Commodity Prices just keep Running

Published 25-MAY-2024 11:05 A.M.

|

25 minute read

Can Sun Silver (ASX:SS1) deliver a Vulcan style result?

Possibly...

We’ll explain why in a second.

But first we need to understand commodity price runs.

Nothing beats a good ol’ commodity price run for small cap resource investors.

Silver, gold, copper, uranium and even nickel prices have been running upwards lately.

(we’ll also cover each of these commodities price runs today)

So why do commodity prices run?

The simplest explanation for now just basic free market.

But with a bit of lag time added based on how long it takes to build a new mine.

When demand for a particular commodity surges

OR

There is a (real or perceived) supply shortage...

That commodity price will go up...

Up enough to make companies want to fast track projects and investors want to give them the money to do it.

Money then flows towards companies with projects in that commodity.

(From investors hoping to capitalise via on market buying of the stock OR investing via capital raises).

These companies now suddenly have more money to progress their projects to (eventually) fill the new demand.

And hopefully a handful of them will actually bring some new supply onto the market at some point in the future.

The lithium price run of 2022 was a perfect example.

The electric vehicle revolution gained real traction and mainstream attention.

Suddenly the world realised it would need a LOT more lithium for all these new electric car batteries.

The lithium price shot up.

And stayed up.

The running lithium price tailwinds swept up lithium stocks, big and small, through on market buying of stock.

They all also raised lots of cash, made new discoveries, progressed projects and some of them are now actually close to bringing new supply online.

After a few years of high lithium prices, the market must have perceived that enough lithium companies now had enough money for future lithium supply needs to eventually be fulfilled.

...and so the lithium price came off.

(If enough new lithium supply turns out NOT to be the case, the lithium price will spike again so lithium companies can raise more cash...)

Investing in lithium companies BEFORE this lithium price run up was the shrewd move for those that managed it, but everyone would be rich if we could all invest with the power of hindsight.

While we certainly do get it wrong sometimes, it’s our job to keep having a crack at getting it right.

One time we DID get it right was with Vulcan Energy Resources (ASX: VUL), which was up >8,000% at its peak.

And we are hoping SS1 has the same ingredients...

IMPORTANT: The past performance of VUL IS NOT an indicator that SS1 will perform in a similar way - remember investing in small caps is very risky and many things can and do go wrong, so only invest what you can afford to lose.

In general, the ingredients that DID work really well for us back in 2020 was to find a company that:

- Acquired the project in a down cycle - Acquired a project in an “unloved” commodity, for a very good price.

- Project size and scale is big - the project has to have genuine size/scale potential so that investors see it as the most leveraged exposure to any particular thematic. That way it captures the biggest audience if things go in its favour... including major funds and potential acquirers.

- In the green theme - Project/commodity has applications in the “decarbonisation / green energy” area, meaning lots of financial incentives and investor interest in this space.

- In a country with demand for the end product - located in a region that is prioritising the particular initiative and directly needs a new, preferably local supply of the critical commodity (...hello government incentives and subsidies).

- Be the first mover - First to go public with their project when the commodity sentiment isn’t in full swing... yet (all the “copycat companies” will come later once the first mover starts showing share price success)

- Then wait for that commodity price run.... 100% NOT in our control - this is where a bit of luck with timing comes into play.

We first Invested in VUL when nobody cared about lithium, because it fit the above recipe...

and ~4 months later the lithium price started moving up...

then 6 months later the lithium price really started running hard.

The elusive and hard to get “ingredient #6” had appeared - it was a ~12 month wait.

Here’s how the VUL investment looked like in our 6-step recipe:

- Acquired the project in a down cycle - VUL picked up a geothermal lithium brine project at a time when lithium was hated and hard rock lithium mines were going into administration. In 2019 when nobody liked lithium, VUL acquired the project for ~$1M paid in stock (with another $2M in stock payments on achieving performance milestones - full deal terms here) - VUL is now at a market cap of nearly $1 Billion.

- Project has size and scale is big - VUL’s project at the time had one of the largest lithium resources in the world and the single biggest inside the EU.

- In the green theme - VUL’s plan was to turn its project into the world’s first ZERO carbon lithium project, a theme where a lot of interest, investment and government incentives are flowing.

- In a country with demand for the end product - VUL’s project was in the heart of the EU's auto industry in Germany. The carmakers started announcing plans to transition their car fleets to EVs which signalled upcoming lithium demand in Germany... not to mention the EU’s critical raw materials act which is now at play.

- Was the first mover - VUL basically invented the “Zero Carbon Lithium” concept. VUL and was a first (listed) mover in the Direct Lithium Extraction (DLE) from lithium brines space, and the first in “Zero Carbon Lithium”. Up until 2020, most of the focus in the lithium industry was on getting old operating mines back into production OR ramping up small scale operations. No one was looking at DLE from brine assets...

- Then wait for that commodity price run... This is where a bit of luck comes into play... VUL completed its deal and started trading a few months before the lithium price took off.. Between 2020 and 2022 the lithium price went up by over 600%... and VUL went up over 8,000%.

Here is how SS1 looks relative to the same 6-step recipe:

- Acquired the project in a down cycle - SS1 picked up its 292M silver ounces equivalent asset in August 2023 when nobody was talking about or investing in silver. SS1 paid ~$4.8M in cash and 3.5M SS1 shares. Silver prices had been trading in a range for over a decade and capital was not interested in primary silver projects.

- Project has size and scale - SS1’s project has a “globally significant” 292M ounce silver equivalent JORC resource - the second biggest on the ASX right now and there is still scope to grow it...

- In the green theme - Silver is a key raw material for producing solar panels to support the energy transition. More solar panels will mean the world needs more silver. SS1’s key differentiator from traditional silver miners is SS1 has a proposed downstream value addition of producing “silver paste” - a material made from silver powder, a solvent, and a binding agent, silver paste is used in the production of solar panels to improve their efficiency. SS1 proposes to sell this directly to the solar industry.

- In a country with demand for the end product - SS1’s project is in Nevada, USA. The USA has set a target for solar to reach 30% of U.S. electricity generation by 2030. That amount of solar will need a lot of silver paste. The US is currently looking to localise manufacturing and has launched a US$300BN Inflation Reduction Act. China is currently producing ~80% of the world’s solar panels which means the US will need to invest a lot of capital into its local solar supply chain to reduce this dependency.

- Was the first mover - SS1 is the first ASX listed company looking at potential downstream “silver paste for solar panels” production to sell directly into the solar panel manufacturing industry. IF this plan succeeds we expect to see other companies try to copy the silver paste strategy like many copied Zero Carbon Lithium and DLE after Vulcan.

- Then wait for that commodity price run... SS1 picked up its project before silver prices started running and then IPO’d just as the silver price started breaking out above decade highs. As a precious metal also with industrial uses, we think silver prices could continue running over the next 3-5 year period.

The silver price over the next year is the wild card for SS1 that we hope will work in our favour.

The silver price has already exceeded our expectations, faster than we hoped by trading above decade highs of US $30 for the last week (after we first invested in VUL it took the lithium price ~12 months to really get moving).

IMPORTANT: The past performance of VUL IS NOT an indicator that SS1 will perform in a similar way - remember investing in small caps is very risky and many things can and do go wrong, so only invest what you can afford to lose.

Now it’s still early for SS1 and lots of work is yet to be done.

The ingredients are all there for SS1, we just need ingredient #6 (silver price moving up) to keep things humming.

What we want is for the silver price to continue its upward trajectory over the next 12 months and for SS1 to start delivering some material progress announcements into a silver price run to really get it going.

Our view is that due to the growing silver supply shortage, at some point over the next 3 to 5 years the silver price will need to go on a big enough run to bring enough interest (and money) into the sector so a few new mines eventually get built.

(and hopefully SS1 is one of them)

See why we Invested in SS1 here: Our Next Investors 2024 Small Cap Pick of the Year: Sun Silver (ASX: SS1)

We do have control of choosing companies that fit the first 5 ingredients of the recipe, we just don’t have any control over what the silver price does. So instead we just watch it like a hawk here.

The lesson we take away is that small cap investing is about acquiring and holding stocks in unloved commodities, and waiting for the commodity to be back in favour.

Sometimes it happens quickly, sometimes it takes ages and unfortunately investors can get heavily diluted in crunch raises while waiting...and for some companies we are STILL waiting.

Also noting that commodities don’t run forever - good companies, on the tail end of a cycle when interest in the commodity is falling, would have hopefully raised money to develop the project, and “re-rate” at a higher step-change valuation while the commodity price takes a rest.

Right now silver, gold, uranium and copper have started running...

Below we will share our view on why each of these commodity prices are running and where we are Invested in each.

The question is now... are these current price runs a “flash in the pan” or the start of something bigger like we saw in lithium a couple of years ago?

Below each commodity price chart is a link to each live commodity price so you can track them too.

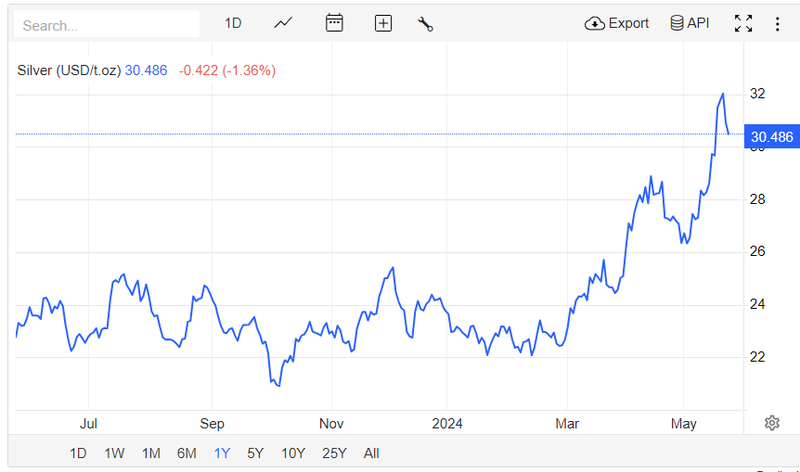

Let’s start with silver, given that it is the most topical across our Portfolio right now.

Silver:

(Source)

Silver has been moving upwards since March 2024, we think there are a few reasons for this:

- Gold prices have been running - Traditionally, silver tracks the gold price relatively closely - when gold goes up, silver tends to follow soon after.

- Silver isn't just a precious metal it is also an industrial metal - Silver is a critical input material into solar panels and as demand for solar panels increases, demand for silver does too.

- Exponential silver demand growth projected to 2050 - By 2050, 50% of silver demand is expected to come from the solar panel manufacturing market. This is a relatively recent development in the silver market.

- Production is declining - Globally, silver production declined by 0.7% in 2023. Decreasing production isn't just a “2023 thing” either. Global silver production has been trending lower since 2016...

- Production falls have led to deficits for 3 years straight - The last three years have seen a significant large supply deficit emerge.

- Underinvestment in new supply due to low commodity prices - Silver has been trading well below incentive prices for over a decade now. That has meant extremely low investment in new mine supply or exploration to make new discoveries.

We think the medium term outlook for silver is positive and think the silver price has a long way to go before it hits “incentive prices” and brings in a flood of capital into the sector.

(“incentive price” means the commodity price is high enough to make mining highly profitable and speed up money flow into companies that are building new mines)

Below are our Investments with silver exposure:

Sun Silver (ASX:SS1)

SS1 is developing a 292M ounce silver equivalent project in Nevada, USA.

SS1’s project has the second largest silver equivalent JORC resource on the ASX - second only to Silver Mines which has a market cap that is multiples higher than SS1’s.

SS1 is also looking to go downstream by producing silver paste so that it can tap directly into the solar panel green thematic.

This week SS1 announced that it has already kicked off a tendering process for an upcoming drill program where the company will be looking to increase its JORC resource even more.

We are looking forward to drilling.

Read our SS1 Investment Memo here

Mithril Resources (ASX:MTH)

MTH is the latest addition to our Portfolio.

MTH’s project in Mexico already has an existing 40M ounce silver equivalent JORC resource.

(373k ounce gold and ~11M ounce silver)

The silver exposure for MTH comes from the multiple >3,000g/t silver drill hits that we think could lead to an increase in the company’s JORC resource.

Off the back of those drill hits, MTH once traded with a market cap >$110M.

We are backing MTH CEO John Skeet to repeat what was done back when he was the GM of projects for an old ASX listed gold explorer - Bolnisi Gold.

Bolnisi took its Mexican gold-silver project into production and eventually through to a takeover that valued the project at ~US$1.1BN back in 2006...

We are hoping his experience at Bolinisi can help drive success with MTH.

Read our MTH Investment Memo here

Titan Minerals (ASX:TTM)

TTM’s main projects have gold/copper exposure, but it's Dynasty project has a 22 million ounce silver JORC resource.

So we think TTM gives us some exposure to a silver price run.

A few weeks back TTM put out rock chip samples from in and around its JORC resource which returned silver grades as high as 197g/t silver.

As long as the silver price keeps running, we think the market may start to look at TTM over the coming months considering its large silver resource.

Read our TTM Investment Memo here:

Gold

(Source)

Gold has been consistently on the run since late 2023, and here are a few reasons why:

- Demand is increasing due to inflation and interest rates - with high inflation and high interest rates, investors can look to gold as a hedge against any market uncertainty and currency devaluation risk.

- Demand is increasing due to geopolitical tensions - as tensions rise around the world from ongoing conflicts, investors and the general public buy gold to protect the value of their wealth.

- Mined gold grades are falling - grades across the major mines are falling and new discoveries aren’t being brought online fast enough to fill in gaps from the falling grades.

- Central bank's demand - Central banks have been piling up gold, with the People's Bank of China stocking up 224.9 metric tonnes in 2023. (source)

We think the short to mid term outlook looks positive for gold.

Below are our investments with gold exposure:

Mithril Resources (ASX:MTH)

We Invested in MTH primarily because it gives us exposure to silver AND gold.

We mentioned MTH’s silver exposures earlier in today’s email but MTH also has a 373k ounce gold resource which we think is a big part of the company’s story.

If the gold price keeps running then we would expect it to drive interest into MTH.

Read our MTH Investment Memo here.

Techgen Metals (ASX:TG1)

TG1 is currently focusing on lithium and copper.

BUT...

TG1 hit gold at its John Bull project in NSW back in September 2022.

At the time TG1 hit discovery intercepts of ~68m at 1g/t gold grades.

TG1 is currently waiting on permits to be granted for a phase 3 drill program on that asset.

We hope to see a further update from TG1 on their gold project (which we actually really like) soon.

Read our TG1 Investment Memo here.

Titan Minerals (ASX:TTM)

TTM’s most advanced project is its Dynasty project in Ecuador.

The project has a 3.1M ounce gold, 22M ounce silver JORC resource so we think the company is well positioned to benefit from a rally in gold prices.

TTM expects to upgrade its JORC resource before the end of this quarter which could be a catalyst for the TTM share price in the short term.

We have been holding TTM for nearly 4 years and hope it starts responding to the gold and silver price moves soon.

Read our TTM Investment Memo here.

LCL Resources (ASX:LCL)

LCL has a gold asset in Columbia with a 2.6M oz gold resource.

Prior to 2022, LCL’s Colombian gold project was progressing rapidly, but was effectively paused by the company due to uncertainty from mining policy changes by the newly elected Colombian government.

In 2023, LCL’s environmental licence was approved, so it seems that the government's stance on mining projects may be thawing earlier than anticipated.

In an update earlier this month LCL mentioned it “is in early stage discussions with several companies seeking advanced gold-copper projects with exploration upside”.

LCL also acquired a new gold project in 2023 located in the highly prospective region of Papua New Guinea, considered "elephant country" for large gold and copper discoveries

Given LCL’s market cap is just $11.5M, we think any positive news on the gold front could start to build some positive momentum for the company...

Read our LCL Investment Memo here.

BPM Minerals (ASX:BPM)

BPM’s gold exposure comes from its Claw Gold project.

BPM’s project sits right next door to Capricorn Metals Mount Gibson mine which has a 3.24m ounce gold resource.

BPM recently did a round of drilling on the project which hit gold mineralisation but the grades weren't quite high enough to be able to declare a discovery.

BPM is currently going through the permitting process for a phase 2 RC drill program which it expects to start mid-year.

Read our BPM Investment Memo here.

Copper

(Source)

Copper is one of those metals we think has the strongest long term tailwinds for a bunch of reasons:

- Production grades are falling - future copper production forecasts are all modelling declining grades across the big copper mines all over the world. As a result most analysts are forecasting shortages out into the future.

- Demand set to increase due to electrification thematic - Copper is one of the most important metals for the global energy transition. It is used in power lines, EV chargers and things like data centres.

- Copper is a critical raw material for the energy transition - copper has been listed on several critical/strategic raw materials acts all over the world. Governments clearly recognise the importance of securing copper supplies.

- For the first time in decades, copper refineries are paying for new ore - typically the big copper refineries charge a fee to process copper ore. For the first time in decades, refinery fees were negative which to us shows that the refineries are getting desperate for copper ore supply.

- New discoveries just aren't happening - the copper sector hasn't seen a huge wave of capital flow into it to incentivize new discoveries yet.

Below are our Investments with copper exposure:

Titan Minerals (ASX:TTM)

(TTM... again, they have the gold, silver, copper “running commodities” trifecta)

TTM’s main asset in Ecuador is its gold-silver project BUT...

TTM recently signed a deal on one of its copper exploration assets with a wholly owned subsidiary of Gina Rinehart’s Hancock Prospecting called Hanrine, worth up to US$120M.

That deal excludes TTM’s 3.1moz gold + 22moz silver JORC resource at its Dynasty asset.

We see this copper exposure as an almost free option for TTM, especially now that Gina is involved and wanting to spend money on the project.

In 2023 the company ran an IP geophysical survey and found what it thinks could be “a much larger porphyry system than previously recognised in surface mapping, geochemistry, and drilling”.

That is going to need funding to drill, which is exactly what Hanrine can bring to the table.

The deal is also structured in a way where the majority of the US$120M gets spent on the project, meaning the deal will force capital into the ground if Hanrine likes what they see.

See our take on Gina’s copper deal with TTM here: Gina Rinehart Hancock Subsidiary to earn into TTM Copper Asset

Solis Minerals (ASX:SLM)

We first Invested in SLM for its lithium assets in Brazil (which didn’t work out) but at the time the company was also working up its copper portfolio.

SLM owns a bunch of copper assets in Peru covering ~43,500 hectares of licences and applications.

These have a few big porphyry style copper targets that could be very interesting if drilled.

Two drill permit applications are underway over llo Este and Ilo Norte (Chancho al Palo). Cinto application is in planning phase.

Any surprise newsflow from these assets could get the market interested in SLM’s copper assets.

Read our SLM Investment Memo here.

TechGen Metals (ASX:TG1)

TG1 recently picked up copper assets in WA that we think look interesting.

Both projects have high grade copper rock chips, with one project containing grades up to 50.5% and the other up to 4%.

Next across both projects TG1 will be running geophysical surveys to identify potential drill targets.

Read our Latest TG1 note here:

Uranium

(Source)

Uranium is slowly becoming a more and more important part of the energy transition. Here is why we think the price is running right now:

- US ban on Russian uranium - On May 13, Joe Biden signed the Prohibiting Russian Uranium Imports Act - which bars US imports of Russian uranium 90 days after enactment. The impact of this is that the US uranium industry will need to start shoring up a local supply of uranium to feed their reactors.

- Lack of supply out of Kazatomprom - Kazatomprom, the world’s largest uranium producer which operates in Kazakhstan, has confirmed in March that it will not be able to meet its previous production forecasts after 2030. This may lead to increasing uncertainty in the uranium supply chain and support prices as more customers look to secure uranium ahead of a potential lack of supply from the Central Asian country.

- Nuclear power becoming more attractive for governments as a source of power (COP28) - following the major climate conference late last year, there was a push from 22 nations declaring their ambitions to triple nuclear output by 2050. This will require large volumes of uranium to sustain the expansion of nuclear power.

Below are our Investments with uranium exposure:

Haranga Resources (ASX:HAR)

HAR owns 70% of its Saraya uranium project in Senegal, which has an existing JORC resource of 16 million pounds of uranium.

HAR is currently running a 20,000m drill program at its uranium project which hosts a large number of uranium anomalies on its expansive land position.

French multinational nuclear power and uranium supplier company Orano, formerly known as Areva previously owned HAR’s uranium project in Senegal twice - once in the 1970s-1980s and again from 2009 to 2011 during uranium bull markets.

With uranium looking like it could be in a third bull market - we’re looking for drilling and assays to help HAR expand its existing JORC resource.

Read our HAR Investment Memo here.

Global Uranium and Enrichment (ASX:GUE)

GUE has four different North American uranium assets and a 21.9% stake in a uranium enrichment technology company.

GUE is currently drilling at its advanced ~50Mlb JORC resource, which is one of the largest undeveloped uranium projects in the US.

This drilling is designed to support a scoping study due in Q3 of this year, which we think will incorporate a strong uranium price.

GUE will also be drilling a brownfields project which has historically high grades - the more pounds in the ground it finds, the higher we think GUE will be valued by the market in this strong uranium price environment.

Read our GUE Investment Memo here.

GTI Energy (ASX: GTR)

GTR has three uranium projects in Wyoming, USA.

GTR has defined JORC uranium resources totaling around 7.37 million pounds across two of these projects.

The projects are located near existing uranium processing facilities owned by major companies like Uranium Energy Corp and Cameco, which could potentially process GTR's resources in the future.

In early 2023, GTR also acquired the Lo Herma project in Wyoming, located within 16 km of Cameco's largest production site in the state.

GTR plans to announce additional JORC resources for its Wyoming projects in the coming months as it continues exploration and drilling activities.

Read our GTR Investment Memo here.

Mandrake Resources (ASX:MAN)

MAN has recently completed a uranium sampling program at its project in Utah, USA.

The project covers an area of around 379 square kilometres and is located less than 5 km away from the La Sal uranium mine, which restarted production in December 2023.

It is also around 100 km away from the only operating conventional uranium mill in the US, the White Mesa Mill, owned by Energy Fuels.

During the sampling program, Mandrake identified several "radioactive outcrops" and collected six rock chip samples for lab testing.

These rock chips were initially too radioactive for the lab to handle and subsequent testing revealed very high grade uranium.

We’re looking forward to future exploration activities for MAN in Utah.

Read our MAN Investment Memo here.

What we wrote about this week

NEW INVESTMENT - Mithril Resources (ASX:MTH)

This week we added MTH to our portfolio.

MTH’s project has an 40M ounces silver equivalent JORC resource in Mexico’s Sierra Madre Gold-Silver Trend.

~10% of all historic silver production has come from this part of the world.

We are Invested in MTH to see it replicate the Bolnisi gold success story - for context, Bolnisi took its gold-silver project in Mexico into production and then an eventual takeover for US$1.1BN.

MTH’s CEO John Skeet was the GM of projects for Bolnisi, we are hoping he can do it all again with MTH.

Read more: Our new Portfolio addition: Mithril Resources (ASX: MTH)

88 Energy (ASX:88E)

88E is about to kick off an exploration program at its onshore Namibian asset right around the time its much larger capped neighbour Recon Africa prepares to drill multiple wells.

We think the market is completely missing the potential of 88E’s Namibian assets and wrote a note this week explaining why...

Read more: 88E starts on “swing for the fence” Namibia oil exploration.

Quick Takes

KNI Resampling 3,000m of Drill Cores to Increase Resource

HAR working toward a uranium resource upgrade by June

GUE confirms high grade uranium, scoping study next

SS1 tenders for silver drilling in US

Bite sized summaries of the latest mainstream news in battery metals, biotechs, uranium etc: The Future Money: https://future-money.co/

Lithium in Arkansas: Norwegian Energy Giant now in Arkansas

Macro News - What we are reading

Copper:

Five Key Charts to Watch in Global Commodity Markets This Week (Bloomberg)

- A short squeeze on the New York Comex exchange caused copper prices to soar, creating a significant premium over London prices and sparking a rush to ship supplies to the US.

Energy:

Rio Tinto declares force majeure on Australian alumina cargoes (afr.com)

- Rio Tinto declared force majeure on alumina from its Queensland refineries due to gas shortages, affecting third-party sales.

- The company notified clients on Monday, citing a gas supply issue worsened by pipeline fires.

Nickel:

Nickel price jumps as unrest cuts output in No. 3 miner New Caledonia (Mining.com)

- Nickel prices surged over 5% due to unrest in New Caledonia, disrupting output from major producer Eramet SA.

- New Caledonia's production woes and global supply issues, including delays in Indonesian mine licensing and Russian sanctions, have driven nickel prices above $20,000 a ton earlier this week.

Have a great weekend,

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.