreadnought Resources, another explorer - which is capped at ~$122M - over four times the size of FNT.

In our launch note we did a deep-dive on the macro-tailwinds behind rare earths and why FNT’s project’s nearology was interesting enough to warrant our investment.

Follow up note: FNT released its EM targets yesterday, which provides a good basis for drill targets - you can read the ASX announcement here.

📰 Read the full breakdown:Our Latest Investment: Rare Earths Exploration

🗣️ Quick takes:

88E: Merlin-2 permit granted and capital raise launched

On Thursday 88E announced that the drilling permit for the Merlin-2 appraisal well was granted.

This has been a long time coming after some issues with environmentalist groups in Alaska related to the polar bear settlements around 88E’s leases.

We mentioned in a previous weekend update that we didn't expect this to be an issue especially given one of 88E’s neighbours, AIM listed Pantheon Resources, getting its permit granted earlier in the year.

We also note that 88E went into a trading halt pending a capital raise with the company expected to come out of its halt on Monday.

It will be interesting to see how much cash was raised and whether or not 88E will be going it alone on the Merlin-2 well instead of having to look for a farm-in partner.

This was the final step before 88E can go in and actually drill the Merlin-2 well and our primary objective in our 2022 investment memo.

IVZ: Well services contract awarded

On Friday IVZ announced that a letter of intent had been signed with Baker Hughes for an integrated well services contract.

The contract covers everything from cementing, mudlogging, drilling fluids and general project management. Basically it is for everything except the drill-rig.

Baker Hughes is one of the world's leading oilfield service providers operating in more than 120 countries worldwide with over US$21 billion in revenues. We think the appointment of Baker Hughes is a great move by IVZ, considering all of the experience they will bring to the drilling team.

This week's announcement moves IVZ one step closer to achieving the primary objective of our 2022 investment memo, with all of the right boxes being ticked leading upto drilling.

GGE: Drilling permit application lodged (Catalyst Hunter Portfolio)

GGE is now one step closer to drilling its first well of its Red Helium project - Jesse#1, lodging an application for a permit to drill with the Utah Division of Oil.

Although this seems like a box ticking exercise, permit delays do happen and can derail a company’s ambitions. Blue Star Helium for example took 13+ months to secure its permit for drilling, frustrating investors and delaying the project.

We don’t anticipate it to take anywhere near as long for GGE, with a 60-90 day timeframe suggested.

This is because GGE’s project is located in the permit friendly state of ‘Utah’ on private/state leases, whereas Blue Star Helium’s drilling was located on federal leases in the non-friendly permitting state of Colorado.

EMN: CAD$8.5M Placement complete

Yesterday EMN closed a C$8.5M placement with the European Bank for Reconstruction and Development (EBRD) at CAD$0.4775¢ first announced in January.

The EBRD supports private sector infrastructure projects around Europe and is a strong partner for EMN.

It is the first placement to come out of the EIT InnoEnergy relationship and hits on three of our four objectives in the 2022 EMN Investment Memo.

The funds will be used to advance both Objective #1 ‘Construct Demonstration Plant’ and Objective #2 ‘Complete Definitive Feasibility Study’ - while if the relationships with EBRD matures, it could set the foundations for project financing (Objective #4).

TMR: Blue Vein Assays Announced

Early in the week TMR announced another batch of assay results from the latest round of drilling at its Canadian gold project.

The key for us was the intercept made on hole EZ-21-27 which returned 1.4m @14.31g/t gold and EZ-21-26 which returned 1.25m @9.13g/t gold.

Both of these intercepts were to the northeast and southwest of the already known part of the “Blue Vein” discovery which we think is the key for TMR to get this project back into production.

With these two results, it is starting to look like the “Blue Vein” may be more akin to the historically mined SW Vein. We compared the two and discussed the drilling being done to extend the “Blue Vein” in our last note on TMR which provides great context for these latest results.

These results show TMR is making progress towards the first and second objectives we set for TMR in our 2022 investment memo, which was to make more discoveries and consequently increase the JORC resource of the Canadian gold project.

DXB: New chief medical officer appointed

On Monday DXB announced the appointment of Dr. Ash Soman to lead the company’s multiple global clinical development programs.

This is a pivotal time for DXB, with three phase-III clinical trials currently underway, and bringing a highly experienced clinician with 30-years in the medical field is the right move to oversee these programs.

Dr. Soman will start with DXB sometime around mid-April.

FYI: Results from HPA anode coatings program with EcoGraph (Wise-Owl portfolio)

During the week, FYI and its graphite partner EcoGraf announced that its high-purity alumina (HPA) anode coatings program had delivered “outstanding results”, generating coatings that met the tech specs of leading battery manufacturers.

The results demonstrated that the electrochemical performance of the HPA-doped coated anode in lithium-ion coin cells achieved higher first charge capacity, reduced first cycle loss and increased battery charge efficiency.

These results indicate that HPA could be used in the anode for batteries increasing its uses and thus demand.

On the results, FYI’s MD commented: “We are particularly encouraged by the out-performance of our developed anode technology In relation to the current market leader.”

LRS: Drill rigs arrive at Brazilian lithium project (Catalyst Hunter)

Early in the week LRS announced that two drill rigs had arrived on site at its lithium project in Brazil.

The drilling program is a 14-hole 2,000m diamond drilling program that is designed to follow up the previous pegmatite sampling program. The sampling program returned lithium grades between 1.45% and 2.71% lithium over a 1.2km strike length.

We don't usually place too much emphasis on rock-chip sample’s when identifying drill-targets but given this is a part of Brazil where CAD$1.3 billion TSX listed Sigma lithium is active, any discovery could get the market extremely interested.

We are yet to launch our investment memo for LRS, but expect this to get done very soon, so be on the lookout for this.

AOU: IP survey brings up new drill targets (Wise-Owl portfolio)

On Thursday AOU announced that the IP survey being completed over the Nepean Nickel project had been completed and that high priority drill targets had been identified.

For us, the Nepean Nickel was the most interesting of AOU’s projects.

With the IP survey identifying anomalies over 16 of the 19 survey lines AOU has already put together a programme of works application to conduct a 3,000m RC drilling program.

Of this 2,200m will be dedicated to testing the newly found targets and the remaining 800m testing three shallow gold targets to the south of the Nepean project.

🌎 Mainstream Media:

Rare Earths

Clean energy transition to fuel growth for China's rare earths sector in 2022 (S&P Global)

Green Energy / Hydrogen

‘Cutting through the greenwash’: Australian energy retailers ranked on climate action (The Guardian)

Hydrogen market is coming sooner than you think – ANZ (AFR)

Investing in Hydrogen: A great opportunity or playing with dynamite? (Livewire Markets)

Fortescue unveils vast WA renewables hub (AFR)

Billions to transform the Pilbara: WA’s hydrogen hubs plan revealed (WA Today)

Renault-Nissan $26B electric push deepens platform, production cooperation (Automotive News Europe)

Cybersecurity (WHK)

Microsoft Considers Pursuing a Deal for Cybersecurity Firm Mandiant (Bloomberg)

US Nursing Crisis (ONE)

U.S. Hospitals Complain Nurses Making Too Much Money During COVID-19 Pandemic (Gizmodo)

Travel Nurses Make Twice as Much as They Did Pre-Covid-19 (WSJ)

Lithium (VUL, EMH)

Where Is There More Lithium to Power Cars and Phones? Beneath a California Lake. (WSJ)

Norway Battery Metals (KNI)

EV Sales Hit Record in Norway With Fossil Engines Soon Gone (Bloomberg)

Semiconductors (GGE)

EU punts $70b into making chips in Europe (AFR)

Investing

John Doerr & Ryan Panchadsaram of Kleiner Perkins + VC Sunday School: cap table management | E1379 (YouTube)

Why the impressive pace of investment growth looks likely to endure (The Economist)

Have a great weekend,

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.