Is it Bull o’clock yet?

Published 18-AUG-2024 19:04 P.M.

|

20 minute read

- Commentary: Pilbara Minerals takeover offer for LRS. The “crash to boom” clock and other potential takeover targets in our Portfolio (in our opinion).

- Quick Takes: SGA, NTI, MNB, EMD

- This week in our Portfolios: SGQ, MNB, NTI, L1M, EXR

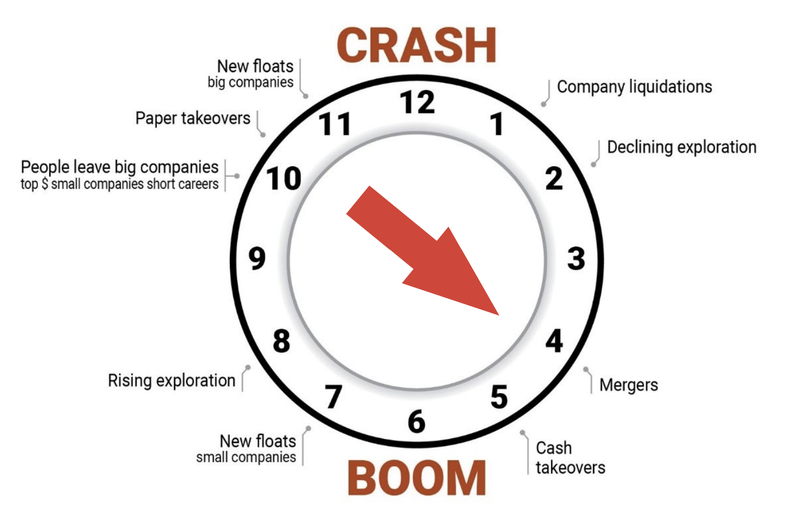

Markets move in cycles.

Right now, in the ASX small cap market, it feels like we are still firmly in “bear” mode.

Equities prices have collapsed, liquidity too...

But there have been signs that the gears on the crash-boom clock are turning ever closer towards “bull” mode.

That sign is an increase in M&A - Mergers and Acquisitions.

Here’s where we are on Lion Selection Group’s market “clock” for junior resource investments:

(Source)

M&A is a good “bottom of the market” sign, as it means that established companies with big balance sheets see real value in oversold stocks.

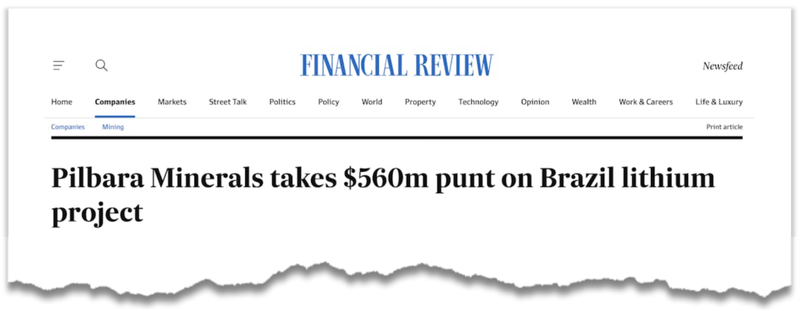

This was a big week for M&A, particularly in our Portfolio with $8.5BN Pilbara Minerals announcing a bid for Latin Resources (ASX:LRS) at a ~$560M implied price.

We think this is a win-win kind of deal.

Pilbara Minerals looked at over 100 different projects globally and chose LRS’s asset as the best undeveloped, low cost hard rock Tier 1 asset on the planet.

The acquisition can diversify Pilbara Minerals from “WA lithium selling to China” to having an asset much closer to the USA market.

As for LRS, while they are confident they could ‘go it alone’, raising CAPEX funding at the moment is hard.

We’ve seen it across the market.

Being a much bigger company, the $8BN capped Pilbara had $1.6BN cash at the end of last quarter, would make getting this funding and then into production significantly easier.

Our Initial Entry Price for LRS was 1.8 cents.

To see a proposal from Pilbara Minerals, one of the biggest hard rock lithium producers in the world, at an implied share price of 20c is pretty incredible to see.

In the current cycle of low market interest for explorers, LRS has been single handedly doing all the heavy lifting in our early stage explorers Portfolio (Catalyst Hunter).

It’s the holy grail of exploration Investment to see a company make a discovery and eventually get acquired at multiples of your entry price.

It doesn't happen every day, so we feel proud to have been early backers of LRS into that discovery hole back in 2022.

In these tough times for mineral exploration it’s a good morale boost and reminder of why we hold on and continue to Invest in exploration stocks - because these kinds of wins can and do happen sometimes.

And exploration always eventually cycles back into favour.

As we noted above, we think this is an excellent deal for LRS and its shareholders and echo the sentiment of LRS’s Managing Director Chris Gale that LRS is swapping “very good undervalued paper” in LRS shares for “excellent undervalued paper” in Pilbara shares.

We think Pilbara Minerals is one of the highest quality lithium exposures in the world.

It's our view that in the long run IF the lithium industry outperforms, Pilbara will continue to be one of the biggest in the industry.

See 43:36 of the following investor webcast for Chris’ take (and in fact the whole webcast is worth a listen if you have the time):

(Source - this link will take you directly to Chris’ comments)

A few months back one of us actually visited Salinas with our early stage Investment L1M (more on that below).

During the trip we had the opportunity to spend some time with the LRS Brazil team.

We saw the quality of the asset, the high calibre team, and the good work LRS is doing on community and social engagement in the town.

Once again, congratulations to Chris and the LRS team.

As we noted above, with Pilbara Minerals as owner-operator, it would mean LRS’s Colina project can be funded through to production much easier than it would have been if LRS went it alone.

In addition to LRS’s asset itself, the proposed acquisition is a very strong validation of Brazil and its potential to become a big player in the lithium industry.

We think that Brazil’s ability, and in particular the state of Minas Gerais, to work with mining companies to fast track the approval process was one of the key reasons for Pilbara’s decision.

We are very comfortable with Investing in Minas Gerais, and Pilbara Minerals is too.

(In fact our most recent Portfolio addition St George Mining (ASX:SGQ) is also in Minas Gerais. SGQ is acquiring an advanced stage niobium and rare earths project in the state)

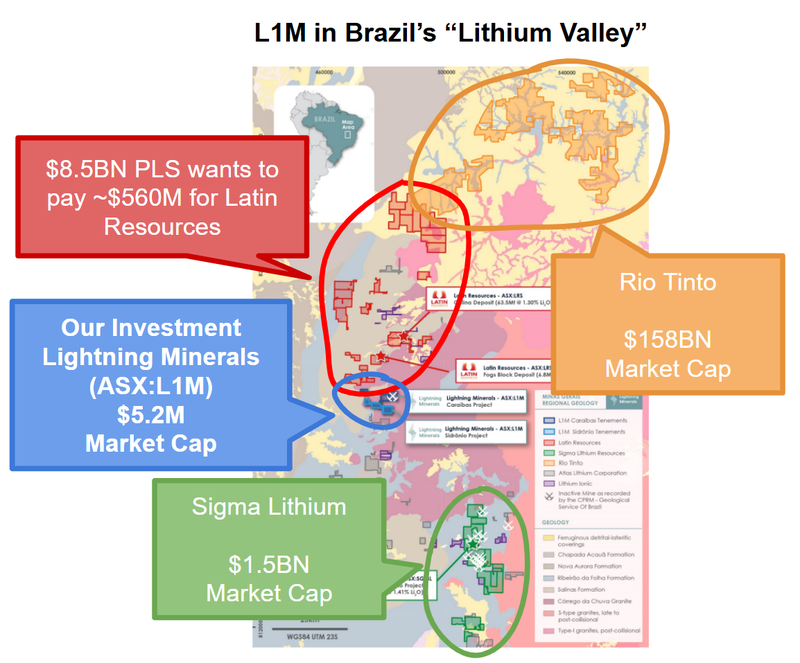

Following our successful LRS Investment, we Invested in another small cap lithium explorer in Minas Gerais, the ~$7M capped Lightning Minerals (ASX:L1M).

We Invested in L1M to hopefully deliver us a similar outsized “LRS style” result.

L1M has been picking up prospective lithium ground near Latin Resources and producer Sigma Lithium.

L1M is exploring for lithium while it is temporarily out of favour, which is a little similar to the approach of LRS in the “pre-discovery” years in 2019-2020.

Here’s where L1M’s lithium ground sits and its proximity to the big companies in Brazil’s Lithium Valley:

(note: L1M market cap now ~$7M)

The lithium industry in Minas Gerais is a fraction of what we think it could be.

Production is only really just getting started, and just like Western Australia spawned several new major discoveries in the previous lithium bull market, we think there will be a lot more lithium to be discovered in this part of the world in the next upcycle.

With a bit (a lot) of luck, hopefully L1M is one of the companies that makes a discovery.

It's very early days though (and we are patient) - you can read more about this in our note from this week on what the Pilbara Minerals LRS takeover might mean for L1M.

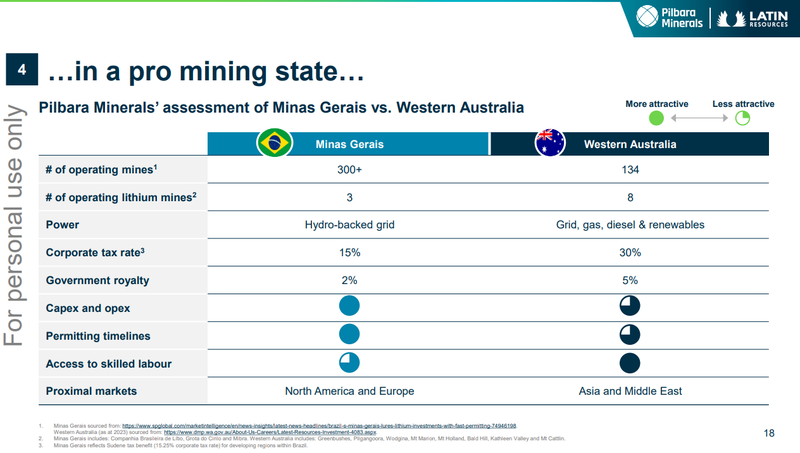

The following slide from the LRS-Pilbara deal deck lays out a comparison of Minas Gerais vs Western Australia when it comes to lithium mining:

(Source)

Scanning the above comparison - it starts to make sense as to why Pilbara Minerals chose to diversify into Minas Gerais from WA.

(and is positive to know for our other Minas Gerais Investments L1M and SGQ).

Another big M&A deal that was announced this week was over on the TSX with Gold Fields reaching an agreement with Canadian miner Osisko in a US$1.57 billion all cash deal to have full ownership of the Windfall project (we don’t own shares in either of them):

(Source)

Two weeks ago BHP made a $3 billion play for Argentinian copper assets...

... and the M&A space remains strong across both biotech and tech sectors.

Given we are at this stage of the cycle and a few deals are popping up, we thought it timely to run through our Portfolio and see which other stocks have M&A potential.

Before reading - please note this is simply our opinion based on some factors we consider that could make a company an attractive acquisition target at this given time.

There is no information to suggest that any of these companies are in any M&A discussions.

Also, this is just a small selection of the stocks in our Portfolio and is by no means definitive.

It’s always possible that any other stock in our Portfolio could attract the interest as a corporate target - that's what keeps investing exciting...

Here are 6 stocks that we think could attract M&A interest in the next 12 months... and why

Arovella Therapeutics (ASX:ALA): $158M market cap

ALA is our “preclinical” biotech Investment, operating in the cell therapy space to beat cancer.

We say preclinical, but it is getting closer to becoming a clinical stage biotech, with Phase 1 trials getting closer.

ALA's latest presentation says it intends to dose its first patient in this FY (Source) and will submit an FDA Investigational New Drug (IND) Application in early Q1 2025 - read our Quick Take).

ALA is developing an off-the-shelf cancer killing cell therapy.

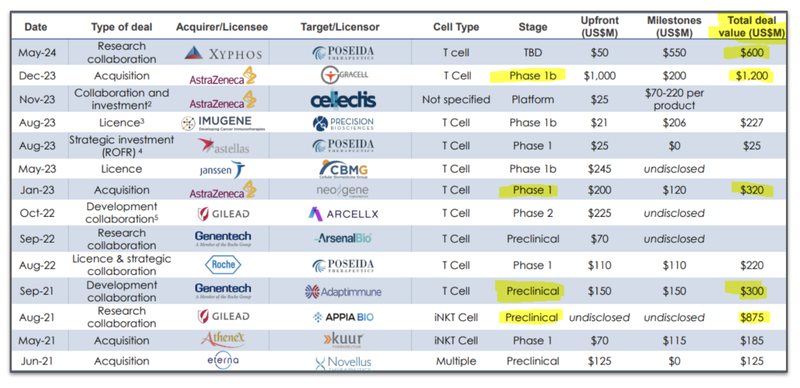

We think ALA could be the target of M&A activity as the cell therapy space has seen a significant amount of deals in recent years.

There are some big price tags attached to early stage treatments too:

(Source)

In recent months, ALA itself has made some acquisitions, identifying key bolt-on tech to improve its cancer killing platform.

Recently, ALA cracked an important cell therapy manufacturing milestone - the scale up of the manufacturing process making it suitable for large-scale and late-phase clinical development.

Manufacturing is often the bottleneck for mass production for any cell therapy platform - perfecting the manufacturing can take time and cause delays to the project.

In order to run clinical trials, ALA needs a stable treatment that can be manufactured consistently and repeatedly.

With this milestone ticked, ALA is now very close to being able to take its iNKT cell therapy technology into the clinic for Phase 1 trials.

We think that this data could set the stage for ALA to potentially be acquired by a big pharma company that is looking to add to its cell therapy pipeline.

NeuroTech International (ASX:NTI) - $72M market cap

Sticking to the biotech space, we think that NTI is another company that is positioning itself for dealmaking.

NTI is developing treatments for both rare and large total addressable market neurological diseases in children.

In the last 12 months NTI published promising clinical trial results for three different conditions: PANDAS/PANS, Rett Syndrome and Autism Spectrum Disorder.

Just this week NTI announced its product strategy and how it plans to best develop its treatment both locally in Australia and globally in the US, Europe and Asia.

Central to the strategy was “strategic partnering”.

NTI intends to find a partner that will support the development of its promising assets through clinical trials overseas.

It makes sense that NTI is now in deal mode, because it can take the data that is very promising and find a partner with a robust balance sheet to take the product through to commercialisation.

NTI specifically mentioned this week that it would look for deals in the US, Europe and Asia which basically covers most of the biggest global markets for big pharma companies.

NTI had $11.6M cash in the bank at June 30th, and is well funded for its Australian work and means it has the runway and flexibility to talk to offshore partners without requiring to raise additional capital in the near to medium term.

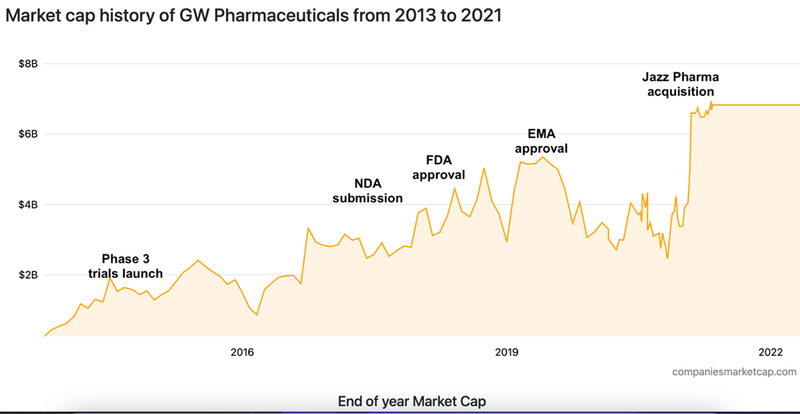

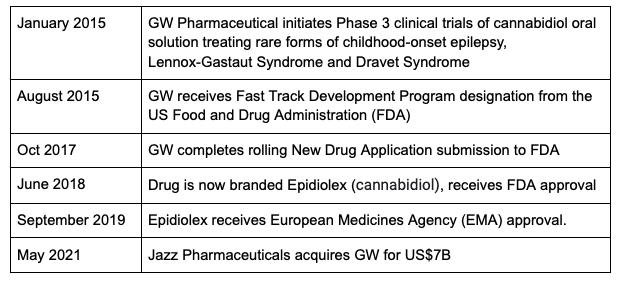

A good model for NTI is the GW Pharmaceuticals story.

GW Pharmaceuticals was acquired by Jazz Pharmaceuticals for US$7.2BN primarily for its (cannabinoid) epilepsy medication Epidiolex in 2021:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Note that it still took over three years from Phase 3 trials in 2015 before Epidiolex received FDA approval.

In that time, GW’s market valuation grew from ~US$1.3BN to US$2.9BN, before Jazz Pharmaceuticals acquired the company for US$7.2BN in 2021.

We’re patient here - and we’re hoping NTI can follow a similar trajectory.

On Wednesday we released our new NTI Investment Memo which you can read here:

NTI clinical data in hand - now entering “deal making” mode.

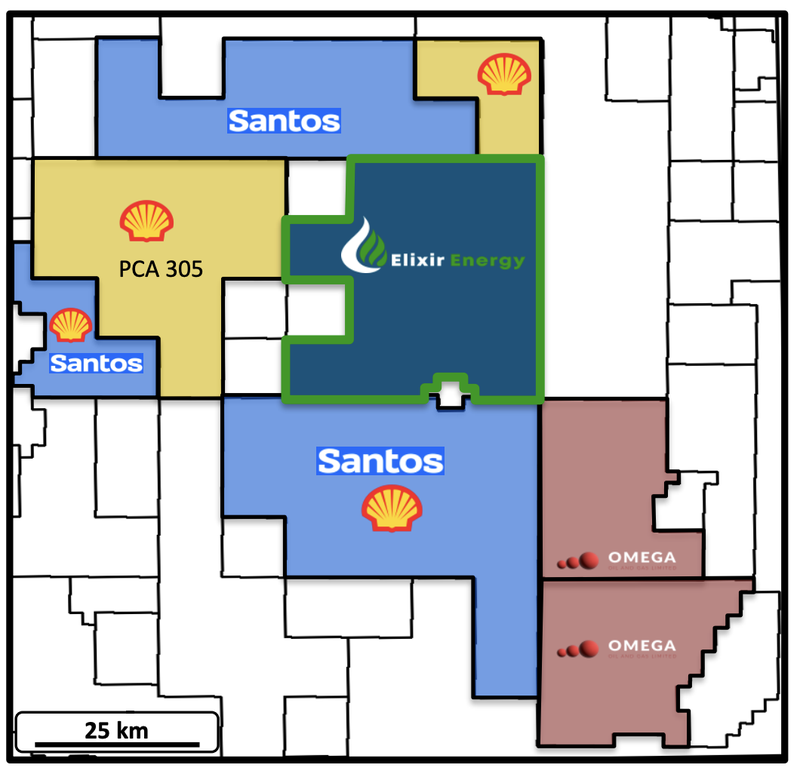

Elixir Energy (ASX:EXR) - $143M market cap

Yesterday EXR published a set of flow test results from its Queensland gas project.

EXR delivered a stabilised flow rate of 2.5 million standard cubic feet of gas which is right at the threshold which EXR believes makes its project commercially viable.

The upside is there are still several other zones of the well to flow test which means that flow rate could get even bigger in the coming weeks.

We think the flow rate news is a significant de-risking event for the company, and a potential signal for bigger players looking for de-risked east coast gas exposure.

The stronger the flow rate - the more attractive the project becomes overall.

EXR’s project sits next to existing gas power plants, pipeline infrastructure and underutilised LNG export capacity.

All of these, we think, add to the attractiveness of EXR’s project.

The project is right next door to Shell and Santos, as well as Omega who is backed by Tri-Star group (a private company owned in part by the billionaire Flannery family).

We covered the EXR flow test news in detail here: EXR delivers commercial gas flow rates - 5 more zones still to be tested.

This Taylor Collison research report is also a pretty good read to get up to speed with EXR (released prior to yesterday’s news): Elixir Energy Limited (ASX:EXR) Taylor Collison Report.

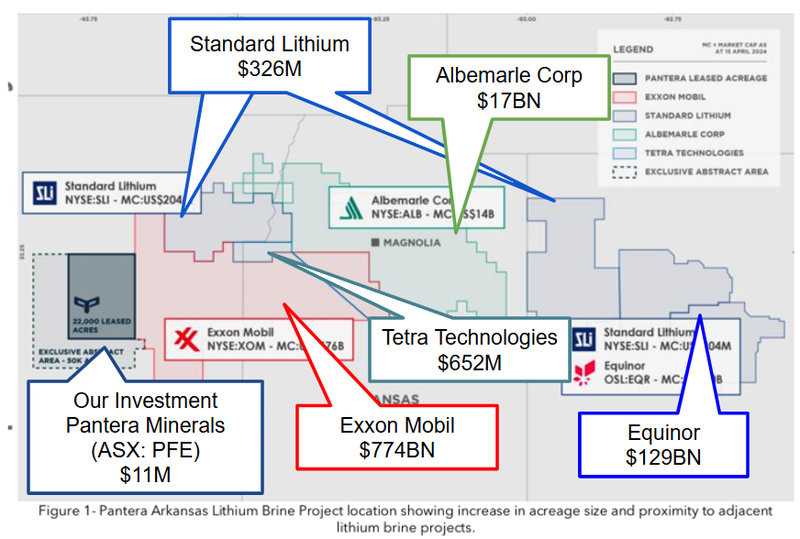

Pantera Minerals (ASX:PFE) - $9.2M market cap

PFE is the only ASX listed small cap with lithium assets in the Smackover region in the USA.

The Smackover is where Exxon, Equinor, Albemarle and Standard Lithium are all actively developing lithium brine assets.

Exxon recently drilled wells in the area and is looking to make Smackover the centre of its lithium business.

PFE has been picking up ground pretty aggressively and is positioning itself right in and amongst the bigger players.

Over the next six months, PFE plans to re-enter an old oil and gas well, sample for lithium, and upgrade its exploration target into a maiden JORC resource.

We think the JORC resource estimate will be a major share price catalyst for PFE because it will de-risk the company’s project from an exploration perspective.

With a JORC resource in hand, it means that larger players could step in like Exxon or Equinor to consider the project as an acquisition target.

If PFE is not already on the radar of the players in the region we expect it to be soon as it gets closer to a re-entry program on its ground and then, all going well, publishing its JORC resource.

Oneview Healthcare (ASX:ONE) - $243M market cap

ONE is our most successful tech Investment, and it's one of our best ever investments across all categories considering how well it is holding its gains.

ONE develops and sells software/hardware to hospitals and has been in our Portfolio since 2022.

The reason we think ONE is interesting from an M&A perspective is because of its recent deal with Baxter, the US$35BN NYSE listed company that sells equipment into the majority of the US hospital market.

ONE and Baxter have signed a “value added reseller agreement” and there are early signs of traction.

In ONE’s quarterly report published a few weeks ago the company announced that a second Purchase Order has been received from the Baxter Partnership.

In addition, the partnership has seen a 24% uplift in qualified leads.

The partnership is still very new, but it appears that this early traction will only grow as time goes on.

ONE also recently shifted to a Bring Your Own Device (BYOD) business model, where it is more of a software than a hardware product.

(this was always a friction point for ONE, hospitals move slowly to upgrade technology and a hardware product was a difficult sell).

This business model change, coupled with the Baxter deal could provide a significant step change for ONE’s revenue in the next few years.

Ultimately ONE’s excellent progress over recent years could catch the eye of a bigger company looking for a neat bolt-on acquisition.

Genmin (ASX:GEN)

GEN is currently trying to lock in project financing to get its iron ore asset in Gabon into production.

GEN’s iron ore project already has all of the permits in place, offtake MoUs with Chinese steelmakers and a project DFS.

GEN is chasing US$200M in CAPEX with the goal to get into production next year (at a US$391M NPV).

However, the iron ore price has not been very favourable over the past 6 months, reaching its lowest point since 2022 and under US$100/t.

And yet, this project is about as "ready to go" as possible.

The major shareholders of the company are Tembo Capital (an experienced private resources fund) and GEN has been developing the asset for more than 10 years now in conjunction with Tembo Capital.

If the iron ore share price was running, then it would be easier for GEN to get through to production.

However, given where the iron ore price is today we think a deep pocketed player with a long-term vision for green iron ore (the product that GEN's project has) could come out of the woodwork.

Generally, when acquiring a large later stage mine, the daily price movements of commodities are not as relevant (even though we like to think so as retail investors).

And Tembo Capital has a successful track record of developing advanced stage assets like Paladin Energy - which it took from administration through to a $3BN capped company.

So we think that Tembo Capital, along with GEN board member John Hodder (who is a managing director at Tembo), and the wider GEN board and management team could be able to close an appealing M&A deal for the project.

Note, this is just us "thinking out loud" - there is no guarantee that any of this actually plays out.

M&A news can come at any time

We like to Invest in early stage companies, when risks are higher but there are greater rewards for successful outcomes.

As each of our Investments progress they gradually will de-risk their assets through more drilling, more sales or more clinical trials.

At some point this work can become attractive to a bigger company with deeper pockets who can take the asset to the next level in a win-win scenario.

By the stage that there is M&A interest we are hoping that we are up significantly on our Investment, like with LRS.

But M&A can come at any time.

Almost all companies talk to the majors at one point or another, and these conversations don’t really go anywhere 99% of the time.

However, it sometimes happens that a company catches lightning in a bottle and gets a deal done.

Sometimes, the smallest macro development can derail months and months of work on a deal - that's just how touch and go these things are.

BUT because these deals can come out of nowhere for any company it means that share price re-rate could always be lurking around the corner.

What we wrote about this week

St George Mining (ASX:SGQ)

Last week, we added St George Mining (ASX:SGQ) to our Portfolio and participated in their capital raise at 2.5c per share, anticipating that their advanced niobium and rare earths project in Brazil will be significantly revalued by the market.

SGQ initially went up on the news, and then down, then went into a trading halt for a few days, and emerged from the halt to respond to misinformation in the market. SGQ’s response reinforced our confidence in the long-term potential of this project.

With a market cap of $55M post-transaction, SGQ is in a position to capitalise on the growing market interest in niobium, especially with its project located next to the world’s largest niobium mine.

Read: SGQ confirms that anonymous person on internet chatroom is wrong

Minbos Resources (ASX:MNB)

Minbos Resources (ASX:MNB) is close to finalising the financing needed to build its phosphate mine in Angola, with production expected by 2025.

MNB recently announced that the Angolan Sovereign Wealth Fund’s board approved a US$10M investment in MNB.

This was a key step toward unlocking a US$14M loan from the IDC of South Africa.

With only the US$14M term loan and converting an existing offtake MoU into binding, MNB is nearly fully funded to begin construction.

Unlocking the CAPEX means MNB can move into phosphate production, where it is aiming for US$55M in average annual EBITDA over a 20-year mine life.

Read: Sovereign Wealth Fund to invest US$10M in MNB... at a premium to current price

Neurotech International (ASX:NTI)

Neurotech International (ASX:NTI) is focussed on developing its lead therapeutic agent NTI164, and demonstrating its effectiveness in treating multiple neurological disorders in children.

NTI announced its forward strategy earlier this week, after delivering multiple successful clinical trial results in recent months.

With $11.6M in the bank, NTI plans to seek a global partner to fund additional clinical trials and navigate regulatory pathways in the US, Europe, and Asia, while simultaneously progressing towards provisional approvals in Australia.

Securing a commercial partner could be a major catalyst, potentially mirroring past success stories like Neuren Pharmaceuticals, which significantly boosted its market cap through strategic licensing deals.

Read: NTI clinical data in hand - now entering “deal making” mode

Lightning Minerals (ASX:L1M)

Pilbara Minerals' proposed $560M takeover of Latin Resources underscores the growing corporate interest in Brazil's "Lithium Valley".

All of Lightning Minerals (ASX:L1M)’s lithium ground sits between the two biggest hard rock listed lithium companies in Brazil in Sigma Lithium and Latin Resources, in similar geology.

AND similarly to LRS, L1M is picking up its ground at the depths of a lithium bear market when no one is really paying attention... (actually this might change given the Pilbara Minerals news...)

We are backing L1M’s counter cyclical approach to building up its land position in Brazil’s Lithium Valley. As the majors (like Pilbara Minerals and Rio Tinto) move into the region, we think the look through value in L1M’s assets should only get stronger.

Next we will be looking out for L1M to identify their best drill targets and eventually try to drill a discovery of their own.

Elixir Energy (ASX:EXR)

This week Elixir Energy (ASX:EXR) achieved a stabilised commercial flow rate of 2.5 million cubic feet of gas, with a peak flow of 3.5 million cubic feet, from a single zone on its Queensland gas project.

This new flow rate is nearly double the initial unstimulated rate and comes as EXR prepares to test five more zones over the coming weeks.

The project’s proximity to major players like Shell and Santos and its location near key infrastructure enhances its potential value.

If further zones also deliver commercial rates, it could confirm the project's viability as a significant Australian gas development.

Read: EXR delivers commercial gas flow rates - 5 more zones still to be tested

Quick Takes

SGA Pre Feasibility Study released

NTI lays out partnership & registration strategy

MNB US$10M investment from Sovereign Wealth Fund

FDA knocks back approval for MDMA-assisted therapy

Macro News - What we are reading & listening to

Biotech:

Big Drugmakers Are Clinching Smaller Deals (WSJ)

- Major drugmakers are now favouring smaller acquisitions, often below $5 billion, due to regulatory challenges and a saturated market, shifting from the large deals seen in recent years.

- In 2024, all 17 deals by big pharma were under $5 billion, with a notable increase in acquisitions of privately held companies compared to last year.

Billionaire Salesforce boss tips into Sydney biotech incubator (AFR)

- Proto Axiom, a Sydney-based biotech investment incubator, has raised $20 million in a Series B funding round, valuing it at $90 million, with notable investors including Salesforce boss Marc Benioff and Ajay Banga.

- The incubator aims to invest in early-stage biotech ventures and university spin-outs, with plans to deploy the new $30 million fund over the next two to three years.

Gold:

Gold Fields to buy Canadian miner Osisko in $1.57 billion cash deal (Reuters)

- Gold Fields Ltd will acquire Osisko Mining for C$2.16 billion, paying a 55% premium per share, to expand its presence in the Americas and gain full control of the Windfall Project in Quebec.

- The deal, funded by cash and bank facilities, caused Osisko's shares to jump 63% and Gold Fields' shares to fall 5.6%, with concerns about execution and funding risks for the Windfall project.

Hydrogen:

Why Almost Nobody Is Buying Hydrogen, Dashing Green Power Hopes (Bloomberg)

- Hydrogen production projects are booming globally, but most lack binding customer agreements, with only 12% having secured buyers for their fuel.

- Successful projects are those with integrated ecosystems, combining local clean energy sources with nearby customers, such as the hydrogen plant in Sweden linked to Mercedes-Benz’s steel mill.

Podcasts & Shows:

Four Corners: Series 2024 The New Trade War (ABC)

Have a great weekend,

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.