Sunday Edition: 19th April

Published 19-APR-2026 18:00 P.M.

|

20 minute read

Disclosure: S3 Consortium Pty Ltd and its associated entities may hold direct or indirect interests in securities referred to in this publication and may receive fees or other forms of consideration from entities mentioned. These interests and arrangements may create a potential conflict of interest in the preparation of this material.

The information contained in this communication is provided for general information purposes only and may relate to speculative investments. It does not constitute financial product advice, and has been prepared without taking into account your personal objectives, financial situation or needs. You should consider obtaining independent financial advice before making any investment decision.

Any forward-looking statements are uncertain and not a guaranteed outcome.

It was a big Saturday night for the psychedelics industry.

(and no, not THAT kind of big Saturday night...)

Overnight Australian time, US President Trump signed an Executive Order that makes accelerating psychedelic-based mental health treatments official US policy.

Off the back of this news, we expect our psychedelics Investment Emyria (ASX:EMD) to get increased attention come Monday morning.

You can read the full Presidential Executive Order here.

This is the clearest, most aggressive federal signal to date that the US intends to move psychedelics from research curiosity to approved medicine.

(Source)

EMD is a first mover in the industry, operating specialised clinics in Australia where it provides Psychedelic-Assisted Therapy to patients not finding relief from conventional care.

EMD is already operating clinics now and generating revenues.

You can read more about EMD here, and other industry updates here.

Watch the most recent EMD investor presentation here.

Below you can find short overviews of all of the other content we wrote last week, plus links to each complete note.

Further down, some links to other interesting stuff we came across on our travels around the internet.

Yesterday’s Saturday note: Oil & Gas is Back on the Market’s Radar

Quick Takes: LSR, PNN, CAY, RML, VKA, PUR, HAR, SS1, CND, L1M, WCE & REE Macro

Deep Dives: WCE, OD6, ION, HAR

LSR kicked off a field exploration program on its US heavy rare earths project in Arizona.

We know that outcropping rare earths have been mapped across ~225m of the 5km structural trend - what we don't know is if they extend further across that 5km.

(maybe we learn more with the work happening now)

LSR has brought in two WA rare earths heavyweights as specialist consultants to help accelerate exploration here.

Dr Ross Chandler, who won 2023 Prospector of the Year for his role in making the Yin rare earths discovery in WA for Dreadnought Resources.

Plus Robin Wilson, the former Exploration Manager for Northern Minerals (ASX: NTU). Ross led the team that made the Browns Range xenotime deposit (LSR has found xenotime on its ground - a good early sign).

Below is a photo of the pair getting stuck into the fieldwork on LSR’s Arizona rare earths project. Let’s hope they can add to their list of discoveries while working with LSR:

And here is LSR exploration manager Finn Hunter with the guys on site in the USA:

We also noticed LSR is looking at other projects in the US - it will be interesting to see what (if anything) happens here.

(source)

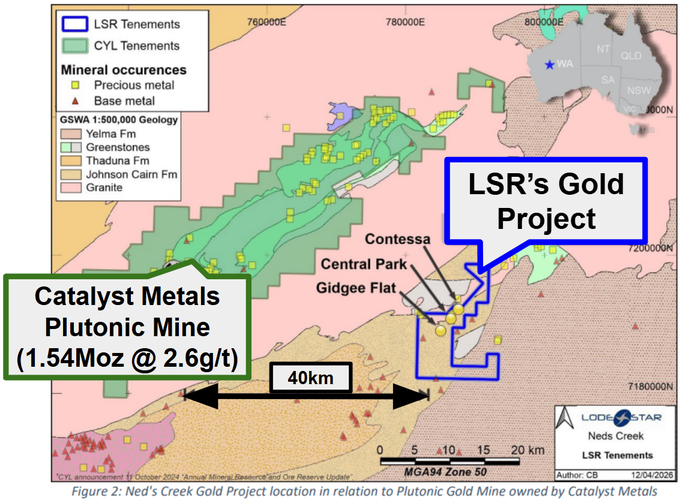

Also this week, LSR kicked off its 10,000m RC drilling program at its WA gold project.

Let’s see how much of the ~250-300k ounce exploration target can be converted into a maiden JORC resource for the project.

PNN completed due diligence on the new rare earths asset it is acquiring in Brazil.

Good to see the deal is almost done. Here are a few reasons we like this asset:

- The grades are not only high, but they are high in “magnet rare earths” - the type of stuff everyone is looking for.

- The project sits on a special title which provides direct ownership rights over the land. This allows for ground disturbing exploration activities (subject to environmental approvals) and reduces permitting complexity.

- The project sits near ASX listed peers which have defined large resources and capped much higher than PNN’s current valuation.

See our deep dive into PNN’s new rare earths project here: PNN: New Brazil rare earths project. 156 drill holes. High grade hits. SGQ 2.0?

PNN new CEO Alistair Stephens has been spending some time in South America visiting each of the company’s projects.

Here’s a video onsite from the Santa Anna niobium rare earth project:

And you can check out his update on the lithium project in Argentina here.

(Source)

CAY released an update on its bauxite project in Cameroon.

The main takeaway for us was CAY confirming that its current cash position would be enough to get the company through to first shipment and cashflow.

(source)

CAY also confirmed:

- Trial mining would start this month.

- Discussions with Camrail continue regarding a potential increase in CAY's ownership above the current 9.1% to above 20%. The parties are targeting completion this quarter (Camrail is the national rail operator, so CAY having more of a stake here would give it much more of a say on upgrades etc).

- Offtake discussions with potential partners are ongoing

- First locomotives delivery remain on track with arrival mid-late Q2 (the first seven locomotives have shipped from China).

- FIRST production is targeted for this quarter. First ore shipment next quarter.

RML (OTC: RLMLF) produced Antimony trioxide from its project in Idaho.

RML’s Antimony Ridge project now has:

- Produced antimony during during WW1, WW2 and the Korean War

- Received FAST-41 status from the US Government (accelerated permitting and basically a badge that labels it a project that the US government thinks is important),

AND

- PRODUCED an antimony trioxide end product - showing its project can be a viable domestic source of antimony in the US again.

That FAST-41 status could unlock permitting for a 250-hole drill program RML has planned for the project too - a permitting timetable is due before the 21st of April (two days to go...) (source)

So we should know how quickly RML can get to drilling this project very soon.

Also, RML brought onboard Brett Lynch as a Non-Executive Director.

Brett served as Managing Director of Sayona Mining which went from micro cap to a peak market cap of ~$1.9BN during the 2020-2021 lithium bull market...

(past performance of Sayona Mining is not an indicator of future performance of RML)

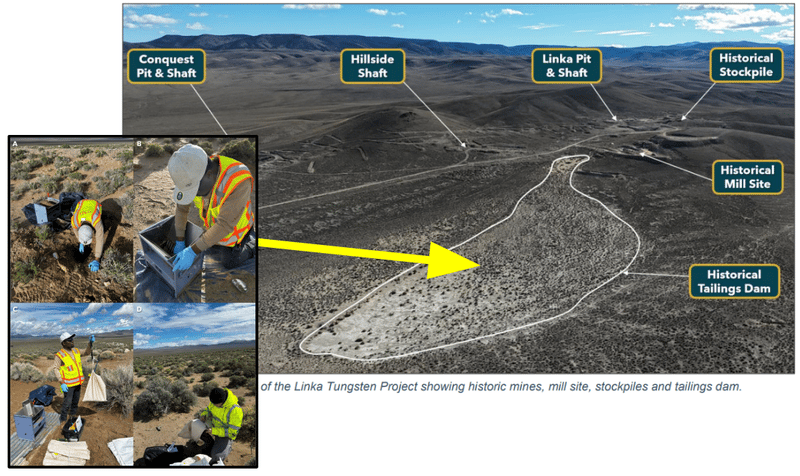

VKA listed on the US OTC market and started sampling old stockpiles and its tailings dam for tungsten.

Here is a link to the US listing where we are tracking trading: OTC:VKALF (nice to see a fair few trades going through too).

Hopefully we get some results from sampling that bring in even more interest to the stock:

(source)

The tungsten price being on a tear is helping VKA’s cause too - more on that below.

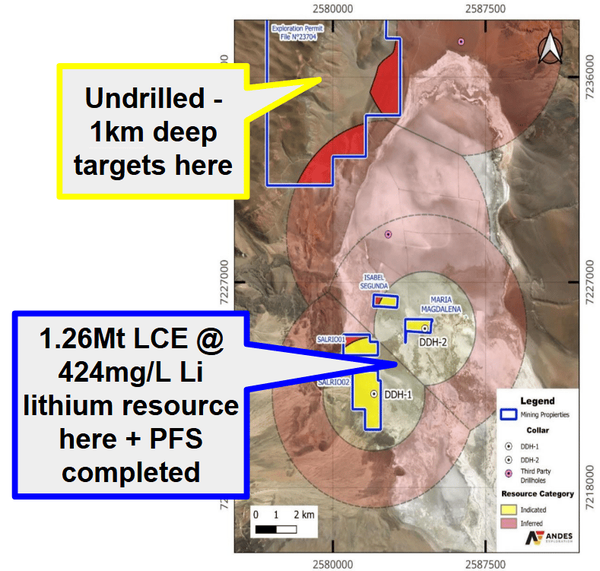

PUR completed processing work on its lithium brine project in Argentina that materially improved depth penetration and resolution. PUR has extended reliable interpretation depth from 250m to 1.1km, significantly expanding the scale of targetable mineralisation

PUR has already got a pretty big 1.26Mt Lithium Carbonate Equivalent (LCE) JORC resource estimate.

However it's the big tenement to the north where we think the potential to multiply that resource is - now that mineralisation potential extends 4.4x deeper.

(1.1km deep instead of previous interpretations being ~250m deep)

(source)

PUR is also aiming to drill three holes on the project with a rig expected on site later this month. Nice timing with lithium prices rallying.

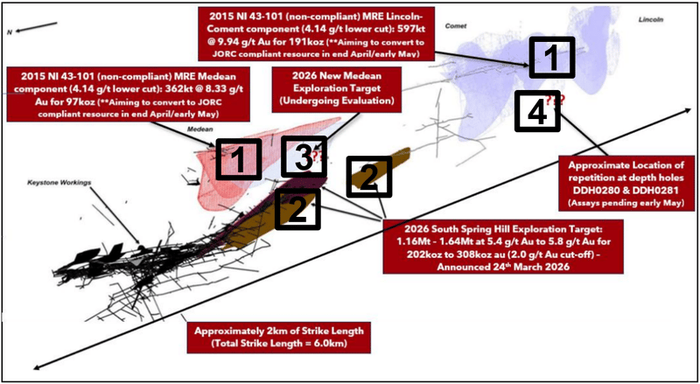

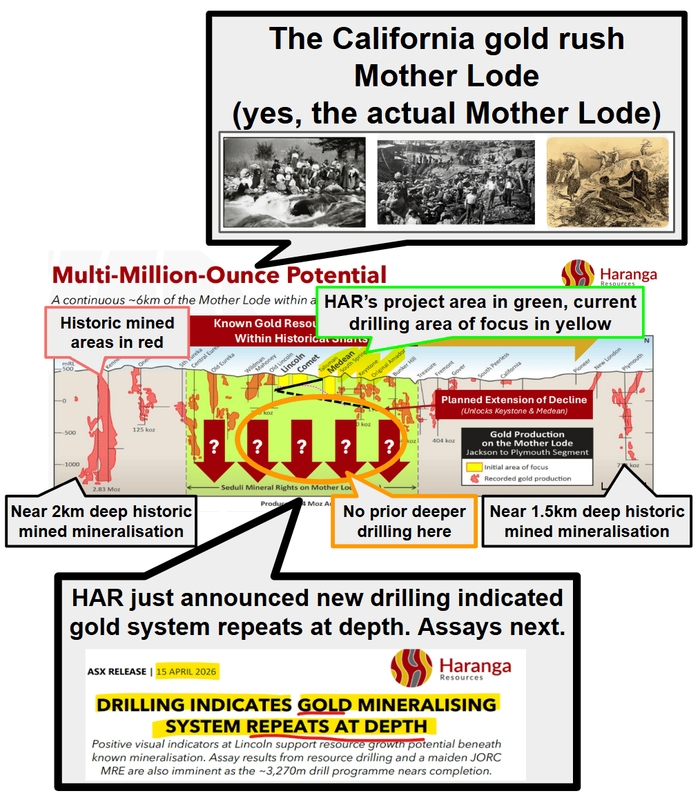

HAR is now a few weeks away from a maiden JORC resource estimate at its project in California.

Below is our favourite image from that announcement, the numbers below refer to:

- HAR’s existing non-JORC 288k ounce gold resource estimate (red and purple sections),

- HAR’s ~308k ounce exploration target at the "South Spring Hill" target,

- HAR’s incoming NEW exploration target, AND;

- Drill holes awaiting assay results - HAR's drilling could be hitting repetitions to the non-JORC resource at depth.

(we have marked those points as numbers in the image below)

More on HAR in the Deep Dive section below and here: HAR: 3 major share price catalysts in the next ~90 days.

SS1 (OTC: SSLVF) appointed Ausenco as engineering consultant on its giant 539M ounce silver equivalent (estimated) resource project in Nevada.

Ausenco is engaged to deliver a maiden Scoping Study / Preliminary Economic Assessment (PEA) for SS1’s project.

SS1 expects to have this delivered in Q4 2026 (hopefully just as the silver price starts running again - no guarantees it will run of course).

(source)

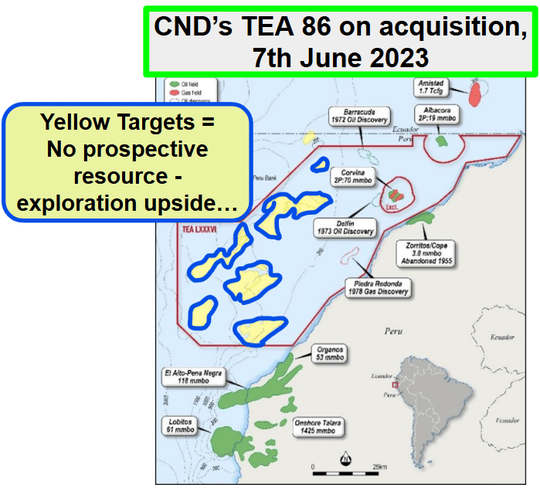

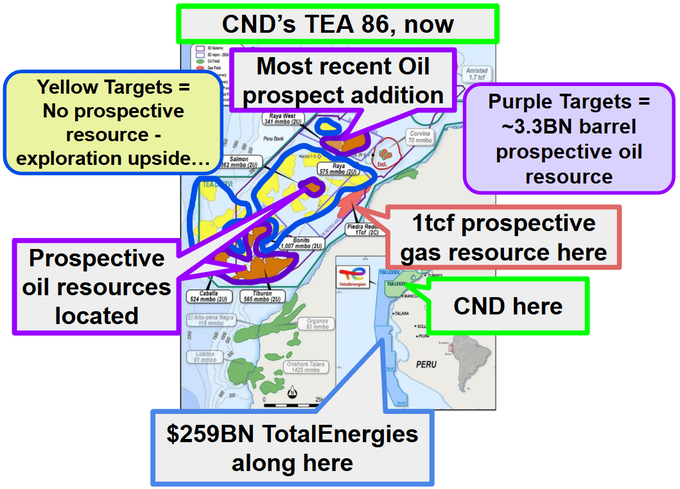

CND completed all of its TEA commitments for its offshore block in Peru.

Now we wait to see CND get that TEA (Technical Evaluation Agreement) turned into an exploration license.

Here is how the block looked when CND first picked up the TEA, and here it is now:

(source)

And here is it right now:

(source)

L1M detailed its strategic reset to focus on gold-copper in Australia.

L1M is now going all in on its gold and copper assets with plans to divest or partner out its lithium assets.

Here new L1M CEO talk through the new strategy here:

Gold strategy reset at Lightning Minerals (ASX: L1M)

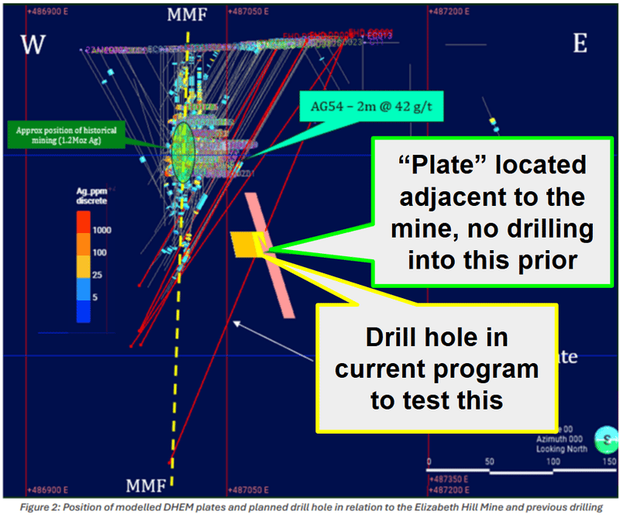

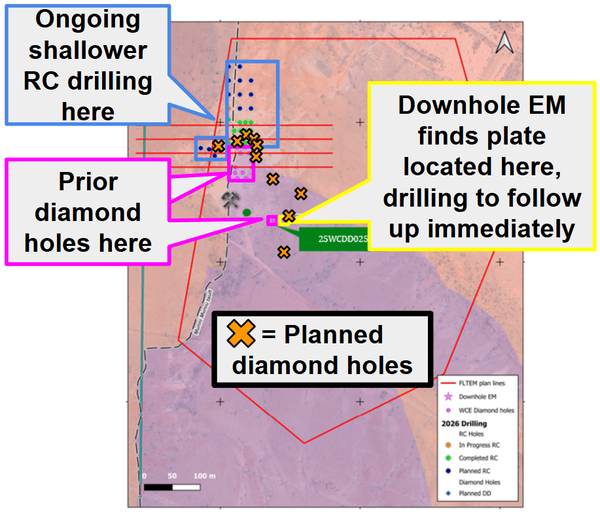

WCE identified a new high-priority drill target at its Elizabeth Hill silver project in WA.

The new target is ~50m east of the old Elizabeth Hill mine and around 110m below surface:

The target has never been drilled before.

(source)

BUT WCE does have a rig on its way to drill it in its current program:

(source)

More on WCE in the Deep Dive section below and here: WCE drilling now underneath highest grade silver mine in Australia

Rare Earths Macro - Our take on the increase in rare earths prices out of China and what it means for our rare earths Investments SGQ, LKY, PNN, LSR & ION.

(source)

Are there games being played by China ahead of that Trump Xi meeting in May? (like what’s happening in oil markets)

Maybe.

All we know is IF prices in China are allowed to (or naturally) rise, then it’s good for anyone exploring or looking to finance a new mine.

West Coast Silver (ASX:WCE)

Between May last year and January this year, silver went on an epic run from US$35 to US$120 per ounce.

In that same period our Investment West Coast Silver (ASX:WCE) went from 5c to a high of ~29c per share.

Silver is currently trading at US $76 per ounce, and WCE is trading at 18c/share.

We think the silver price is going to run again, even higher than before (this is our opinion - we could be wrong).

Silver has spent the last two months putting in a new base a full 50% higher than its two previous all time highs of ~US$49 in 1980 and ~US$50/oz in 2011.

The past performance is not an indicator of future performance.

WCE just started diamond drilling beneath its historical WA silver mine.

WCE’s Elizabeth Hill silver mine holds the record for the highest grade silver mine in Australia, ever.

WCE’s current drilling campaign is for 1,500m over six holes, and is the first test of deeper mineralisation below the historical high grade mine.

(plus WCE still has ~20 regional Elizabeth Hill look-a-likes to drill - to also try and find a whole NEW Elizabeth Hill style deposit nearby)

Read more: WCE drilling now underneath highest grade silver mine in Australia

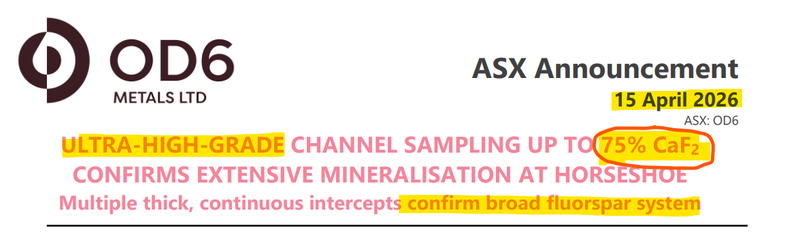

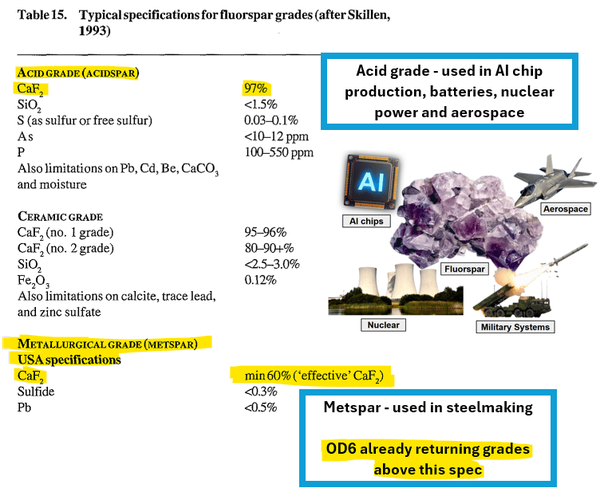

OD6 Metals (ASX:OD6)

This week our USA fluorspar Investment OD6 Metals (ASX:OD6) announced ultra high grades of fluorspar that could “support potential for Direct Shipping Ore (DSO)”...

... from surface, in and around the old open-pits that OD6’s historic mine was producing fluorspar from back in the 1950s in Nevada, USA.

Fluorspar is used in the production of missile systems, military electronics and jet fuel.

(not to mention an essential role in AI semiconductor chip production, batteries, nuclear power and aerospace)

The USA currently has no domestic supply.

For us, the key takeaway from today’s announcement is that, based on the 60%+ grades, OD6’s project COULD be at a spec high enough to sell directly into the metallurgical fluorspar market.

(called “metspar” - used in steel making).

That’s what OD6 means when it's saying “potential for direct shipping ore (DSO)”.

Meaning the material could be mined and shipped directly to a buyer.

So the grades today (from surface) are literally high enough that the ore could be dug out and shipped directly as an end product for steel making with minimal processing required.

Some quick back-of-the-napkin calcs - even just 100,000 tonnes of steel making fluorspar would be worth ~US$40M+ (more on these numbers in a second - and note these numbers are based on a bunch of assumptions we made, things can change so don’t treat them as gospel).

And the CAPEX wouldn’t be high because there is no processing (ie: no processing plant build costs).

OD6 Managing Director Brett Hazelden reckons this new development might enable OD6 to apply for a White House FAST41 application:

(source - today’s OD6 announcement)

A great potential nearer term cash flow source for OD6 while it works to fill the USA’s domestic supply gap of fluorspar for more “nationally strategic” use cases.

(military, AI, nuclear, aerospace and all that kind of stuff)

Fluorspar 101: Over 97% grade is known as ‘acidspar’. 60-96% grade is known as ‘metspar’.

(source)

OD6 is announcing today’s news into a market where the US government is actively looking for domestic fluorspar production to fill up its critical mineral stockpile.

That US critical mineral stockpile just happens to sit 300km from OD6’s project.

Read more: OD6 announces ultra high grade fluorspar in USA - high enough for direct shipping ore?

Iondrive (ASX:ION)

We think critical minerals recycling/processing tech companies could be the biggest winners from the east/west divide in critical minerals markets.

(and where the next big wave of capital is flowing to next in the US).

We expect to see more and more deals like the one from earlier this week - US$600M from the US Export Import Bank and Export Finance Australia for a rare earths refinery in WA.

Our exposure to the critical minerals recycling theme is Iondrive (ASX:ION).

ION is developing Deep Eutectic Solvents (DES) recycling tech (which it's also applying to critical minerals processing for mining companies).

It sounds complicated, but it's essentially just applying biodegradable, benign solvents to recover metals and critical minerals.

ION has an exclusive worldwide license for the technology developed by the University of Adelaide.

This week ION announced rare earths recovery rates (>90%) from its tech on ~250kg of end of life magnet materials - recovering neodymium (Nd) and praseodymium (Pr) the main inputs for rare earth magnets.

More on those results in a second - but first...

What’s happened with ION’s share price lately?

In November last year, ION raised $4M at 4.4c. We participated in this raise, alongside existing investors, well known institutions, and family offices on at least a pro rata basis, plus one new institution joining the register...

Since then the share price got as low as 1.6c, and is now at ~2.5c per share.

Why did the share price go down?

It’s our view that the market has recently punished ION for its lack of material news since the capital raise, especially considering the pilot plant being built was meant to be up and running early this year.

The markets are impatient and hate silence... ‘no news’ can be viewed as ‘bad news’ by the market.

Especially if there’s delays to previously communicated timelines for no reason.

That changed this week - ION delivered two material announcements and a new investor presentation... So is the quiet period now over?

ION is currently capped at $32M and had $8.4M cash at 31 December 2025.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Read more: ION: Critical Minerals recycling tech - punished for no news? Well it’s back now...

Haranga Resources (ASX:HAR)

Is the gold price about to go on a big run higher?

We think so... but don't actually know.

If it does (or even just stays at its current historic highs) - we think gold stocks with realistic pathways to producing gold bars in the near term will be the ones to run the hardest.

Companies like our Investment Haranga Resources (ASX:HAR) - trading at an enterprise value of ~$47M.

(Based on a market cap of $59M and its $12.4M cash held at 31 December 2025).

HAR is expecting THREE major share price catalysts in the next ~90 days.

The first TWO are from HAR’s 100% owned US gold project, sitting in the heart of California's legendary "Mother Lode" Gold Belt.

(This is the same region that triggered the original Californian gold rush in 1848-49.)

We like HAR’s project because it comes with permits and $90M of infrastructure in excellent condition (we went to visit the project site in California and saw it with our own eyes).

This kind of stuff can take years to do and lots of capital - meaning HAR theoretically can get into gold production much faster than if they were exploring a greenfields site in the middle of nowhere.

HAR’s bet was that IF they drill deeper below the historically mined areas...

AND find more gold...

THEN they can quickly restart the gold processing plant and start selling and producing gold while the gold price is at record highs.

This week HAR announced that the deeper drilling had almost finished - and just from eyeballing the drill cores it looks like they have hit gold bearing rocks.

Now we just wait for the assay results over the coming weeks (Major HAR catalyst #1).

HAR’s USA gold asset already has a VERY high grade (~286koz at 9.29g/t) non-JORC resource estimate, mostly based on drilling down to ~150m depths. (source)

But it's looking more and more like the resource potential on the project could grow to that 1M ounce mark (more on why we think that in the link below).

The SECOND major catalyst is a maiden JORC resource estimate at the project - potentially including these new drill results (Major HAR catalyst #2).

Why?

Because the project is supported by ~$90M of prior capital investment; including a processing plant (315ktpa), 880m long underground decline & development drives totaling 900m, workshops & offices and key operational permits in place.

So a defined JORC mineral resource estimate has a realistic pathway to being monetised with gold prices where they are.

Read more: HAR: 3 major share price catalysts in the next ~90 days.

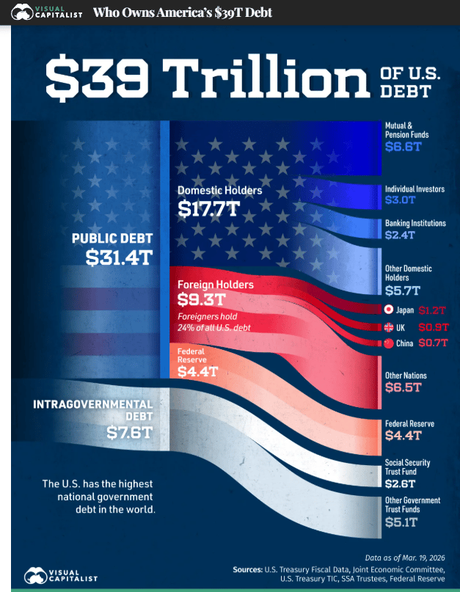

Visual Capitalist - posted the below graphic during the week showing just who holds US debt. When debts get out of control, the relative value of gold increases.

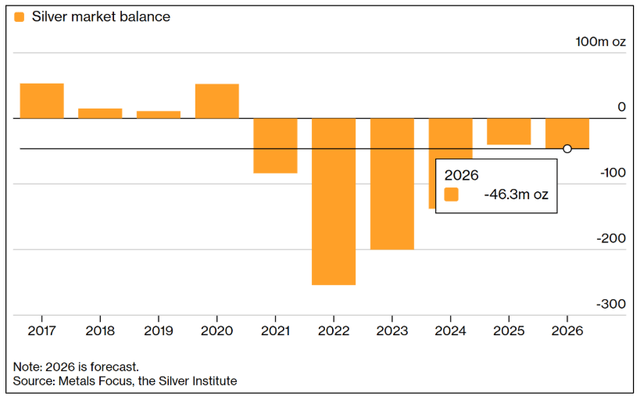

Bloomberg - The silver market is facing its sixth straight annual deficit, widening to 46.3M ounces as shrinking supply outpaces declining industrial demand amid heightened investor interest.

(source)

Kitco - China’s looming sulphuric acid export ban is threatening copper production, potentially triggering a silver supply squeeze by slashing the byproduct metal’s primary source during deficits.

Sulphuric acid is the lifeblood of copper mining. The heap leach process, dominant across Chile, Morocco, and Indonesia, works by pouring acid over crushed ore to dissolve the copper out. No acid could mean no copper.

Substack (Veronken) - An in depth piece by Veron Wickramasinghe, titled "The Tungsten Throttle" goes in depth into how China flexing (combined with a lack of planning elsewhere) has created a 775% price increase (so far), leaving Western defense and tech industries facing a structural deficit and a 2027 regulatory cliff.

So which part of the tungsten supply chain - defence, semiconductors, or industrial tooling - is going to be impacted most over the next 12 months?

RK Equity - released a “Battery Metals Review” report which goes from the raw materials in the ground right to the finished end product in use, a comprehensive overview of the dynamics at play:

Bloomberg - The US and Australia offered US$600M in financing for Tronox’s rare earths refinery, a key move under their minerals partnership to secure critical supplies for defence and technology from a “Western” source.

South China Morning Post - Brazil is demanding local rare earth processing, leveraging its massive ionic clay reserves to force technology transfers from the US and China amidst intensifying competition.

This could lead to government incentives through faster permitting, tax reductions and even funding opportunities to aid the development of production in country, which could be good for both of our Brazilian rare earth Investments SGQ and PNN.

X (@jeremie0117) from Aurelion Research went deep into the nickel market and thinks that a new bull cycle is possibly not too far away after a few years now of oversupply causing suppressed prices.

This would be great for our Investment NC1 should it play out this year, with drilling at its large nickel resource and a DFS to follow. The prior PFS showed it sat in the first cost quartile.

MTH - Exploring Mexico’s Sierra Madre Gold-Silver Trend - High Grade, Fully Funded and Ready to Grow - Ignite Investment Summit Hong Kong 15-16 April 2026

WCE - Elizabeth Hill Silver Project - Grade is King: Future growth and mine restart potential April 2026

ION - Urban Mining: Securing Supply Chains for Critical Minerals - IONSolv Critical Mineral Recovery Platform High-Value Recovery, Lower Environmental Impact, and Lower Capital Expenditure, Investor Presentation April 2026

SGQ posted this REE focused research report by Macquarie which includes an increase in the price target for SGQ from 20 to 26c.

Increasing price targets seem to be a common theme in the wake of recent rare earths rumblings and deals in the industry.

Caution: don't invest on analyst price targets alone, these numbers are based on a bunch of assumptions that could prove incorrect - yes even when the work is done by someone from a fancy bank.

Kaiser Reef, Brad Valiukas, Managing Director (ASX:KAU) presents at Gold Coast Gold March 2026

Viking Mines (ASX: VKA) advances Linka Tungsten Project with new studies

EIQ: AI Diagnostics, Mayo Clinic & Hypergrowth | Echo IQ (ASX:EIQ) | CWS Ep. 224

OD6 Metals (ASX: OD6) advances Quinn Fluorspar Project with strong results

RML: Watch: Resolution Minerals (ASX: RML) Highlights Major Scale Potential at Antimony Ridge

EXR: Elixir Energy | Stuart Nicholls on global energy conditions

AVM posted some pre drilling work preparation from on site at the Gavilanes silver project that will be drilled next:

SS1 posted a video update to LinkedIn which went through the progress and things to look forward to with study preparation now underway:

IVR MD Lachlan Wallace was in Hong Kong presenting at the Ignite Partners summit:

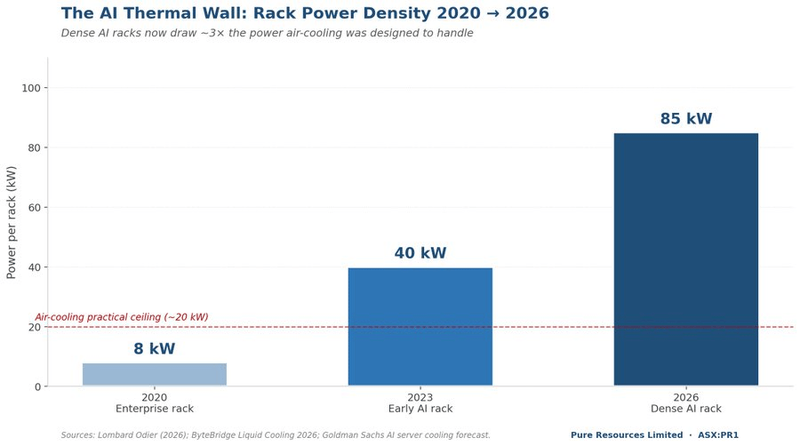

Our Recent Investment Pure Resources (ASX: PR1) posted this graphic to X, showing how heat is now a bottleneck for AI, which it is looking to solve:

A word of caution...

While we aim to highlight developments in the small cap space, investing in early-stage and small cap companies - like those we cover - is inherently risky.

These companies often face funding challenges, regulatory hurdles, and market volatility. Announcements may reflect aspirations more than guaranteed outcomes.

Things can, and often do, change.

Just because a company has signed a deal, released drill results, or appointed a new director doesn’t mean success is assured.

Always assume delays, cost overruns, or results that don’t pan out.

We’re here to share insights, not offer personal financial advice - so please do your own research and speak with a licensed adviser before acting on anything mentioned.

Follow us on social media: X, LinkedIn, Facebook

Bye for now.

Did someone forward this to you? Subscribe Here

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.