Raising cash in a rough market and what to watch out for

Published 18-JUN-2022 09:58 A.M.

|

17 minute read

A US interest rate hike led to a massive sell off in markets with the ASX200 falling by 7% for the week.

We felt that pain in the small cap end of the market too with most of the companies on our watchlists in the red for much of the week.

Some of the companies we hold in our Portfolio and those that currently sit on our watchlist are trading at near 1-2 year lows.

Some are starting to approach levels at or below where we originally Invested.

We believe strongly that the critical metals, commodities and green energy thematics will still be strong once the broad fear in the markets subsides, as it always does eventually.

So we continue to hold companies we believe in over the long term, through the short term ups and downs of the market.

As long term holders, we prefer our portfolio companies to raise capital during a hot market.

Companies with a couple of years worth of cash in the bank can weather the storm of a bad market and focus on executing their plan.

Companies that DIDN’T raise money during the hot market now find themselves in a situation where their share price is down, and raising capital will need to be done at a deep discount to an already beaten up share price to attract now-cautious investors.

While a heavily discounted cap raise in a down market isn’t great for existing shareholders like us from a dilution perspective, Investments we made during the last down market have historically delivered us the best returns.

The 2c EXR placement in the depths of the COVID crash is one that springs to mind, after we originally Invested at 3.9c the year before.

We will likely participate in most cap raisings from our Portfolio companies during this rough market patch - we see it as a good time to add to our positions (in our opinion, not financial advice).

Types of capital raisings on the ASX

Companies have a few options when it comes to raising capital - and they will work with a stock broker to structure, price and execute a capital raise.

Here are the different types of capital raising structures:

IPO - This is a capital raise done for a private company as part of its listing on the ASX.

The valuation is determined by the broking firm leading the IPO, at a price which is attractive enough for investors to put in their cash based on where the company is on its development lifecycle.

We think that IPO valuations will need to come down significantly to attract money in this market.

Placement - A share "Placement” is the most common type of capital raise, where a listed company creates (issues) new shares and they are sold to new investors.

Placements can only be offered to “sophisticated investors”.

The Corporations Act defines a sophisticated or professional investor as having had a gross personal income over the last two years of at least $250,000 per year OR have net assets of over $2.5M.

Placements are usually launched and closed over a couple of days after the company goes into a trading halt, and are done at a discount to the last traded share price to encourage investors to participate.

While Placements are often offered to some existing shareholders who qualify as sophisticated investors, given the speed at which Placements need to be completed they are usually filled by the clients or networks of the broking firm leading the Placement.

Placements are the fastest and easiest way for companies to raise capital, but can be frustrating for existing shareholders who may not be offered the chance to participate.

Share Purchase Plan - A Share Purchase Plan (SPP) is a way to offer access to a capital raise to retail shareholders who don’t qualify as “sophisticated investors” under the Corporations Act definition.

As described above, a Placement may only be offered to sophisticated investors.

An SPP is often done alongside a Placement, but offers ANY shareholder the opportunity to invest between $2k and $30k at the same terms as the placement.

SPP’s are great to give equal access to all shareholders and we try to encourage all our Portfolio companies to include an SPP when doing a Placement.

From a companies perspective however, SPPs take a LONG time to execute and require a LOT of paperwork.

In a down market, retail inventors are generally more cautious and not as likely to participate in any cap raise unless it’s deeply discounted.

The other issue we have observed with SPPs is that while a corresponding placement is completed in ~2 days, the SPP needs to be open for many weeks, and the share price usually drifts down post placement completion.

This makes the SPP look less attractive, and can result in less capital raised.

Recent examples of this happening in our Portfolio include ONE and KNI.

EXR did an SPP over a year ago alongside their last cap raise, which was successfully completed, but the share price went down after it closed.

IVZ successfully ran an SPP alongside their last raise (in January 2022 at 11c) which was oversubscribed and delivered a great result for participants with IVZ doubling in the months after completion.

The above examples are a mixed bag that can be delivered when raising via SPP to all shareholders.

Rights Issue - A Rights Issue (also sometimes called an entitlement offer) is similar to a “Placement” but is ONLY offered to existing shareholders who are invited to participate in proportion to their existing shareholding.

So if you own 1% of the company, you can take up to 1% of the capital raise allocation.

Rights Issues are good for existing shareholders as it allows them to invest more to maintain their percentage shareholding in the company, as opposed to being diluted by new investors coming in via a Placement.

From a company’s perspective, rights issues to existing shareholders can be more difficult than a Placement to new investors because (1) they take a lot more time and paperwork and (2) it is unlikely that all (or even most) existing shareholders will invest more, leaving a “shortfall” in the required capital to be raised.

The remaining shortfall can be placed to new investors, after any existing shareholders have taken up their right to invest first.

So we have Placements, Rights Issues and SPP’s - What to look out for in a rough market:

With many share prices trading at multi-year lows, there are things we look for that have historically been good signals that valuations are becoming attractive.

Some of the positive signs are as follows:

- Companies opt to do smaller capital raises through share purchase plans (SPPs), Rights Issues or Entitlement Offers (instead of doing Placements). These give existing shareholders like us AND retail investors an opportunity to increase their shareholding at valuations that boards/management teams think are attractive.

- Directors start buying shares on market or in capital raises. This is self explanatory, the people managing the business day to day start to step up and buy shares - a really strong signal that they see value in the company’s shares.

There are some negative signals to watch out for too:

- Some companies may do big placements at heavy discounts without giving existing shareholders the chance to participate. We hate seeing this happen when the shares are trading near multi-year lows after we Invested at a higher price. Instead of preserving cash and doing small raises to see out the market lows, these placements can be extremely dilutionary to existing shareholders.

- Companies delaying capital raises waiting for the markets to recover. This can be a risky strategy whereby companies miss the opportunity to raise capital now and are then forced into a raise later in the cycle when markets may be in even worse shape.

Capital is critical to a company's ongoing operations, and being caught having to raise cash in a down market can be a tough spot for company management, a hard job for stockbrokers, and frustrating for existing shareholders who get diluted.

At the end of the day the most important thing is that our Portfolio companies all have enough cash to operate during the down market.

In terms of how a raise is priced and structured - the actions of our existing portfolio companies help inform our judgement of the management teams and board of directors, and the corporate advisor/stockbroker they use to help structure their capital raising.

When it comes to the companies we are watching as potential new additions to our Portfolio, the more positive signals on how they conduct themselves in a down market, the more likely we are to make an Investment.

Mind you, we also are keeping an eye out for heavily discounted cap raises to participate in — where a solid company is trading at multi-year lows and a cap raise is offered at a significant discount.

Why are interest rate hikes driving a market sell off?

We have been around the markets for 20 years and have seen these sorts of sell off events before.

Those who are new to the markets will probably be trying to get their heads around why these rate hikes are leading to red days in the stock market.

The last two decades have seen rates slowly move lower and the investing community isn't used to central banks hiking aggressively.

That’s why we think the sell offs in markets have been especially strong — the 0.75% rate hike in the US was much higher than was expected by the market.

Second, the Fed’s commentary was extremely hawkish (aggressive) signalling more rate rises over the coming months.

The US cash rate is now 1.75%, and markets seem to be pricing in a rate of ~3.5% by the end of the year.

It’s a similar story here in Australia with the Reserve Bank of Australia's (RBA) governor Phillip Lowe announcing that “Australians should expect more aggressive rate hikes” over the coming months.

All of this came as a surprise to the markets, which were largely expecting a less aggressive stance by central banks and perhaps a more gradual increase in rates over the coming months.

The market hates surprises.

Putting aside the “surprise factor”, what do higher interest rates mean for small cap stocks?

It's actually relatively simple: small caps are high risk / high reward investments where investors take concentrated bets on small companies.

They hope that $10-15M market cap companies turn into $200-300M market cap companies.

Inherently these types of investments require capital that is willing to take on the added risks that come with investing in small, high risk companies.

This is where interest rates come into play.

The cash rate is a measure of the “risk-free” rate and so it has an impact on the willingness of investors to take on the added risks that come with share markets investing.

To illustrate this point we will run through two scenarios with different cash rates.

Scenario 1:

Where the cash rate is pinned to the floor at 0.1%, capital sitting in a bank account is yielding 0.1% per annum, meaning $10,000 in cash in a bank account returns $10 per year in interest.

Investors see the nominal $10 return and think, “I want to make a bigger return and am willing to take more risks to try and do this”, so they might look to invest in the share market.

Scenario 2:

Where the cash rate is now let's say 2%, capital sitting in the bank account is yielding 2% per annum, meaning $10,000 in cash in a bank account returns $200 per year in interest.

Because of this, there will be incrementally more investors who are willing to park $10,000 in a bank account and receive the $200 in interest than there would be if the return was only $10.

Not to mention that discretionary spending power is reduced so surplus cash is better to have around.

This all leads to a flurry of investment capital away from the share markets, which are deemed “risky”, and into cash or cash equivalents like term deposits.

This isn't the first time this has happened.

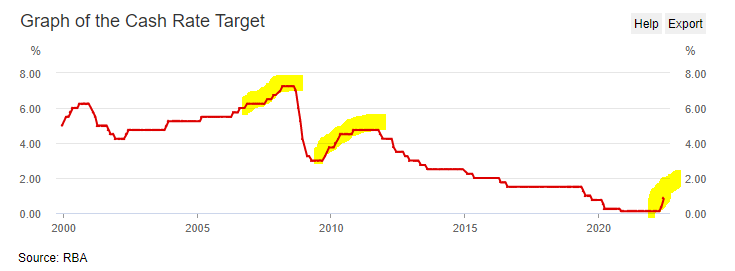

As we mentioned above, we have been investing in the share market for 20 years, including through the Global Financial Crisis when the RBA raised rates from ~5.5% in 2006 to a high of ~7.25% in 2008. Again, in 2009-10 rates rose from ~3% to ~4.5%.

Our learnings from these times is that they provide temporary sell offs where small cap companies with good prospects go “on sale” as investors generally leave the market, especially higher risk investments.

When the dust settles and months and years pass, the Investments we make during these rough periods often end up being our best performers over the long term.

These are the times when we put in the long hours and do even more due diligence work, looking for companies with high quality long term prospects.

Coming back to the current market sell off, we think the timing of these rate hikes is adding to the selling pressure.

Investors have gone from “sell in May and go away” straight into June - known to be a brutal time where investors sell their losing positions (tax loss selling).

This puts the markets into a position where there is a lot more selling pressure than there is buying.

There may have been no changes to the fundamentals of a company, but the share prices continue to fall.

Generally, if we go into June with weak market conditions we tend to see the selling continue all the way up to the last week before the end of the financial year.

This time things are just that much worse due to rate hikes, inflationary issues and geopolitical concerns.

We aren't sitting around watching share prices fall. Instead, we are using this period of market panic to brush up our due diligence on new names, and some older names where valuations have become attractive in our view.

Some macro themes where we think valuations have become attractive are:

- Battery metals and critical metals

- Energy (gas)

- Green energy

- Food tech and food security

Currently unloved macro themes we think will shine again in the medium term:

- Precious metals

- Biotechs in general

- Medicinal cannabis

- Drugs (psilocybin, MDMA, ketamine) for mental health

- Health tech

We already have a few names on our watchlist and have started to do our internal due diligence.

Thanks also for the suggestion we recieved to look into “insects as a source of protein for food” which we have added to our macro themes list to explore.

If you know any companies in the above sectors that we should look at, reply to this email with your reasons why - we would love to hear from you.

Thanks to everyone who replied last week with their investment ideas, here is the list of tickers we recorded and have added to our due diligence process:

QPM, WBT, BRN, PTX, OKR, PCL, KRR, BOT, TEG, MR1, ARU, LPD, TLG, MSB, NMT, PCK, CHP, VR8, RAC, ATH, FBR, BC8, MEK, LOM, REC, VMS, MLS, AGY, AZL, CAA, ASN, ADO, BRK, HIO and GMR.

As counter-intuitive as it may feel, accelerating new Investments during an awful market has worked for us in the past.

We hope to announce some of these new additions to our Portfolios over the coming months. If the market continues to perform poorly we expect a lot more companies to enter our “investable” bucket.

⚠️ Breaking news:

On Friday our 2019 Pick of the year Elixir Energy (ASX:EXR) went into a trading halt pending:

“signing of a joint Memorandum of Understanding (“MOU”) to develop Elixir’s green hydrogen project”

Last night, we noted the following press release on the website of Softbank Energy (part of Softbank Group, the 44th largest listed company in the world according to Forbes):

Given this press release we assume EXR will announce the deal on Monday, so we are busy putting together our commentary on it, especially around the significance of Softbank and Softbank Energy as a partner.

We are excited about the green hydrogen thematic and are also keenly watching our Investments EXR, PRL and MNB in this space.

⏲️ Upcoming potential share price catalysts list

Results expected in the near term:

- GGE is drilling its maiden helium well in Utah where it’s aiming to make a commercial helium discovery (memo).

- IN PROGRESS: GGE has completed its maiden drilling program with a ~203 foot (~62 metre) gas bearing column intercepted.

- Update: This week we saw GGE mobilise its workover rig and commence stimulation testing leading up to the all important flow test. We covered this in a Quick Take which you can view here: Workover rig mobilised, flow testing underway.

- PRL signing a Joint Development Agreement with its partner, Total Eren to materially de-risk its WA Green Hydrogen Project (memo)

- IN PROGRESS: The signing of the “Joint development agreement” (JDA) with TotalEnergies. PRL’s deadline to sign the JDA is now set at 31 July 2022.

- Update: No updates on this front this week.

- IVZ to drill its giant gas prospect in Zimbabwe - we have been waiting two years for this event (memo).

- IN PROGRESS: Drilling is scheduled for July. IVZ recently said it had three separate farm-in offers being considered.

- Update: No updates on this front this week.

- KNI to drill its cobalt targets in Norway (memo).

- IN PROGRESS: Last week KNI confirmed it has completed ~1,007 metres of the total ~2,800m drilling planned. We covered the update in a Quick Take which you can read here.

- Update: No update on this front this week.

- BPM to drill its lead zinc prospect in the Earaheedy Basin close to Rumble Resources’ recent discovery (memo)

- IN PROGRESS: BPM is currently completing a ~7,500m AC/RC drilling program at its Hawkins project (along strike from Rumble’s discovery). This is the exploration program we have been waiting for since May last year and hope to see preliminary results in coming weeks.

- Update: No update on this front this week.

- LNR (formerly FNT) commencing drilling for rare earths (memo)

- IN PROGRESS: LNR is still in the process of getting approvals so we are not sure exactly when drilling will occur. It may be later than most on the above list, but we are keeping an eye on progress.

- Update: No progress has been made this week.

🗣️ Quick Takes

Here are this week's Quick Takes:

EMH: Superfund now a major shareholder of our lithium Investment

EXR: Investor presentation - A tale of two energy solutions

GGE: Permit submitted for second helium well in the US

GGE: Workover rig mobilised, flow testing underway

GTR: Acquisition completed, drilling for uranium in July

MNB: Investor presentation - Green hydrogen-ammonia in Angola

ONE: ResMed to Acquire MediFox Dan for $1B

PFE: Drilling set to commence at Hellcat

PUR: AC drilling program underway at WA gold project

TMR: Visible gold observed along strike of discovery

VUL: Local support for Zero Carbon Lithium Project; project expansion

Macro: Iron ore front and centre of Chinese governments mind

Macro: Energy transition requires 5-6x more key commodities

📰 This week on Next Investors

Thomson Resources (ASX:TMZ)

This week we covered Thomson Resources which released its latest Mineral Resource Estimate (MRE) for its Webbs deposit - another tick mark for the company on the road to a planned 100Moz silver equivalent resource across its five deposits.

We also included our commentary on the Investment to date and some of the key risks.

This is TMZ’s fifth JORC 2012 MRE release and is an essential part of its push towards production.

We said that with a Final Investment Decision slated for 2025, we intend to hold the majority of our TMZ position until it gets into production.

TMZ also clearly outlined the next steps for the company and how it intends to get to that 100Moz silver equivalent target:

- Getting base metals into the re-stated Mt Carrington JORC 2012 resource estimate (key and in progress)

- Drilling at Texas Silver District to extend resource and test geophysical targets (to start in June)

- Webbs deposit drilling (to start Q3)

- Metallurgical and Process Pathway for central processing hub (happening now)

We’re confident that TMZ can hit the 100Moz AgEq mark or at least (base case) get very close.

We’ve outlined the following cases for TMZ:

Bullish case: >100Moz AgEq

Base case: 90-100Moz AgEq

Bear: <90Moz AgEq

📰 Read our full Note: TMZ’s Releases Webbs MRE Chasing 100Moz Target

📰 In our other portfolios 🧬 🦉 🏹

🏹 Catalyst Hunter

Microcap TG1 pinpoints gold drill targets

On Thursday our early stage micro cap exploration investment TechGen Metals (ASX:TG1) put out the results from geophysical surveys completed at its newly acquired gold project in NSW.

TG1 is setting up for a busy second half of the year with two drilling programs planned. The first will be at its newly acquired NSW gold project and the second at its copper/gold projects in WA.

This comes as TG1 trades at a market cap of just $6.6M with $2.6M in cash on hand at the end of the March quarter. This means TG1 currently trades at a tiny enterprise value (EV) of just $4M.

TG1 has now reprocessed historical IP surveys and confirmed the existence of IP chargeability anomalies right below previously completed surface trenching work, where average gold grades of 1.2g/t were delivered over a 160m strike length.

TG1 has also been busy putting together drilling targets across its copper/gold prospects in WA.

Just last week it released results of an IP survey at its Ashburton Basin Project where the company identified two specific high priority anomalies right underneath rock chip samples, which returned copper grades as high as 54.8% and 249g/t silver.

Each of the projects are expected to be drilled later this year, with TG1 entering a busy period of exploration. With an enterprise value so low, we think TG1 is highly leveraged to a re-rate in the event of a new discovery.

📰 Read our latest full Note: Microcap TG1 pinpoints gold drill targets

Have a great weekend,

Next Investors

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.