WCE drilling now underneath highest grade silver mine in Australia

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 3,908,000 WCE Shares at the time of publishing this article. The Company has been engaged by WCE to share our commentary on the progress of our Investment in WCE over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

Between May last year and January this year, silver went on an epic run from US$35 to US$120 per ounce.

In that same period our Investment West Coast Silver (ASX:WCE) went from 5c to a high of ~29c per share.

Silver is currently trading at US $76 per ounce, and WCE is trading at 18c/share.

We think the silver price is going to run again, even higher than before (this is our opinion - we could be wrong).

Silver has spent the last two months putting in a new base a full 50% higher than its two previous all time highs of ~US$49 in 1980 and ~US$50/oz in 2011.

The past performance is not an indicator of future performance.

WCE just started diamond drilling beneath its historical WA silver mine today.

WCE’s Elizabeth Hill silver mine holds the record for the highest grade silver mine in Australia, ever.

WCE’s current drilling campaign is for 1,500m over six holes, and is the first test of deeper mineralisation below the historical high grade mine.

(plus WCE still has ~20 regional Elizabeth Hill look-a-likes to drill - to also try and find a whole NEW Elizabeth Hill style deposit nearby)

Zooming out by about 50 years, we think the silver price is settling at a level above two of the previous generational bull runs - so we think that even sideways trading could be a trigger for the next run in silver stocks:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

And in an ideal world, the start of the rally coincides with drill results from WCE - next quarter.

(keeping in mind, the world is rarely ideal)

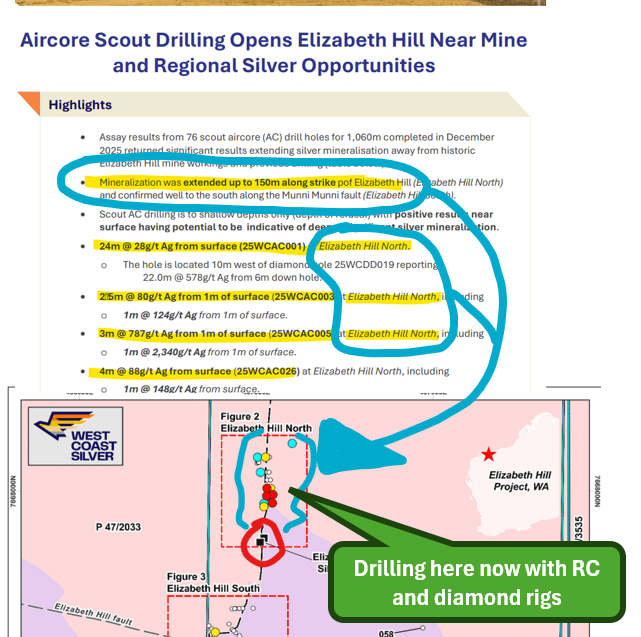

WCE is drilling now with two rigs at its 70% owned Elizabeth Hill Silver mine in WA.

As we mentioned above, WCE’s Elizabeth Hill mine was once the highest-grade producing silver mine in Australia.

It produced ~1.2 million ounces of silver (US$88M in silver at today's prices) from just 16,830 tonnes of ore at a head grade of 2,194g/t silver.

(Nowadays, even just 100g/t is considered “very high grade”)

Mining stopped in 2000 when silver dropped to US$5 per ounce...

Today’s prices of above US$75 / ounce are a VERY different story.

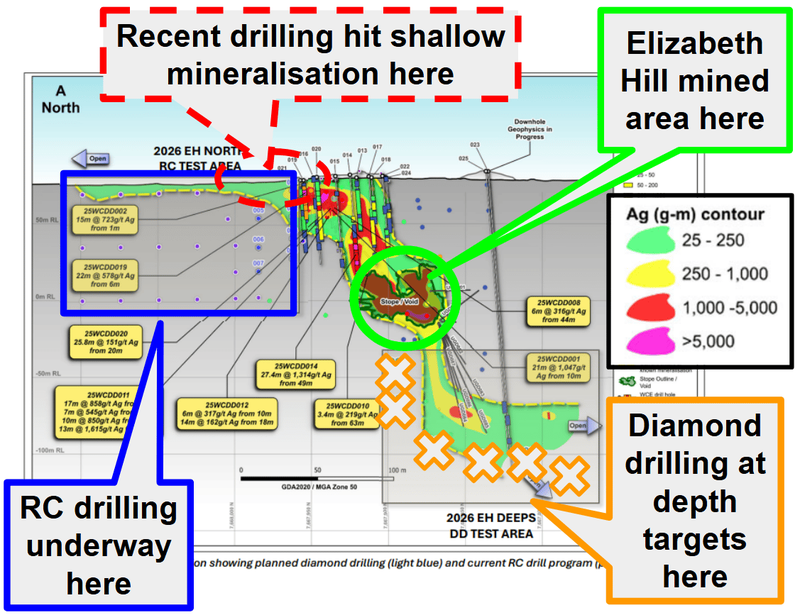

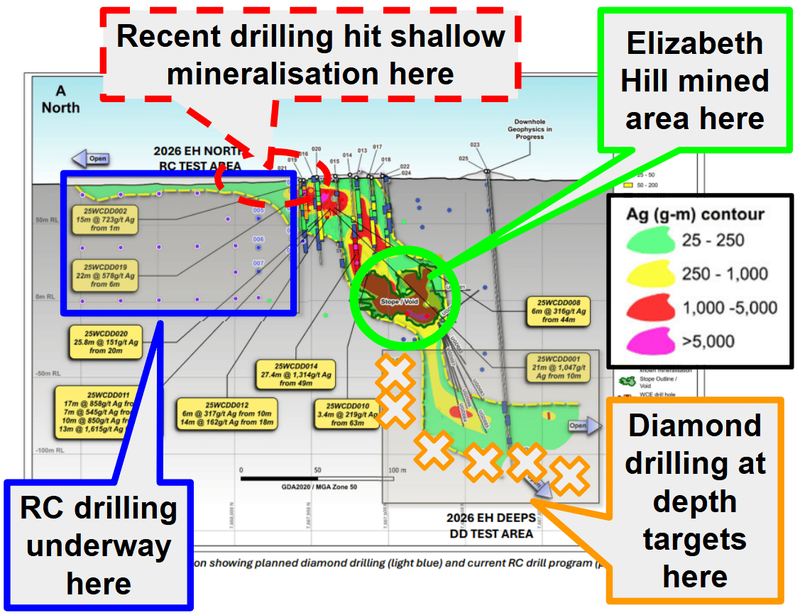

And as of today, WCE is drilling below and to the north of that same mine:

- 4,000m of RC drilling - testing extensions to the north of the old workings, AND;

- 1,500m of diamond drilling - testing extensions at depth to the old workings.

(source)

When we first Invested in WCE - the two main things we wanted to see were:

1. source). Then finding a way to put the asset back into production while the silver price is high. WCE drill around the old mine workings, trying to find extensions to the old remnant resource of ~46.8kt @ 2,700g/t silver for 4.05Moz (

AND

2. Find an Elizabeth Hill repeat by making an entirely new discovery nearby.

The current round of drilling is mainly focusing on point 1.

IF WCE can extend the old 4.05Moz remnant resource (especially near surface), then it could start to bring forward a fast to production strategy on the project.

(Replicating the mining runs the project has delivered in the past)

Small tonnages of ore, but very high grade silver - leveraging existing infrastructure in the area.

(WCE is currently in discussions with a nearby mill owner too - more on that in a second).

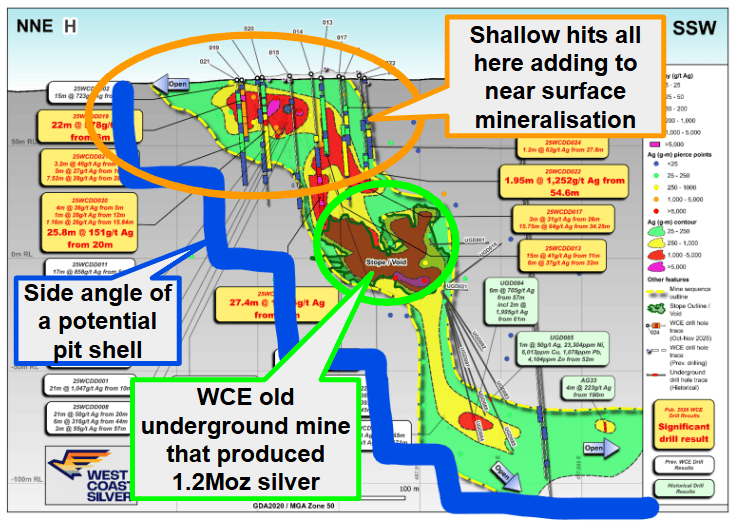

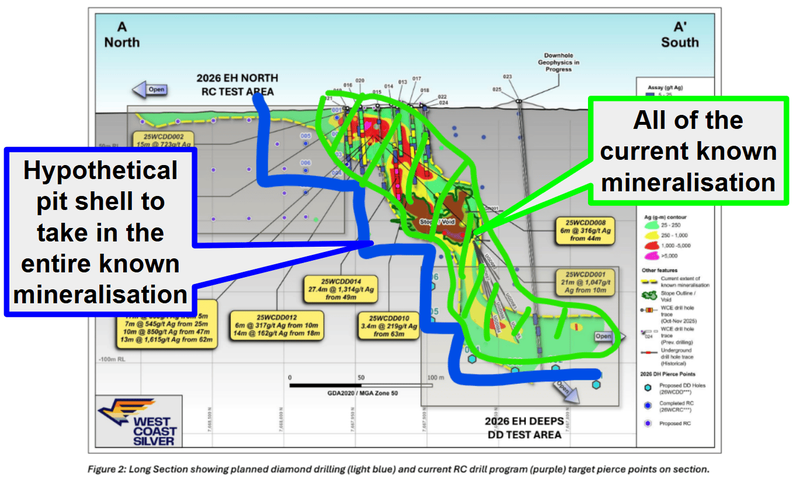

With last year’s drilling, WCE added weight behind a potential open-pit development scenario for WCE’s project, which we did a deep dive on in a previous note here.

We tried to visualise what an open pit scenario would look like - see the thick blue lines below. But we are not mining engineers, and this may not even be possible. There’s more work to be done to establish what a mining scenario would look like.

(source)

Then, with some aircore drilling straight after, last year WCE also added a bunch of regional targets where it can look for Elizabeth Hill repeats.

At the moment, WCE has ~20 of those regional targets defined - most of which have never been drilled before (more on the regional targets in a second).

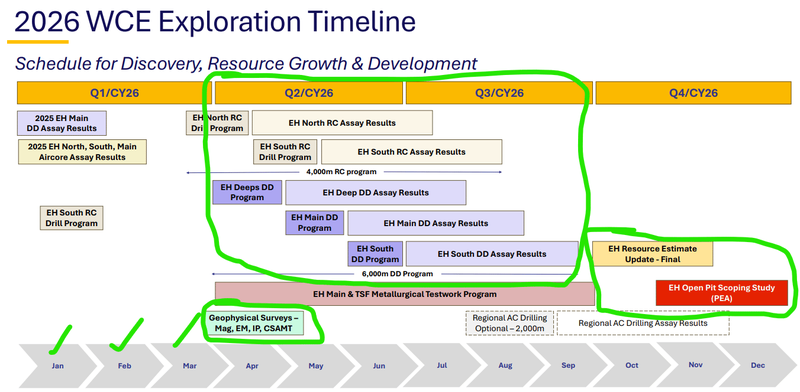

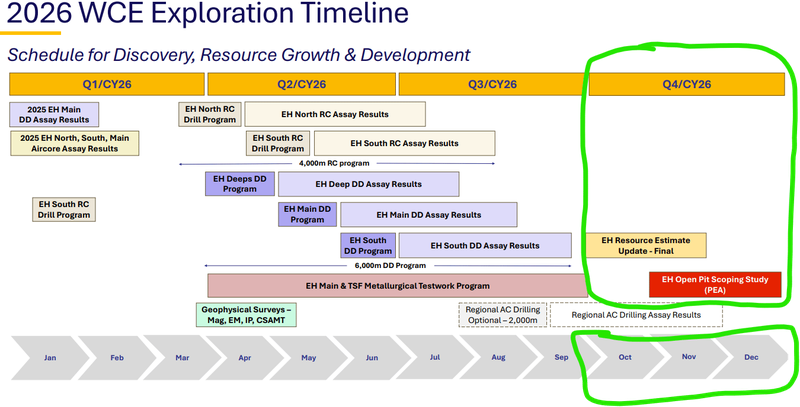

For now, the focus is on the 6 diamond holes WCE will be drilling (testing for at-depth extensions at the old mine) AND the 4,000m of RC drilling to hunt for extensions to the north.

Here is that summary image again of the areas WCE is targeting:

(source)

After that, in Q4 WCE plans to put a maiden JORC resource estimate out on the project - hopefully larger than that remnant resource.

And then roll all of that data into a scoping study for an open-pit mining scenario on the project in Q4.

(source)

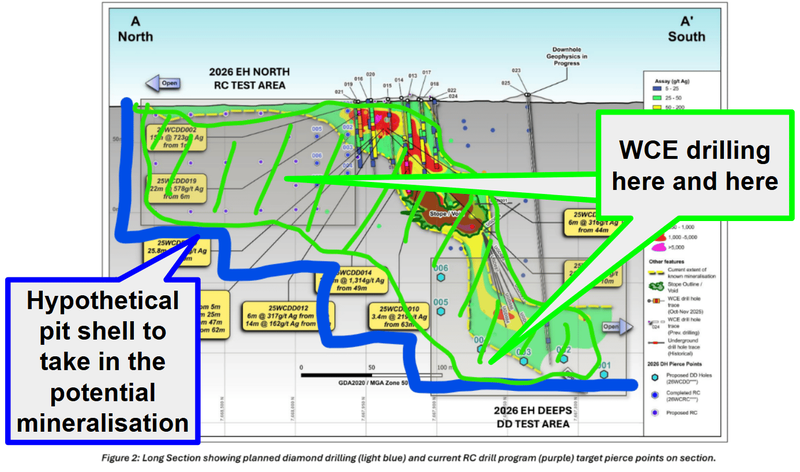

A win for us would be IF this round of drilling changes the potential open-pit mining scenario from this (here’s another crayon drawing of what it could look like):

(source)

To something like this:

(source)

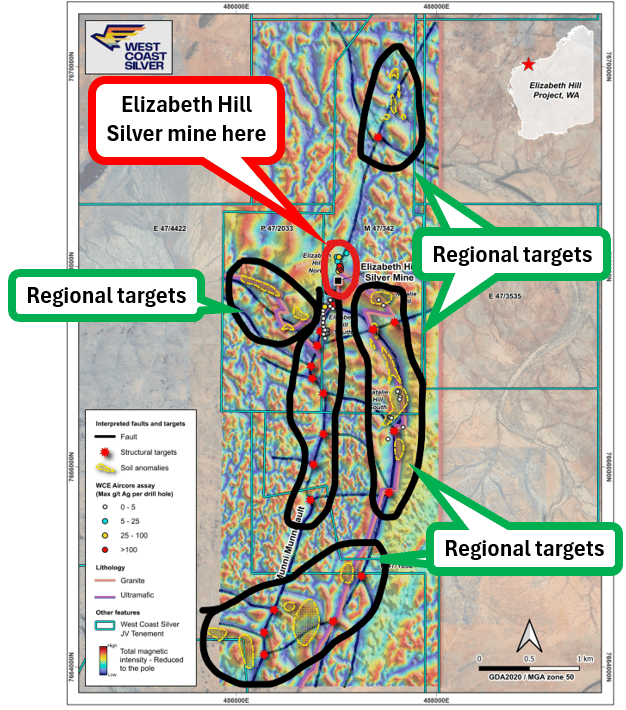

Then there are WCE’s regional targets we mentioned earlier.

WCE still has ~20 regional Elizabeth Hill “look-a-likes” to drill test

WCE’s project area sits on over a 180km2 area - most of which hasn’t been touched in decades.

(source)

WCE has so far run geophysical surveys (drone magnetics, transient electromagnetics and surface sampling), with these results coming back in October.

This narrowed down the existing ~20 targets to seven higher priority, near mine targets that span across ~2km of strike. (source)

Here are all the targets WCE has defined along trend from the old Elizabeth Hill mine:

(source)

One of the main reasons we Invested in WCE was because we think the company could make repeat discoveries similar to Elizabeth Hill.

Here is one of the key reasons we listed in our initiation note back in August 2025:

Reason #8: Regional targets ranked, exploration starting soon

There is very limited modern exploration over WCE’s regional targets. WCE just identified ~12 high priority and 8 earlier stage regional targets. These are the targets where we are hoping to see a repeat of the high grades at Elizabeth Hill. Air-core/channel sampling to start on these very soon.

Source: “Why did we Invest in WCE” - WCE Investment Memo 2025

WCE has already run geophysics across the broader project area.

And then run its first shallow aircore program ( looking for spots of mineralisation that warrant coming back in with a heavier rig).

The first batch of results from that program were announced in February - hitting silver to the north of the Elizabeth Hill silver mine.

(source)

And now, WCE has the heavier rigs in (RC and diamond) - testing those targets to see if it can (in this case) extend the old mine workings to the north and at depth.

WCE expects to be drilling all the way through to May, with assays coming out over the coming months.

So we should know whether or not WCE’s exploration upside plays out or not.

Ultimately, we think any discovery or operation resembling the old high grade Elizabeth Hill mine could re-rate WCE’s valuation higher from where it is today, which forms the basis for our WCE Big Bet.

Our WCE Big Bet:

“WCE re-rates to a market cap of $300M by bringing the Elizabeth Hill mine back online OR making a new discovery that is as big (if not bigger) than Elizabeth Hill into a strong macro silver theme.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our WCE Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

What we want to see next from WCE

In early April, WCE released an updated presentation here.

It’s always good to see a Gantt chart showing what’s ahead in these presentations - a one pager on what to expect next.

(source)

The three things we are most looking out for are:

- The RC drill campaign on the targets to the north of the Elizabeth Hill Mine (happening now).

- The diamond drilling going for at depth extensions to the Elizabeth Hill mine (started today).

- Geophysics across the broader project area

And then all of that data rolling into a JORC resource and scoping study before the end of the year.

What could go wrong?

In the short term the key risk is around “exploration risk” and “commodity price risk”.

WCE is currently drilling surrounding the historical mine. There is a risk WCE does not find enough economically viable mineralisation and the company’s share price re-rates lower.

Exploration risk

There is no guarantee that WCE’s upcoming drill programs are successful. WCE may fail to find economic deposits of silver.

Source: What could go wrong? - WCE Investment Memo 8 August 2025.

Right now, the silver price has pulled back significantly from its all time highs earlier in the year.

WCE’s primary commodity exposure is silver, so any further falls in the silver price could mean WCE’s share price moves lower.

Commodity price risk

The performance of commodity stocks are often closely linked to the value of the underlying commodities they are seeking to extract. Should silver prices fall, this could hurt the WCE share price.

Source: What could go wrong? - WCE Investment Memo 8 August 2025.

Other risks

Like any small-cap exploration company, WCE carries significant risk, here we aim to identify a few more risks.

A major near-term risk for WCE is the transition from a historic remnant resource to a modern JORC-compliant resource estimate.

The historic grades at Elizabeth Hill were incredibly high, but the resource is a "remnant", which means that the easiest, highest-grade ore has already been mined.

There is a high statistical probability that the current diamond and RC drilling fails to replicate those bonanza grades or define sufficient tonnage to support a modern open-pit operation. If the maiden JORC resource estimate disappoints the market, it would likely cause a sharp negative re-rating of the share price.

Furthermore, the narrow-vein, high-grade nature of the historical Elizabeth Hill deposit can be notoriously difficult to mine efficiently on a larger scale. So if the proposed scoping study reveals that the cost of extracting this ore (either via open pit or a restarted underground decline) is higher than anticipated, the project may be deemed uneconomic even at current silver prices.

Executing 5,500m of combined diamond and RC drilling, running geophysical surveys, and producing a scoping study will result in a relatively high cash burn for WCE.

If these don’t deliver good drill results or WCE is unable to secure a proposed toll-treating agreement with a nearby mill owner, it will likely need to tap equity markets in the near term to fund ongoing development. Any future capital raises will likely result in dilution for existing shareholders.

Finally, while WCE has ~20 regional targets defined, exploring for new, distinct "Elizabeth Hill look-a-likes" across a 180km2 area is high-risk, greenfield exploration. There is no guarantee that any of these regional targets host economic silver mineralization.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our WCE Investment Memo

In our WCE Investment Memo, you can find the following:

- What does WCE do?

- The macro theme for WCE

- Our WCE Big Bet

- What we want to see WCE achieve

- Why we are Invested in WCE

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.