HAR: 3 major share price catalysts in the next ~90 days.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 7,803,780 HAR Shares at the time of publishing this article. The Company has been engaged by HAR to share our commentary on the progress of our Investment in HAR over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

Is the gold price about to go on a big run higher?

We think so... but don't actually know.

If it does (or even just stays at its current historic highs) - we think gold stocks with realistic pathways to producing gold bars in the near term will be the ones to run the hardest.

Companies like our Investment Haranga Resources (ASX:HAR) - trading at an enterprise value of ~$47M.

(Based on a market cap of $59M and its $12.4M cash held at 31 December 2025).

HAR is expecting THREE major share price catalysts in the next ~90 days.

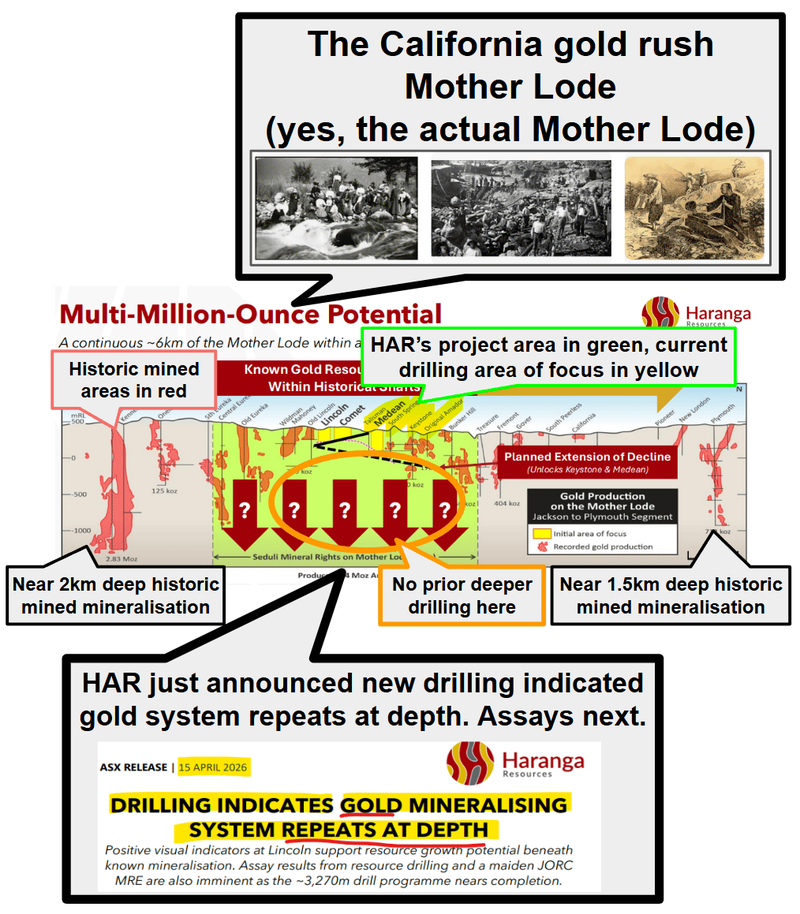

The first TWO are from HAR’s 100% owned US gold project, sitting in the heart of California's legendary "Mother Lode" Gold Belt.

(This is the same region that triggered the original Californian gold rush in 1848-49.)

We like HAR’s project because it comes with permits and $90M of infrastructure in excellent condition (we went to visit the project site in California and saw it with our own eyes).

This kind of stuff can take years to do and lots of capital - meaning HAR theoretically can get into gold production much faster than if they were exploring a greenfields site in the middle of nowhere.

HAR’s bet was that IF they drill deeper below the historically mined areas...

AND find more gold...

THEN they can quickly restart the gold processing plant and start selling and producing gold while the gold price is at record highs.

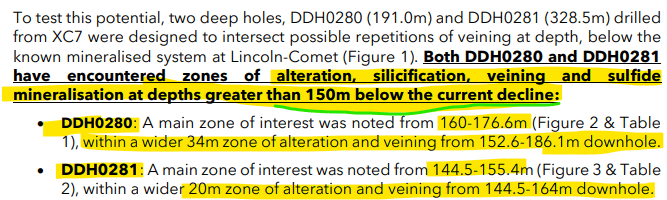

This week HAR announced that the deeper drilling has almost finished - and just from eyeballing the drill cores it looks like they have hit gold bearing rocks.

Now we just wait for the assay results over the coming weeks (Major HAR catalyst #1).

HAR’s USA gold asset already has a VERY high grade (~286koz at 9.29g/t) non-JORC resource estimate, mostly based on drilling down to ~150m depths. (source)

But it's looking more and more like the resource potential on the project could grow to that 1M ounce mark (more on why we think that later in today’s note).

The SECOND major catalyst is a maiden JORC resource estimate at the project - potentially including these new drill results (Major HAR catalyst #2).

Why?

Because the project is supported by ~$90M of prior capital investment; including a processing plant (315ktpa), 880m long underground decline & development drives totaling 900m, workshops & offices and key operational permits in place.

So a defined JORC mineral resource estimate has a realistic pathway to being monetised with gold prices where they are.

We went to California last year to see it with our own eyes:

(source - our full write up and pics from a site visit last year, see that here)

(more on all the US asset in a second)

What about the THIRD major catalyst?

It is on HAR’s Senegal gold project.

The one that nobody really cared about until HAR surprised the market (and probably even themselves) with high grade gold intercepts from surface from aircore drilling back in September last year.

The market certainly liked the drill hits from Senegal, pushing HAR’s share price from 8.6c to a peak of 25c around 2 weeks.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

This morning HAR announced a new drill campaign on this project, this time with a heavy RC Drill rig that can drill down to 300m deep.

Results of this drilling are HAR’s Catalyst #3.

That last round that delivered the market moving gold intercepts was all aircore and only down to max depths of ~85m.

This time with a heavier RC rig - drilling down to ~300m depths.

So with this morning's “just commenced” drilling in Senegal we should find out if HAR’s onto a larger gold system or if those previous hits were isolated pockets of high grade gold.

IF the drilling comes in, HAR could re-run the $2.4BN Predictive Discovery playbook in Africa again).

(drill aircore, hit high grade intercepts, follow it up with a heavier RC rig and declare a discovery)

Predictive was just involved in a “merger of equals” type deal, with a valuation of over $2BN (more on the similarities with Predictive in a second).

HAR at yesterday’s close traded with an enterprise value of ~$46.5M.

So in summary, within the next 90 days, HAR has catalysts across its two gold assets that we think could trigger a re-rate in its valuation to the upside:

- USA project: Assays from a 3,127M drill program - where it looks like two hail mary deep holes have hit the right type of rocks and COULD have hit repetitions to the gold we already know exists at the project.

- USA project: JORC resource estimate and drilling results coming from its US gold asset - that’s the project that has US$90M of infrastructure in place. AND

- Senegal Project: Results from HAR started drilling its gold asset with a heavy RC rig - following up on 20m high grade hits from last year.

We think that across its two assets - HAR is going into a period of newsflow where even if just 1 of the catalysts comes in, it could be a company maker for HAR.

Especially when its trading at an enterprise value of ~$48.5M (at 13c).

With the rest of today’s article we will do a deep dive on why we think the upcoming catalyst could be material for HAR:

- On the US asset - Why we think the JORC resource (and drill results) could be material.

- On the Senegal asset - How the drilling in Senegal could be HAR’s attempt at re-playing the $2.4BN Predictive Discovery playbook.

A JORC resource could allow the market to compare HAR to gold peers

We typically don't think of maiden JORC resources as a major catalyst for companies because usually, in the lead-up to a JORC resource, while a company is drilling, the market will re-rate a company (off the back of results) and then sell off into a JORC resource.

For HAR, we haven’t really seen the build up of expectations going into the maiden JORC resource.

Instead it looks to us like HAR’s been caught up in fear selling from all of the geopolitical uncertainty (and a short correction in gold prices):

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

We think that IF HAR can define a resource at or above the level of its non-JORC 286k ounce (source) it will allow for comparisons with peers that have similar resources.

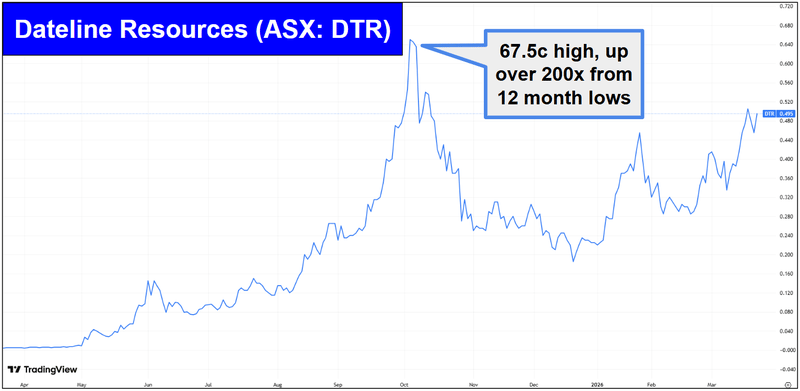

We have used this example before, but the big US gold peer is Dateline Resources.

Dateline has been in the media for its rare earth potential but its Colosseum project in California is in fact, primarily a gold project.

Dateline’s project has a 1.1M ounce gold resource estimate with the project at the Bankable Feasibility Study stage. (Source)

Unlike HAR, Dateline has no infrastructure on site and no permitting in place.

HAR’s project is an underground high grade project, whereas Dateline’s is a bulk tonnage open-pit deposit.

AND the average grade of Dateline’s resource is 1.26g/t. (source)

HAR’s non-JORC resource is 286k ounces but the grade at 9.29g/t gold is over 7X Datelines at 1.26g/t gold.

Haranga is currently capped at $59M, Dateline is currently capped at $1.4BN.

(Source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

It’s almost impossible to find comparisons to HAR’s project because that 9.29g/t average grade is pretty ridiculous.

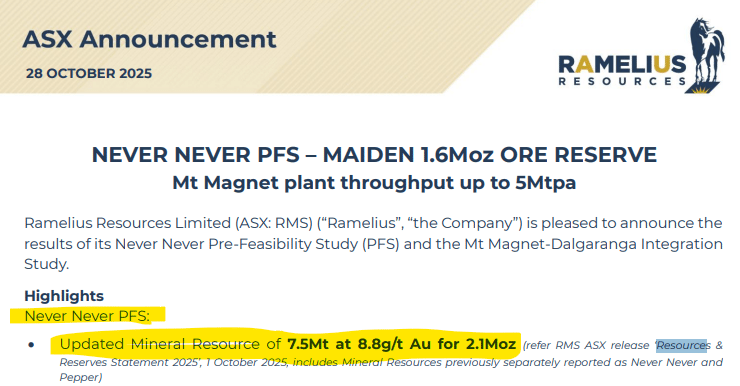

But one is the Never Never discovery that Spartan Resources made a few years ago.

That deposit had an 2.1m ounce resource with an average grade of 8.8g/t gold - and it was eventually taken out in a deal worth ~$2.4BN by Ramelius Resources. (source)

(source)

In terms of ounces another one is ASX listed Torque Metals which has a 250k ounce gold resource with an average gold grade of ~3.1g/t gold (similar ounces to HAR’s non-JORC resource, but 1/3rd of the grade).

Torque is currently capped at $330M.

IF HAR can define even 500k ounces - with all of the infrastructure in place it could start to draw comparisons to its project and the likes of Dateline, Spartan’s discovery and Torque...

Especially because of its grade profile because higher grades usually mean:

- More gold per tonne processed (obvious, but the economics compound quickly)

- Lower cost per ounce produced (you move less rock for the same amount of gold)

HAR’s market cap right now is $59M.

And let's not forget - HAR’s project also comes with:

- ~A$90M of sunk infrastructure** built by previous owners

- A 100% owned and permitted 350,000tpa gold processing plant (last operated in 2022)

- An 880m underground decline

- Offices, workshop, and laydown yard

- AND a Conditional Use Permit that allows production of gold

We saw all of this with our own eyes when we visited the project last year and we were positively surprised by the condition of everything - when we hear “historically producing gold mill” we generally think of rusty ball mills, timber frames and broken rail tracks.

(source - our pics from a site visit last year, see that here)

While other companies need to think about building processing equipment from scratch.

HAR’s project would have a “faster to market” edge relative to most other ASX explorers/developers on the ASX that are drilling out their projects.

All we need to see now is how big HAR’s resource is when the JORC resource comes out (expected later this month).

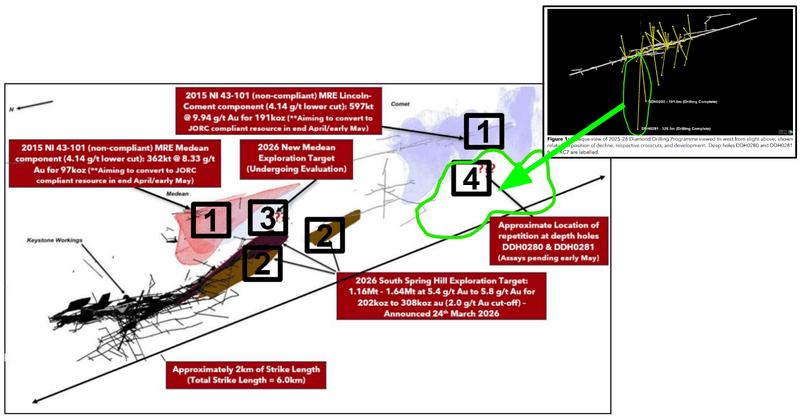

As it stands, HAR has:

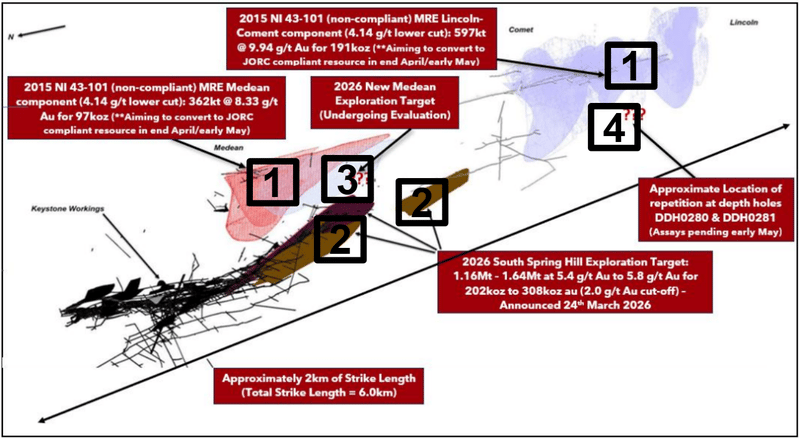

- Its existing non-JORC 288k ounce gold resource (the red and purple sections in the image below)

- The ~308k ounce exploration target sits at the "South Spring Hill" target

- A new exploration target coming from, AND

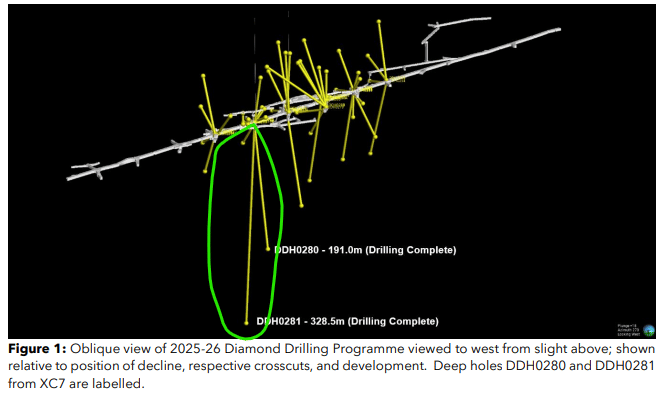

- The biggest ones - HAR's drilling could be hitting repetitions to the non-JORC resource at depth with holes 280 and 281 AND all of the work done so far is only across ~2km of strike (whereas the project covers ~6km of strike).

There is almost 600k ounces there already in non-JORC resources and an exploration target.

BUT, the main thing that caught our attention on that project was the two hail mary holes (#280 and 281).

HAR really went for it with those two - drilling beyond the 150m depth extent of the projects current resource:

(source)

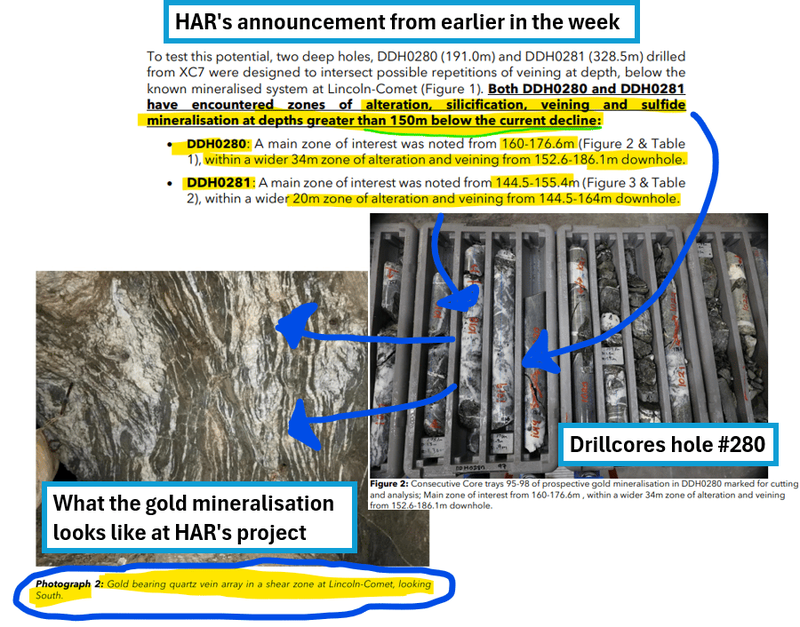

And in the announcement HAR said it hit “zones of interest” over 34m in hole 280 and ~20m in hole 281:

(source)

Looking at the drillcore in that announcements it looks like HAR’s in the right type of rocks too:

(fingers crossed those “quartz veins” are full of gold)

IF it is, HAR could be hitting repetitions to its current ~281k ounce non-JORC resource well below the ~150m depths that number was based on:

(source)

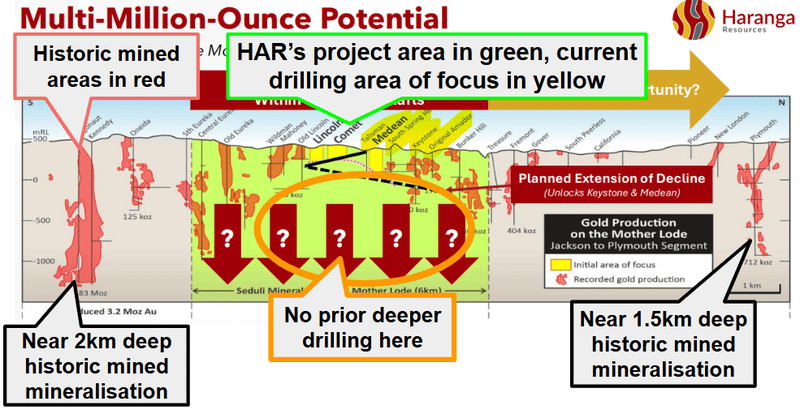

The thing with the US asset is that there is still so much of the project left to drill - some mines in the area run down to ~2km depths and HAR has over 6km of strike to test...

So, who knows how much more gold HAR finds when it tests the rest of its project.

Here is the image we always refer back to to get a sense of the exploration upside on the project:

(source - HAR presentation November 2025)

We did a deep dive on how big we think the resource could get in our last note here: HAR: Going for fast, high grade gold production in the USA - gold’s wild ride continues.

How about in Senegal - can HAR repeat the $2.4BN Predictive Discovery playbook?

As mentioned earlier, the second major catalyst for HAR could come from its Senegal asset.

HAR’s big hit from this asset was hole #8 back in October 2025 which hit 20m at 6.54g/t gold and quickly captured the market's attention.

That first batch of results were strong enough for HAR to go straight into a second shallow round of drilling.

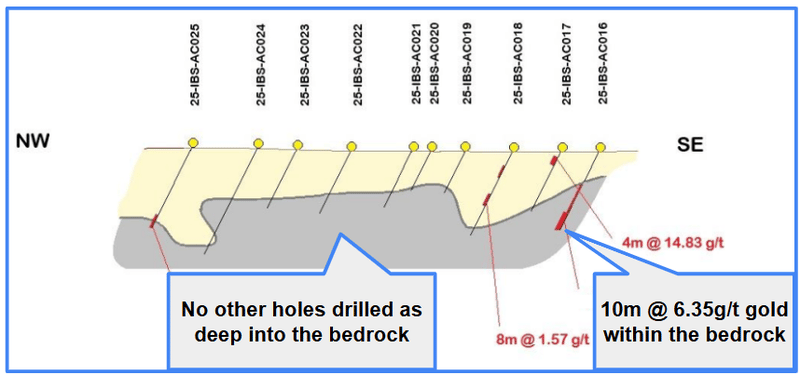

And now we know there is ~800m of strike to test with a fair few holes that ended in mineralisation.

Here is a cross-section of one hole that ended in mineralisation “within bedrock”:

(source)

All of the drilling so far has been holes down to ~20-85m depths.

Today the main event started - the deeper RC drilling testing down to depths of “260 to 300m”.

With this program we should find out if HAR accidentally made a big new gold discovery, OR if the results from back in October were isolated pockets of high grade gold.

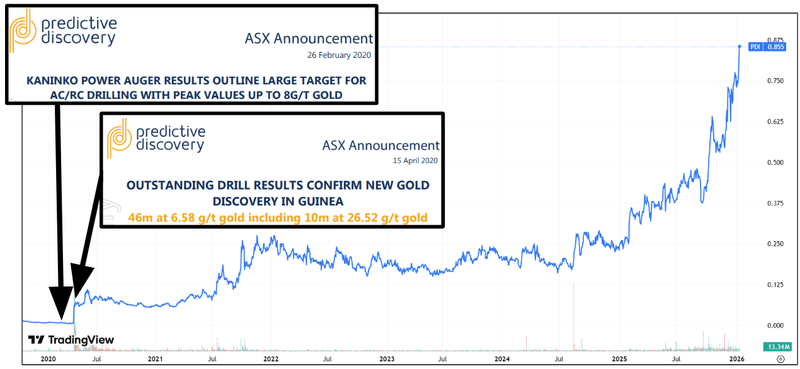

We think HAR is now in a similar position to where $2.3BN Predictive Discovery was when it made its discovery back in February 2020.

Predictive’s asset ended up a 4.9M ounce discovery and took the company’s share price from 0.6c per share to 85c per share.

The ultimate win for HAR in Senegal would be a “Predictive Discovery style” major gold discovery.

So far HAR has followed the Predictive story pretty closely.

Predictive drilled a few aircore holes with low expectations, hit high grade gold, followed it up with RC drilling and ~5 years later it’s capped at ~$2.3BN.

Predictive hit gold in shallow aircore holes, and the market didn’t really react to the news.

Then, when the deeper holes came back with gold and a discovery was declared, Predictive's share price started running.

Predictive is the most obvious comparable success story to what a big, outsized win for HAR could look like here. No guarantees of course.

(Source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

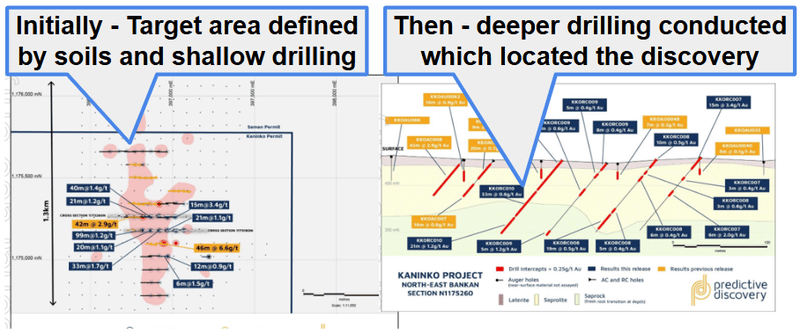

With HAR’s next round of drilling being the one that will make or break this project we went back and looked at how Predictive’s discovery evolved in the very early days.

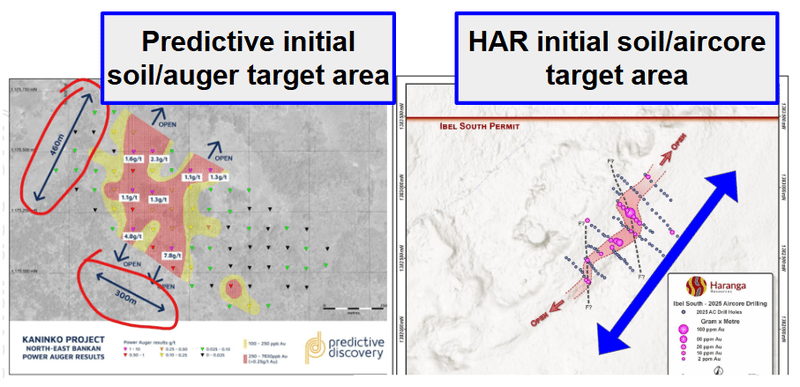

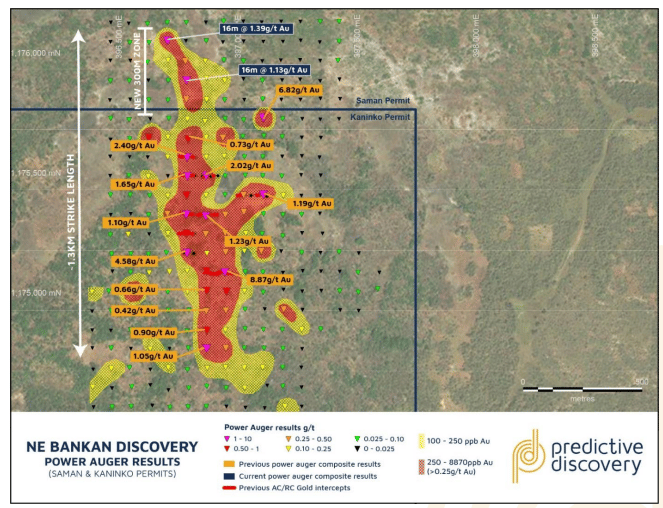

The Predictive announcement from 26 February 2020 was when we got a first look at the extent of gold structures (from shallow auger drilling) - similar to what HAR has defined so far.

Here is what Predictive had in February of 2020, and what HAR has now side by side:

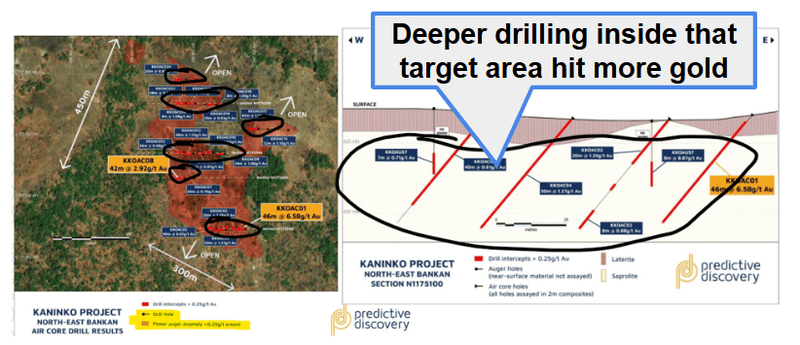

Then a few months later, Predictive followed up with deeper holes along that area that the shallow drilling had defined (they literally drilled below those shallow gold targets):

(source)

The deeper drilling opened the door to a big capital raise for Predictive, who then did some more shallow auger drilling - defined the big Bankan structure over ~1,300m by July 2020:

(source)

Then came the deeper drilling into that expanded target area - which is when the market started to really take the discovery seriously.

(source)

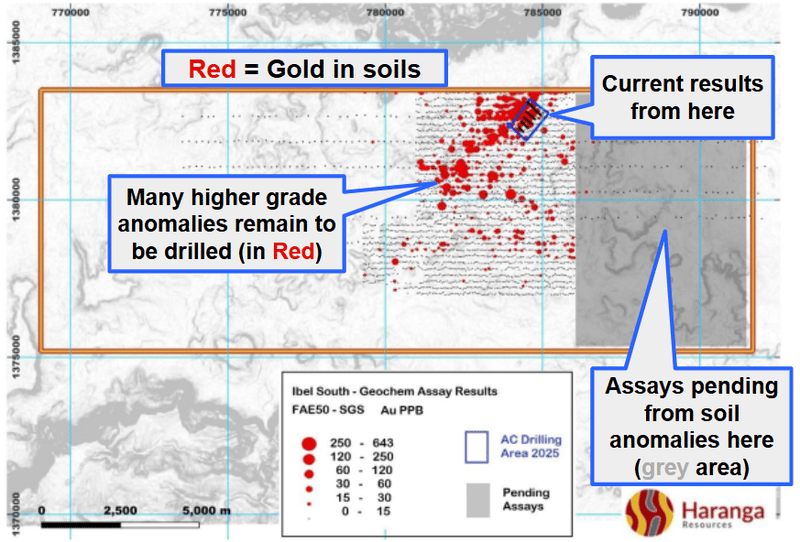

HAR’s got its 800m gold in termite mound soil anomalies - confirmed by shallow aircore drilling.

And the area that’s been drilled so far only makes up a small fraction of the ~5km area with gold in soils across the project:

(source)

These early results could be the makings of a big discovery - or it could go nowhere.

What we do know is that often big discoveries are made when no one expects anything to happen (that’s exploration for you 🤷♂️).

The deeper drilling (IF it comes in - no guarantees of course) just like Predictives did between February & April 2020 could be what sets up HAR to go off and test the rest of the project.

And that drilling started today...

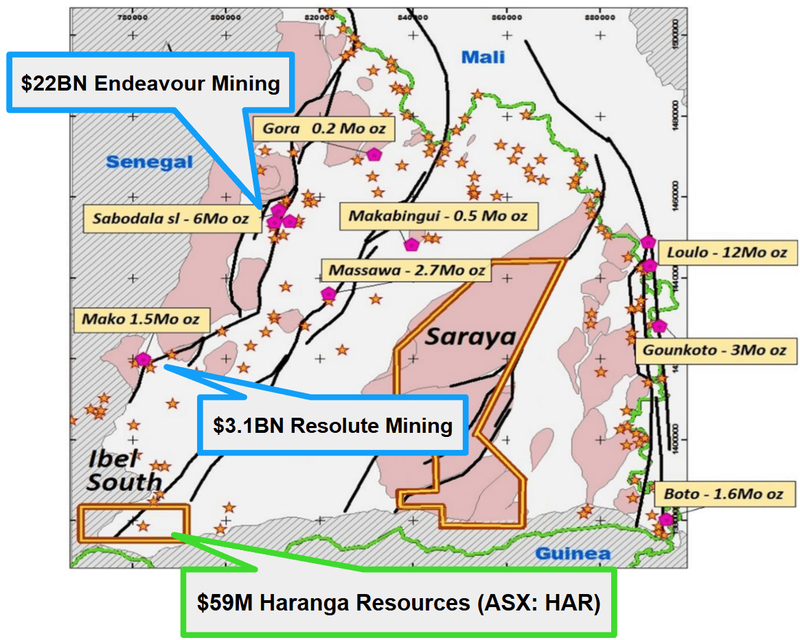

IF HAR can find anything remotely valuable, then it is also in a part of the world where it could attract attention from much larger-cap peers too.

HAR’s project sits in an area with some big operating mines including projects owned by $22BN Endeavour Mining and $3.1BN Resolute Mining.

(The region has a few other gold discoveries too, so it's not in the middle of nowhere).

So a big discovery from HAR here could very easily bring with it corporate attention (if the early results haven’t already).

(source)

Ultimately, success at either of HAR’s projects could be what helps the company achieve our Big Bet as follows.

Our HAR Big Bet:

“HAR re-rates to a market cap greater than $200M by making new gold discoveries in California and progressing towards production or is acquired at a multiple of our initial entry price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our HAR Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

What's Next for HAR?

🔄 Maiden JORC resource estimate (due end of April/earlry May)

We want to see HAR convert its ~286koz non-JORC gold resource estimate into JORC compliance.

HAR's latest update confirmed the 3,270m drill program was "nearing completion" and prior to this, that the program had been expanded from 30 holes to ~40 holes (for a total of ~3,270m).

HAR expects assay results from drilling during April and a maiden JORC resource estimate by early May.

As mentioned earlier, we are especially looking forward to results from those two holes drilled at depth (hole 280 and 281).

(source)

Here are the milestones we are tracking for the US asset:

- ✅ Drilling commenced (December 2025)

- ✅ Drilling expanded to 40 holes / 3,270m

- 🔄 Drilling at XC7, XC8 drilling (XC8 drilling nearly complete)

- 🔄 Assay results ("imminent")

- ⬜ Maiden JORC Mineral Resource Estimate (Expected by early May)

- ⬜ Deep hole to test at depth

🔄 Senegal gold - deeper drilling

HAR is now drilling its asset in Senegal with a deeper RC rig.

As mentioned earlier, here we are hoping that previous hit (20m @ 6.54 g/t gold from just 12m depth) can be followed up and proven as part of a larger gold system.

Here are the milestones we are tracking for the Senegal asset:

- ✅ Drilling started

- 🔄 Assay results

- ⬜ Decision to come back and do more drilling

See our most recent coverage of the Senegal asset here: HAR: 800m of continuous gold mineralisation - deeper drilling to start this quarter

What Could Go Wrong?

The near-term risk for HAR is exploration risk and resource risk.

There is no guarantee that the current drilling at HAR’s US asset finds economically viable gold mineralisation.

There is also a risk that the current drilling fails to confirm the historic results - which could mean HAR delivers results well below the market's expectations.

IF that were to happen, we would expect HAR’s share price to re-rate lower.

Exploration risk

There is no guarantee that HAR's upcoming drill programs are successful and HAR may fail to find economic gold deposits.

Source: "What could go wrong" - HAR Investment Memo 25 June 2025.

Another risk is the volatility in the gold price.

When the markets are experiencing peak fear, gold prices can sometimes suffer.

IF the gold price were to fall enough, then we would expect it to impact HAR’s share price.

Resource risk

Currently, HAR’s US based project has a “foreign resource estimate”. This means it used a different set of assumptions & guidelines compared to the JORC standards we are required to see on the ASX. There is no guarantee that HAR will convert all of its foreign resources into a JORC resource. If this risk were to materialise, it may have a negative impact on the company's share price.

Source: "What could go wrong" - HAR Investment Memo 25 June 2025.

Other risks

Like any early-stage exploration company, HAR carries significant risk, here we aim to identify a few more risks.

A major part of the HAR story is the high-grade historical resource in the USA, but there is always a chance that modern JORC standards don’t confirm those older numbers.

If the upcoming maiden resource estimate comes in lower than the non-JORC figures, it could lead to a negative re-rating of the share price.

In Senegal, the company is moving from shallow aircore hits to deeper RC drilling to see if a massive gold system exists deeper.

There is a risk that these deeper holes fail to replicate the high grades, which would suggest the previous hits were in isolation.

While HAR reported a healthy cash balance at the end of 2025, aggressive drilling programs in two countries consume capital very quickly.

This high cash burn means the company may eventually need to raise more funds, which could result in further shareholder dilution.

As a gold-focused explorer, HAR’s valuation is also highly sensitive to the global gold price and general market sentiment toward junior miners.

Even with great drill results, a significant drop in the gold price would likely put downward pressure on the share price.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our HAR Investment Memo

Our Investment Memo provides a short, high-level summary of our reasons for Investing.

We use this memo to track the progress of all our Investments over time.

Click here to read our HAR Investment Memo where you will find:

- What does HAR do?

- The macro theme for HAR

- Our HAR Big Bet

- What we want to see HAR achieve

- Why we are Invested in HAR

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.